|

GMA711S-MANAGEMENT ACCOUNTING 310-2ND OPP- JULY 2025 |

|

|

1 Page 1 |

▲back to top |

nAmlBIA UnlVERSITY

OF SCIEnCE Ano TECHnOLOGY

FACULTY OF COMMERCE, HUMAN SCIENCES AND EDUCATION

DEPARTMENT OF ACCOUNTING, ECONOMICS AND FINANCE

QUALIFICATION: BACHELOR OF ACCOUNTING

QUALIFICATION CODE: 07BGAC LEVEL:?

COURSE CODE: GMA711 S

COURSE NAME: MANAGEMENT ACCOUNTING 310

SESSION: JULY 2025

PAPER: THEORY AND CALCULATIONS

DURATION: 3 HOURS

MARKS: 100

SECOND OPPORTUNITY EXAMINATION QUESTION PAPER

EXAMINERS Lameck Odada; Moses Nyakuwanika and Labanus Nashinwe

MODERATOR Alfred Makosa

INSTRUCTIONS

1. Answer ALL the questions in blue or black ink only. NO PENCIL

2. Start each question on a new page and number the answers correctly and clearly.

3. Write clearly and neatly, showing all your workings/assumptions.

4. Round off only final answers to two (2) decimal places

5. Questions relating to this examination may be raised in the initial 30 minutes after the start

of the examination. Thereafter, candidates must use their initiative to deal with any

perceived error or ambiguities, and any assumptions the candidate makes should be

clearly stated.

·

PERMISSIBLE MATERIALS

1. Silent, non-programmable calculators

THIS QUESTION PAPER CONSISTS OF _5_ PAGES (including this front page)

|

|

2 Page 2 |

▲back to top |

QUESTION 1

[25 MARKS]

iTechArt has been the partner of choice for fast-growing start-ups and innovative companies

since 2002, providing fully dedicated engineering teams and custom software solutions. The

company is divided into Divisions that provide services to each other and also to external

clients. The performance of the Divisional Managers is measured against profit targets that

are set by central management.

In May 2024, the Consulting Division undertook a project for HP Enterprise. The agreed fee

was N$15 500, excluding data processing, and the costs were N$2 600. The data processing,

which needed 200 hours of processing time, was carried out by the Data Processing (DP)

division. An external agency could have been used for data processing, but the DP division

had 200 chargeable skilled hours available in May 2024. The DP division provides data

processing services to the other divisions and also to external customers. The budgeted costs

of the DP division for the year ending 31 December 2024, which is divided into 12 equal

monthly periods, are as follows:

Variable costs

Skilled labour (6000 hours worked)

Semi-skilled labour

Other processinQ costs

Fixed costs

N$

120 000

96 000

60 000

240 000

These costs are recovered on the basis of chargeable skilled labour hours (data processing

hours) which are budgeted to be 90% of skilled labour hours worked. The DP division's

external pricing policy is to add a 40% mark-up to its total budgeted cost per chargeable hour.

During May 2024, actual labour costs incurred by the DP division were 10% higher than

expected, but other costs were 5% lower than expected.

REQUIRED

MARKS

Calculate the total transfer value that would have been charged by the DP 13

division to the Consulting division for the 200 hours on its HP Enterprise

project using the following bases:

a)

i. Actual variable cost.

ii. Standard variable cost + 40% mark-up.

iii. Market price

Prepare statements to show how the alternative values calculated in 12

b) answer to requirement (a) above would reflect in the performance

measurement of the DP division and the Consulting division.

1

|

|

3 Page 3 |

▲back to top |

QUESTION 2

[25 MARKS]

Northern Atlantic Fishing (NAF) is considering the acquisition of a vessel to boost its vessel

fleet for its coastal operations in Namibia in 2025. A Dutch ship manufacturer quoted a price

of N$11 million to manufacture and deliver the vessel to the company's specifications. The

company contracted a Dutch lawyer and Architect to draft the Agreement and design the ship's

specifications to the tune of N$1.5 million.

Profitability projections for the first three years of operations on the Namibian cost is as follows:

2024

2025

2026

Profit before tax (in millions)

5

6.5

8

Depreciation of the vessel in profit before tax is calculated on a straight-line at 10% per annum,

and the Tax Authority grants wear and tear tax allowances on a straight-line method for a

three-year period (i.e., 33.3% per annum). Tax payment: half payable in the year incurred and

the balance in the following year. Northern Atlantic fishing also holds rights to a quota to be

harvested at the coast in West Africa valued at N$8 million, which will require the use of a

vessel. Due to the economic crunch, its credit rating has deteriorated; thus, it cannot borrow

sufficient funds to acquire two different vessels for both operations. The finance team has

determined that the West Africa fishing operation would yield cash profit after tax equivalent

of N$2 million in the first year, increasing to N$2.8 million in the third year of operation.

Absorbed/allocated overheads in the 2024 profit before tax amounts to N$100 000.

Corporate tax in Namibia is 32% and the cost of capital of the company is 15%.

REQUIRED

a) Calculate the Net Present Value (NPV) of the vessel

b) Calculate the Payback Period of the project

MARKS

20

3

Highlight to the management of North Atlantic Fishing any TWO (2)

2

c)

disadvantages of the Payback Period

2

|

|

4 Page 4 |

▲back to top |

QUESTION 3

[25 MARKS]

SWZ is a manufacturing company that has many trading divisions. Return on Investment (ROI)

is the main measure of each division's performance. Each divisional Manager's salary is linked

only to their division's ROI. The following information relating to S division summarises the

financial performance of the three years including the projected figures for 2025.

2023

2024

2025

N$000

N$000

N$000

Turnover

400

400

400

Cost of sales

240

240

240

Gross profit

160

160

160

Other operating costs

120

104

98

Operating profit

40

56

62

Capital invested as at the end of the year

400

320

256

Other operating costs include asset depreciation calculated at the rate of 20% per annum on

a reducing balance basis. The figures shown in the above table for the capital invested as at

the end of the year is the net book value of the division's fixed assets. At the beginning of

2025, the Manager of the S division is considering investing in an additional machine to boost

production capacity. The new machine will cost N$100 000 with an expected life of five years

depreciated using the same depreciation rate as the existing machinery on straight line

method. The new machine will increase sales by 10% and costs by 3%. The divisional cost

of capital is 8% per annum. The company has evaluated the investment and correctly

determined that it has a positive Net Present Value (NPV) of N$24 536.

REQUIRED

MARKS

Calculate the return on investment (ROI) for three-year period (i.e., without

3

a)

the new investment).

Calculate ROI for 2025 after considering the new investment and comment 11

b) on whether Management of S Division will still go ahead with the new

investment

Using Residual Income (RI) comment on whether Management of S 11

c)

Division will go ahead with the new investment

3

|

|

5 Page 5 |

▲back to top |

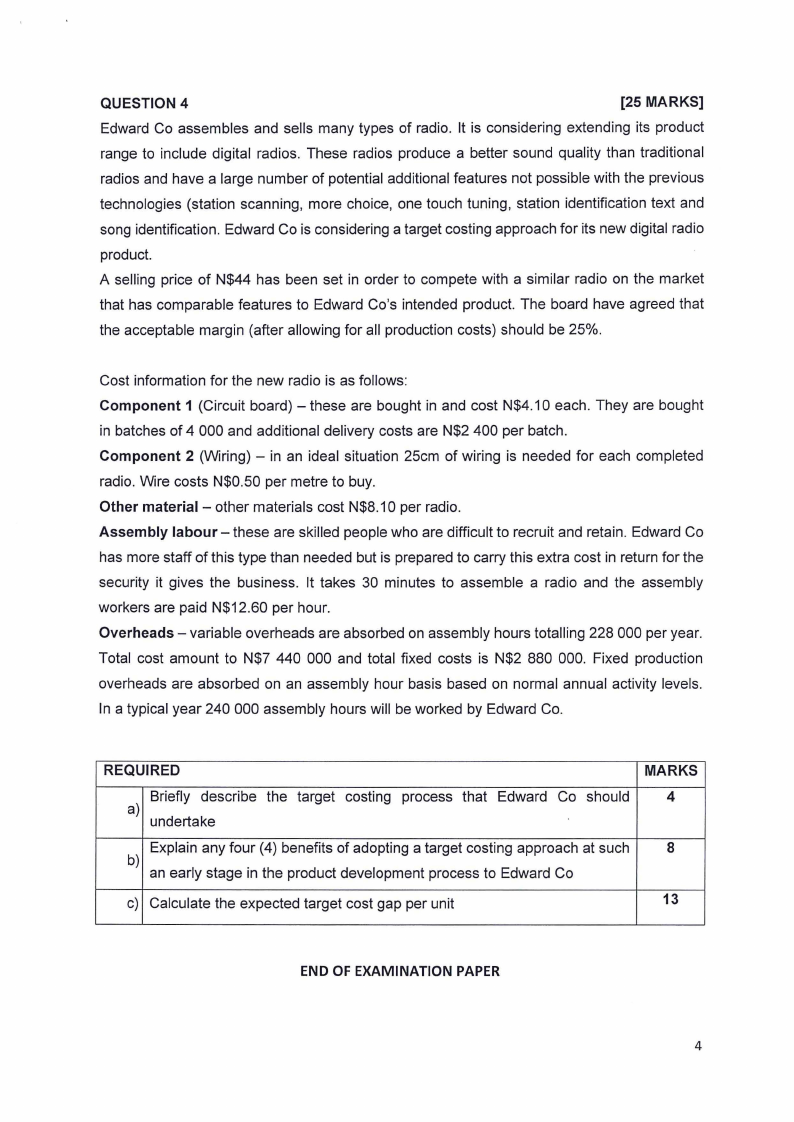

QUESTION 4

[25 MARKS]

Edward Co assembles and sells many types of radio. It is considering extending its product

range to include digital radios. These radios produce a better sound quality than traditional

radios and have a large number of potential additional features not possible with the previous

technologies (station scanning, more choice, one touch tuning, station identification text and

song identification. Edward Co is considering a target costing approach for its new digital radio

product.

A selling price of N$44 has been set in order to compete with a similar radio on the market

that has comparable features to Edward Co's intended product. The board have agreed that

the acceptable margin (after allowing for all production costs) should be 25%.

Cost information for the new radio is as follows:

Component 1 (Circuit board) - these are bought in and cost N$4.10 each. They are bought

in batches of 4 000 and additional delivery costs are N$2 400 per batch.

Component 2 (Wiring) - in an ideal situation 25cm of wiring is needed for each completed

radio. Wire costs N$0.50 per metre to buy.

Other material - other materials cost N$8.10 per radio.

Assembly labour - these are skilled people who are difficult to recruit and retain. Edward Co

has more staff of this type than needed but is prepared to carry this extra cost in return for the

security it gives the business. It takes 30 minutes to assemble a radio and the assembly

workers are paid N$12.60 per hour.

Overheads - variable overheads are absorbed on assembly hours totalling 228 000 per year.

Total cost amount to N$7 440 000 and total fixed costs is N$2 880 000. Fixed production

overheads are absorbed on an assembly hour basis based on normal annual activity levels.

In a typical year 240 000 assembly hours will be worked by Edward Co.

REQUIRED

MARKS

Briefly describe the target costing process that Edward Co should

4

a)

undertake

Explain any four (4) benefits of adopting a target costing approach at such

8

b)

an early stage in the product development process to Edward Co

c) Calculate the expected target cost gap per unit

13

END OF EXAMINATION PAPER

4

|

|

6 Page 6 |

▲back to top |

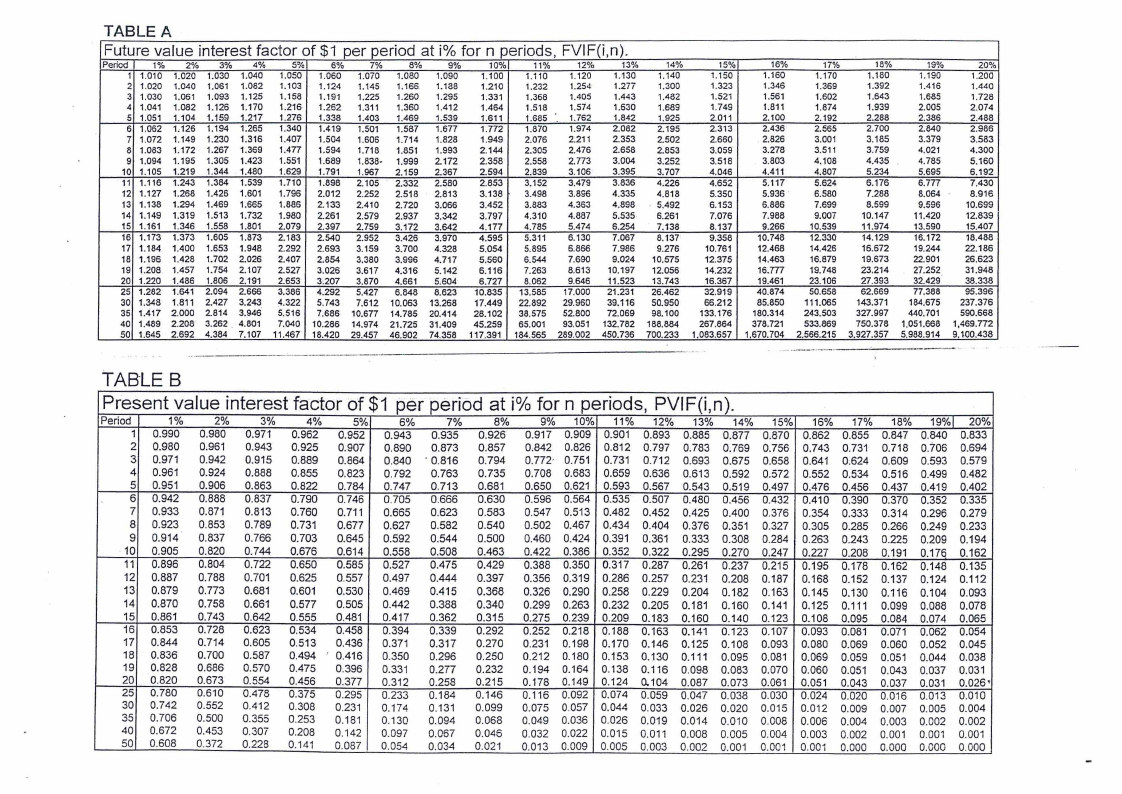

TABLE A

Future value interest factor of $1 per period at i% for n periods, FVIF(i,n).

Period

1

2

3

1%

1.010

1.020

1.030

2%

1.020

1.040

1.061

3%

1.030

1.061

1.093

4%

1.040

1.082

1.125

5%

1.050

1.103

1.158

6%

1.060

1.124

1.191

7%

1.070

1.145

1.225

ao1o 9%

1.080 1.090

1.166 1.188

1.260 1.295

10%

1.100

1.210

1.331

11%

1.110

1.232

1.368

12%

1.120

1.254

1.405

13%

1.130

1.277

1.443

14%

1.140

1.300

1.482

4 1.041 1.082 1.126 1.170 1.216 1.262 1.311 1.360 1.412 1.464 1.518 1.574 1.630 1.689

5 1.051 1.104 1.159 1.217 1.276 1.338 1.403 1.469 1.539

1.611

1.685 ·. 1.762

1.842

1.925

6 1.062 1.126 1.194 1.265 1.340 1.419 1.501 1.587 1.677 1.772 1.870 1.974 2.082 2.195

7 1.072 1.149 1.230 1.316 1.407 1.504 1.606 1.714 1.828 1.949 2.076 2.211 2.353 2.502

8 1.083 1.172 1.267 1.369 1.477 1.594 1.718 1.851 1.993

9 1.094 1.195 1.305 1.423 1.551 1.689 1.838· 1.999 2.172

2.144

2.358

2.305

2.558

2.476

2.773

2.658

3.004

2.853

3.252

10 1.105 1.219 1.344 1.480 1.629 1.791 1.967 2.159 2.367

2.594

2.839 3.106

3.395

3.707

11 1.116 1.243 1.384 1.539

12 1.127 1.268 1.426 1.601

1.710

1.796

1.898

2.012

2.105

2.252

2.332

2.518

2.580

2.813

2.853

3.138

3.152

3.498

3.479

3.896

3.836

4.335

4.226

4.818

13 1.138 1.294 1.469 1.665 1.886 2.133 2.410 2.720 3.066

3.452

3.8.83 4.363

4.898

5.492

14 1.149 1.319 1.513 1.732

15 1.161 1.346 1.558 1.801

16 1.173 1.373 1.605 1.873

1.980

2.079

2.183

2.261

2.397

2.540

2.579

2.759

2.952

2.937

3.172

3.426

3.342

3.642

3.970

3.797

4.177

4.595

4.310

4.785

5.311

4.887

5.474

6.130

5.535

6.254

7.067

6.261

7.138

8.137

17 1.184 1.4.00 1.653 1.948 2.292 2.693 3.159 3.700 4.328

18 1.196 1.428 1.702 2.026 2.407 2.854 3.380 3.996 4.717

5.054

5.560

5.895

6.544

6.866

7.690

7.986 9.276

9.024 10.575

19 1.208 1.457 1.754 2.107

20 1.220 1.486 1.806 2.t91

2.527

2.653

3.026

3:207

3.617

3.870

4.316

4.661

5.142

5.604

6.116

6.727

7.263

8.062

8.613 10.197 12.056

9.646 11.523 13.743

25 1.282

30 1.348

35 1.417

40 1.489

50 1.645

1.641

1.811

2.000

2.208

2.692

2.094 2.666

2.427 3.243

2.814 3.946

3.262 . 4.801

4.384 7.107

3.386

:4-322

5.516

7.040

11.467

4.292

5.743

7.686

10.286

18.420

5.427

7.612

10.677

14.974

29.457

6.848

10.063

14.785

21.725

46.902

8.623

13.268

20.414

31.409

74.358

10.835

17.449

28.102

45.259

117.391

13.585

22.892

38.575

65.001

184.565

17.000

29.960

52.800

93.051

289.002

21.231

39.116

72.069

132.782

450.736

26.462

50.950

98.100

188.884

700.233

15%

1.150

1.323

1.521

1.749

2.011

2.313

2.660

3.059

3.518

4.046

4.652

5.350

6.153

7.076

8.137

9.358

10.761

12.375

14.232

16.367

32.919

66.212

133.176

267.864

1.083.657

16%

1.160

1.346

1.561

1.811

2.100

2.436

2.826

3.278

3.803

4.411

5.117

5.936

6.886

7.988

9.266

10.748

12.468

14.463

16.m

19.461

40.874

85.850

180.314

378.721

1,670.704

17%

1.170

1.369

1.602

1.874

2.192

2.565

3.001

3.511

4.108

4.807

5.624

6.580

7.699

9.007

10.539

12.330

14.426

16.879

19.748

23.106

50.658

111.065

243.503

533.869

2,566.215

18%

1.180

1.392

1.643

1.939

2.288

2.700

3.185

3.759

4.435

5.234

6.176

7.288

8.599

10.147

11.974

14.129

16.672

19.673

23.214

27.393

62.669

143.371

327.997

750.378

3,927.357

19%

1.190

1.416

1.685

2.005

2.386

2.840

3.379

4.021

4.785

5.695

6.777

8.064

9.596

11.420

13.590

16.172

19.244

22.901

27.252

32.429

77.388

184.675

440.701

1.051.668

5.988.914

20%

1.200

1.440

1.728

2.074

2.488

2.986

3.583

4.300

5.160

6.192-

7.430

8.916

10.699

12.839

15.407

18.488

22.186

26.623

31.948

38.338

95.396

237.376

590.668

1,469.772

9,100.438

TABLE B

Present value interest factor of $1 per period at i% for n periods, PVIF(i,n).

Period

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

25

30

35

40

50

1%

0.990

0.980

0.971

0.961

0.951

0.942

0.933

0.923

0.914

0.905

0.896

0.887

0.879

0.870

0.861

0.853

0.844

0.836

0.828

0.820

0.780

0.742

0.706

0.672

0.608

2%

0.980

0.961

0.942

0.924

0.906

0.888

0.871

0.853

0.837

0.820

0.804

0.788

0.773

0.758

0.743

0.728

0.714

0.700

0.686

0.673

0.610

0.552

0.500

0.453

0.372

3%

0.971

0.943

0.915

0.888

0.863

0.837

0.813

0.789

0.766

0.744

0.722

0.701

0.681

0.661

0.642

0.623

0.605

0.587

0.570

0.554

0.478

0.412

0.355

0.307

0.228

4%

5%

0.962 0.952

0.925 0.907

0.889 0.864

0.855 0.823

0.822 0.784

0.790 0.746

0.760 0.711

0.731 0.677

0.703 0.645

0.676 0.614

0.650 0.585

0.625 0.557

0.601 0.530

0.577 0.505

0.555 0.481

0.534 0.458

0.513 0.436

0.494 ' 0.416

0.475 0.396

0.456 0.377

0.375 0.295

0.308 0.231

0.253 0.181

0.208 0.142

0.141 0.087

6%

0.943

0.890

0.840

0.792

0.747

0.705

0.665

0.627

0.592

0.558

0.527

0.497

0.469

0.442

0.417

0.394

0.371

0.350

0.331

0.312

0.233

0.174

0.130

0.097

0.054

7%

0.935

0.873

· 0.816

0.763

0.713

0.666

0.623

0.582

0.544

0.508

0.475

0.444

0.415

0.388

0.362

0.339

0.317

0.296

0.277

0.258

0.184

0.131

0.094

0.067

0.034

8%

0.926

0.857

0.794

0.735

0.681

0.630

0.583

0.540

0.500

0.463

0.429

0.397

0.368

0.340

0.315

0.292

0.270

0.250

0.232

0.215

0.146

0.099

0.068

0.046

0.021

9% 10% 11% 12% 13% 14% 15% 16% 17% 18% 19%1 20%

0.917 0.909 0.901 0.893 0.885 0.877 0.870 0.862 0.855 0.847 0.840 0.833

0,842 0.826 0.812 0.797 0.783 0.769 0.756 0.743 0.731 0.718 0.706 0.694

0.772· 0.751 0.731 0.712 0.693 0.675 0.658 0.641 0.624 0.609 0.593 0.579

0.708 0.683 0.659 0.636 0.613 0.592 Q.572 0.552 0.534 0.516 0.499 0.482

0.650 0.621 0.593 0.567 0.543 0.519 0.497 0.476 0.456 0.437 0.419 0.402

0.596 0.564 0.535 0.507 0.480 0.456 0.432 0.410 0.390 0.370 0.352 0.335

0.547 0.513 0.482 0.452 0.425 0.400 0.376 0.354 0.333 0.314 0.296 0.279

0.502 0.467 0.434 0.404 0.376 0.351 0.327 0.305 0.285 0.266 0.249 0.233

0.460 0.424 0.391 0.361 0.333 0.308 0.284 0.263 0.243 0.225 0.209 0.194

0.422 0.386 0.352 0.322 0.295 0.270 0.247 0.227 0.208 0.191 0.176 0.162

0.388 0.350 0.317 0.287 0.261 0.237 0.215 0.195 0.178 0.162 0.148 0.135

0.356 0.319 0.286 0.257 0.231 0.208 0.187 0.168 0.152 0.137 0.124 0.112

0.326 0.290 0.258 0.229 0.204 0.182 0.163 0.145 0.130 0.116 0.104 0.093

0.299 0.263 0.232 0.205 0.181 0.160 0.141 0.125 0.111 0.099 0.088 0.078

0.275 0.239 0.209 0.183 0.160 0.140 0.123 0.108 0.095 0.084 0.074 0.065

0.252 0.218 0.188 0.163 0.141 0.123 0.107 0.093 0.081 0.071 0.062 0.054

0.231 0.198 0.170 0.146 0.125 0.108 0.093 0.080 0.069 0.060 0.052 0.045

0.212 0.180 0.153 0.130 0.111 0.095 0.081 0.069 0.059 0.051 0.044 0.038

0.194 0.164 0.138 0.116 0.098 0.083 0.070 0.060 0.051 0.043 0.037 0.031

0.178 0.149 0.124 0.104 0.087 0.073 0.061 0.051 0.043 0.037 0.031 0.026'

0.116 0.092 0.074 0.059 0.047 0.038 0.030 0.024 0.020 0.016 0.013 0.010

0.075 0.057 0.044 0.033 0.026 0.020 0.015 0.012 0.009 0.007 0.005 0.004

0.049 0.036 0.026 0.019 0.014 0.010 0.008 0.006 0.004 0.003 0.002 0.002

0.032 0.022 0.015 0.011 0.008 0.005 0.004 0.003 0.002 0.001 0.001 0.001

0.013 0.009 0.005 0.003 0.002 0.001 0.001 0.001 0.000 0.000 0.000 0.000

|

|

7 Page 7 |

▲back to top |

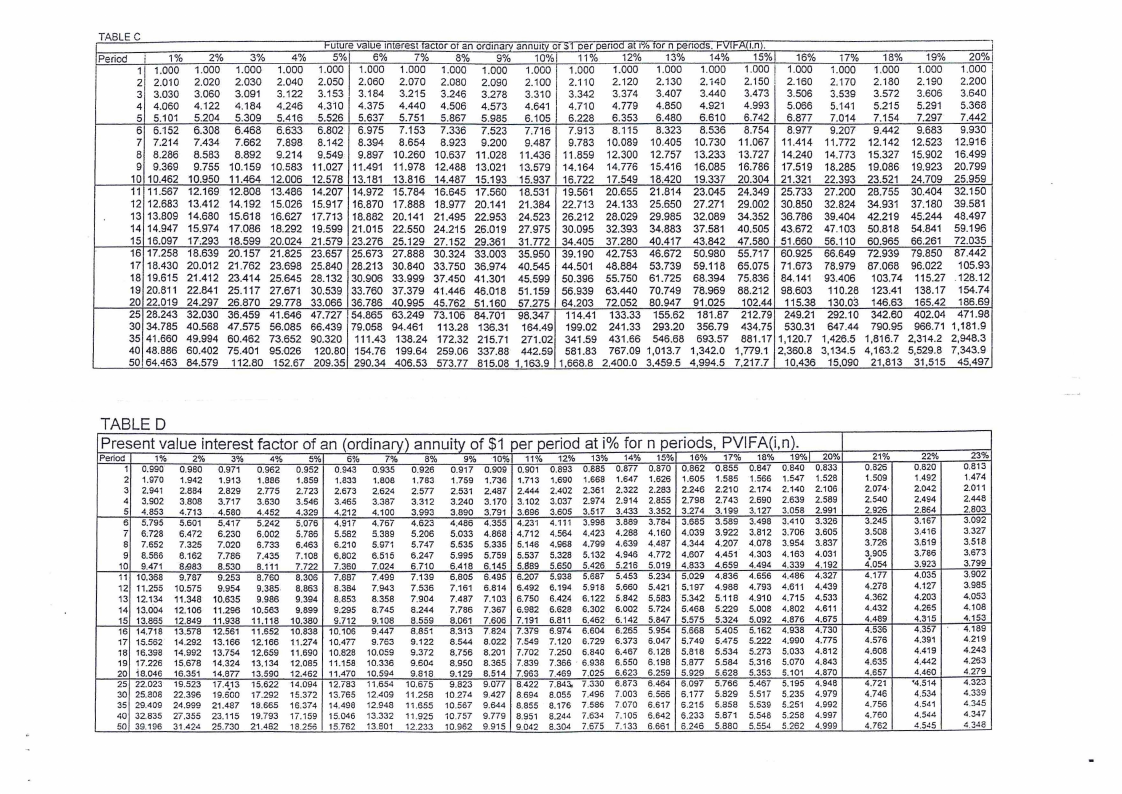

TABLE C

i-uture va1uemterest-ractor or an oramart annuity or :51 per oenoa at I roror n penoas. ,v'lt-All.nJ.

Period II 1%

2%

3%

4%

5%I 6%

7%

8%

9% 10% 11% 12% 13% 14% 15%I 16% 17% 18% 19% 20%

1 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 I

2 2.010 2.020 2.030 2.040 2.050 2.060 2.070 2.080 2.090 2.100 2.110 2.120 2.130 2. i40 2.150 2.160 2.170 2.180 2.190 2.200

3 3.030 3.060 3.091 3.122 3.153 3.184 3.215 3.246 3.278 3.310 3.342 3.374 3.407 3.440 3.473 3.506 3.539 3.572 3.606 3.640

4 4.060 4.122 4.184 4.246 4.310 4.375 4.440 4.506 4.573 4.641 4.710 4.779 4.850 4.921 4.993 5.066 5.141 5.215 5.291 5.368

5 5.101 5.204 5.309 5.416 5.526 5.637 5.751 5.867 5.985 6.105 6.228 6.353 6.480 6.610 6,742 6.877 7.014 7.154 7.297 7.442

6 6.152 6.308 6.468 6.633 6.802 6.975 7.153 7.336 7.523 7.716 7.913 8.115 8.323 8.536 8.754 8.977 9,207 9.442 9.683 9.930

7 7.214 7.434 7.662 7.898 8.142 8.394 8.654 8.923 9.200 9.487 9.783 10.089 10.405 10.730 11.067 11.414 11.772 12.142 12.523 12.916

8 8.286 8.583 8.892 9.214 9.549 9.897 10.260 10.637 11.028 11.436 11.859 12.300 12.757 13.233 13.727 14.240 14.773 15.327 15.902 16.499

9 9.369 9.755 10.159 10.583 11.027 11.491 11.978 1-2.488 13.021 13.579 14.164 14.776 15.416 16.085 16.786 17.519 18.285 19.086 19.923 20.799

10 10.462 10.950 11.464 12.006 12.578 13.181 13.816 14.487 15.193 15.937 16.722 17.549 18.420 19.337 20.304 21.321 22.393 23.521 24.709 25.959

11 11.567 12.169 12.808 13.486 14.207 14.972 15.784 16.645 17.560 18.531 19.561 20.655 21.814 23.045 24.349 25.733 27.200 28.755 30.404 32.150

12 12.683 13.412 14.192 15.026 15.917 16.870 17.888 18.977 20.141 21.384 22.713 24.133 25.650 27.271 29.002 30.850 32.824 34.931 37.180 39.581

13 13.809 14.680 15.618 16.627 17.713 18.882 20.141 21.495 22.953 24.523 26.212 28.029 29.985 32.089 34.352 36.786 39.404 42.219 45.244 48.497

14 14.947 15.974 17.086 18.292 19.599 21.015 22.550 24.215 26.019 27.975 30.095 32.393 34.883 37.581 40.505 43.672 47.103 50.818 54.841 59.196

15 16.097 17.293 18.599 20.024 21.579 23.276 25.129 27.152 29.361 31.772 34.405 37.280 40.417 43.842 47.580 51.660 56.110 60.965 66.261 72.035

16 17.258 18.639 20.157 21.825 23.657 25.673 27.888 30.324 33.003 35.950 39.190 42.753 46.672 50.980 55,717 60.925 66.649 72.939 79.850 87.442

17 18.430 20.012 21. 762 23.698 25.840 28.213 30.840 33.750 36.974 40.545 44.501 48.884 53.739 59.118 65.075 71.673 78.979 87.068 96.022 105.93

18 19,615 21.412 23.414 25.645 28.132 30.906 33.999 37.450 41.301 45.599 50.396 55.750 61.725 68.394 75.836 84.141 93.406 103.74 115.27 128.12

19 20.811 22.841 25.117 27.671 30.539 33.760 37.379 41.446 46.018 51.159 56.939 63.440 70.749 78.969 88.212 98,603 110.28 123.41 138.17 154.74

20 22.019 24.297 26.870 29.778 33.066 36.786 40.995 45.762 51.160 57.275 64.203 72.052 80.947 91,025 102.44 115.38 130.03 146.63 165.42 186.69

25 28.243 32.030 36.459 41.646 47.727 54.865 63.249 73.106 84.701 98.347 114.41 133.33 155.62 181.87 212.79 249.21 292.10 342.60 402.04 471.98

30 34.785 40.568 47.575 56,085 66.439 79.058 94.461 113.28 136.31 164.49 199.02 241.33 293.20 356.79 434.75 530.31 647.44 790.95 966.71 1,181.9

35 41.660 49.994 60.462 73.652 9.0.320 111.43 138.24 172.32 215. 71 271.02 341.59 431.66 546.68 693.57 881.17 1,120.7 1,426.5 1,816.7 2,314.2 2,948.3

40 48.886 60.402 75.401 95:026 120.80 154.76 199.64 259.06 337.88 442.59 581.83 767.09 1,013.7 1,342.0 1,779.1 2,360.8 3,134.5 4,163.2 5,529.8 7,343.9

50 64.463 84.579 112.80 152.67 209.35 290.34 406.53 573.77 815.08 1,163.9 1,668.8 2,400.0 3.459.5 4,994.5 7,217.7 10,436 15,090 21,813 31,515 45,497

TABLED

Present value interest factor of an (ordinary) annuity of $1 per period at i% for n periods, PVIFA(i,n).

Period

1%

2%

1 0.990" 0.980

2 1.970 1.942

3 2.941 2.884

4 3.902 3.808

5 4.853 4.713

6 5,795 5.601

7 6:728 6.472

8 7.652 7.325

9 8,566 8.162

10 9.471 8:983

11 10,368 9.787

12 11.255 10.575

13 12.134 11.348

14 13.004 12.106

15 13.865 12.849

16 14.718 13.578

17 15.562 14.292

18 16,398 14,992

19 17.226 15.678

20 18.046 16.351

3%

0.971

1.913

2.829

3,717

4.580

5.417

6.230

7.020

7.786

8,530

9.253

9.954

10.635

11.296

11.938

12.561

13.166

13.754

14.324

14,877

4%

0.962

1.886

2.775

3,630

4,452

5.242

6.002

6.733

7.435

8.111

8.760

9.385

9.986

10,563

11.11"8

11.652

12.166

12.659

13,134

13,590

5%

0.952

1,859

2.723

3.546

4.329

5.076

5.786

6,463

7.108

7.722

8,306

8.863

9.394

9.899

10,380

10.838

11.274

11.690

12.085

12.462

6%

0.943

1.833

2.673

3.465

4.212

4.917

5.582

6.210

6.802

7,360

7.887

8.384

8,853

9.295

9.712

10.106

10.477

10,828

11.158

11.470

7-%

0.935

1.808

2.624

3.387

4.100

4.767

5.389

5.971

6.515

7.024

7.499

7,943

8.358

8.745

9.108

9.447

9.763

10.059

10.336

10,594

8%

0.926

1,783

2.577

3.312

3,993

4.623

5,206

5.747

6,247

6.710

7.139

7.536

7,904

8.244

8.559

8.851

9.122

9.372

9.604

9.818

9%

0.917

1,759

2.531

3.240

3,890

4.486

5.033

5.535

5.995

6.418

6,805

7.161

7.487

7.786

8.061

8,313

8.544

8,756

6.950

9.129

10% 11%

0,909 0.901

1.736 1.713

2.487 2.444

3.170 3.102

3,791 3.696

4,355 4.231

4.868 4.712

5.335 5.146

5.759 5.537

6.145 5.889

6.495 6.207

6.814 6.492

7.103 6,750

7.367 6.982

7.606 7.191

7.824 7.37S

8.022 7.549

8.201 7.702

8.365 7.839

8.514 7.963

12% 13%

0,893 0.885

1.690 1.668

2.402 2.361

3,037 2.974

3.605 3,517

4,111 3.998

4.564 4.423

4.968 4.799

5.328 5.132

5,650 5.426

5.938 5,667

6.194 5.916

6.424 6.122

6.628 6.302

6.811 6.462·

6.974 6.604

7.120 6.729

7.250 6.840

7.366 · 6.938

7.469 7.025

14%

0,877

1.647

2.322

2.914

3.433

3.889

4.288

4.639

4.946

5.216

5.453

5.660

5.842

6,002

6.142

6,265

6,373

6.467

6,550

6,623

15%

0.870

1.626

2.283

2.855

3.352

3.784

4.160

4.487

4.772

5.019

5.234

5.421

5.583

5.724

5.847

5.954

6.047

6.128

6.198

6.259

16%

0.862

1.605

2.246

2,798

3.274

3.665

4,039

4.344

4.607

4,833

5.029

5.197

5.342

5.468

5.575

5.668

5.749

5.818

5,877

5.929

17%

0.855

1.585

2.210

2.743

3.199

3.589

3.922

4.207

4.451

4.659

4,836

4.988

5,118

5.229

5.324

5.405

5.475

5.534

5.584

5.628

18%

0.847

1.566

2.174

2.690

3.127

3.498

3.812

4.078

4.303

4.494

4.656

4.793

4,910

5.008

5.092

5.162

5.222

5.273

5.316

5,353

19%1 20%

0.840 o:833

1.547 1.528

2.140 2.106

2.639 2.589

3.058 2.991

3.410 3.326

3.706 3.605

3.954 3.837

4.163 4.031

4.339 4,192

4,486 4.327

4.611 4.439

4,715 4,533

4.802 4.611

4.876 4.675

4,938 4.730

4,990 4.775

5.033 4,812

5,070 4,843

5.101 4,870

25 22.023 19,523 17.4.13 15.622 14.094 12.783 11,654 10.675 9.823 9,077 8.422 i.843,, 7.330 6.873 6.464 6.097 5.766 5.467 5,195 4.948

30 25.308 22.396 19.600 17.292 15.372 13.765 12.409 11.258 10.274 9.427 8,694 8.055 7.496 7.003 6.566 6,177 5.829 5.517 5.235 4,979

35 29,409 24.999 21.487 18.665 16.374 14.498 12.948 11.655 10.567 9.644 8.855 8.176 7.586 7.070 6.617 6.215 5.858 5.539 5.251 4.992

40 32.835 27.355 23.115 19,793 17.159 15.046 13.332 11.925 10.757 9.779 8.951 8,244 7.634 7,105 6,642 6.233 5.871 5.548 5.258 4.997

50 39,196 31.424 25.730 21.482 18.256 15.762 13.801 12.233 10.962 9.915 9.042 8,304 7,675 7.133 6.661 6,246 5,880 5,554 5.262 4,999

21%

0.826

1.509

2.074·

2.540

2.926

3.245

3.508

3.726

3.905

4.054

4,177

4.278

4.362

4.432

4.489

4.536

4.576

4,608

4.635

4,657

4.721

4.746

4.756

4,760

4.762

22%

0.820

1.492

2.042

2.494

2.864

3.167

3.416

3.619

3.786

3.923

4.035

4.127

4.203

4.265

4.315

4,357

4,391

4.419

4,442

4.460

'4.514

4.534

4.541

4,544

4.545

23%

0.813

1.474

2.011

2.448

2,803

3.092

3.327

3.518

3.673

3.799

3.902

3.985

4,053

4.108

4.153

4.189

4.219

4.243

4,263

4.279

4,323

4.339

4.345

4.347

4.348