|

GMA711S-MANAGEMENT ACCOUNTING 310- 1ST OPP -JUNE 2025 |

|

|

1 Page 1 |

▲back to top |

nAmlBIA unlVERSITY

OF SCIEnCE Ano TECHnOLOGY

FACULTY OF COMMERCE, HUMAN SCIENCES AND EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING AND FINANCE

QUALIFICATION: BACHELOR OF ACCOUNTING

QUALIFICATION CODE: 0?BGAC LEVEL:?

COURSE CODE: GMA711 S

COURSE NAME: MANAGEMENT ACCOUNTING 310

SESSION: JUNE 2025

PAPER: THEORY AND CALCULATIONS

DURATION: 3 HOURS

MARKS: 100

EXAMINERS

MODERATOR

FIRST OPPORTUNITY EXAMINATION QUESTION PAPER

Lameck Odada; Moses Nyakuwanika and Rabanus Nashinwe

Alfred Makosa

INSTRUCTIONS

1. This question paper consists of FOUR (4) Questions.

2. Answer ALL the FOUR (4) questions in blue or black ink only. NO PENCIL and TIPEX

3. Start each question on a new page and number the answers correctly and clearly.

4. Write clearly and neatly, showing all your formulas, workings, and assumptions.

5. Unless otherwise stated, round off final answers only to two (2) decimal places.

6. Questions relating to this examination may be raised in the initial 30 minutes after the start

of the examination. Thereafter, candidates must use their initiative to deal with any

perceived error or ambiguities, and any assumptions the candidate makes should be

clearly stated.

PERMISSIBLE MATERIALS

1. Silent, non-programmable calculators

THIS QUESTION PAPER CONSISTS OF _7_ PAGES (including this front page)

|

|

2 Page 2 |

▲back to top |

QUESTION 1

[30 MARKS]

Charm Inc., a software company, has developed a new game, Fingo', which it plans to launch

soon. Sales of the new game are expected to be very strong, following a favourable review by

a popular PC magazine. Charm Inc. has been informed that the review will give the game a

'Best Buy' recommendation. Sales volumes, production volumes, and selling prices for 'Fingo'

over its four-year life are expected to be as follows

Year

1

2

3

4

Sales and production (units)

150 000

70 000 60 000

60 000

Selling price (N$ per game)

25

24

23

22

Financial information on 'Fingo' for the first year of production is as follows:

N$

Direct material cost

5.40 per game

Other variable production cost

6.00 per game

Fixed costs

4.00 per game

Advertising costs to stimulate demand are expected to be N$650 000 in the first year of

production and N$100 000 in the second year of production. No advertising costs are expected

in the third and fourth years of production. Fixed costs represent incremental cash fixed

production overheads. The fixed cost per unit is based on normal production of 150 000 units.

Assume there is no over/under allocation of fixed costs.

'Fingo' will be produced on a new production machine costing N$800 000. Although this

production machine is expected to have a useful life of up to ten years, government legislation

allows Charm Inc. to claim the capital cost of the machine against the manufacture of a single

product. Capital allowances will, therefore, be claimed on a straight-line basis over four years.

Charm Inc. pays tax on profit at a rate of 30% per year, and tax liabilities are settled in the

year in which they arise. Charm Inc. uses an after-tax discount rate of 10% when appraising

new capital investments. Ignore inflation.

REQUIRED:

MARKS

a) Calculate the net present value of the proposed investment.

20

b) Calculate the internal rate of return of the proposed investment using

5

20% cost of capital

c) Discuss the reasons why the net present value investment appraisal

5

method is preferred to other investment appraisal methods

1

|

|

3 Page 3 |

▲back to top |

QUESTION 2

[20 MARKS]

CYMOT is a privately-owned, wholly Namibian company founded in 1948. The Company has

since grown to become a leader in the supply of quality products to its customers through its

distribution network of branches within Namibia, as well as trading on a wholesale basis in

both South Africa and Angola.

The company is launching a new product. Market research shows that if the selling price of

the product is N$2100 the demand will be 2 400 units, but for every N$20 increase in selling

price there will be a corresponding decrease in demand of 400 units and for every N$20

decrease in selling price there will be a corresponding increase in demand of 200 units. The

estimated variable costs of the product are N$60 per unit. There are no specific fixed costs,

but general fixed costs are absorbed using an absorption rate of N$16 per unit.

REQUIRED

MARKS

Identify four (4) external factors the company should consider when setting

4

a)

the price of the new product

Derive an equation for the demand function (that is, the price as a function

4

= = b)

of quantity demanded). Note: If P a-bx, then MR a-2bx.

c) Find the quantity that maximises profit

4

d) Calculate the optimum price

2

e) Determine the contribution and maximum profit

5

QUESTION 3

[25 MARKS]

The Portable Garage Co (PGC) is a company specialising in manufacturing and selling a

range of products for motorists. It is split into two divisions: the battery division (Division B)

and the adaptor division (Division A). Division B sells one product - portable battery chargers

for motorists, which can be attached to a car's battery and used to start the engine when the

car's battery fails.

Division A sells adaptors that are used by customers to charge mobile devices and laptops by

attaching them to the car's internal power source. Recently, Division B has upgraded its

portable battery so it can also be used to rapidly charge mobile devices and laptops. The

mobile device or laptop must be attached to the battery using a special adaptor, which is

supplied to the customer with the battery. Division B currently buys the adaptors from Division

A, which also sells them externally to other companies.

The following data is available for both divisions:

2

|

|

4 Page 4 |

▲back to top |

Division B

Sellinq price for each portable battery, including the adaptor

Costs per battery:

Adaptor from Division A

Other materials from external suppliers

Labour costs

Annual fixed overheads

Annual production and sales of portable batteries (units)

Maximum annual market demand for portable batteries (units)

N$180

N$13

N$45

N$35

N$5 460 000

150 000

180 000

Division A

Sellinq price per adaptor to Division B

Sellinq price per adaptor to external customers

Costs per adaptor:

Materials

Labour costs

Annual fixed overheads

Current annual production capacity and sales of adaptors - both

internal and external sales (units)

Maximum annual external demand for adaptors (units)

N$13

N$15

N$3

N$4

N$2 200 000

350 000

200 000

In addition to the materials and labour costs above, Division A incurs a variable cost of N$1

per adaptor for all adaptors it sells externally. Currently, the head office's purchasing policy

only allows Division B to purchase the adaptors from Division A, but Division A has refused to

sell Division B any more than the current level of adaptors it supplies to it. The manager of

Division Bis unhappy. He has a special industry contact whom he could buy the adaptors from

at exactly the same price charged by Division A if he were given the autonomy to purchase

from outside the group. After discussions with both of the divisional managers and to ensure

that the managers are not demotivated, Head Office has now agreed to change the purchasing

policy to allow Division B to buy externally, provided that it optimises the profits of the group

as a whole.

REQUIRED

MARKS

a) Identify and describe the THREE (3) methods of transfer pricing

6

Under the current transfer pricing system, prepare a profit statement 19

showing each division's profit and the PGC as a whole. Where appropriate,

b)

your sales and cost figures should be split into external sales and inter-

divisional transfers.

3

|

|

5 Page 5 |

▲back to top |

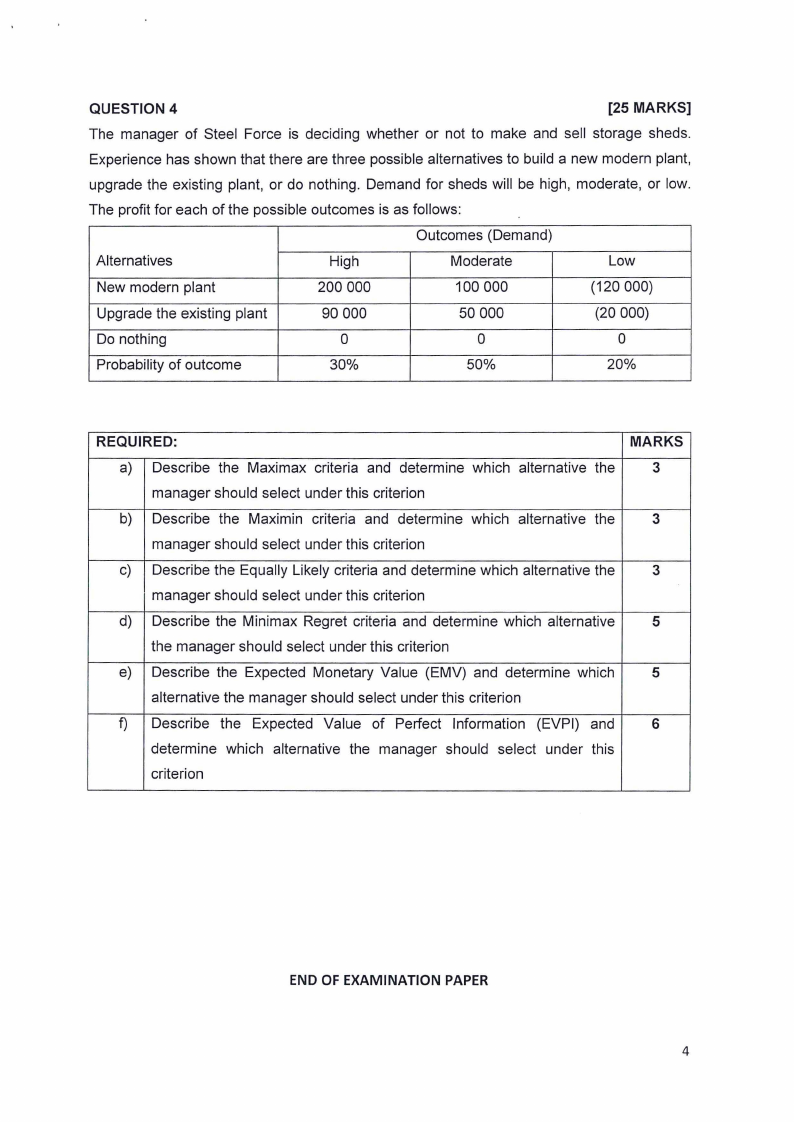

QUESTION 4

[25 MARKS]

The manager of Steel Force is deciding whether or not to make and sell storage sheds.

Experience has shown that there are three possible alternatives to build a new modern plant,

upgrade the existing plant, or do nothing. Demand for sheds will be high, moderate, or low.

The profit for each of the possible outcomes is as follows:

Outcomes (Demand)

Alternatives

High

Moderate

Low

New modern plant

200 000

100 000

(120 000)

Upgrade the existing plant

90 000

50 000

(20 000)

Do nothing

0

0

0

Probability of outcome

30%

50%

20%

REQUIRED:

MARKS

a) Describe the Maximax criteria and determine which alternative the

3

manager should select under this criterion

b) Describe the Maximin criteria and determine which alternative the

3

manager should select under this criterion

c) Describe the Equally Likely criteria and determine which alternative the

3

manager should select under this criterion

d) Describe the Minimax Regret criteria and determine which alternative

5

the manager should select under this criterion

e) Describe the Expected Monetary Value (EMV) and determine which

5

alternative the manager should select under this criterion

f) Describe the Expected Value of Perfect Information (EVPI) and

6

determine which alternative the manager should select under this

criterion

END OF EXAMINATION PAPER

4

|

|

6 Page 6 |

▲back to top |

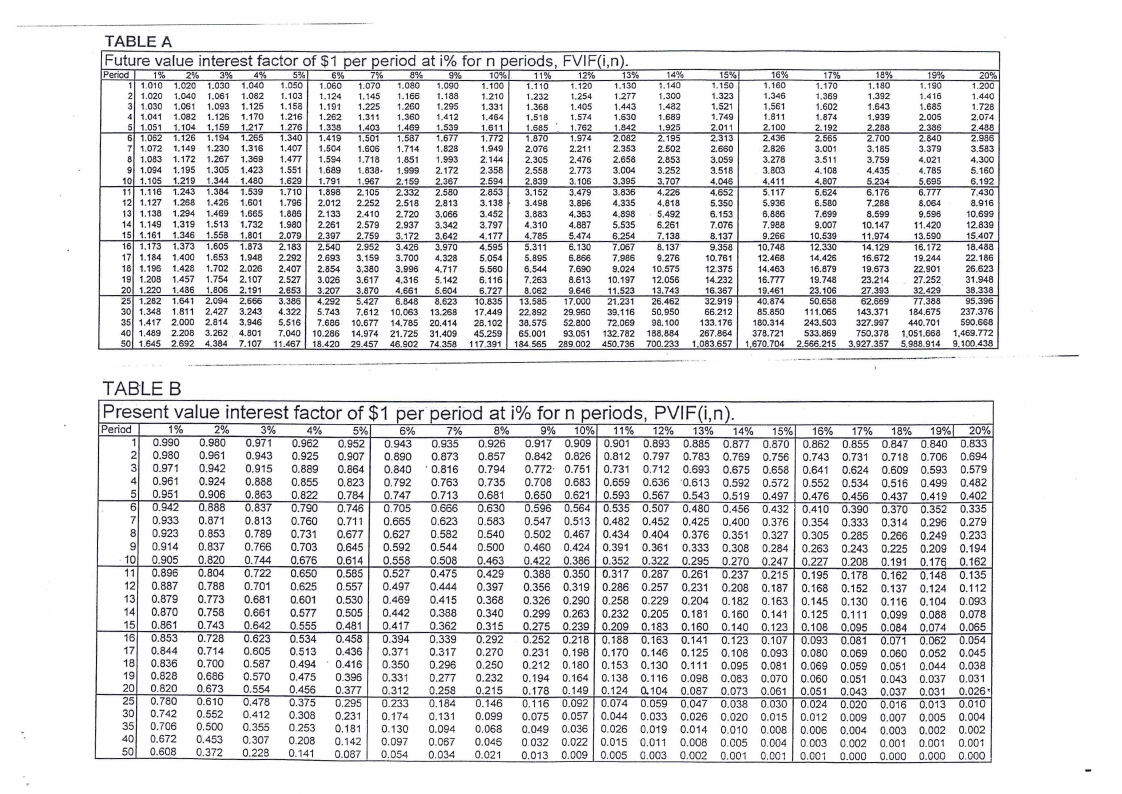

TABLE A

Future value interest factor of $1 per period at i% for n periods, FVIF(i,n).

Period

1%

1 1.010

2 1.020

3 1.030

4 1.041

5 1.051

6 1.062

7 1.072

2%

1.020

1.040

1.061

1.082

1.104

1,126

1,149

3%

1.030

1.061

1.093

1.126

1.159

1.194

1.230

4%

1.040

1.082

1.125

1.170

1.217

1.265

1.316

5%

1.050

1.103

1.158

1.216-

1.276

1.340

1.407

6%

1.060

1.124

1.19"1

1.262

1.338

1.419

1.504

7%

1.070

1.145

1.225

1.311

1.403

1.501

1.606

8%

1.080

1.166

1.260

1.360

1.469

1.587

1.714

9%

1.090

1.188

1.295

1.412

1.539

1.677

1.628

10%

1.100

1.210

1.331

1.464

1.611

1.772

1.949

11%

12%

1.110 1.120

1.232 1.254

1.366 1.405

1.518 1.574

1.685 ·_ 1.762

1.870 1.974

2.076 2.211

13%

1.130

1.277

1.443

1.630

1.642

2.082

2.353

14%

1.140

1.300

1.482

1.689

1.925

2.195

2.502

8 1.063 1.172 1.267 1.369

9 1.094 1.195 1.305 1.423

10 1.105 1.219 1.344 1.480

1.477

1.551

1.629

1.594

1.689

1.791

1.718

1.638-

1.967

1.851

1.999

2.159

1.993

2.172

2.367

2.144

2.358

2.594

2.305

2.558

2.839

2.476

2.773

3.106

2.656

3.004

3.395

2.853

3.252

3.707

11 1.116 1.243 1.384 1.539 1.710 1.898 2.105 2.332 2.580

12 1.127 1.268 1.426 1.601 1.796 2.012 2.252 2.518 2.813

2.853

3.138

3.152

3.498

3.479

3.896

3.836

4.335

4.226

4.818

13 1.138 1.294 1.469 1.665 1.886 2.133 2.410 2.720 3.066 3.452 3.883 4.363 4.898 5.492

14 1.149

15 1.161

16 1.173

17 1.184

1.319

1.346

1.373

1.400

1.513

1.558

1.605

1.653

1.732

1.801

1.873

1.948

1.980

2.079

2.183

2.292

2.261

2.397

2.540

2.693

2.579

2.759

2.952

3.159

2.937

3.172

3.426

3.700

3.342

3.642

3.970

4.328

3.797

4.177

4.595

5.054

4.310

4.785

5.311

5.895

4.887

5.474

6.130

6.866

5.535

6.254

7.067

7.986

6.261

7.138

8.137

9.276

18 1.196 1.428 1.702 2.026 2.407 2.854 3.380 3.996 4.717 5.560 6.544 7.690 9.024 10.575

19 1.208 1.457 1.754 2.107

20 1.220 1.486 1.806 2.191

25 1.262 1.641 2.094 2.666

2.527

2.653

3.386

3.026

3.207

4.292

3.617

3.870

5.427

4.316

4.661

6.848

5.142

5.604

8.623

6.116

6.727

10.835

7.263

8.062

13.585

6.613

9.646

17.000

10.197

11.523

21.231

12.056

13.743

26.462

30 1.348

35 1.417

40 1.489

50 1.645

1.811

2.000

2.208

2.692

2.427

2.814

3.262

4.384

3.243

3.946

4.801

7.107

4.322

5.516

7.040

11.467

5.743

7.686

10.286

16.420

7.612

10.677

14.974

29.457

10.063

14.785

21.725

46.902

13.266

20.414

31.409

74.358

17.449

28.102

45.259

117.391

22.892

38.575

65.001

184.565

29.960

52.800

93.051

289.002

39.116

72.069

132.782

450.736

50.950

98.100

188.884

700.233

15%

1.150

1.323

1.521

1.749

2.011

2.313

2.660

3.059

3.518

4,046

4.652

5.350

6.153

7.076

8.137

9.358

10.761

12.375

14.232

16.367

32.919

66.212

133.176

267.864

1.083.657

16%

1.160

1.346

1.561

1.811

2.100

2.436

2.826

3.278

3.803

4.411

5.117

5.936

6.886

7.988

9.266

10.748

12.468

14.463

16.m

19.461

40.874

85.850

160.314

378.721

1,670.704

17%

1.170

1.369

1.602

1.874

2.192

2.565

3.001

3.511

4.108

4.807

5.624

6.580

7.699

9.007

10.539

12.330

14.426

16.679

19.748

23.106

50.658

111.065

243.503

533.869

2.566.215

18%

1.180

1.392

1.643

1.939

2.288

2.700

3.185

3.759

4.435

5.234

6.176

7.288

8.599

10.147

11.974

14.129

16.672

19.673

23.214

27.393

62.669

143.371

327.997

750.378

3.927.357

19~1,

20%

1.190

1.200

1.416

1.440

1.685

1.728

2.005

2.074

2.386

2.488

2.840

2.986

3.379

3.583

4,021

4.300

4.785

5.160

5.695

6.192

6.777

7.430

8.064

8.916

9.596

10.699

11.420

12.839

13.590

15.407

16.172

18.488

19.244

22.166

22.901

26.623

27.252

31.948

32.429

38.338

77.386

95.396

184.675 237.376

440.701 590.668

1,051.668 1,469.772

5,988.914 9. 100.438

TABLE B

Present value interest factor of $1 per"period at io/ofor n periods, PVIF(i,n).

Period

1

2

3

4

5

6

7

8

9

· 10

11

12

13

14

15

16

17

18

19

20

25

30

35

40

50

1%

0.990

0.980

0.971

0.961

0.951

0.942

0.933

0.923

0.914

0.905

0.896

0.887

0.879

0.870

0.861

0.853

0.844

0.836

0.828

0.820

0.780

0.742

0.706

0.672

0.608

2%

0.980

0.961

0.942

0.924

0.906

0.888

0.871

0.853

0.837

0.820

0.804

0.788

0.773

0.758

0.743

0.728

0.714

0.700

0.686

0.673

0.610

0.552

0.500

0.453

0.372

3%

0.971

0.943

0.915

0.888

0.863

0.837

0.813

0.789

0.766

0.744

0.722

0.701

0.681

0.661

0.642

0.623

0.605

0.587

0.570

0.554

0.478

0.412

0.355

0.307

0.228

4%

5%

0.962 0.952

0.925 0.907

0.889 0.864

0.855 0.823

0.822 0.784

0.790 0.746

0.760 0.711

0.731 0.677

0.703 0.645

0.676 0.614

0.650 0.585

0.625 0.557

0.601 0.530

0.577 0.505

0.555 0.481

0.534 0.458

0.513 0.436

0.494 ' 0.416

0.475 0.396

0.456 0.377

0.375 0.295

0.308 0.231

0.253 0.181

0.208 0.142

0.141 0.087

6%

0.943

0.890

0.840

0.792

0.747

0.705

0.665

0.627

0.592

0.558

0.527

0.497

0.469

0.442

0.417

0.394

0.371

0.350

0.331

0.312

0.233

0.174

0.130

0.097

0.054

7%

0.935

0.873

· 0.816

0.763

0.713

0.666

0.623

0.582

0.544

0.508

0.475

0.444

0.415

0.388

0.362

0.339

0.317

0.296

0.277

0.258

0.184

0.131

0.094

0.067

0.034

8%

0.926

0.857

0.794

0.735

0.681

0.630

0.583

0.540

0.500

0.463

0.429

0.397

0.368

0.340

0.315

0.292

0.270

0.250

0.232

0.215

0.146

0.099

0.068

0.046

0.021

9% 10% 11% 12% 13% 14% 15% 16% 17% 18% 19%1 20%

0.917 0.909 0.901 0.893 0.885 0.877 0.870 0.862 0.855 0.847 0.840 0.833

0.842 0.826 0.812 0.797 0.783 0.769 0.756 0.743 0.731 0.718 0.706 0.694

0.772· 0.751 0.731 0.712 0.693 0.675 0.658 0.641 0.624 0.609 0.593 0.579

0.708 0.683 Q.659 0.636 ·0.613 0.592 0.572 0.552 0.534 0.516 0.499 0.482

0.650 0.621 0.593 0.567 0.543 0.519 0.497 0.476 0.456 0.437 0.419 0.402

0.596 0.564 0.535 0.507 0.480 0.456 0.432 0.410 0.390 0.370 0.352 0.335

0.547 0.513 0.482 0.452 0.425 0.400 0.376 0.354 0.333 0.314 0.296 0.279

0.502 0.467 0.434 0.404 0.376 0.351 0.327 0.305 0.285 0.266 0.249 0.233

0.460 0.424 0.391 0.361 0.333 0.308 0.284 0.263 0.243 0.225 0.209 0.194

0.422 0.386 0.352 0.322 0.295 0.270 0.247 0.227 0.208 0.191 0.176 0.162

0.388 0.350 0.317 0.287 0.261 0.237 0.215 0.195 0.178 0.162 0.148 0.135

0.356 0.319 0.286 0.257 0.231 0.208 0.187 0.168 0.152 0.137 0.124 0.112

0.326 0.290 0.258 0.229 0.204 0.182 0.163 0.145 0.130 0.116 0.104 0.093

0.299 0.263 0.232 0.205 0.181 0.160 0.141 0.125 0.111 0.099 0.088 0.078

0.275 0.239 0.209 0.183 0.160 0.140 0.123 0.108 0.095 0.084 0.074 0.065

0.252 0.218 0.188 0.163 0.141 0.123 0.107 0.093 0.081 0.071 0.062 0.054

0.231 0.198 0.170 0.146 0.125 0.108 0.093 0.080 0.069 0.060 0.052 0.045

0.212 0.180 0.153 0.130 0.111 0.095 0.081 0.069 0.059 0.051 0.044 0.038

0.194 0.164 0.138 0.116 0.098 0.083 0.070 0.060 0.051 0.043 0.037 0.031

0.178 0.149 0.124 0.104 0.087 0.073 0.061 0.051 0.043 0.037 0.031 0.026·

0.116 0.092 0.074 0.059 0.047 0.038 0.030 0.024 0.020 0.016 0.013 0.010

0.075 0.057 0.044 0.033 0.026 0.020 0.015 0.012 0.009 0.007 0.005 0.004

0.049 0.036 0.026 0.019 0.014 0.010 0.008 0.006 0.004 0.003 0.002 0.002

0.032 0.022 0.015 0.011 0.008 0.005 0.004 0.003 0.002 0.001 0.001 0.001

0.013 0.009 0.005 0.003 0.002 0.001 0.001 0.001 0.000 0.000 0.000 0.000

|

|

7 Page 7 |

▲back to top |

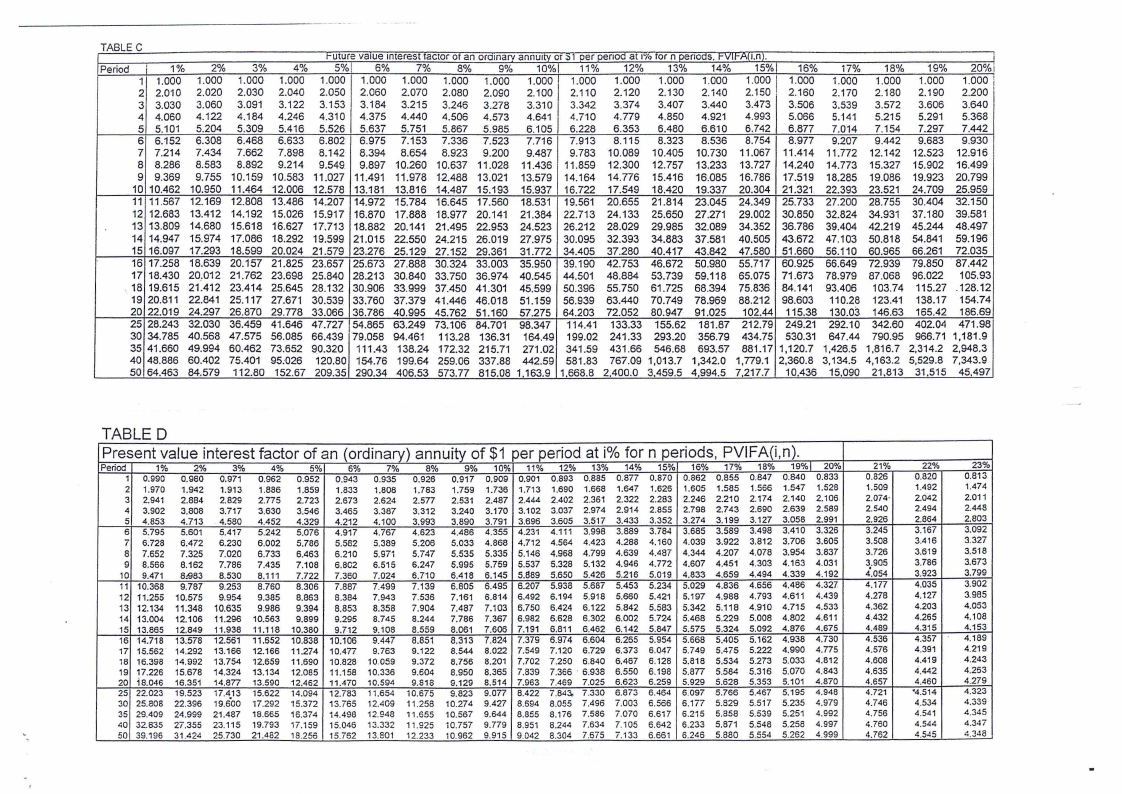

TABLE C

i-uture vaIue Interest·TactorOTan orainarv annuItv or ::,1oer oenoa at I-;oTorn oenoas. i-vu-Au.nJ.

Period I 1%

2%

3%

4%

5%1 6%

7%

8%

9% 10%1 11% 12% 13% 14% 15% 16% 17% 18% 19% 20%\\

1 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000

2 2.010 2.020 2.030 2.040 2.050 2.060 2.070 2.080 2.090 2.100 2.110 2.120 2.130 2.140 2.150 2.160 2.170 2.180 2.190 2.200

3 3.030 3.060 3.091 3.122 3.153 3.184 3.215 3.246 3.278 3.310 3.342 3.374 3.407 3.440 3.473 3.506 3.539 3.572 3.606 3.640

4 4.060 4.122 4.184 4.246 4.310 4.375 4.440 4.506 4.573 4.641 4.710 4.779 4.850 4.921 4.993 5.066 5.141 5.215 5.291 5.368

5 5.101 5.204 5.309 5.416 5.526 5.637 5.751 5.867 5.985 6.105 6.228 6.353 6.480 6.610 6.742 6.877 7.014 7.154 7.297 7.442

6 6.152 6.308 6.468 6.633 6.802 6.975 7.153 7.336 7.523 7.716 7.913 8.115 8.323 8.536 8.754 8.977 9.207 9.442 9.683 9.930

7 7.214 7.434 7.662 7.898 8.142 8.394 8.654 8.923 9.200 9.487 9.783 10.089 10.405 10.730 11.067 11.414 11.T72 12.142 12.523 12.916

8 8.286 8.583 8.892 9.214 9.549 9.897 10.260 10.637 11.028 11.436 11.859 12.300 12.757 13.233 13.727 14.240 14.773 15.327 15.902 16.499

9 9.369 9.755 10.159 10.583 11.027 11.491 11.978 12.488 13.021 13.579 14.164 14.776 15.416 16.085 16.786 17.519 18.285 19.086 19.923 20.799

10 10.462 10.950 11.464 12.006 12.578 13.181 13.816 14.487 15.193 15.937 16.722 17.549 18.420 19.337 20.304 21.321 22.393 23.521 24.709 25.959

11 11.567 12.169 12.808 13.486 14.207 14.972 15.784 16.645 17.560 18.531 19.561 20.655 21.814 23.045 24.349 25.733 27.200 28.755 30.404 32.150

12 12.683 13.412 14.192 15.026 15.917 16.870 17.888 18.977 20.141 21.384 22.713 24.133 25.650 27.271 29.002 30.850 32.824 34.931 37.180 39.581

13 13.809 14.680 15.618 16.627 17.713 18.882 20.141 21.495 22.953 24.523 26.212 28.029 29.985 32.089 34.352 36.786 39.404 42.219 45.244 48.497

14 14.947 15.974 17.086 18.292 19.599 21.015 22.550 24.215 26.019 27.975 30.095 32.393 34.883 37.581 40.505 43.672 47.103 50.818 54.841 59.196

15 16.097 17.293 18.599 20.024 21.579 23.276 25.129 27.152 29.361 31.772 34.405 37.280 40.417 43.842 47.580 51.660 56.110 60.965 66.261 72.035

16 17.258 18.639 20.157 21.825 23.657 25.673 27.888 30.324 33.003 35.950 39.190 42.753 46.672 50.980 55.717 60.925 66.649 72.939 79.850 . 87.442

17 18.430 20,012 21.762 23.698 25.840 28.213 30.840 33.750 36.974 40.545 44.501 48.884 53.739 59.118 65.075 71.673 78.979 87.068 96.022 105.93

. 18 19.615 21.412 23.414 25.645 28.132 30.906 33.999 37.450 41.301 45.599 50.396 55.750 61.725 68.394 75.836 84.141 93.406 103.74 115.27 .128.12

19 20.811 22.841 25.117 27.671 30.539_ 33.760 37.379 41.446 46.018 51.159 56.939 63.440 70.749 78.9.69 88.212 98.603 110.28 123.41 138.17 154.74

20 22.019 24.297 26.870 29.778 33.066 36.786 40.995 45.762 51.160 57.275 64.203 72.052 80.947 91.025 102.44 115.38 130.03 146.63 165.42 186.69

25 28.243 32.030 36.459 41.646 47.727 54.865 63.249 73.106 84.701 98.347 114.41 133.33 155.62 181.87 212.79 249.21 292.10 342.60 402.04 471.98

30 34.785 40.568 47.575 56.085 66.439 79.058 94.461 113.28 136.31 164.49 199.02 241.33 293.20 356.79 434.75 530.31 647.44 790.95 966.71 1,181.9

35 41.660 49.994 60.462 73.652 90.320 111.43 138.24 172.32 215. 71 271.02 341.59 431.66 546.68 693.57 881.17 1,120.7 1,426.5 1,816.7 2,314.2 2,948.3

40 48.886 60.402 75.401 95.026 120.80 154.76 199.64 259.06 337.88 442.59 581.83 767.09 1,013.7 1,342.0 1,779.1 2,360.8 3,134.5 4,163.2 5,529.8 7,343.9

50 64.463 84.579 112.80 152.67 209.35 290.34 406.53 573.77 815.08 1.163.9 1,668.8 2.400.0 3.459.5 4,994.5 7,217.7 10.436 15,090 21.813 31,515 45.497

TABLED

Present value interest factor of an (ordinary) annuity of $1 per period at i% for n periods, PVIFA(i,n).

Period

1%

1 0.990

2 1.970

3 2.941

4 3.902

5 4.853

6 5.795

7 6;728

8 7.652

9 8.566

10 9.471

11 10.368

12 11.255

13 12.134

14 13.o'04

15 13.865

16 14.718

17 15.562

18 16.398

19 17.226

20 18.046

25 22.023

2%

0.980

1.942

2.884

3,808

4.713

5.601

6.472

7.325

8.162

8"983

9.787

10.575

11.348

12.106

12.849

13.578

14.292

14.992

15.678

16.351

19.523

3%

0.971

1.913

2.829

3.717

4.580

5.417

6.230

7.020

7.786

8.530

9.253

9.954

10.635

11.296

11.938

12.561

13.166

13.754

14.324

14.877

17.413

4o/o

5%

0.962 0.952

1.886 1.859

2.775 2.723

3.630 3.546

4.452 4.329

5.242 5.076

6.002 5.786

6.733 6.463

7.435 7.108

8.111 7.722

8.760 8.306

9.385 8.863

9.986 9.394

10.563 9.899

11.118 10,380

11,652 10.838

12.166 11.274

12.659 11,690

13.134 12.085

13.590 12.462

15.622 14.094

6%

0.943

1.833

2.673

3,465

4.212

4.917

5.582

6.210

6.802

7.360

7.887

8.384

8.853

9.295

9.i12

10.106

10.4TT

10.828

11.158

11.470

12.783

7%

0.935

1.808

2.624

3.387

4.100

4.767

5.389

5.971

6.515

7.024

7.499

7.943

8.358

8.745

9.108

9.447

9.763

10.059

10.336

10.594

11.654

8%

0.926

1.783

2.577

3.312

3.993

4.623

5.206

5.747

6.247

6.710

7.139

7.536

7.904

8.244

8.559

8,851

9.122

9.372

9.604

9.618

10.675

9%

0.917

1.759

2.531

3.240

3.890

4.486

5.033

5.535

5.995

6.418

6.805

7.161

7.487

7.786

8.061

8.313

8.544

8.756

8.950

9.129

9.823

10%

0.909

1.736

2.487

3.170

3.791

4.355

4.868

5.335

5.759

6.145

6.495

6.814

7.103

7.367

7.606

7.824

8.022

8.201

8.365

8.514

9.077

11%

0.901

1.713

2.444

3.102

3.696

4.231

4.712

5.146

5.537

5,889

6.207

6.492

6.750

6.982

7.191

7.379

7.549

7.702

7.839

7.963

8.422

12% 13%

0.893 0.885

1.690 1.668

2.402 2.361

3.037 2.974

3.605 3.517

4.111 3.998

4.564 4.423

4.968 4.799

5.328 5.132

5.650 5.426

5.938 5.687

6.194 5.918

6.424 6.122

6.628 6.302

6.811 6.462

6.974 6.604

7.120 6.729

7.250 6.840

7.366 · 6.938

7.469 7.025

7.843, 7.330

14%

0.877

1.647

2.322

2.914

3.433

3.889

4.288

4.639

4.946

5.216

5.453

5.660

5.842

6.002

6.142

6.265

6.373

6.467

6.550

6.623

6.873

15%

0.870

1,626

2.283

2.855

3.352

3.784

4.160

4.487

4.772

5.019

5.234

5.421

5.583

5.724

5.847

5.954

6.047

6.128

6.198

6.259

6.464

16%

0.862

1.605

2.246

2.798

3.274

3,685

4.039

4.344

4.607

4.833

5.029

5.197

5.342

5.468

5.575

5.668

5.749

5.818

5.877

5.929

6.097

17%

0.855

1.585

2.210

2.743

3.199

3.589

3.922

4.207

4.451

4.659

4.836

4.988

5.118

5.229

5.324

5.405

5.475

5.534

5.584

5.628

5.766

18%

0.847

1.566

2.174

2.690

3.127

3.498

3.812

4.078

4.303

4.494

4.656

4.793

4.910

5.008

5.092

5.162

5.222

5.273

5.316

5.353

5.467

19%1 20%

0.840 0.833

1.547 1.528

2.140 2.106.

2.639 2.589

3,058 2.991

3.410 3.326

3.706 3.605

3.954 3.837

4.163 4.031

4.339 4.192

4.486 4.327.

4.611 4.439

4.715 4.533

4.802 4.611

4.876 4.675

4.938 4.730

4.990 4.775

5.033 4.812

5.070 4.843

5.101 4,870

5.195 4.948

30 25.808 22.396 1s.6·00 17.292 15.372 13.765 12.409 11.258 10.274 9.427 8.694 8,055 7.496 7.003 6.566 6.177 5.829 5.517 5.235 4.979

35 29.409 24.999 21.487 18.665 16.374 14.498 12.948 11.655 10.567 9.644 8.855 8.176 7.586 7.070 6.617 6.215 5.858 5.539 5.251 4.992

40 32.835 27.355 23.115 19.793 17.159 15.046 13.332 11.925 10.757 9.779 8.951 8.244 7.634 7.105 6.642 6.233 5.871 5.548 5.258 4.997

50 39.196 31.424 25.730 21.482 18.256 15.762 13.801 12.233 10.962 9.915 9 042 8.304 7.675 7.133 6.661 6.246 5.880 5.554 5.262 4.999

21%

0.826

1.509

2.074·

2.540

2.926

3.245

3.508

3.726

3.905

4.054

4.177

4.2i8

4.362

4.432

4.489

4.536

4.576

4.608

4.635

4.657

4.721

4.746

4.756

4.760

4.762

22%

0.820

1.492

2.042

2.494

2.864

3.167

3.416

3.619

3.786

3.923

4.035

4.127

4.203

4.265

4.315

4.357

4.391

4.419

4.442

4.460

'4.514

4.534

4.541

4.544

4.545

23%

0.813

1.474

2.011

2.448

2.803

3.092

3.327

3.518

3,673

3.799

3.902

3.985

4.053

4.108

4.153

4.189

4.219

4.243

4.263

4.279

4.323

4.339

4.345

4.347

4.348