|

FAC601Y-FINANCIAL ACCOUNTING 200-2ND OPP-DEC 2025 |

|

|

1 Page 1 |

▲back to top |

nAm ·1BI A Un IVE RSITY

OF SCIEnCE Ano TECHnOLOGY

FACULTY OF COMMERCE, HUMAN SCIENCES AND EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING AND FINANCE

QUALIFICATION : BACHELOR OF ACCOUNTING (CHARTERED ACCOUNTANCY)

QUALIFICATION CODE: 07 BACC LEVEL: 6

COURSE CODE: FAC601Y

COURSE NAME: FINANCIAL ACCOUNTING 200

SESSION: DECEMBER 2025

PAPER: THEORY (PAPER 2)

DURATION: 150 MIN

MARKS: 100

SECOND OPPORTUNITY EXAMINATION QUESTION PAPER

EXAMINER: M E Cloete

MODERATOR: Z Stellmacher

INSTRUCTIONS

1. Answer ALL questions in blue or black ink only.

2. Read all the questions carefully before answering.

3. This paper consists of TWO questions.

4. Make sure your name and surname, student number, question number and the

date appears on the answer script.

5. Please ensure that your writing is legible, neat and presentable.

6. No programmable calculators are allowed.

7. Questions relating to the paper may be raised in the initial 30 minutes after the

start of the paper. Thereafter, candidates must use their initiative to deal with

any perceived error or ambiguities & any assumption made by the candidate

should be clearly stated.

8. Any resemblance to any people, places, organisations or anything are purely

coincidenta I.

9. Round any numbers to the nearest whole number and show all workings

clearly.

THIS QUESTION PAPER CONSISTS OF 7 PAGES (Including the front page)

1

|

|

2 Page 2 |

▲back to top |

QUESTION 1

(65 MARKS)

Shadow (Pty) Ltd ("Shadow") is a security company that specializes in supplying security cameras.

The company has a 31 December financial year end.

Contract with Gogo Inc

Shadow sells some security cameras to Gago Inc. ("Goga"), a South African company. Shadow and

Gago have been business partners for a long time, and this relationship has resulted in Goga

procuring cameras solely from Shadow.

Shadow and Gago entered into the following agreement:

■ Contract date: 19 December 2024

• Contract price: N$890 000

• Contract obligations:

o Supply of security cameras

o Installation of the security cameras at Gogo's South African branch

o Providing maintenance services for 3 years whereby Shadow will be expected to

provide backup whenever needed.

Many of Shadow's customers make use of this 3-year maintenance programme. The stand-alone

prices of the various contract components are as follows:

- Security cameras - N$ 142 499

Installation process - N$ 373 800

3-year maintenance - N$ 587 400

Delivery and installation information:

• The South African company took delivery of the security cameras on 28 December 2024

but were unable to use them until the installation team arrived at their offices to install

them.

• The installation team arrived and completed the installation on 10 January 2025.

The contact price (N$890 000) was payable by Goga in instalments as follows:

• Half the total contract price (N$445 000) was to be paid on 27 December 2024 (this

payment was received on the due date);

• The balance of the contract price is due in two equal annual instalments:

o One on 31 December 2025

o One on 31 December 2026.

This contract does not contain a significant financing component.

2

|

|

3 Page 3 |

▲back to top |

Patent held

A few years ago, Shadow purchased a patent from another security company. The details of this

patent are as follows:

Date of purchase

Cost

Expected finite useful life

Legal life

Residual value

1 January 2022

N$960 000

30 years

25 years (non-renewable)

Zero

The cost of this patent was recognized as an intangible asset and was amortized over its expected

finite useful life. However, during 2025 and after all the journals for the patent were already

processed for the year, the financial manager identified that the patent acquisition agreement had

given Shadow the legal rights for a non-renewable period of only 25 years and thus the

amortization period was inappropriate. The effect of this on profits is considered to be material

from this error.

The following is an extract of the draft statement of changes in equity for the year ended 31

December 2025, before making any necessary adjustments for the patent:

Shadow (Pty) Ltd

Statement of Changes in Equity

For the year ended 31 December 2025

Balance: 1 January 2024

Total comprehensive income: 2024

Balance: 31 December 2024

Total comprehensive income: 2025

Balance: 31 December 2025

Retained Earnings (N$)

1280 000

432 000

1712000

592 000

2 304000

3

|

|

4 Page 4 |

▲back to top |

QUESTION 1

TO BE ANSWERED ON A SEPARATE PAGE

YOU ARE REQUIRED TO:

MARKS

(a)

Define the terms as described in IFRS 15 Revenue from contracts

with customers :

• "performance obligation" and

(3)

• "distinct"

(5)

(b)

Briefly explain the application of steps 2 to 4 of revenue recognition

(20)

per IFRS 15 Revenue from contracts with customers to the contract

of Shadow with Gogo.

(c)

Prepare the journal entries for Shadow (Pty) Ltd in relation to the

(12)

contract with Gogo for the years ended 31 December 2024 and 2025.

Narrations are not required. You may ignore loss allowances.

(d)

Prepare the correcting journal entries in relation to the patent for

(9)

the year ended 31 December 2025. Narrations are not required

(e)

Prepare the following disclosure relating to the patent in the

financial statements of Shadow (Pty) Ltd for the year ended 31

December 2025 in accordance with the International Financial

Reporting Standards:

•

Correction of error note; and

(8)

•

Statement of changes in equity.

(8)

TOTAL MARKS: QUESTION 1

(Source Adaptedfrom GAAP Graded Questions 2022, SeNice & Kolitz)

(65)

4

|

|

5 Page 5 |

▲back to top |

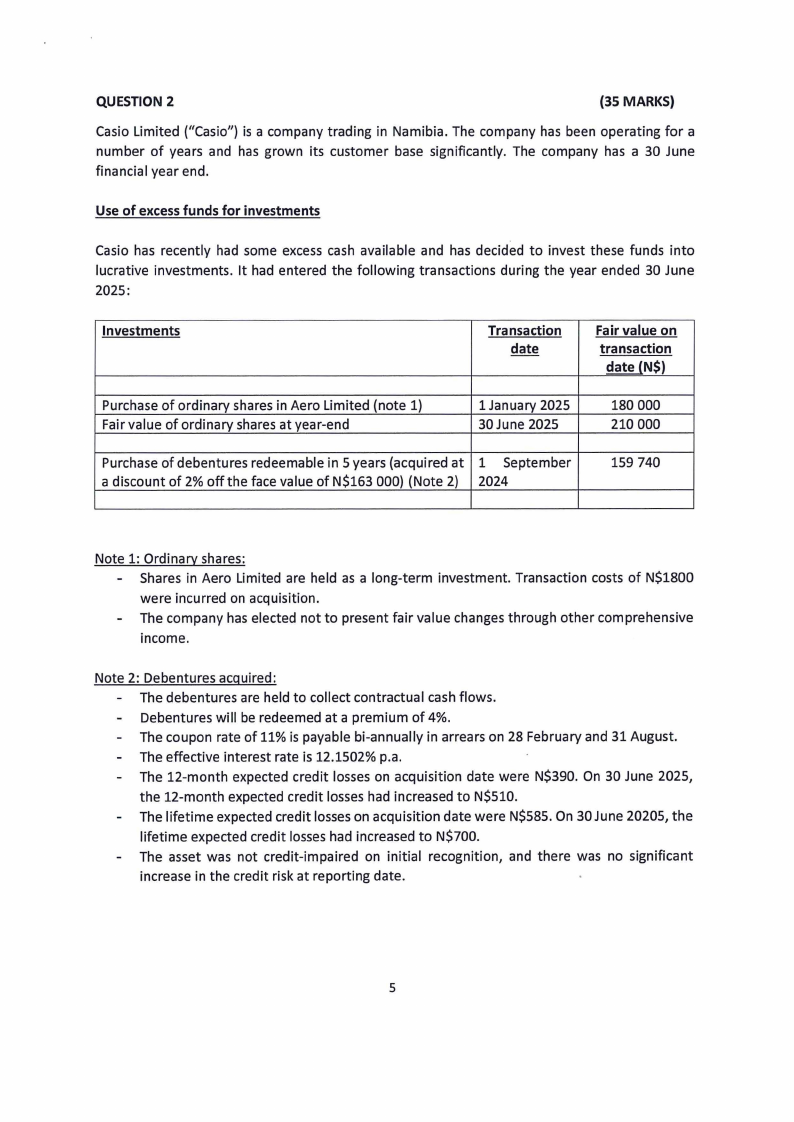

QUESTION 2

(35 MARKS)

Casio Limited ("Casio") is a company trading in Namibia. The company has been operating for a

number of years and has grown its customer base significantly. The company has a 30 June

financial year end.

Use of excess funds for investments

Casio has recently had some excess cash available and has decided to invest these funds into

lucrative investments. It had entered the following transactions during the year ended 30 June

2025:

Investments

Transaction

date

Fair value on

transaction

date (N$)

Purchase of ordinary shares in Aero Limited (note 1)

Fair value of ordinary shares at year-end

1 January 2025

30 June 2025

180 000

210 000

Purchase of debentures redeemable in 5 years (acquired at 1 September

a discount of 2% off the face value of N$163 000) (Note 2) 2024

159 740

Note 1: Ordinary shares:

- Shares in Aero Limited are held as a long-term investment. Transaction costs of N$1800

were incurred on acquisition.

- The company has elected not to present fair value changes through other comprehensive

income.

Note 2: Debentures acquired:

- The debentures are held to collect contractual cash flows.

Debentures will be redeemed at a premium of 4%.

- The coupon rate of 11% is payable bi-annually in arrears on 28 February and 31 August.

The effective interest rate is 12.1502% p.a.

- The 12-month expected credit losses on acquisition date were N$390. On 30 June 2025,

the 12-month expected credit losses had increased to N$510.

- The lifetime expected credit losses on acquisition date were N$585. On 30 June 20205, the

lifetime expected credit losses had increased to N$700.

- The asset was not credit-impaired on initial recognition, and there was no significant

increase in the credit risk at reporting date.

5

|

|

6 Page 6 |

▲back to top |

The Chief Operating Officer (COO) runs into you during lunch one day, stopping you as he knows

you are busy with the preparation of the financial statements . You inform him that the process is

long, but you are coming along well. Just before you leave, he makes the following statement:

COO: " I had a look at the draft financial statements and see that you omitted the dividend

declaration from the statement of changes in equity. Don't forget to include it! The directors plan

to authorize the financial statements on 25 August 2025 and we declared the dividend on 10

August 2025."

You: "We need to make sure that we are compliant with the principles in IFRS while preparing

these financial statements though."

COO:" I hear you but just bear that in mind. I have also heard about the concept of verifiability in

a few of our directors' meetings now, and I noticed the Conceptual Framework covers this, after

doing a bit of research thereon. What I don't understand is that if you can't reliably estimate the

useful life or residual value of PPE, how can the financial statements be verifiable?"

You: "Yes, we covered the conceptual framework in all our years while studying, the concept is

actually quite easy. Let me prepare a memo for you addressing your above points, that way you

have something to refer to when you are in your meetings."

COO: "That would be great!"

6

|

|

7 Page 7 |

▲back to top |

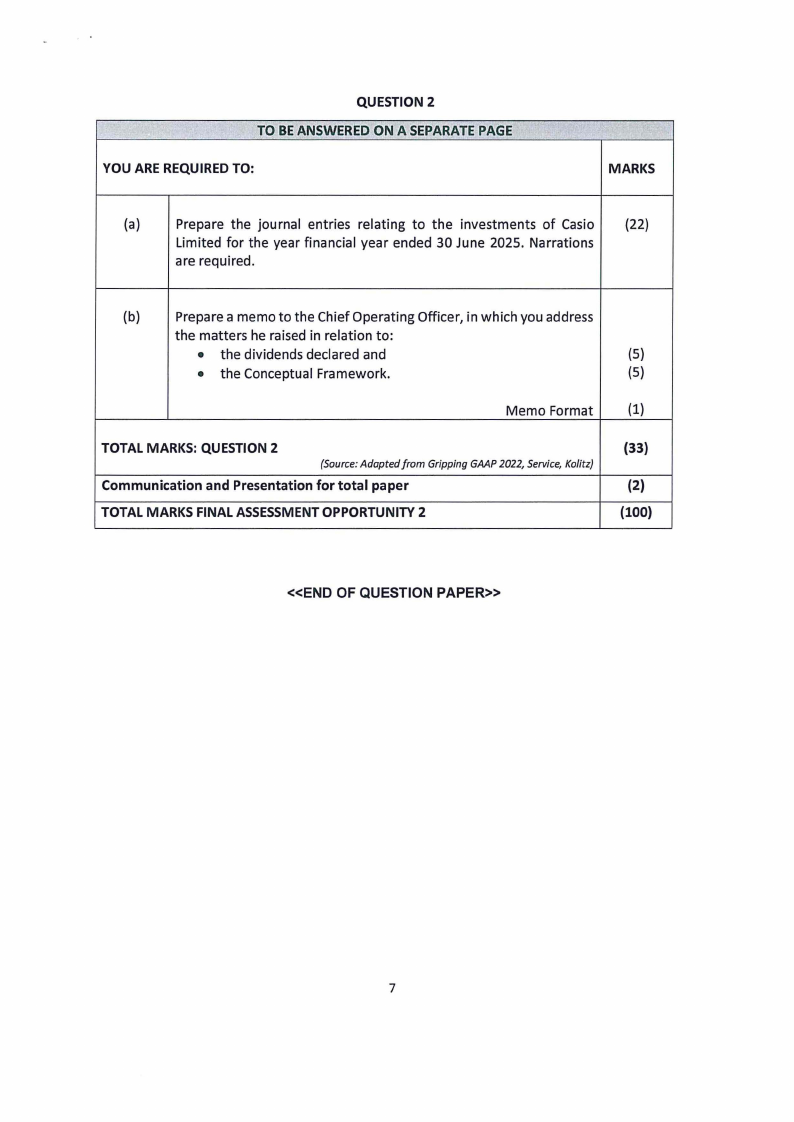

QUESTION 2

TO BE ANSWERED ON A SEPARATE PAGE

YOU ARE REQUIRED TO:

MARKS

(a)

Prepare the journal entries relating to the investments of Casio (22)

Limited for the year financial year ended 30 June 2025. Narrations

are required.

(b)

Prepare a memo to the Chief Operating Officer, in which you address

the matters he raised in relation to:

• the dividends declared and

(5)

• the Conceptual Framework.

(5)

Memo Format (1)

TOTAL MARKS: QUESTION 2

(Source: Adoptedfrom Gripping GAAP 2022, Service, Kolitz)

Communication and Presentation for total paper

TOTAL MARKS FINAL ASSESSMENT OPPORTUNITY 2

(33)

(2)

(100)

<<END OF QUESTION PAPER>>

7