|

FAC601Y-FINANCIAL ACCOUNTING 200-1ST OPP-NOV 2025 |

|

|

1 Page 1 |

▲back to top |

nAmlBIA unlVERSITY

OF SCIEnCE Ano TECHnOLOGY

FACULTY OF COMMERCE, HUMAN SCIENCES AND EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING AND FINANCE

QUALIFICATION : BACHELOR OF ACCOUNTING (CHARTERED ACCOUNTANCY)

QUALIFICATION CODE: 07 BACC LEVEL: 6

COURSE CODE: FAC601Y

COURSE NAME: FINANCIAL ACCOUNTING 200

SESSION: NOVEMBER 2025

PAPER: THEORY AND PRACTICAL

DURATION: 150 MIN

MARKS: 100

FIRST OPPORTUNITY EXAMINATION QUESTION PAPER

EXAMINER: ME Cloete

MODERATOR: Z Stellmacher

INSTRUCTIONS

1. Answer ALL questions in blue or black ink only.

2. This paper consists of THREE questions.

3. Write clearly and neatly.

4. Start each question on a new page and number the answers clearly.

5. No programmable calculators are allowed.

6. Questions relating to the paper may be raised in the initial 30 minutes after the

start of the paper. Thereafter, candidates must use their initiative to deal with

any perceived error or ambiguities & any assumption made by the candidate

should be clearly stated.

7. Any resemblance to any people, places, organisations or anything are purely

coincidenta I.

8. Round any numbers to the nearest whole number and show all workings

clearly.

THIS QUESTION PAPER CONSISTS OF 8 PAGES (Including the front page)

1

|

|

2 Page 2 |

▲back to top |

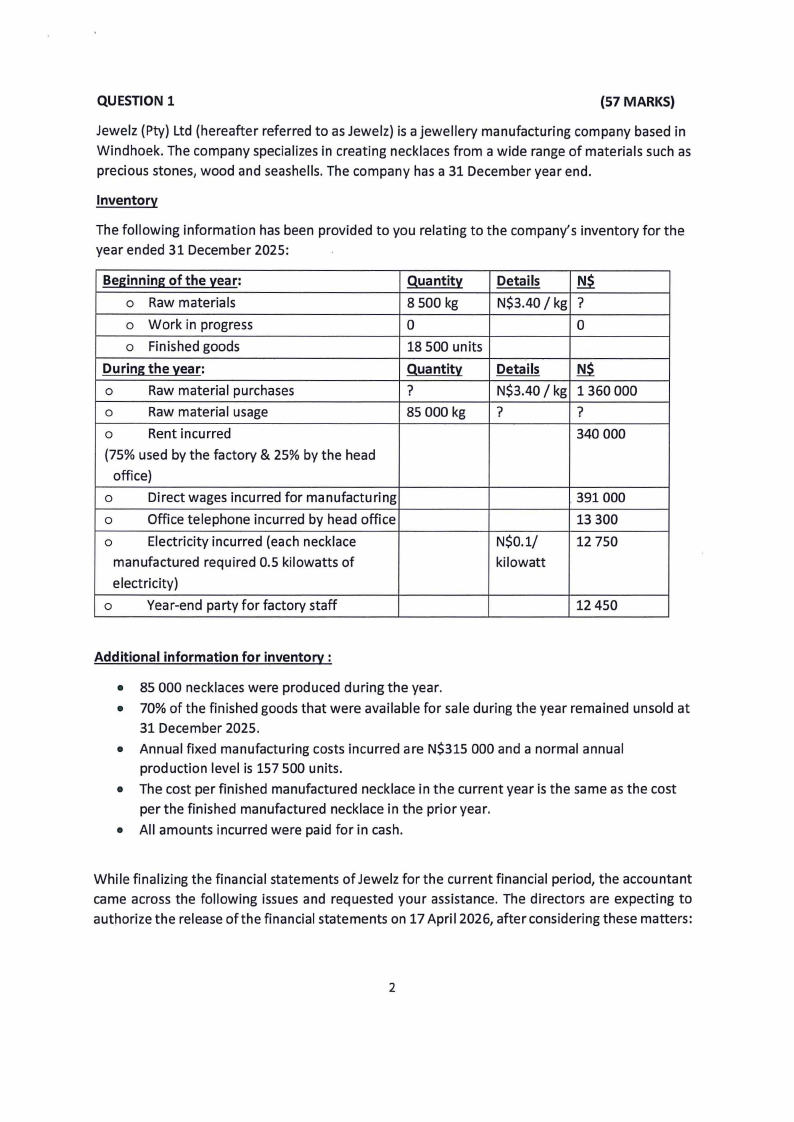

QUESTION 1

(57 MARKS)

Jewelz (Pty) Ltd (hereafter referred to as Jewelz) is a jewellery manufacturing company based in

Windhoek. The company specializes in creating necklaces from a wide range of materials such as

precious stones, wood and seashells. The company has a 31 December year end.

Inventory

The following information has been provided to you relating to the company's inventory for the

year ended 31 December 2025:

Beginning of the year:

Quantity

Details

~

0 Raw materials

8 500 kg

N$3.40 / kg ?

0 Work in progress

0

0

0 Finished goods

18 500 units

During the year:

0

Raw material purchases

Quantity

?

Details

~

N$3.40 / kg 1360 000

0

Raw material usage

85 000 kg ?

?

0

Rent incurred

340 000

(75% used by the factory & 25% by the head

office)

0

Direct wages incurred for manufacturing

. 391000

0

Office telephone incurred by head office

13 300

0

Electricity incurred (each necklace

N$0.1/

12 750

manufactured required 0.5 kilowatts of

kilowatt

electricity)

0

Year-end party for factory staff

12 450

Additional information for inventory :

• 85 000 necklaces were produced during the year.

• 70% of the finished goods that were available for sale during the year remained unsold at

31 December 2025.

• Annual fixed manufacturing costs incurred are N$315 000 and a normal annual

production level is 157 500 units.

• The cost per finished manufactured necklace in the current year is the same as the cost

per the finished manufactured necklace in the prior year.

• All amounts incurred were paid for in cash.

While finalizing the financial statements of Jewelz for the current financial period, the accountant

came across the following issues and requested your assistance. The directors are expecting to

authorize the release of the financial statements on 17 April 2026, after considering these matters:

2

|

|

3 Page 3 |

▲back to top |

Audit invoice

An invoice from the auditors for N$235 000 was received on 20 February 2026, relating to the

audit of Jewelz' financial statements for the year ended 31 December 2025.

The invoice stated that the audit work was completed as follows:

•

75% of the audit work was performed before 31 December 2025; and

•

25% of the audit work was completed during January 2026.

•

Jewelz has not provided for any part of these audit fees at 31 December 2025.

Investment in shares

Jewelz owns 35 000 shares in Ringz Limited, a company listed on the New York Stock Exchange

NYSE). At 31 December 2025, the market price of each share was N$9.35.

During March 2026, a President Trump made some political changes which resulted in the share

price dropping dramatically to N$4.15 per share. The investment in shares as at 31 December 2025

has not been adjusted for the drop in share price.

Packaging equipment

Jewelz has packaging equipment in its factory that was purchased on 1 January 2023, at a cost of

N$ 1740000. The equipment originally had an estimated useful life of 6 years and was depreciated

to a nil residual value on the straight-line basis.

On 1 January 2025, the total useful life of the equipment was re-estimated to 8 years. Jewelz uses

the re-allocation method to account for changes in accounting estimates.

QUESTION 1

TO BE ANSWERED ON A SEPARATE PAGE

YOU ARE REQUIRED TO:

MARKS

(a)

With regards to the inventory information provided, calculate the

following:

i)

Budgeted fixed manufacturing cost application rate

(1)

ii)

Fixed manufacturing costs allocated to work-in-progress

(1)

iii) Total manufacturing cost per unit

(5)

3

|

|

4 Page 4 |

▲back to top |

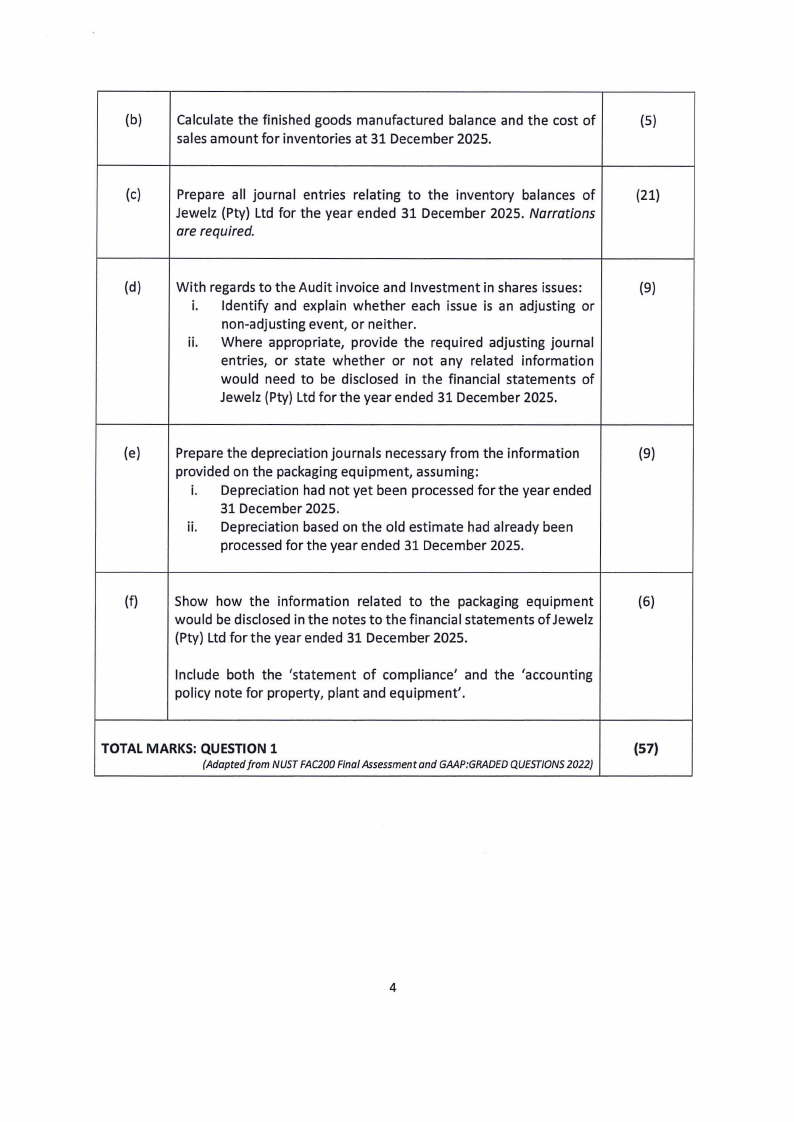

(b}

Calculate the finished goods manufactured balance and the cost of

(5}

sales amount for inventories at 31 December 2025.

(c}

Prepare all journal entries relating to the inventory balances of

(21}

Jewelz (Pty} Ltd for the year ended 31 December 2025. Narrations

are required.

(d}

With regards to the Audit invoice and Investment in shares issues:

(9}

i. Identify and explain whether each issue is an adjusting or

non-adjusting event, or neither.

ii. Where appropriate, provide the required adjusting journal

entries, or state whether or not any related information

would need to be disclosed in the financial statements of

Jewelz (Pty} Ltd for the year ended 31 December 2025.

(e}

Prepare the depreciation journals necessary from the information

(9}

provided on the packaging equipment, assuming:

i. Depreciation had not yet been processed for the year ended

31 December 2025.

ii. Depreciation based on the old estimate had already been

processed for the year ended 31 December 2025.

(f}

Show how the information related to the packaging equipment

(6)

would be disclosed in the notes to the financial statements of Jewelz

(Pty} Ltd for the year ended 31 December 2025.

Include both the 'statement of compliance' and the 'accounting

policy note for property, plant and equipment'.

TOTAL MARKS: QUESTION 1

{Adapted /ram NUST FAC200 Final Assessment and GMP:GRADED QUESTIONS 2022)

(57)

4

|

|

5 Page 5 |

▲back to top |

QUESTION 2

(15 MARKS)

Sports Limited (Ltd) is a small manufacturer of various sporting balls, operating in Oshakati. The

products of Sports Ltd include golf balls, tennis balls, rugby and soccer balls. The company has a

31 August financial year end. You have been presented with the below list of balances for the

reporting periods ending 31 August 2025 and 2024.

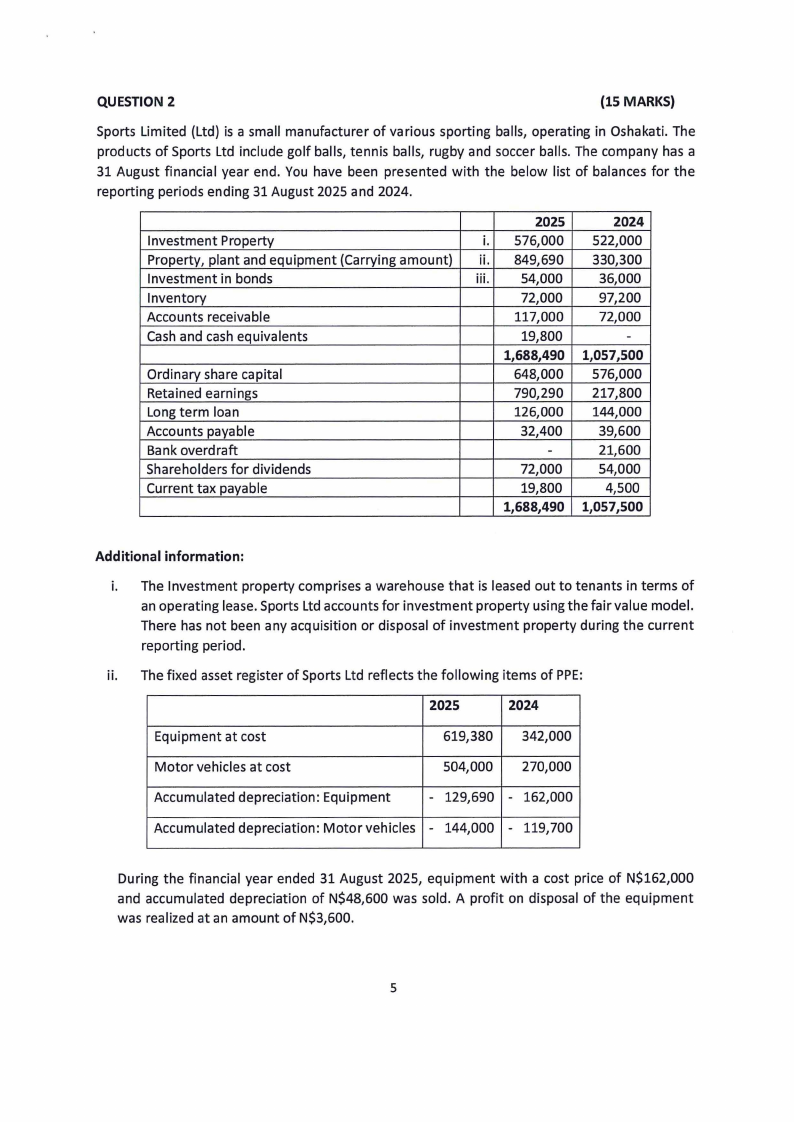

Investment Property

Property, plant and equipment (Carrying amount)

Investment in bonds

Inventory

Accounts receivable

Cash and cash equivalents

Ordinary share capital

Retained earnings

Long term loan

Accounts payable

Bank overdraft

Shareholders for dividends

Current tax payable

2025

i. 576,000

ii. 849,690

iii. 54,000

72,000

117,000

19,800

1,688,490

648,000

790,290

126,000

32,400

-

72,000

19,800

1,688,490

2024

522,000

330,300

36,000

97,200

72,000

-

1,057,500

576,000

217,800

144,000

39,600

21,600

54,000

4,500

1,057,500

Additional information:

i. The Investment property comprises a warehouse that is leased out to tenants in terms of

an operating lease. Sports Ltd accounts for investment property using the fair value model.

There has not been any acquisition or disposal of investment property during the current

reporting period.

ii. The fixed asset register of Sports Ltd reflects the following items of PPE:

2025

2024

Equipment at cost

619,380 342,000

Motor vehicles at cost

504,000 270,000

Accumulated depreciation: Equipment

- 129,690 - 162,000

- Accumulated depreciation: Motor vehicles 144,000 - 119,700

During the financial year ended 31 August 2025, equipment with a cost price of N$162,000

and accumulated depreciation of N$48,600 was sold. A profit on disposal of the equipment

was realized at an amount of N$3,600.

5

|

|

6 Page 6 |

▲back to top |

iii. The investment in bonds is a long-term investment the generates interest income on an

annual basis. The income from the investments in the current reporting period amounted

to N$15,300. Investment income from government bonds is classified as income from

operating activities.

iv. Dividends declared during the period amounted to N$63,000

v. Current tax for the period amounted to N$313,110

vi. Revenue and cost of sales and other operating expenses amounted to N$1,440,000,

N$360,000 and N$148, 770 respectively.

vii. Total finance cost for the reporting period ended 31 August 2025 amounted to N$14,940.

viii. Profit before tax has correctly been determined at N$948,600.

QUESTION 2

t,,

TO BE ANSWERED ON A SEPARATE PAGE

YOU ARE REQUIRED TO:

MARKS

(a)

Prepare the cash flows from Operating activities section of the (15)

statement of cashflows of Sports Limited for the reporting period

ended 31 August 2025 in compliance with IAS 7 Statement of

cashflows using the indirect method. Show all workings.

TOTAL MARKS: QUESTION 2

(Source: Adaptedfrom NUST Assessment)

(15)

6

|

|

7 Page 7 |

▲back to top |

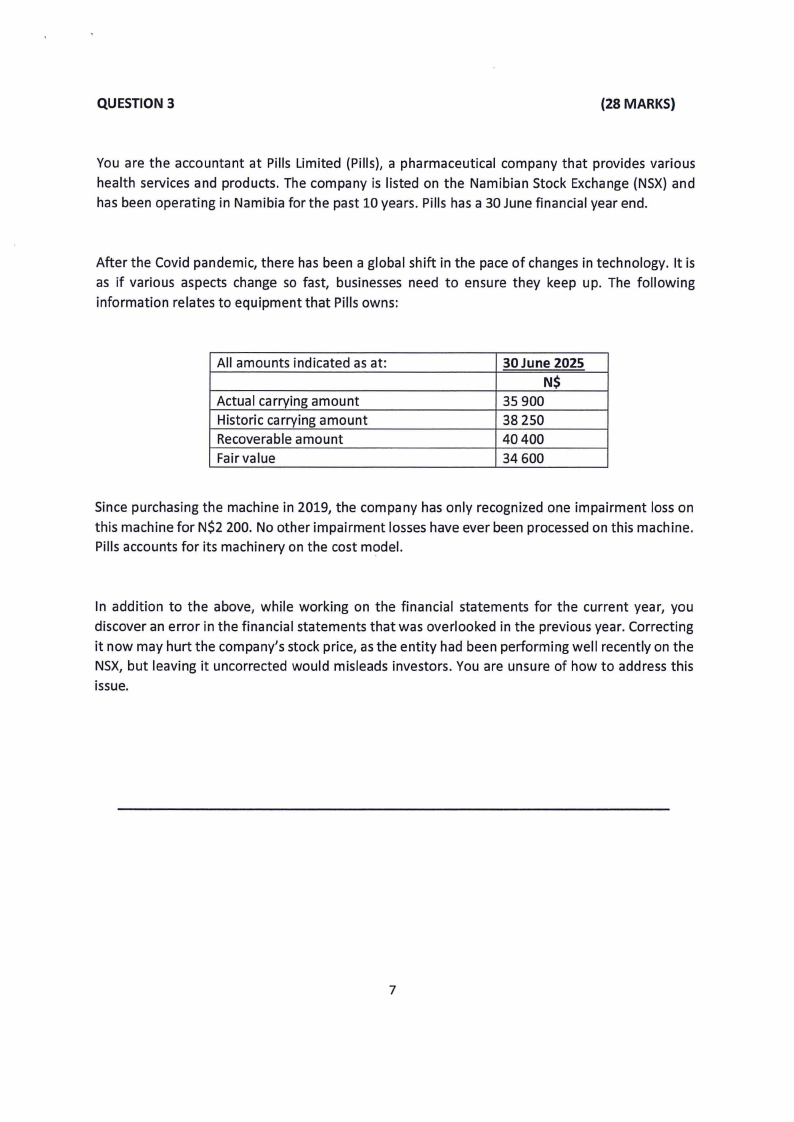

QUESTION 3

(28 MARKS}

You are the accountant at Pills Limited (Pills), a pharmaceutical company that provides various

health services and products. The company is listed on the Namibian Stock Exchange (NSX} and

has been operating in Namibia for the past 10 years. Pills has a 30 June financial year end.

After the Covid pandemic, there has been a global shift in the pace of changes in technology. It is

as if various aspects change so fast, businesses need to ensure they keep up. The following

information relates to equipment that Pills owns:

All amounts indicated as at:

Actual carrying amount

Historic carrying amount

Recoverable amount

Fair value

30June 2025

N$

35 900

38 250

40400

34600

Since purchasing the machine in 2019, the company has only recognized one impairment loss on

this machine for N$2 200. No other impairment losses have ever been processed on this machine.

Pills accounts for its machinery on the cost model.

In addition to the above, while working on the financial statements for the current year, you

discover an error in the financial statements that was overlooked in the previous year. Correcting

it now may hurt the company's stock price, as the entity had been performing well recently on the

NSX, but leaving it uncorrected would misleads investors. You are unsure of how to address this

issue.

7

|

|

8 Page 8 |

▲back to top |

QUESTION 3

TO BE ANSWERED ON A SEPARATE PAGE

YOU ARE REQUIRED TO:

I

MARKS

(a)

In general, explain which cash flows should be included in a value-in-

(4)

use calculation.

(b)

Prepare the journal entries relating to the impairment of the

(2)

machine processed for its first impairment loss. Dates and narrations

are not required.

(c)

Discuss at what amount the machine will be recorded for the

financial year ended 30 June 2025. Additionally, provide the journal (11)

entries that will be processed relating to the machine for the 2025

financial year (do not concern yourself with any depreciation

journals). Narrations are required.

(d)

In general, list and describe 3 factors that can lead to the reversal of

(6)

an impairment loss previously recognized?

(e)

With regards to the error identified in the financial statements from

(3)

the prior year, discuss what your professional ethics obligation is.

TOTAL MARKS: QUESTION 3

(Source: Adaptedfrom Gripping GAAP 2022, Service, Kolitz)

Communication and Presentation for total paper

TOTAL MARKS FINAL ASSESSMENT OPPORTUNITY 1

(26)

(2)

(100)

<<END OF QUESTION PAPER>>

8