|

AEM810S-APPLIED ACONOMETRICS QP JULY 2024 |

|

|

1 Page 1 |

▲back to top |

nAmI BI A un IVERSITY

OF SCIEnCE Ano TECHnDLOGY

FACULTY OF COMMERCE, HUMAN SCIENCES AND EDUCATION

DEPARTMENT OF ECONOMICS ACCOUNTING AND FINANCE

QUALIFICATION: BACHELOR OF ECONOMICS HONOURS DEGREE

QUALIFICATION CODE: 08HECO

LEVEL:

8

COURSE CODE:

AEM810S

COURSE NAME: APPLIED ECONOMETRICS

SESSION:

2024

PAPER:

THEORY

DURATION:

3 HOURS

MARKS:

100

SECONDOPPORTUNITYQUESTIONPAPER

EXAMINER(S) Prof. Tafirenyika Sunde

MODERATOR: Dr. Reinhold Kamati

INSTRUCTIONS

1. Answer all questions.

2. Write clearly and neatly.

3. Number the answers.

PERMISSIBLEMATERIALS

1. Ruler

2. calculator

THIS QUESTIONPAPER CONSISTSOF 6 PAGES

1

|

|

2 Page 2 |

▲back to top |

QUESTION 1 [25 marks]

(a) Given the following distributed lag model:

GDP= a+ ~0 PCEr + ~1 PCEr-i + ~2 PCEr-z + ...+ ~pPCEr-p + µt

i) Please explain how you can use it to determine the lag length of the

independent variable.

[3)

ii) What is the short-run or impact multiplier?

[3)

iii) What is the long run or total distributed lag multiplier?

[3)

iv) What is the proportion of the long run felt after one period?

[3)

v) What is the proportion of the long run felt after period p?

[3)

(b) Use Y as the dependent variable and X and Z as the independent

variables to answer the following questions:

i) Specify the long-run model.

[2]

ii) Specify the static error correction model.

[4)

iii) Specify the dynamic error correction model.

[4)

QUESTION 2 [25 marks]

Explain all steps taken to apply the cointegration and error correction

modelling (ECM) technique. Assume that the dependent variable is Gross

Domestic Product (Y), and the independent variables are Capital (K) and

Labour (L).

a) What order of integration of the variables is appropriate to run this

model?

[2)

b) Specify the long-run equation with an intercept and no trend.

[5)

c) Explain how you generate the errors and use them to test for

cointegration (state the hypothesis and decision rule for the

cointegration test).

[6)

d) If there is no cointegration, what do you do?

[2]

e) If there is cointegration among the variables, state the model you

estimate.

[5]

f) Which parameters in your model are short-run, and which parameters

are long-run?

[5]

2

|

|

3 Page 3 |

▲back to top |

QUESTION 3 [25 marks]

(a) Suppose you want to test for the Dynamic Granger causality between

GDP (Y) and money supply (M), whose model is given as follows:

L L n

n

LiYc=Ao+

AliLiYc-i + AziLiMc-1 + A3Eu-1 + µlt

(1)

i=l

i=l

L L n

n

LiMc = <po+ <p1iLiYt-i+ <pziLiMc-1+ <p3Ezt-1+ µzt

(2)

i=l

i=l

a) State the hypothesis and decision rule used when testing whether

money supply Granger causes GDP.

[5]

b) State the hypothesis and decision rule used when testing whether

GDP Granger causes Money Supply.

[5]

c) State the joint Granger causality hypotheses for the two equations. [5]

d) State the conditions that must be met in this VAR model to have

feedback causality.

[5]

e) State the conditions that must be met in this VAR model to have

unidirectional causality running from M to Y.

[5]

QUESTION 4 [25 marks]

Use the estimated model below in Table 1 to answer the following questions:

a) State the econometrics method used to obtain these results.

[1]

b) What is the order of integration of the variables used in the model? [1]

c) Is the estimated model over-parameterized or parsimonious?

[ 1]

d) Interpret the DW statistic in each of the estimated models.

[3]

e) Comment on all the possible Granger causality relationships you observe

in the results.

[7]

3

|

|

4 Page 4 |

▲back to top |

Table 1

System: UNTITLED

Estimation Method: Least Squares

Date: 06/03/21 Time: 15:55

Sample: 1993 2019

Included observations: 27

Total system (balanced) observations

Coefficient

C(2)

-0.847813

C(3)

0.610685

C(6)

0.132214

C(7)

0.030303

C(9)

-1.006227

C(l0)

0.480942

C(l3)

0.171119

C(l4)

0.039613

C(16)

-3.543975

C(l 7)

4.801334

C(l9)

-0.474299

C(20)

0.350457

81

Std. Error

0.299441

0.192159

0.065553

0.008845

0.217585

0.139630

0.047633

0.006427

1.070876

0.906802

0.186298

0.256055

t-Statistic

-2.831313

3.178019

2.016896

3.425799

-4.624524

3.444412

3.592429

6.163073

-3.309417

5.294798

-2.545917

1.368676

Prob.

0.0061

0.0022

0.0476

0.0010

0.0000

0.0010

0.0006

0.0000

0.0015

0.0000

0.0131

0.1755

Determinant residual covariance

2.65E-l l

Equation: D(LNGDP) = C(2)*D(LNGDP(-2)) + C(3)*D(LNPCE(-l)) + C(6) *D(LNPDI(-2)) + C(7)

Observations: 27

R-squared

IAdiusted R-squared

S.E. of regression

Durbin-Watson stat

0.404463

0.326784

0.017286

2.431954

Mean dependent var

S.D. dependent var

Sum squared resid

0.029535

0.021068

0.006873

Equation: D(LNPCE) = C(9)*D(LNGDP(-2)) + C(l0)*D(LNPCE(-1)) + C(l3)*D(LNPDI(-2)) + C(l4)

Observations: 27

R-squared

Adjusted R-squared

S.E. of regression

Durbin-Watson stat

0.553562

0.495331

0.012561

2.008833

Mean dependent var

S.D. dependent var

Sum squared resid

0.031553

0.017681

0.003629

Equation: D(LNPDI) = C(l6)*D(LNGDP(-2)) + C(l 7)*D(LNPCE(-l)) + C(l 9)*D(LNPDI(-l)) +

C(20)*D(LNPDI(-2))

Observations: 27

R-squared

!Adjusted R-squared

S.E. of regression

Durbin-Watson stat

0.512427

0.448831

0.076234

2.332224

Mean dependent var

S.D. dependent var

Sum squared resid

0.041603

0.102684

0.133666

4

|

|

5 Page 5 |

▲back to top |

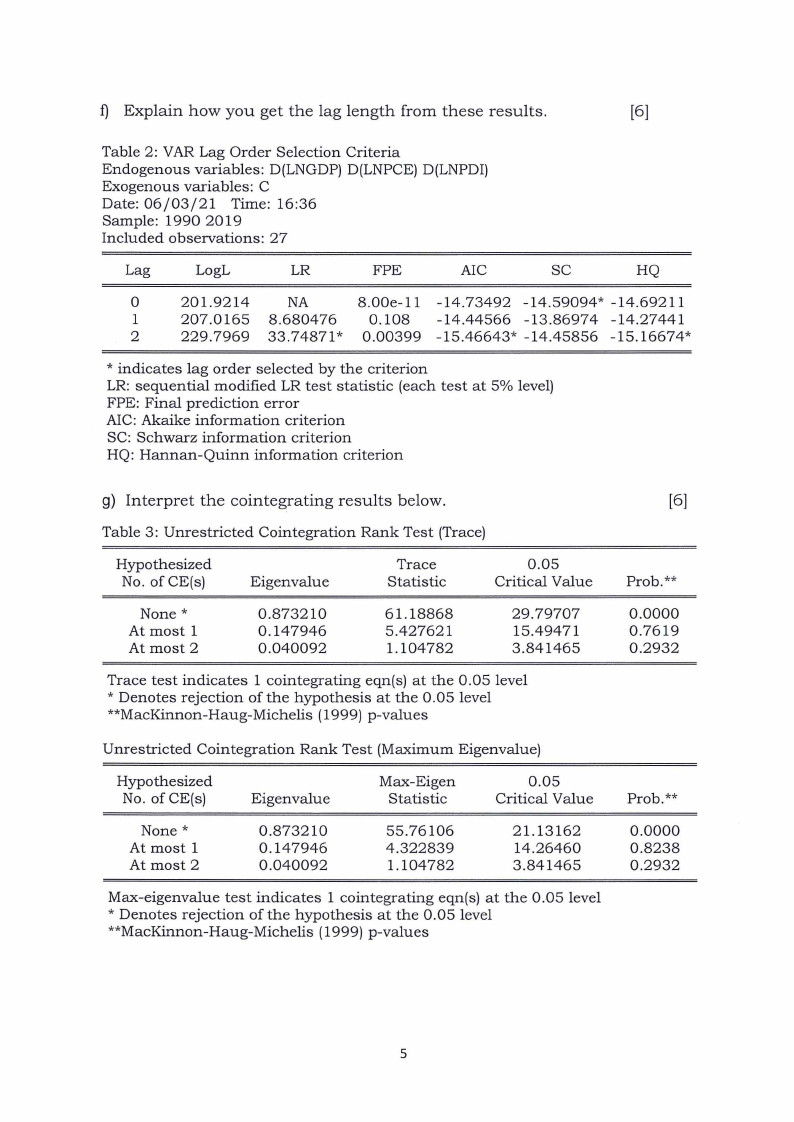

f) Explain how you get the lag length from these results.

[6]

Table 2: VAR Lag Order Selection Criteria

Endogenous variables: D(LNGDP) D(LNPCE) D(LNPDI)

Exogenous variables: C

Date: 06/03/21 Time: 16:36

Sample: 1990 2019

Included observations: 27

Lag

LogL

LR

FPE

AIC

SC

HQ

0

201.9214

NA

8.00e-11 -14.73492 -14.59094* -14.69211

1

207.0165 8.680476

0.108 -14.44566 -13.86974 -14.27441

2

229.7969 33.74871 * 0.00399 -15.46643* -14.45856 -15.16674*

* indicates lag order selected by the criterion

LR: sequential modified LR test statistic (each test at 5% level)

FPE: Final prediction error

AIC: Akaike information criterion

SC: Schwarz information criterion

HQ: Hannan-Quinn information criterion

g) Interpret the cointegrating results below.

Table 3: Unrestricted Cointegration Rank Test (Trace)

Hypothesized

No. of CE(s)

Eigenvalue

Trace

Statistic

0.05

Critical Value

None*

At most 1

At most 2

0.873210

0.147946

0.040092

61.18868

5.427621

1.104782

29.79707

15.49471

3.841465

Trace test indicates 1 cointegrating eqn(s) at the 0.05 level

* Denotes rejection of the hypothesis at the 0.05 level

**MacKinnon-Haug-Michelis (1999) p-values

Unrestricted Cointegration Rank Test (Maximum Eigenvalue)

Hypothesized

No. of CE(s)

Eigenvalue

Max-Eigen

Statistic

0.05

Critical Value

None*

At most 1

At most 2

0.873210

0.147946

0.040092

55.76106

4.322839

1.104782

21.13162

14.26460

3.841465

Max-eigenvalue test indicates 1 cointegrating eqn(s) at the 0.05 level

* Denotes rejection of the hypothesis at the 0.05 level

**MacKinnon-Haug-Michelis (1999) p-values

[6]

Prob.**

0.0000

0.7619

0.2932

Prob.**

0.0000

0.8238

0.2932

5