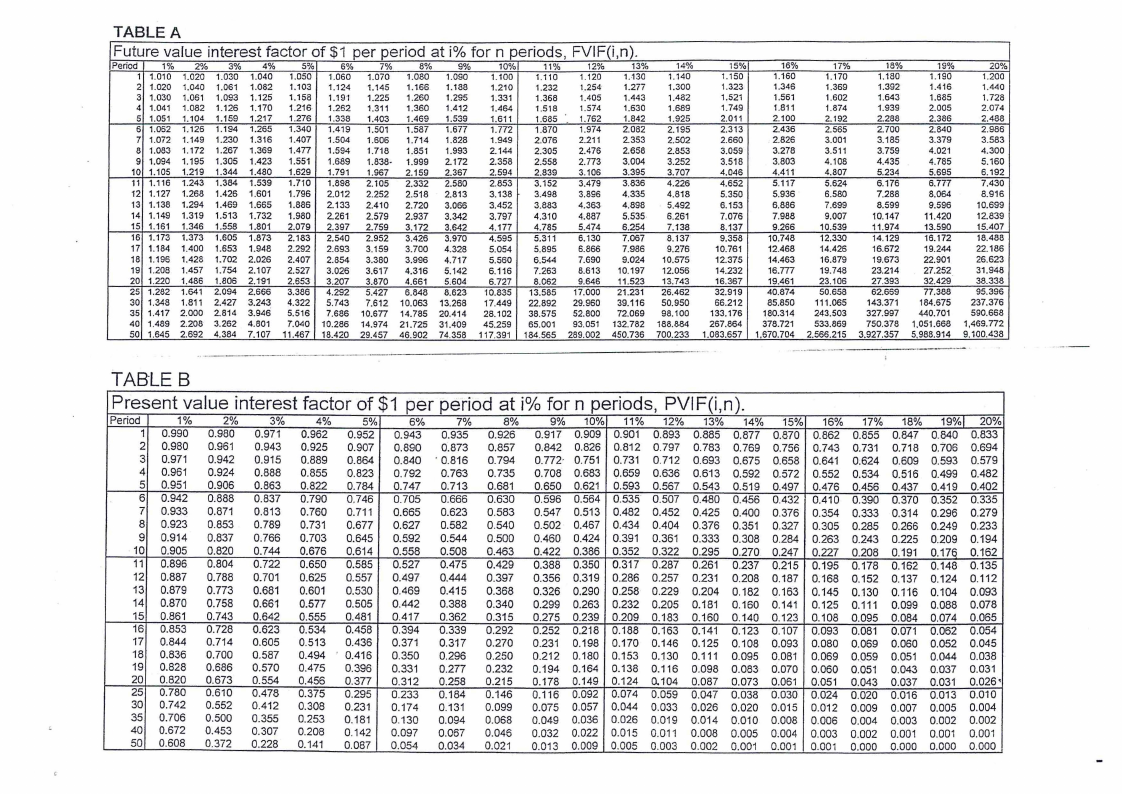

TABLE C

1-uturev.a1ue1nterest-ractoror an orainarv annu1[Yor ::,1 per p_enooat I roror nnenons, 1--VTFAfl,nl,

Period I 1%

2%

3%

4%

5%

6%

7%

8%

9% l0%

11% 12% 1-3% 14% 15% 16% 17% 18% 19% 20%

1 1,000 1.000 1,000 1.000 1,000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.QQO 1.000 1.000 1.000 1,000 1.000 1.000 I

2 2.010 2.020 2.030 2.040 2.050 2.060 2,070 2.080 2.090 2.100 2.-110 2.120 2.130 2.140 2.15.0 2.160 2.170 2.180 2.190 2.200

3 3.030 3.060 3.091 3.122 3.153 3.184 3.215 3.246 3.278 3,310 3.342 3.374 3.407 3.440 3.473 3.506 3.539 3.572 3.606 3.640

4 4,060 4.12·2 4.184 4.246 4.310 4.375 4.440 4.506 4.573 4.641 4.710 4.779 4.850 4.921 4.993 5.066 5.141 5.215 5.291 5.368

5 5.101 5.204 5.309 5.416 5,526 5.637 5.751 5.867 5.985 6.105 6.228 6.353 6.480 6:610 6.742 6.877 7.014 7.154 7.297 7.442

6 6.152 6.308 6.468 6.633 6.802 6.975 7.153 7.336 7.523 7.716 7,913 8.115 8.323 8,536 8.754 8.977 9.207 9.442 9.683 9.930

7 7.214 7.434 7.662 7.898 8.142 8.394 8.654 8.923 9.200 9.487 9.783 10.089 10.405 10.730 11.067 11:414 11.772 12.142 12.523 12:916

8 8.286 8.583 8.892 9.214 9.549 9.897 10.260 10.637 11.028 11.436 11.859 12.300 12.757 13,233 13.727 14.240 14.773 15.327 15.902 16.499

9 9.369 9.755 10.159 10.583 11.027 11.491 11.978 1-2,488 13.021 13.579 14.164 14.776 15.416 16.085 16:786 17.519 18.285. 19.086 19.923 20.799

10 10.462 10.950 11.464 12.006 12.578 13.181 13.816 14.487 15.193 15:937 16.722 17.549 18.420 19.337 20.304 21.3.21 22.393 23.521 24.709 25.959

11 11.567 12.169 12.808 130486 14.207 14.972 15,784 16.645 17.560 18.531 19.561 20.655 21.814 23.045 24.349 25.733 27.200 28.755 30.404 32.150

12 12.683 13.412 14.192 15.026 15.917 16.870 17.88_8 18.977 20.141 21.384 22.7l3 24.133 25.650 27.271 29.002 30.850 32.8.24 34.931 37.180 39,581

13 13.809 14.680 15.618 16.627 17.713 18.882 20.-141 21.495 22.953 24.523 26.212 28.029 29.985 32.089 34.352 36.786 39.404 42.219 45:244 48.497

14 14.947 15.974 17.086 18:292 19,599 21.015 22.550 24.215 26.019 27.975 30.095 32,393 34.883 37.581 40.505 43.672 47.103 50.818 54.841 59.196

15 16.097 17.293 18.599 20.024 21.579 23.276 25.129 27.152 29.361 31.772 34.405 37.280 40.417 43.842 47.580 51.660 56.110 60.965 66.261 72.035

16 17.258 18.639 20.157 21.825 23,657 25,673 27.888 30,324 33.003 35.950 39.190 42.753 46.672 50.980 55.717 60.925 66.649 72.939 79.850 87.442

17 18.430 20.012 21.762 23.698 25.840 28.213 30.840 33,750 36.974 40,545 44.501 48.884 53.739 59.118 65.075 71.673 78.979 87:068 96.022 105.93

18 19.615 21.412 23.414 25.645 28.132 30.906 33:999 37.450 41301 45.599 50.396 55.750 61.725 68.394 75,836 84.141 93.406 103.74 115.27 .128.12

19 20.811 22.841 25.117 27.671 30.539 33.760 37.379 41.446 46.018 51.159 56,939 63.440 70.749 78.969 88.212 98,603 110.28 123.41 138.17 154.74

20 22.019 24.297 26,870 29.778 33.066 36.786 40.995 45.762 51.160 57.275 64.203 72.052 80.947 91.025 102.44 115.38 130.03 146.63 165.42 186.69

25 28.243 32.030 36.459 41.646 47.727 54.865 63,249 73.106 84.701 98.347 114.41 133.33 155.62 181.87 212.79 249.21 292.10 342.60 402.04 471.98

30 34.785 40.568 47.575 56.085 66.439 79.058 94.461 113.28 136.31 164.49 199.02 241.33 293.20 356.79 434.75 530.31 647.44 790.95 966.71 1,181.9

35 41.660 49.994 60A62 73.652 90.320 111.43 138.24 172.32 215.71 271.02 341.59 431.6.6 546.68 693.57 881.17 1,120.7 1.426.5 1,816.7 2,314.2 2,948.3

40 48:886 60.402 75.401 95:026 120.80 154.76 199.64 259.06 337.88 442.59 581.83 767.09 1,013.7 1,342.0 1,779.1 2,360.8 3,t34.5 4,163.2 5,529.8 7,343.9

50 64.463 84.579 112.80 152.67 209:35 290.34 406,53 573,77 815.08 1,163.9 1,668.8 2.400:0 3,459.5 4994.5 7,217.7 10436 15090 21,813 31.515 45.497

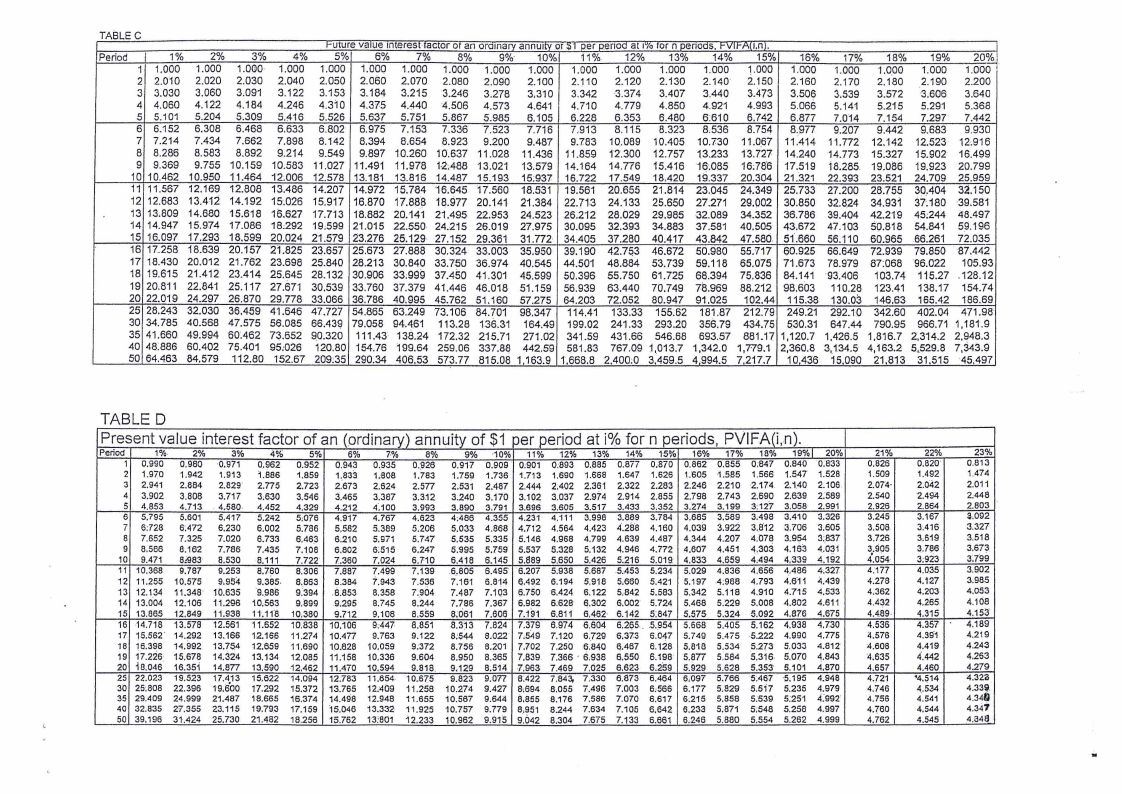

TABLED

Present value interest factor of an (ordinary) annuity of $1 oer period at i% for n periods, PVIFA(i,n).

P~riod

1

2

3

4

5

6

1%.

0:990

1.970

2.941

3.902

4.853

5,795

2%

3%

0.980 ·0.971

1.942 1.913

2.884 2.829

3,808 3.717

4.713 . 4.580-

5.601 5.417

4%

0,962

Ui86

2.775

3.630

4.452

5.242

5%

0.952

1.859

2.723

3.546

4.329

5,076

6%

0.943

1..833

2.673

3.465

4.212

4.917

7%

0..935

1:808

2,624

3.387

4·_100

4.767

8%

0,,928

1.783

2.577

3.3:12

3.993

4.623

9%

0,917

1.759

2.531

3.240

3.890

4.486

·10% 11%

0.909 - 0,901

1.736 1.713

2.487 2.444

3.170 3.102

3.791 3.696

4.355 4.231

12%

0.893

1.690

2.402

3.037

3.605

4.111

13%

0.8. 85

1.668

2.36_1

2.974

3.517

3.998

14_% 15%

0.877 0.870

1.647 1.626

2,322 2.283

2.914 2.855

3.433 3,352

3.889 3.764

16% 17%

0.862 0.855

1,"60,5 1.5135

2,246 2.210

2.798 2.743

3.274 3.199

3.685 3.589

18%

0:847

1.566

2.174

2.690

3:127

3:498

19%1 20%

0,840 ·0:033

1.547 1.528

2,1.40 2.106

2.639 2:589

3,058 2.991

3.410 3.326

7 6:728 6:472 6,230 6,0_02 5.786 5,582 5.389 5.206 5.033 4.868 4.71°2 4.564 4.423 4.2il8 4.160 4.039 :i.922 3.a12 3.706 3.605

8 7,652

9 8,566

7.325

8.162

7.020

7.786

6.733

7.435

6.463

7.108

6.210

6.802

5.971

6:515

5.747

6.247

5.535 5,335 5.146 4.968 4,799 4.639 4.487 4.344 4.207 4.078 3.954 3:.837

5:995 5.759' 5.537 5.328 5.132 4.946 4.772 4.607 4.451 4.303 4,163 4.031

10 9.471 8.:983 8.530 8.111 7.722 7,360 7.024 6. 7-10 6.418 6.145 5.S89 5.650 5.426 5.216 5.019: 4.8'j3 4.659 4.494 4,339 4,192

11 10,368 9,787 9.253 8.760 8.306 7.887 7.499 7.1.39 .6,.805 6.495 6.207 5.938 5,687 .5.453 5.234 5.029 4.836 4,656 4.486 4·,327

12 11.255 10.575 9,954 9.385, 8.,863 8.384 7,943 7.536 7,161 6.814 q.492 6.194 5.9)8 5,660 5.421 5.197 -4:988 4.793 4.611 4.439

13 12.134 11.348' 1b.635 9Jl86 9.394 8.853 8.358 7,_904 7.487 7.1Q3 6,7$0 6.424 6.122 5,842 5.583 5.342 5.118 4.910 4.715 4.533

14 13.004 12:106 1-1.296 10,563 9,899 .9.295 8.745 8,244 7.786 7.367 6.982 6:628· q.302 6.002' 5.724 5.468 5:229 5.008 4.802 4.611

15 13.86.5 12,849 11.938 1Uf8 10,380 9.712 9,108 B,559 8:061 7.606 7.191 6.811 6.462· 6.142 5:847 5.575 5,324 5.092 4.876 4.675

16 14.718 13.578 12.561 11.652 10,838 10,106 9.447 8.851 8.3~3 7.824 7.379 6.974 6,604 6,265 .. 5,954 5.668 5.405 5.162 4,938 4,7.30

17 15.562 14.292 13.166 1-2.16.6 11.274 10.477 9.763 9.122 8:544 8.022' 7.5. 49 7,120 6.729 6,373 6.047 5.749 5.475 -5.222 4,990 4.775

18 16,398 14,992 13.754 12.659 11.690 10:828 10,059 9;372 8.756 8.201 7,702 7.250 6.840 q.467 6.128 5.810 5.534 _5.-273· 5.033 4.812

19 17.226: 15.678 14.324 13.134 12.08_5 11:158 10.336 9.604 8.950 8.365 7.839 7.366 · 6.938 6.550 6.198 5.877 5.584 5.316, 5.070 4.843

20 18.046 16.351 14.877 13.590 12.462 11.470 10.594 9.818. 9,129 8.514 7,963 7.469 7.025 6,623 6,259 5,929 5.628 5,353' 5.101 4,870

25 22.023

30 25:808

35 29.409

40 32.835

19.523

22.396

24.999

27.355

17.413

19.Eioo

21.487

23.115

15.622

17.292

18.665

19.79.3

·14.094

15.372

16,374

17.159

12,783

13.765

14.498

15.046

11,654.

12.409

12,948

13.332

10.675

11.258

11.655

11.925

9.823

10.274

10.567

10.757

9.017

9.427

9.644

9.779

8:422

8,694

8,855

8,951

7.843,. 7.330

8.055 7.496

8.176 7,586

8.244 7.634

6,873

7.003

7.070

7,105

6.464

6:566

6.617

6.642

6,097

6,177

6;215

6,233

5.766

5.829

5.858

5.871

-5:457 5.195

5.5i7 5.235

5_-539 5:251

5;548 5.258

4 ..948

4.979

4:992·

4.997

50 39,196 31-.424 25,730 21.482 18.256 15.762 13'801 12.233 10.962 9.915 9.042 8,304 7.675 7.133 6.661 6.246 5.880 5,554 5.262 4.999

21%

0.826

1.509

2.074·

2.540

2.926

3.245

3.508.

3.726

3.905

4,054

4.177

4.278

4.362

4.432

4.489-

4.536

4.576

4.608

4.635

4.657

4.721

4.746

4.756

4.760

4.762

22%

0.820'

1.492

2.042

'2.494

2.864

3.167

3-.416

3,619

3.786

3:923

4.0.35

4.127

4.203

4.265

4.315

4.357

4_39·1

4.419

4.442

4.460

'4.514

4.534

4.541

4.544

4.545

23%

0.813

1.474

2.011

2.448

2.803

3.092

3.327

3.518

3.67;3.

3'.799

3.902

3.985

4.053

4.108

4.15:3

4.189

4,219

4.243

4,263

4.279

4.320

4.3311.

4.340

4.347

4.a48