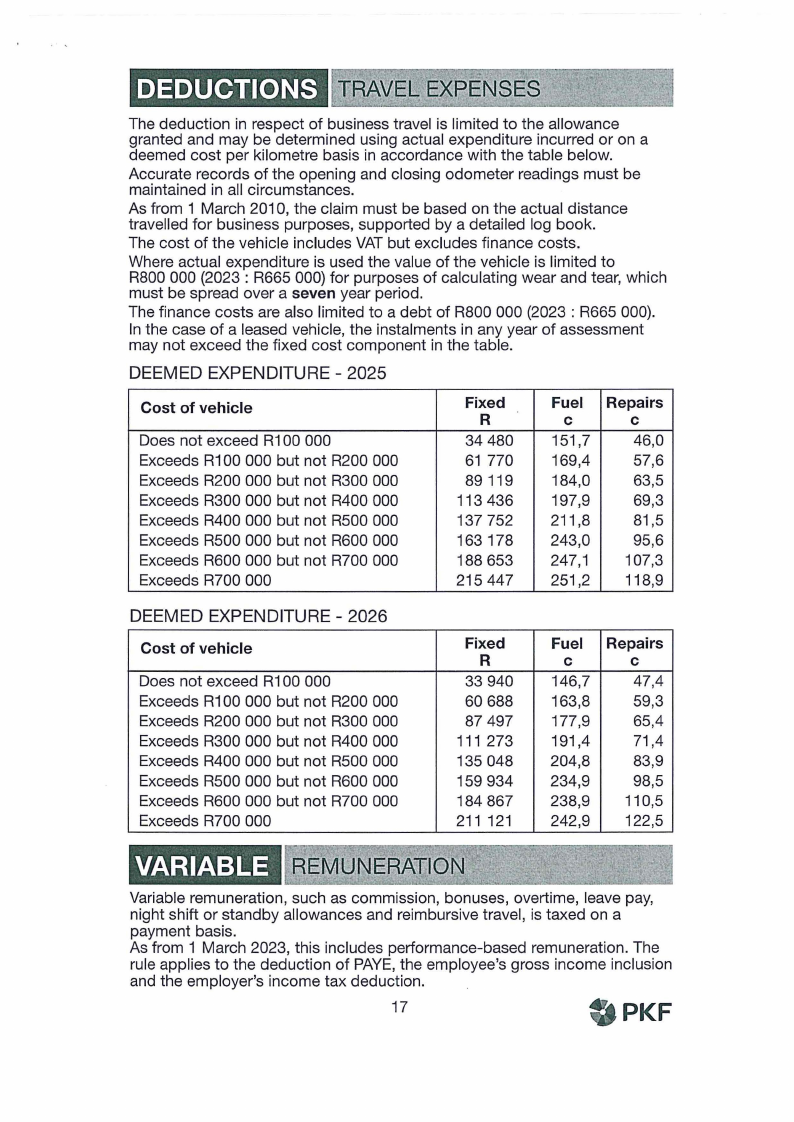

DEDUCTIONS TRAVE.L 'EXPENSES

The deduction in respect of business travel is limited to the allowance

granted and may be determined using actual expenditure incurred or on a

deemed cost per kilometre basis in accordance with the table below.

Accurate records of the opening and closing odometer readings must be

maintained in all circumstances.

As from 1 March 2010, the claim must be based on the actual distance

travelled for business purposes, supported by a detailed log book.

The cost of the vehicle includes VAT but excludes finance costs.

Where actual expenditure is used the value of the vehicle is limited to

R800 000 (2023 : R665 000) for purposes of calculating wear and tear, which

must be spread over a seven year period.

The finance costs are also limited to a debt of R800 000 (2023 : R665 000).

In the case of a leased vehicle, the instalments in any year of assessment

may not exceed the fixed cost component in the table.

DEEMED EXPENDITURE - 2025

Cost of vehicle

Does not exceed R100 000

Exceeds R100 000 but not R200 000

Exceeds R200 000 but not R300 000

Exceeds R300 000 but not R400 000

Exceeds R400 000 but not R500 000

Exceeds R500 000 but not R600 000

Exceeds R600 000 but not R700 000

Exceeds R700 000

Fixed

R

34 480

61 770

89 119

113 436

137 752

163 178

188 653

215 447

Fuel

C

151,7

169,4

184,0

197,9

211,8

243,0

247,1

251,2

Repairs

C

46,0

57,6

63,5

69,3

81,5

95,6

107,3

118,9

DEEMED EXPENDITURE - 2026

Cost of vehicle

Does not exceed R100 000

Exceeds R100 000 but not R200 000

Exceeds R200 000 but not R300 000

Exceeds R300 000 but not R400 000

Exceeds R400 000 but not R500 000

Exceeds R500 000 but not R600 000

Exceeds R600 000 but not R700 000

Exceeds R700 000

Fixed

R

33 940

60 688

87 497

111 273

135 048

159 934

184 867

211 121

Fuel

C

146,7

163,8

177,9

191,4

204,8

234,9

238,9

242,9

Repairs

C

47,4

59,3

65,4

71,4

83,9

98,5

110,5

122,5

VARIABLE REM·UN6RATION

Variable remuneration, such as commission, bonuses, overtime, leave pay,

night shift or standby allowances and reimbursive travel, is taxed on a

payment basis.

As from 1 March 2023, this includes performance-based remuneration. The

rule applies to the deduction of PAYE, the employee's gross income inclusion

and the employer's income tax deduction.

17

PKF