|

CMA612S-COST AND MANAGEMENT ACCOUNTING 202-2ND OPP-DEC 2025 |

|

|

1 Page 1 |

▲back to top |

nAmlBIA UnlVERSITY

OF SCIEnCE Ano TECHnOLOGY

FACULTY OF COMMERCE, HUMAN SCIENCE AND EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING & FINANCE

QUALIFICATION: BACHELOR OF ACCOUNTING

QUALIFICATION CODE: 07BGAC

COURSE CODE: CMA612S

LEVEL: 6

COURSE NAME: COST & MANAGEMENT

ACCOUNTING 202

SESSION: NOVEMBER/DECEMBER 2025

DURATION: 3 HOURS

PAPER: PRACTICAL AND THEORY

MARKS: 100

SECOND OPPORTUNITY EXAMINATION QUESTION PAPER

EXAMINERS: Dr M Nyakuwanika, M Modestus, T Shaalukeni & H Namwandi

MODERATOR: p Erkie

INSTRUCTIONS

• This question paper is made up of five (5) questions.

• Answer all the questions in blue or black ink only.

• You are advised to pay due attention to expression and presentation. Failure to do so

will result in a loss of marks.

• Start each question on a new page in your answer booklet and show all your workings.

• Questions relating to this paper may be raised in the initial 30 minutes after the start

of the paper. Thereafter, candidates must use their initiative to address any perceived

errors or ambiguities, and any assumptions made by the candidate should be clearly

stated.

PERMISSIBLE MATERIALS

Non-programmable calculator

THIS QUESTION PAPER CONSISTS OF 7 PAGES (Including this front page)

|

|

2 Page 2 |

▲back to top |

Question 1

(25 Marks)

Mr Tuhafeni worked as a woodwork teacher for the past thirty-five years in Windhoek. In June

2024, he decided to accept voluntary redundancy and establish a company, Vision Ltd, which

will produce and sell special types of beds in the Windhoek marketplace. The company will

commence trading on 1 January 2025. Mr Tuhafeni plans to invest all his redundancy money,

N$105,000, on January 1, 2025, into the company. Mr Tuhafeni has prepared the following

budgeted information for the first six months of trading:

(i) Sales of beds can be broken down into two categories: large wooden beds and small

wooden beds. Sales of small wooden beds will be made on a cash-only basis. Sales

of the large wooden beds will be made on a credit basis, with 50% of the sale amount

due within one month of the sale. These qualify for a 5% early settlement discount. Of

the remaining credit sales, 10% will become bad debts, and the balance will be

received equally in the second and third months after sale. Small wooden beds will

have a selling price of $150 per unit, and large wooden beds will have a selling price

of N$220 per unit. The projected sales, in units, of each are as follows:

Month

January

February

March

April

May

June

July

Sales (in units) of

Small wooden beds

50

60

50

60

70

80

00

Sales (in units) of

large wooden beds

40

60

50

40

50

70

40

(ii) Small wooden beds will be produced in the month they are sold. The variable

production cost of one small wooden bed will be N$76, which will be paid in the month

it is incurred.

(iii) Production of large wooden beds will be in the month before the sale. The production

cost of one large wooden bed will be N$130, and 60% of this amount will be paid in

the month it is incurred, with the balance due one month later.

(iv) In January, Mr Tuhafeni will purchase equipment, costing N$68,000, and this will be

paid for in April. This equipment is expected to have a useful life of five years.

Depreciation will be assumed to be on a straight-line basis.

(v) Fixed production overheads are projected at N$3,800 per month and will include the

monthly depreciation charge for the equipment.

(vi) Mr Tuhafeni has organised for a bank loan of N$35,000 to be received on 1 February.

For the first year only, Mr Tuhafeni will make a monthly interest repayment at a rate of

10% per annum . Thereafter, Mr Tuhafeni will have to start making capital repayments

on the loan.

2

|

|

3 Page 3 |

▲back to top |

(vii) Mr Tuhafeni will employ one salesperson, commencing on 1 January, who will receive

a monthly salary of N$2,500 plus sales commission of 4% of the total sales value made

during the period . The compensation will be paid in the month incurred, while the sales

commission will be paid one month in arrears.

REQUIRED:

(a) Describe three benefits a company can obtain from implementing an

effective budgeting svstem .

(b) Prepare a cash budget for Vision Ltd. for each month of the six-month

period commencing January 1, 2025, showing the closing cash balance at

the end of each month.

(c) Explain why the closing cash balance at the end of the six months will be

different from the net profit reported for the same six-month period .

Show all your workings!

Total

Marks

(6)

(15)

(4)

25

Question 2

(25 Marks)

Taku-Tau is a newly established company in the home spa industry. They produce body

lotions, scrubs, fizz balls and bath salts for sale to the general public. Taku-Tau uses a standard

absorption costing system .

The following information relates to the production of body scrubs:

Sea salt and marula oil is used to make the body scrub. These two ingredients can be used

to varying extents in the production of the scrub. The limitations are that only between 45%

and 60% of the final product may consist of oil.

Sea salt is purchased from a supplier at the coast. The budgeted cost of sea salt is N$18 per

kilogram . The following is the latest price list obtained from the supplier of sea salt:

Quantity supplied

0-100 kg

101 - 300 kg

301 -500kg

501 kg and above

Cost per kilogram

N$20

N$18

N$16

N$15

Marula oil is purchased per kilogram. The budgeted cost per kilogram of Marula oil is N$40.

Due to the drought being experienced in the country, N$43 was actually paid per kilogram of

Marula oil purchased.

Market research shows that 850 tubs of scrub will be sold during the month of December if a

price of N$45 per tub is charged. No opening or closing stock is budgeted. Based on the

budget, one tub should weigh 500 grams.

Sales were not as high as expected, and only 810 tubs were sold at a price of N$45. 830 tubs

were produced. In total 301 kilograms of sea salt was purchased. 225 kg of salt was used

during production. 200 kilograms of oil were purchased and used .

3

|

|

4 Page 4 |

▲back to top |

One plastic tub is used for every tub of scrub filled. Plastic tubs were expected to cost N$1.50,

however, another supplier had to be used and the actual cost was N$1. 70 per tub. 840 tubs

were purchased . There was no opening or closing stock of plastic tubs.

Labourers should be paid N$100 for every 8 hours worked. After various disputes with trade

unions, labourers were actually paid N$110 for every 8 hours worked. It should take 15 minutes

for one tub to be fully completed . The total actual cost of labour was N$2 905 for total

production .

The budgeted overheads were as follows:

Water and electricity

N$2 000 per month

Rental of the workspace

N$4 000 per month

The actual overheads were as follows:

Water and electricity

N$2 225 for December

Rental of workspace

N$4 000 for December

Overheads are allocated to the types of products based on the number of products produced.

In total , 5 000 units of all types of products were expected to be produced. 4 500 units were

actually produced during the month.

REQUIRED:

(a) Calculate the budgeted profit expected to be made by Taku-Tau by using

the optimal mix of salt and oil.

(b) Calculate all possible variances for Taku-Tau . Assume that Taku-Tau

would like to identify material price variances when the material is used.

(NB: Material mix and Yield variances must be included in calculations)

Show all your workings!

Total

Marks

(5)

(20)

25

Question 3

(20 Marks)

DGF manufacture two products from different combinations of the same resources. Units

selling price and unit costs details for each product are as follows:

Selling price

Direct material A (N$5 per kg)

Direct material B (N$3 per kg)

Skilled labour (N$7 per hour)

Variable overhead (N$2 per machine hour)

Fixed overheads #

Profit

D

N$ per unit

115

20

12

28

14

28

13

G

N$ per unit

120

10

24

21

18

36

11

#Fixed overheads are absorbed using an absorption rate per machine hour. This is an

unavoidable central overhead cost which is not affected by the mix or volume of products

produced .

4

|

|

5 Page 5 |

▲back to top |

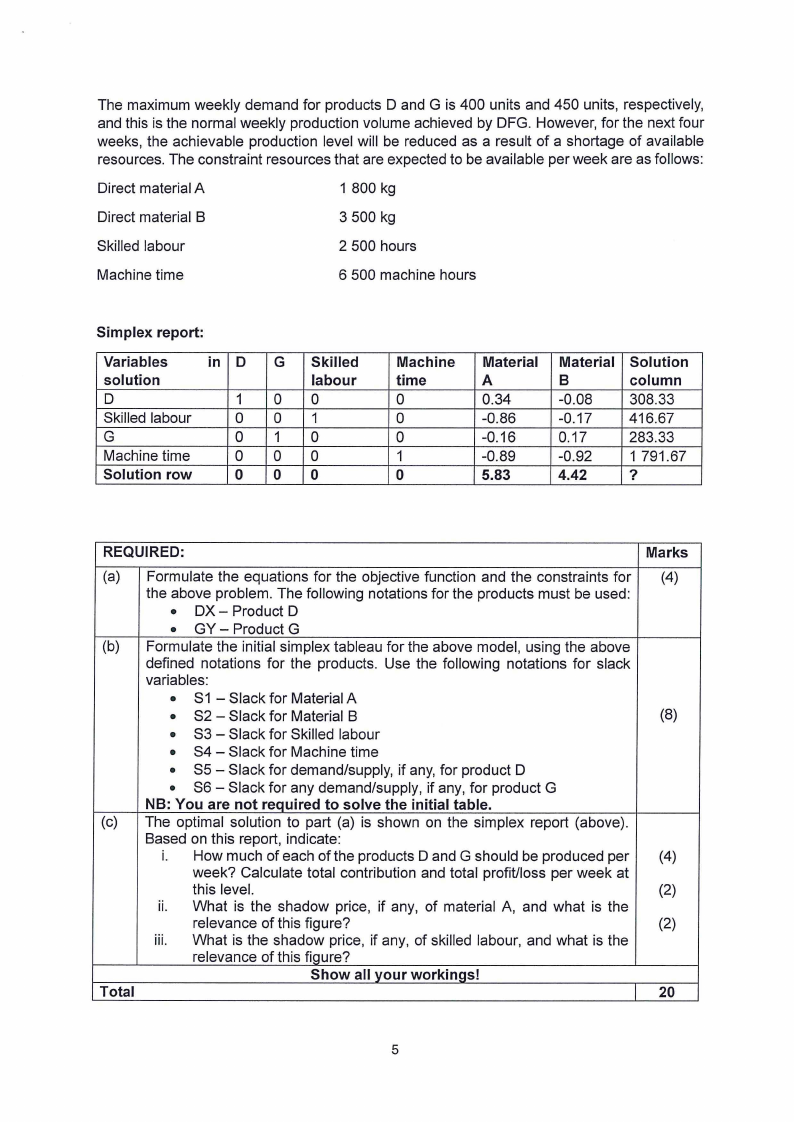

The maximum weekly demand for products D and G is 400 units and 450 units, respectively,

and this is the normal weekly production volume achieved by DFG. However, for the next four

weeks, the achievable production level will be reduced as a result of a shortage of available

resources. The constraint resources that are expected to be available per week are as follows:

Direct material A

1 800 kg

Direct material B

3 500 kg

Skilled labour

2 500 hours

Machine time

6 500 machine hours

Simplex report:

Variables

in D G Skilled

solution

labour

D

100

Skilled labour

001

G

0 10

Machine time

0 00

Solution row

0 00

Machine

time

0

0

0

1

0

Material

A

0.34

-0.86

-0.16

-0.89

5.83

Material

B

-0.08

-0.17

0.17

-0.92

4.42

Solution

column

308.33

416.67

283.33

1 791.67

?

REQUIRED:

Marks

(a) Formulate the equations for the objective function and the constraints for (4)

the above problem. The following notations for the products must be used:

• DX - Product D

• GY - Product G

(b) Formulate the initial simplex tableau for the above model, using the above

defined notations for the products. Use the following notations for slack

variables:

• S1 - Slack for Material A

• S2 - Slack for Material B

(8)

• S3 - Slack for Skilled labour

• S4 - Slack for Machine time

• S5 - Slack for demand/supply, if any, for product D

• S6 - Slack for any demand/supply, if any, for product G

NB: You are not required to solve the initial table.

(c) The optimal solution to part (a) is shown on the simplex report (above).

Based on this report, indicate:

i. How much of each of the products D and G should be produced per (4)

week? Calculate total contribution and total profit/loss per week at

this level.

(2)

ii. What is the shadow price, if any, of material A, and what is the

relevance of this figure?

(2)

iii. What is the shadow price, if any, of skilled labour, and what is the

relevance of this figure?

Show all vour workin~s!

Total

20

5

|

|

6 Page 6 |

▲back to top |

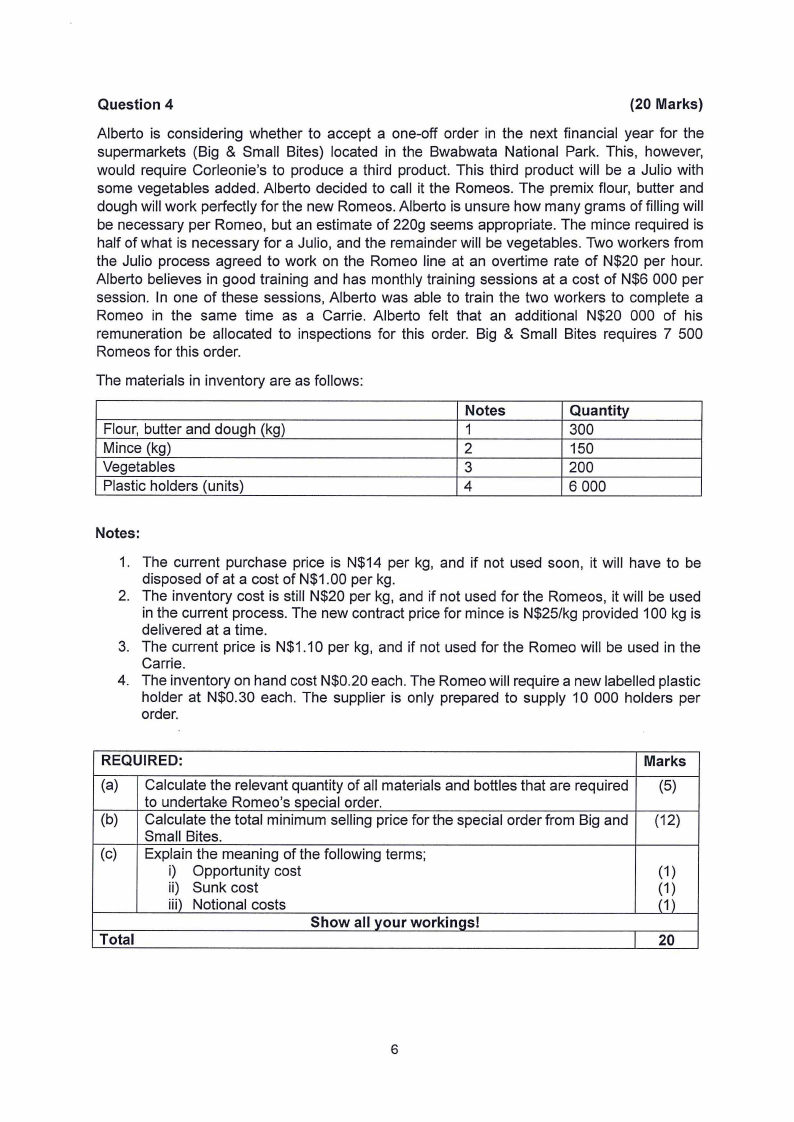

Question 4

(20 Marks)

Alberto is considering whether to accept a one-off order in the next financial year for the

supermarkets (Big & Small Bites) located in the Bwabwata National Park. This, however,

would require Corleonie's to produce a third product. This third product will be a Julio with

some vegetables added. Alberto decided to call it the Romeos. The premix flour, butter and

dough will work perfectly for the new Romeos. Alberto is unsure how many grams of filling will

be necessary per Romeo, but an estimate of 220g seems appropriate. The mince required is

half of what is necessary for a Julio, and the remainder will be vegetables. Two workers from

the Julio process agreed to work on the Romeo line at an overtime rate of N$20 per hour.

Alberto believes in good training and has monthly training sessions at a cost of N$6 000 per

session . In one of these sessions, Alberto was able to train the two workers to complete a

Romeo in the same time as a Carrie. Alberto felt that an additional N$20 000 of his

remuneration be allocated to inspections for this order. Big & Small Bites requires 7 500

Romeos for this order.

The materials in inventory are as follows:

Flour, butter and dough (kg)

Mince (kg)

Vegetables

Plastic holders (units)

Notes

1

2

3

4

Quantity

300

150

200

6 000

Notes:

1. The current purchase price is N$14 per kg , and if not used soon, it will have to be

disposed of at a cost of N$1.00 per kg.

2. The inventory cost is still N$20 per kg, and if not used for the Romeos, it will be used

in the current process. The new contract price for mince is N$25/kg provided 100 kg is

delivered at a time.

3. The current price is N$1 .1O per kg, and if not used for the Romeo will be used in the

Carrie.

4. The inventory on hand cost N$0.20 each . The Romeo will require a new labelled plastic

holder at N$0.30 each. The supplier is only prepared to supply 10 000 holders per

order.

REQUIRED:

(a) Calculate the relevant quantity of all materials and bottles that are required

to undertake Romeo's special order.

(b) Calculate the total minimum selling price for the special order from Big and

Small Bites.

(c) Explain the meaning of the following terms;

i) Opportunity cost

ii) Sunk cost

iii) Notional costs

Show all your workings!

Total

Marks

(5)

(12)

(1)

(1)

(1)

20

6

|

|

7 Page 7 |

▲back to top |

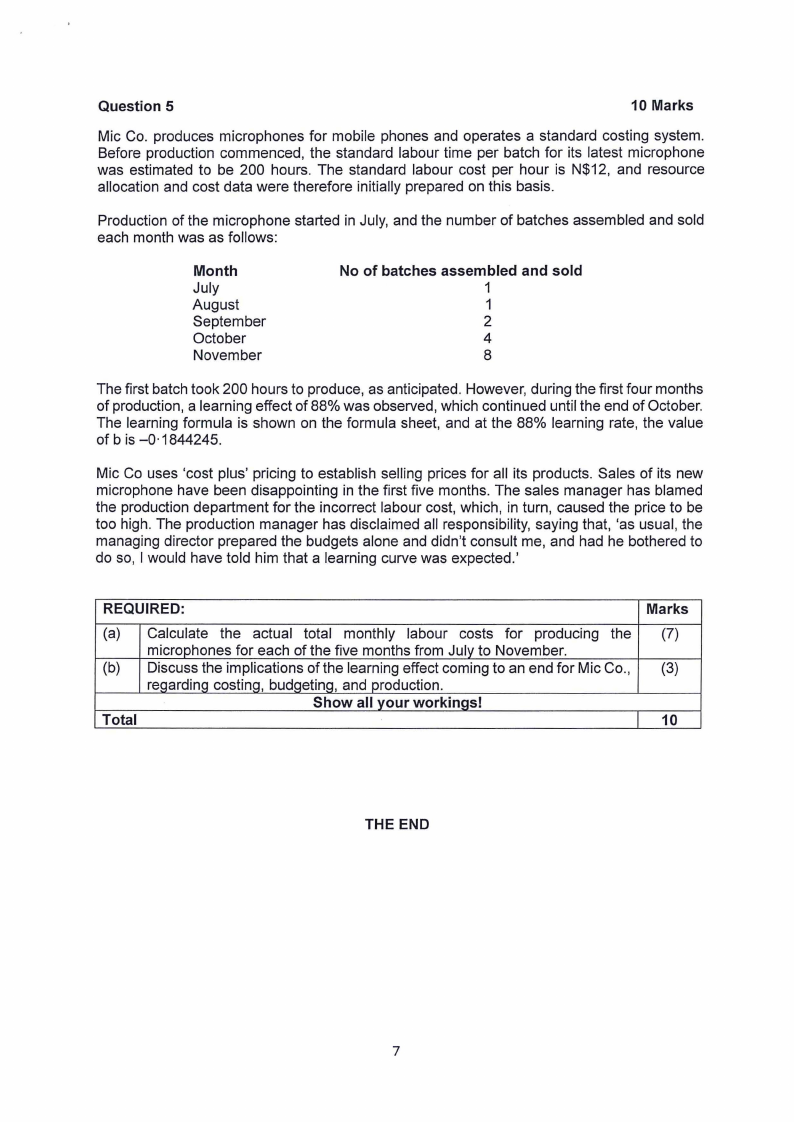

Question 5

10 Marks

Mic Co. produces microphones for mobile phones and operates a standard costing system .

Before production commenced, the standard labour time per batch for its latest microphone

was estimated to be 200 hours. The standard labour cost per hour is N$12, and resource

allocation and cost data were therefore initially prepared on this basis.

Production of the microphone started in July, and the number of batches assembled and sold

each month was as follows:

Month

July

August

September

October

November

No of batches assembled and sold

1

1

2

4

8

The first batch took 200 hours to produce, as anticipated. However, during the first four months

of production, a learning effect of 88% was observed, which continued until the end of October.

The learning formula is shown on the formula sheet, and at the 88% learning rate, the value

of bis -0·1844245.

Mic Co uses 'cost plus' pricing to establish selling prices for all its products. Sales of its new

microphone have been disappointing in the first five months. The sales manager has blamed

the production department for the incorrect labour cost, which, in turn, caused the price to be

too high. The production manager has disclaimed all responsibility, saying that, 'as usual, the

managing director prepared the budgets alone and didn't consult me, and had he bothered to

do so, I would have told him that a learning curve was expected.'

REQUIRED:

Marks

(a) Calculate the actual total monthly labour costs for producing the (7)

microphones for each of the five months from July to November.

(b) Discuss the implications of the learning effect coming to an end for Mic Co., (3)

reqardinq costinq, budgeting, and production.

Show all your workings!

Total

10

THE END

7