|

CMA612S-COST AND MANAGEMENT ACCOUNTING 202-1ST OPP-NOV 2025 |

|

|

1 Page 1 |

▲back to top |

nAmlBIA unlVERSITY

OF SCIEnCE Ano TECHnOLOGY

FACULTY OF COMMERCE, HUMAN SCIENCE AND EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING & FINANCE

QUALIFICATION: BACHELOR OF ACCOUNTING

QUALIFICATION CODE: 07BGAC

COURSE CODE: CMA612S

LEVEL: 6

COURSE NAME: COST & MANAGEMENT

ACCOUNTING 202

SESSION: OCTOBER 2025

DURATION: 3 HOURS

PAPER: PRACTICAL AND THEORY

MARKS: 100

FIRST OPPORTUNITY EXAMINATION QUESTION PAPER

EXAMINERS: Dr M Nyakuwanika, M Modestus, T Shaalukeni & H Namwandi

MODERATOR: p Erkie

INSTRUCTIONS

• This question paper is made up of five (5) questions.

• Answer all the questions in blue or black ink only.

• You are advised to pay due attention to expression and presentation. Failure to do so

will result in a loss of marks.

• Start each question on a new page in your answer booklet and show all your workings.

• Questions relating to this paper may be raised in the initial 30 minutes after the start

of the paper. Thereafter, candidates must use their initiative to address any perceived

errors or ambiguities, and any assumptions made by the candidate should be clearly

stated.

PERMISSIBLE MATERIALS

Non-programmable calculator

THIS QUESTION PAPER CONSISTS OF 6 PAGES (Including this front page)

1

|

|

2 Page 2 |

▲back to top |

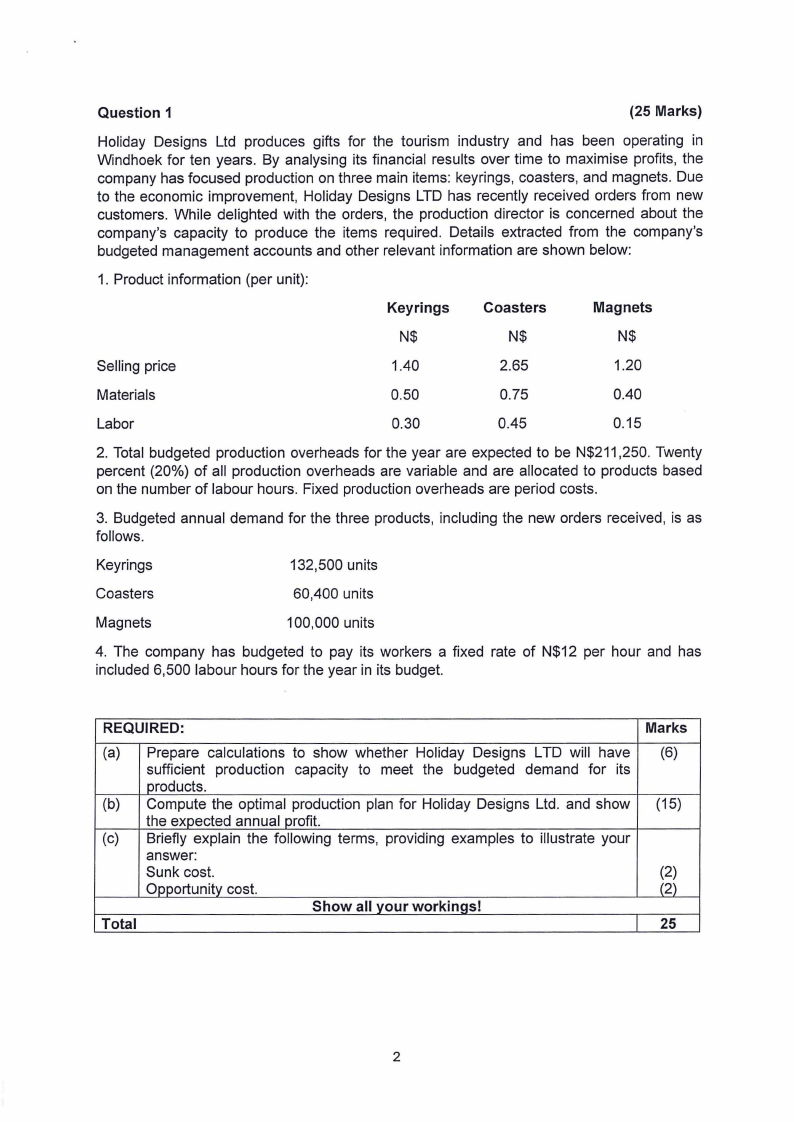

Question 1

(25 Marks)

Holiday Designs Ltd produces gifts for the tourism industry and has been operating in

Windhoek for ten years . By analysing its financial results over time to maximise profits, the

company has focused production on three main items: keyrings , coasters, and magnets. Due

to the economic improvement, Holiday Designs LTD has recently received orders from new

customers. While delighted with the orders, the production director is concerned about the

company's capacity to produce the items required . Details extracted from the company's

budgeted management accounts and other relevant information are shown below:

1. Product information (per unit):

Keyrings Coasters

Magnets

N$

N$

N$

Selling price

1.40

2.65

1.20

Materials

0.50

0.75

0.40

Labor

0.30

0.45

0.15

2. Total budgeted production overheads for the year are expected to be N$211,250. Twenty

percent (20%) of all production overheads are variable and are allocated to products based

on the number of labour hours. Fixed production overheads are period costs.

3. Budgeted annual demand for the three products, including the new orders received, is as

follows .

Keyrings

132,500 units

Coasters

60,400 units

Magnets

100,000 units

4. The company has budgeted to pay its workers a fixed rate of N$12 per hour and has

included 6,500 labour hours for the year in its budget.

REQUIRED:

Marks

(a) Prepare calculations to show whether Holiday Designs LTD will have (6)

sufficient production capacity to meet the budgeted demand for its

products.

(b) Compute the optimal production plan for Holiday Designs Ltd. and show (15)

the expected annual profit.

(c) Briefly explain the following terms, providing examples to illustrate your

answer:

Sunk cost.

(2)

Opportunity cost.

(2)

Show all vour workinas!

Total

25

2

|

|

3 Page 3 |

▲back to top |

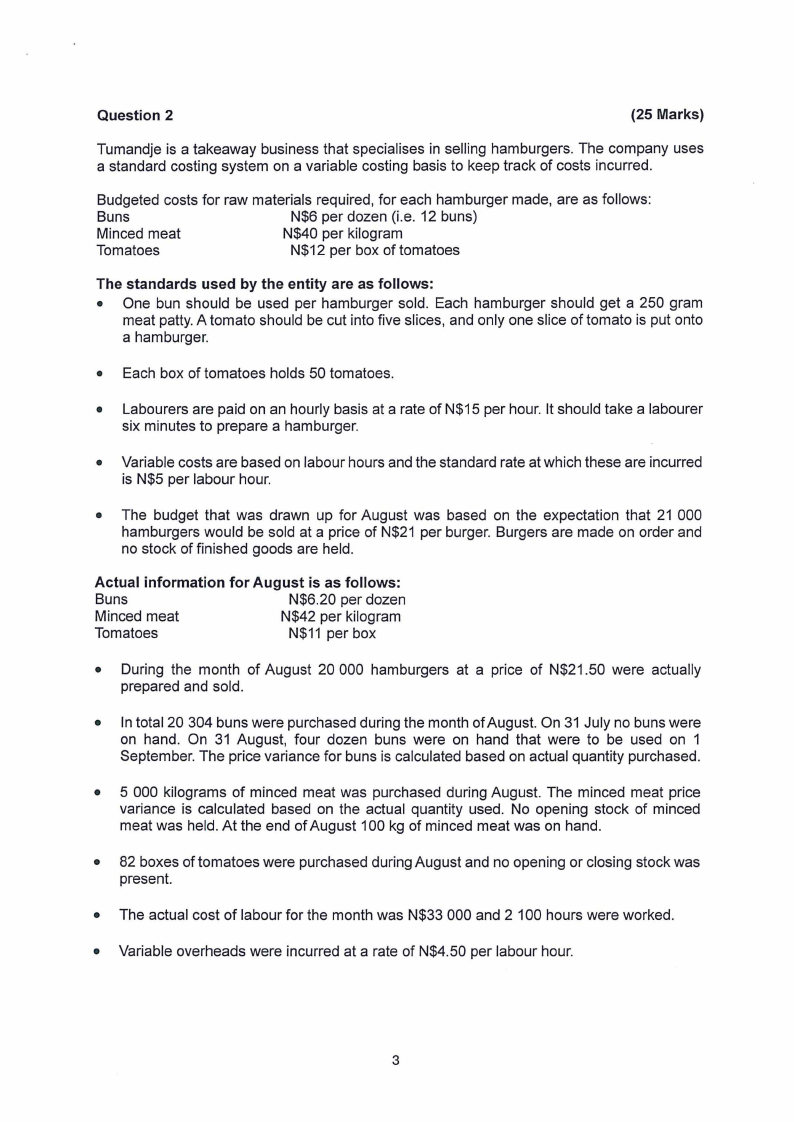

Question 2

(25 Marks)

Tumandje is a takeaway business that specialises in selling hamburgers. The company uses

a standard costing system on a variable costing basis to keep track of costs incurred.

Budgeted costs for raw materials required, for each hamburger made, are as follows:

Buns

N$6 per dozen (i.e. 12 buns)

Minced meat

N$40 per kilogram

Tomatoes

N$12 per box of tomatoes

The standards used by the entity are as follows:

• One bun should be used per hamburger sold. Each hamburger should get a 250 gram

meat patty. A tomato should be cut into five slices, and only one slice of tomato is put onto

a hamburger.

• Each box of tomatoes holds 50 tomatoes.

• Labourers are paid on an hourly basis at a rate of N$15 per hour. It should take a labourer

six minutes to prepare a hamburger.

• Variable costs are based on labour hours and the standard rate at which these are incurred

is N$5 per labour hour.

• The budget that was drawn up for August was based on the expectation that 21 000

hamburgers would be sold at a price of N$21 per burger. Burgers are made on order and

no stock of finished goods are held .

Actual information for August is as follows:

Buns

N$6.20 per dozen

Minced meat

N$42 per kilogram

Tomatoes

N$11 per box

• During the month of August 20 000 hamburgers at a price of N$21.50 were actually

prepared and sold.

• In total 20 304 buns were purchased during the month of August. On 31 July no buns were

on hand. On 31 August, four dozen buns were on hand that were to be used on 1

September. The price variance for buns is calculated based on actual quantity purchased.

• 5 000 kilograms of minced meat was purchased during August. The minced meat price

variance is calculated based on the actual quantity used. No opening stock of minced

meat was held. At the end of August 100 kg of minced meat was on hand.

• 82 boxes of tomatoes were purchased during August and no opening or closing stock was

present.

• The actual cost of labour for the month was N$33 000 and 2 100 hours were worked.

• Variable overheads were incurred at a rate of N$4.50 per labour hour.

3

|

|

4 Page 4 |

▲back to top |

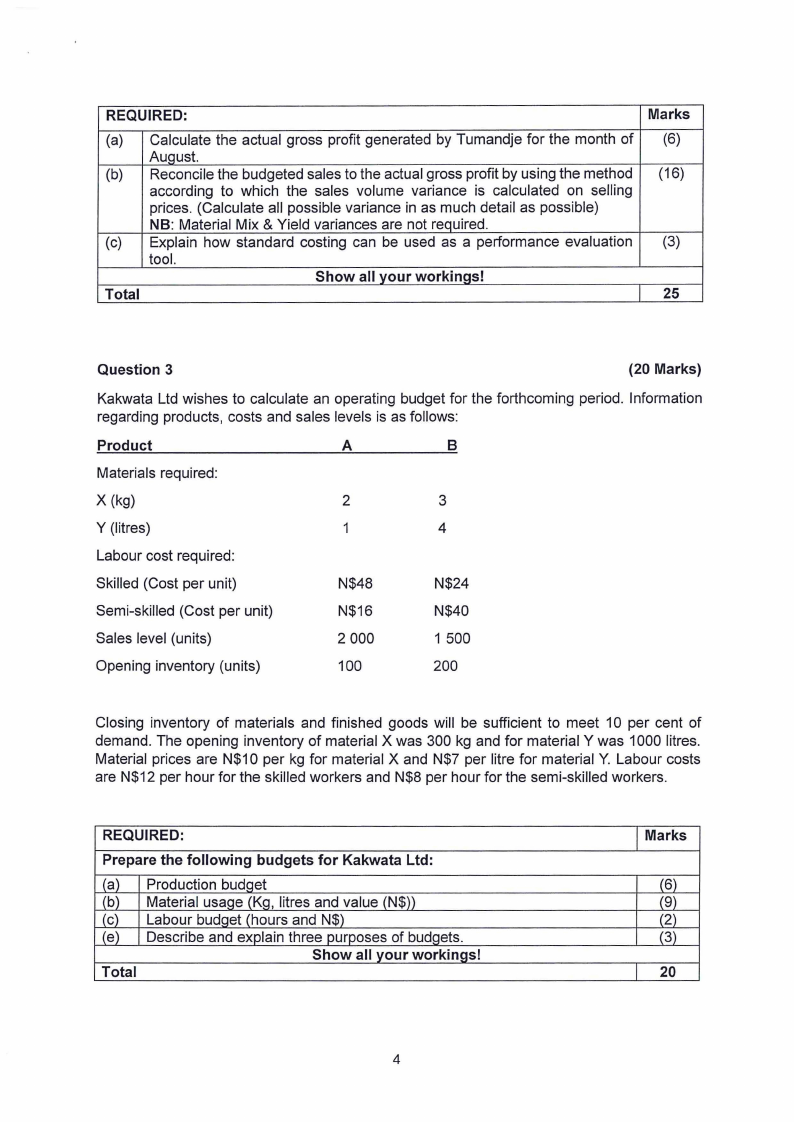

REQUIRED:

Marks

(a) Calculate the actual gross profit generated by Tumandje for the month of (6)

AuQust.

(b) Reconcile the budgeted sales to the actual gross profit by using the method (16)

according to which the sales volume variance is calculated on selling

prices. (Calculate all possible variance in as much detail as possible)

NB: Material Mix & Yield variances are not required.

(c) Explain how standard costing can be used as a performance evaluation (3)

tool.

Show all your workings!

Total

25

Question 3

(20 Marks)

Kakwata Ltd wishes to calculate an operating budget for the forthcoming period. Information

regarding products, costs and sales levels is as follows:

Product

A

B

Materials required:

X (kg)

2

3

Y (litres)

1

4

Labour cost required:

Skilled (Cost per unit)

N$48

N$24

Semi-skilled (Cost per unit)

N$16

N$40

Sales level (units)

2 000

1 500

Opening inventory (units)

100

200

Closing inventory of materials and finished goods will be sufficient to meet 10 per cent of

demand. The opening inventory of material X was 300 kg and for material Y was 1000 litres.

Material prices are N$10 per kg for material X and N$7 per litre for material Y. Labour costs

are N$12 per hour for the skilled workers and N$8 per hour for the semi-skilled workers.

REQUIRED:

Prepare the following budgets for Kakwata Ltd:

Production

Labour bud

Describe a

Total

Marks

6

9

2

3

20

4

|

|

5 Page 5 |

▲back to top |

Question 4

(10 marks)

On weekends, Tatekulu Ngwala spends his spare time carving toy figures from wood. The two

types of toys that he carves are the Incredible Hulk and Iron Man. Each Incredible Hulk needs

15 minutes of machine time and 12 minutes finishing time, while every Iron Man requires 20

minutes of machine time and 1Ominutes finishing time. Only Japie operates the machine, and

he has only 15 hours available. A worker with an available time of 10 hours does the finishing.

Japie received an order for 15 Iron Man toys (which still need to be produced) for next week.

Usually Japie sells all the toys he produces. Incredible Hulk toys make a profit of N$6 per toy,

and Iron Man gives a profit of N$5 per toy.

The total fixed cost for the Hulk toy is N$2 while for Iron Man it is N$4. Tatekulu Ngwala was

informed that you are able to assist him with a production-related problem .

REQUIRED:

Marks

Use the graphical method to determine the optimum combination of toy men (Hulk (10)

& Iron) to be made and sold in order to maximise profits, by algebraically

calculating the profit at each intersection within the feasible region.

Round down to the lower unit. E.g. 3.6 becomes 3.

Show all your workings!

Total

10

Question 5

(20 Marks)

Henry Company (HC) provides skilled labour to the building trade. A builder has recently

asked them to bid for a kitchen fitting contract for a new development of 600 identical

apartments. HC has not worked for this builder before.

The general kitchen fitting process begins with site preparation, which includes inspection,

measurement verification, and confirmation that all necessary materials and tools are

available. The team, comprising carpenters, plumbers, electricians, and assistants, marks the

layout for cabinets, plumbing, and electrical points before installation begins. Wall and base

cabinets are fitted first, followed by plumbing connections for the sink and water outlets, and

electrical installations for lighting and appliances.

Once the structural components are in place, countertops and splashbacks are installed, and

final finishes such as handles, hinges, and trims are added. The process concludes with a

thorough quality inspection, testing of plumbing and electrical systems, and cleaning of the

work area to ensure the kitchen is fully functional, aligned, and ready for use.

Cost information for the new contract is as follows:

Labour for the contract is available. HC expects that the first kitchen will take 24 man-hours

to fit, but thereafter the time taken will be subject to a 95% learning rate . After 200 kitchens

are fitted, the learning rate will stop, and the time taken for the 200th kitchen will be the time

taken for all the remaining kitchens. Labour cost is N$15 per hour.

Overheads are absorbed on a labour hour basis. HC has collected overhead information for

the last four months and this is shown below:

5

|

|

6 Page 6 |

▲back to top |

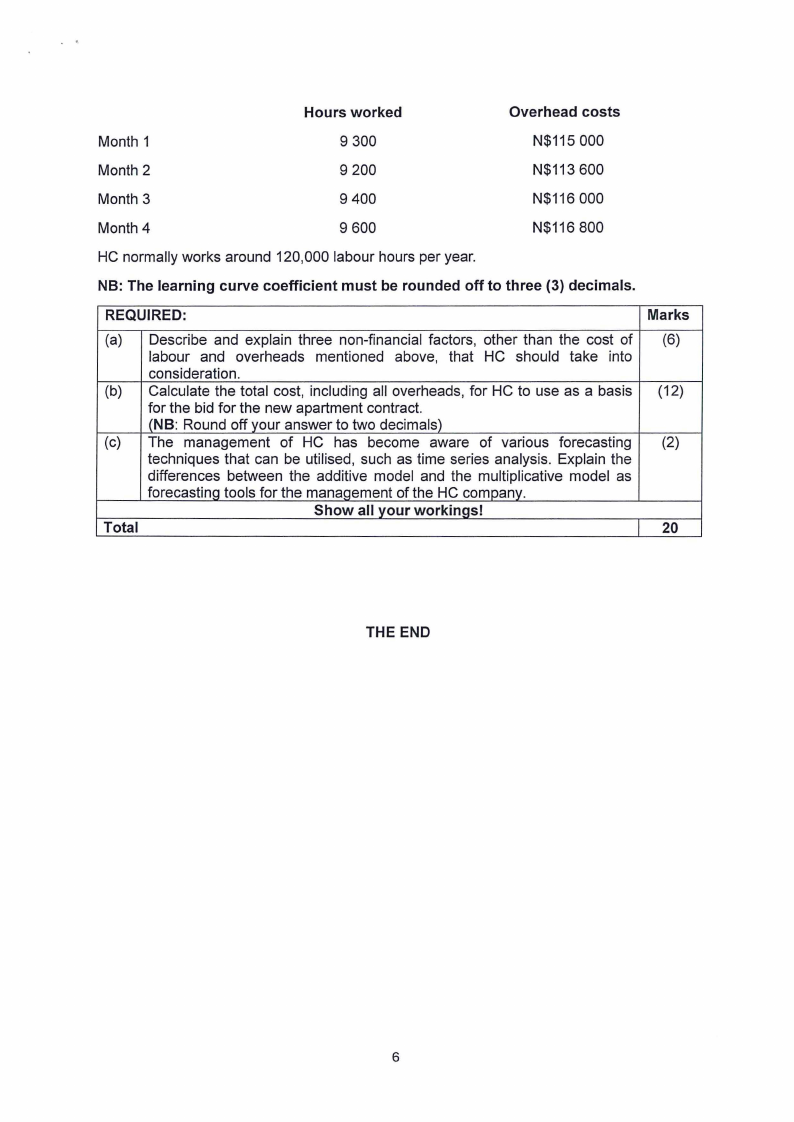

Hours worked

Overhead costs

Month 1

9 300

N$115 000

Month 2

9 200

N$113 600

Month 3

9 400

N$116 000

Month 4

9 600

N$116 800

HC normally works around 120,000 labour hours per year.

NB: The learning curve coefficient must be rounded off to three (3) decimals.

REQUIRED:

Marks

(a) Describe and explain three non-financial factors, other than the cost of (6)

labour and overheads mentioned above, that HC should take into

consideration.

(b) Calculate the total cost, including all overheads, for HC to use as a basis (12)

for the bid for the new apartment contract.

(NB: Round off your answer to two decimals)

(c) The management of HC has become aware of various forecasting (2)

techniques that can be utilised, such as time series analysis. Explain the

differences between the additive model and the multiplicative model as

forecasting tools for the manaQement of the HC company.

Show all your workings!

Total

20

THE END

6