|

AUT621S-AUDITING 202-2ND OPP-DEC 2025 |

|

|

1 Page 1 |

▲back to top |

n Am I BI A u n IVER s I TY

OF SCIEnCE Ano TECHnOLOGY

FACULTY OF COMMERCE, HUMAN SCIENCES & EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING AND FINANCE

QUALIFICATION: BACHELOR OF ACCOUNTING

QUALIFICATION CODE: 07 BOAC

LEVEL: 7

COURSE CODE: AUT 6215

COURSE NAME: AUDITING 202

SESSION: DECEMBER 2025

DURATION: 3 HOURS

PAPER: THEORY

MARKS: 100

SECOND OPPORTUNITY QUESTION PAPER

EXAMINER(S) P. ERKIE, F. SHIKOYENI AND E.N . SAKEUS

MODERATOR: DR. D. MUZIRA

INSTRUCTIONS

1. This test paper is made up of six (6) questions.

2. Answer ALL Question in blue or black ink

3. Start each question on a new page in your answer sheet

4. Questions relating to this paper may be raised in the initial 30 minutes after the

start of the paper. Thereafter, candidates must use their initiative to deal with any

perceived error or ambiguities & any assumption made by the candidate should be

clearly stated.

This question paper consists of 6 pages (including the cover page)

1

|

|

2 Page 2 |

▲back to top |

QUESTION 1

(20 MARKS)

SilverPeak Construction (Pty) Ltd is a medium-sized Namibian construction and engineering

company specializing in large infrastructure projects, including roads, schools, and public

housing. The company has been under increasing financial pressure due to rising input costs,

delayed government payments, and fierce competition from larger regional firms. To stabilize

its cash flows and meet pressing debt obligations, the company has been aggressively

pursuing government contracts, particularly housing tenders.

On 10 September while performing the audit for the financial year ended 30 June 2025, the

audit partner, Ms. Nandago, identified unusual bank transfers while reviewing SilverPeak's

financial records. A payment of N$2.8 million made in April 2025 raised concern. The transfer

was directed to Kavango Business Advisory, an unregistered consultancy whose records could

not be verified. Further checks revealed that the entity was owned by a close associate of the

Chief Financial Officer (CFO), Mr. Shilongo.

When queried, Mr. Shilongo explained that the payment was a "facilitation fee" aimed at

helping the company secure a lucrative government housing tender worth over N$120

million . The payment was neither authorised by the Board nor supported by a written

agreement. Instead, it was misclassified as 'Consulting Expenses' in the financial statements

and deliberately concealed from shareholders and regulators.

Ms. Nandago was convinced that this constituted a reportable irregularity, and on 10

September 2025, she called to formally reported the matter to the Public Accountants and

Auditors Board (PAAB) in line with her obligations.

On 18 September 2025, the company's management was formally notified of the issue and

asked to provide an explanation . On 25 October 2025, Ms. Nandago convened a meeting with

SilverPeak's senior management to address the matter. At this meeting, management

downplayed the transaction, describing it as an "accounting error" and not an intentional act

of wrongdoing. Ms. Nandago accepted management's explanation and deemed the matter

resolved. She subsequently removed the finding from her audit documentation.

Required:

a) Would you agree with Ms. Nandago that this constitutes a reportable irregularity in terms

of the Auditing Profession Act 6 of 2005? Provide reasons to support your answer. (10)

b) Assuming this is a reportable irregularity, has Ms. Nandago followed the correct

procedures after confirming or finding out that a reportable irregularity had occurred?(l0)

2

|

|

3 Page 3 |

▲back to top |

QUESTION 2

(10 MARKS)

Accountants must always act with integrity, objectivity, professional competence and due

care, confidentiality, and professional behavior. These are the fundamental principles of the

SAICA Code of Professional Conduct. The Code also identifies situations, called threats, that

may compromise professional judgment or adherence to these principles.

Required: Read each scenario below and indicate which threat to the fundamental principles

is being described.

(10)

1. An auditor has a close relative who holds a senior position in the client company.

2. A member of the audit team is offered an expensive gift by the client to secure a

contract.

3. The auditor relies heavily on fees from one client, which represents 80% of the audit

firm's revenue.

4. An auditor previously worked in a senior management position at the client's company

and was responsible for financial reporting.

5. The audit firm's partner has a direct financial interest in the client's business.

6. An auditor is asked by management to prepare accounting records for the client while

also auditing them.

7. A member of the audit team wants to please the client to secure a promotion within

the audit firm.

8. An auditor is simultaneously performing internal audit services for the client while

conducting the external audit.

9. The audit partner has a personal friendship with the client's CEO and often socializes

with them outside work.

10. A client requests that the auditor overlook a small misstatement in the financial

statements to meet targets.

3

|

|

4 Page 4 |

▲back to top |

QUESTION 3

(10 MARKS)

EcoGen Solutions (Pty) Ltd is a large Namibian company operating in the renewable energy

and manufacturing sector.

Composition of the Audit Committee (5 Members):

• Mr. Haikali - Non-Executive Director and Chairperson of the Board of Directors. He also

serves as Chairperson of the Audit Committee.

• Ms. Kahuure - Independent non-executive director with an MBA.

• Mr. Shivute - Independent non-executive director with an IT background.

• Ms. Uushona - non-executive director, professional engineer

• Ms. Tjipueja - Independent non-executive director, social worker by profession) .

Required: Critically evaluate the composition of the Audit Committee of EcoGen Solutions

(Pty) Ltd, using the King IV Report on Corporate Governance as your benchmark. (APA). (10)

QUESTION 4

(15 MARKS)

Internal controls in auditing refer to the processes and systems implemented by an

organization to ensure the integrity of financial reporting, compliance with laws and

regulations, and the efficiency of operations.

Required:

i)

Name 5 type of internal controls activities and give an example for each activity. (10)

ii)

Describe the limitations of Internal Control.

(5)

4

|

|

5 Page 5 |

▲back to top |

QUESTION 5

(25 MARKS)

You are an audit senior at JSS Audit Incorporated ("JSS"), a medium-sized audit firm based in

Windhoek. Mr John Jerome the CEO of Bubble Instant Porridge Ltd ("Bubble") has recently

appointed your audit firm as Bubble's external auditors for the 31 December 2024 ("FY2024")

year-end audit.

The following information relating to the company is available to you :

Background information

Bubble is a company in the manufacturing of instant porridges. The company is listed on the

Namibia Stock Exchange (NSX) since 2020.

Bubble operates from a large property of 2 000 square metres in Omaruru. Bubble's

manufacturing facility is situated on the property, next to the head office building where all

administrative and accounting functions are performed. The colourants used in Bubble's

instant porridges are imported from South Africa. All other raw materials used in the

production process of Bubble instant porridges, such as flour, sugar and glucose are sourced

from local suppliers.

The manufacturing facility has a large central warehouse that stores all bubble's inventory.

There1s also a separate storage facility on the property that is temperature controlled and

where the sugar is stored to ensure that the sugar stock is not exposed to humidity and expiry.

Bubble transports its finished goods from the manufacturing facility directly to the distribution

centres .

Senior management of Bubble are offered lucrative performance bonuses for achieving high

sales targets.

The company has experienced some negative publicity. Bubble has failed to include a warning

on its labels prohibiting the consumption of Bubble instant porridge by children under the age

of 4 and those with high blood pressure in terms of the Foodstuffs, Cosmetics and

Disinfectants Act 54 of 1972 (' FCD Act 1 ). Bubble is facing three major lawsuits claiming that

children have experienced serious side-effects after consuming Bubble instant porridge. The

company is also being accused of deceptive advertising practices.

Despite the popularity of Bubble, the company has faced many challenges in FY2024. There1s

uncertainty about Bubble future amidst poor cash management and its inability to pay its

creditors. FBN Bank has indicated that they are willing to give Bubble a loan on condition that

Bubble1s FY2024 audited financial statements are provided by 31 January 2024 and reflect an

unqualified audit opinion.

5

|

|

6 Page 6 |

▲back to top |

Required:

a} With reference to the background information of Bubble:

i. Identify the events or conditions (risk indicators} at the financial statement

level

(8)

ii. For each identified event or condition (risk indicator} describe the risks of

material misstatement present in the financial statements of Bubble.

(17)

Present your answer as follows:

(a) Events or conditions/ (risk indicators)

(1 mark each)

1 .......................

(b) Description of risks of material

misstatement (2 marks each)

1.................. .........................................

QUESTION 6

(20 MARKS)

You recently graduated from NUST and was fortunate enough to be appointed in an audit firm

BOTHA Incorporated, as the trainee auditor. During your weekly briefings, you were informed

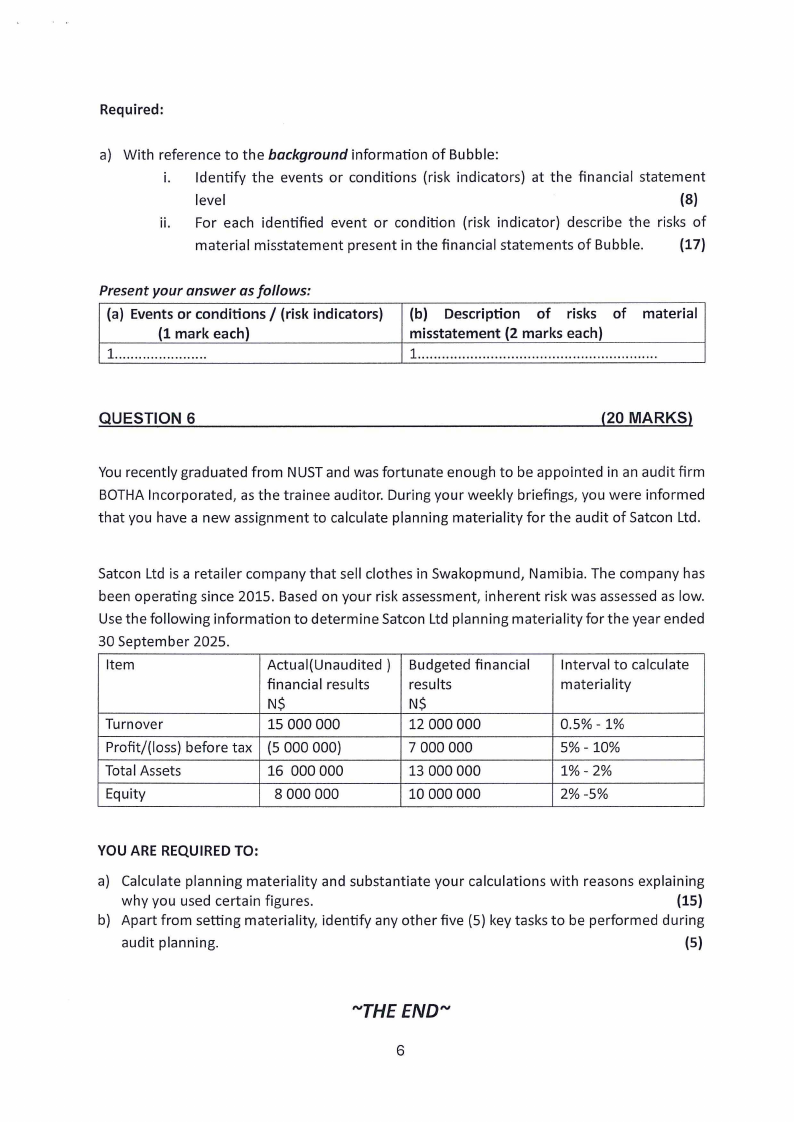

that you have a new assignment to calculate planning materiality for the audit of Satcon Ltd.

Satcon Ltd is a retailer company that sell clothes in Swakopmund, Namibia. The company has

been operating since 2015. Based on your risk assessment, inherent risk was assessed as low.

Use the following information to determine Satcon Ltd planning materiality for the year ended

30 September 2025.

Item

Actual(Unaudited } Budgeted financial Interval to calculate

financial results

results

materiality

N$

N$

Turnover

15 000 000

12 000 000

0.5% - 1%

Profit/(loss} before tax (5 000 000}

7 000 000

5%-10%

Total Assets

16 000 000

13 000 000

1%- 2%

Equity

8 000 000

10 000 000

2%-5%

YOU ARE REQUIRED TO:

a} Calculate planning materiality and substantiate your calculations with reasons explaining

why you used certain figures.

(15)

b} Apart from setting materiality, identify any other five {5} key tasks to be performed during

audit planning.

(5)

~rHEEND~

6