|

AUT621S-AUDITING 202-1ST OPP-NOV 2025 |

|

|

1 Page 1 |

▲back to top |

nAmlBIA unlVERSITY

OF SCIEnCE Ano TECHnOLOGY

FACULTY OF COMMERCE, HUMAN SCIENCES & EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING AND FINANCE

QUALIFICATION: BACHELOR OF ACCOUNTING

QUALIFICATION CODE: 07 BOAC

LEVEL: 7

COURSE CODE: AUT 621S

COURSE NAME: AUDITING 202

SESSION: OCT/NOV 2025

DURATION: 3 HOURS

PAPER: THEORY

MARKS: 100

FIRST OPPORTUNITY QUESTION PAPER

EXAMINER(S) P. ERKIE, F. SHIKOYENI AND E.N. SAKEUS

MODERATOR: DR. D. MUZIRA

INSTRUCTIONS

1. This test paper is made up of five (5) questions.

2. Answer ALL Question in blue or black ink

3. Start each question on a new page in your answer sheet

4. Questions relating to this paper may be raised in the initial 30 minutes after the

start of the paper. Thereafter, candidates must use their initiative to deal with any

perceived error or ambiguities & any assumption made by the candidate should be

clearly stated.

This question paper consists of 7 pages (including the cover page)

1

|

|

2 Page 2 |

▲back to top |

QUESTION 1

(20 MARKS)

PART A

One afternoon, your cousin who is studying engineering calls you with a puzzled look. They

have been reading about companies and their financial statements and reports and ask: "How

do people really know if these numbers are correct? Can we just trust what is on paper?"

Requiredd: Try to explain to your cousin what auditing is and why someone might want a

company's financial information to be reviewed .

(10)

PARTB

The SAICA Code of Professional Conduct (CPC) provides the foundation for how professional

accountants should behave in the performance of their duties.

Required: Read each of the following statements carefully. For every statement, indicate

which fundamental principle of the CPC is being described or best applies.

(10)

1. An accountant refuses to manipulate financial figures even though management

pressures them to do so.

2. A trainee auditor avoids being influenced by close friendships when evaluating a

client's transactions.

3. An auditor takes continuing professional development (CPD) courses to stay up to

date with new auditing standards.

4. A professional does not disclose client information to a competitor without proper

authority.

5. A chartered accountant avoids engaging in conduct that could discredit the profession,

even outside work.

6. A tax consultant provides advice only in areas where they are qualified and

experienced.

7. An auditor ensures that audit working papers are properly documented and filed in

accordance with firm pol icy.

8. A professional declines a gift from a cl ient because it could create the perception of

bias.

9. A financial manager openly and honestly communicates the results of an internal

review, even though it reveals weaknesses.

10. A practitioner corrects a previously issued report when they discover that it contained

an error.

2

|

|

3 Page 3 |

▲back to top |

QUESTION 2

(10 MARKS)

You are part of the audit team reviewing the annual financial statements of a medium-sized

Namibian company. During your review, you discover a payment error made by the senior

accountant in the financial reporting department.

The accountant was supposed to pay Safa Pty Ltd an amount of N$250,000 for goods supplied.

However, due to a data entry error, the payment was made to Stafas Pty Ltd instead. When

the company contacted Stafas Pty Ltd to request a refund, the company indicated that they

were not aware of the payment and were unwilling to return the money, claiming that the

funds had been absorbed by an overdraft on their account.

As a result, the company had to repay N$250,000to Safa Pty Ltd. There is no evidence of theft,

or intentional misconduct by the accountant as the error occurred due to misreading the

beneficiary's name during the payment process. However, it becomes clear that the errors

occurred because the accountant did not fully comply with internal controls and company

policies, such as proper authorization and verification of supporting documents.

Required: Assess whether this situation qualifies as a reportable irregularity under the

Auditing Profession Act (APA}.

{10)

3

|

|

4 Page 4 |

▲back to top |

QUESTION 3

(20 MARKS)

You are on the audit team of Maano Auditing Services. Your firm has been approached to audit

lnnoTech Dynamics Ltd, a technology-based company planning to expand its operations next

year. This will be the first client your firm is handling from the technology sector. The proposed

audit is scheduled for November 2025, but most of your trainee accountants will be on study

leave preparing for their APC exams, which may affect the availability of staff for the

engagement.

lnnoTech Dynamics is a new client for Maano, and preliminary investigations have revealed

that the previous CEO, Mr. Leonard Mathews, was recently terminated due to

misappropriation of company funds. The company is also experiencing significant financial

difficulties, including delayed payments from key clients and liquidity challenges.

Compounding these concerns is the fact that the company uses a non-standard accounting

framework called "TechnoStat Reporting Standards (TRS}", which is not widely recognized, and

relies on a fully integrated IT system for its financial reporting, which may introduce technical

risks if the audit team is unfamiliar with the system.

The audit manager assigned to this engagement, Ms. Rachel Swan, is married to the

company's lnnoTech CFO, Mr. Adrian Cole. The company has recently appeared in the news

for tax evasion schemes related to cryptocurrency operations, which raises the risk of criminal

exposure and regulatory scrutiny. The client has requested a limitation in the audit scope,

specifically that audit testing of revenue recognition be restricted to selected transactions

only, citing time and cost constraints.

Required: Assess and evaluate whether the firm should accept or decline this engagement(20}

4

|

|

5 Page 5 |

▲back to top |

QUESTION 4

(10 MARKS)

SCENARIO: BOARD COMPOSITION AT MANPOWER RESOURCES LTD

ManPower Resources Ltd is a listed Namibian energy company operating primarily in the

Erongo and Kunene regions. The company recently underwent a restructuring process and is

aiming to align with the principles of the King IV Report on Corporate Governance and the

requirements of the Namibian Stock Exchange (NSX).

As part of this process, attention has been placed on the composition of the Governing body

committee. Below is the current structure of the governing body:

Name

Paulus Amutenya

Johan van Wyk

Thomas lilonga

Michael Beukes

Simon Nghitila

Peter de Villiers

Elias Haufiku

Willem Botha

Anna Shilongo

Helena Swart

Role on the Governing Body

Chair (Independent Non-Executive)

Independent Non-Executive

Independent Non-Executive

Independent Non-Executive

Independent Non-Executive

Non-Executive

Non-Executive

Non-Executive

Non-Executive

Executive - CFO

Race

Black

White

Black

White

Black

White

Black

White

Black

White

Gender

Male

Male

Male

Male

Male

Male

Male

Male

Female

Female

Required: Critically comment on the composition of the governing body of NamPower

Resources Ltd.

(10)

5

|

|

6 Page 6 |

▲back to top |

QUESTION 5

(40 MARKS)

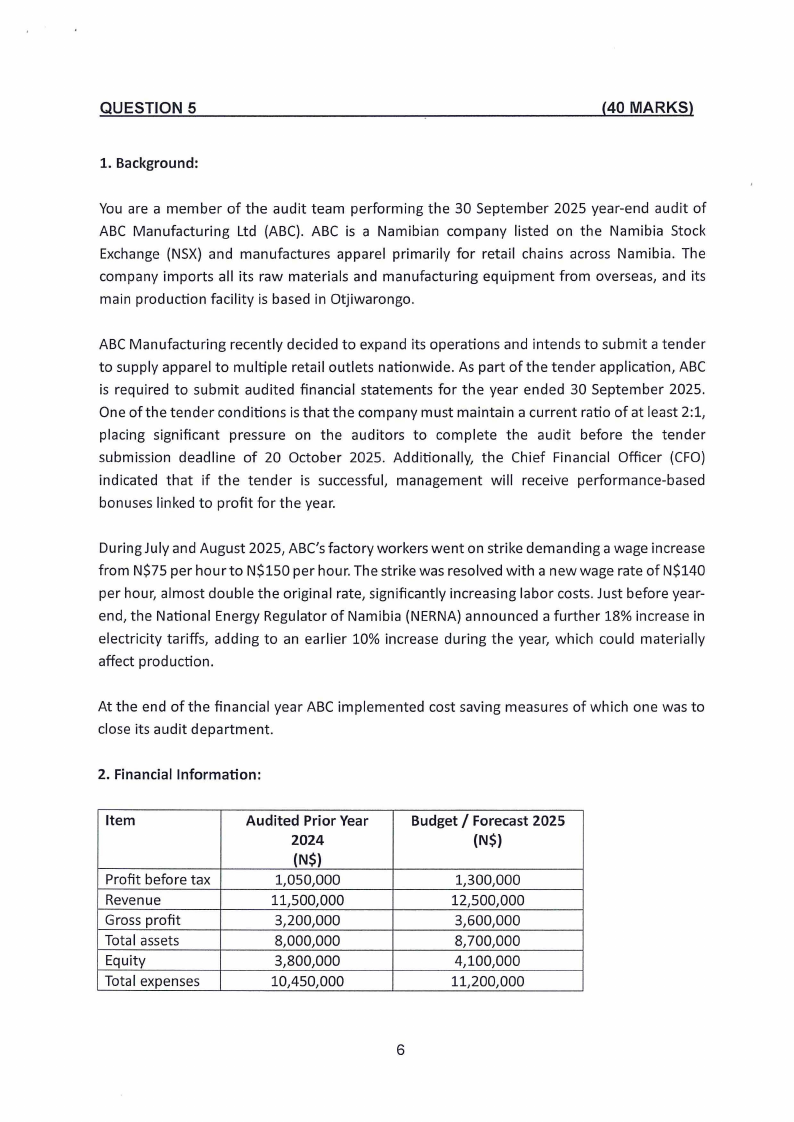

1. Background:

You are a member of the audit team performing the 30 September 2025 year-end audit of

ABC Manufacturing Ltd {ABC). ABC is a Namibian company listed on the Namibia Stock

Exchange {NSX) and manufactures apparel primarily for retail chains across Namibia. The

company imports all its raw materials and manufacturing equipment from overseas, and its

main production facility is based in Otjiwarongo.

ABC Manufacturing recently decided to expand its operations and intends to submit a tender

to supply apparel to multiple retail outlets nationwide. As part of the tender application, ABC

is required to submit audited financial statements for the year ended 30 September 2025.

One of the tender conditions is that the company must maintain a current ratio of at least 2:1,

placing significant pressure on the auditors to complete the audit before the tender

submission deadline of 20 October 2025. Additionally, the Chief Financial Officer {CFO)

indicated that if the tender is successful, management will receive performance-based

bonuses linked to profit for the year.

During July and August 2025, ABC's factory workers went on strike demanding a wage increase

from N$75 per hour to N$150 per hour. The strike was resolved with a new wage rate of N$140

per hour, almost double the original rate, significantly increasing labor costs. Just before year-

end, the National Energy Regulator of Namibia {NERNA) announced a further 18% increase in

electricity tariffs, adding to an earlier 10% increase during the year, which could materially

affect production.

At the end of the financial year ABC implemented cost saving measures of which one was to

close its audit department.

2. Financial Information:

Item

Profit before tax

Revenue

Gross profit

Total assets

Equity

Total expenses

Audited Prior Year

2024

(N$)

1,050,000

11,500,000

3,200,000

8,000,000

3,800,000

10,450,000

Budget/ Forecast 2025

(N$)

1,300,000

12,500,000

3,600,000

8,700,000

4,100,000

11,200,000

6

|

|

7 Page 7 |

▲back to top |

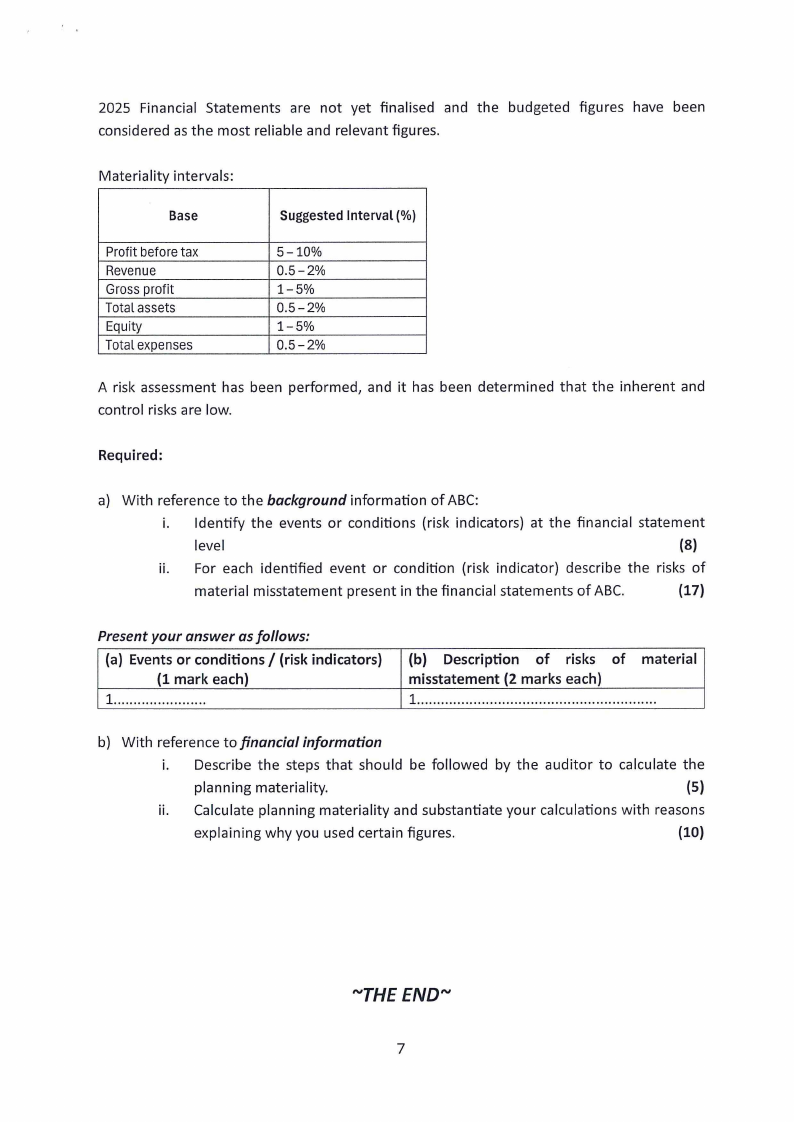

2025 Financial Statements are not yet finalised and the budgeted figures have been

considered as the most reliable and relevant figures.

Materiality intervals:

Base

Profit before tax

Revenue

Gross profit

Total assets

Equity

Total expenses

Suggested Interval(%)

5-10%

0.5-2%

1-5%

0.5-2%

1-5%

0.5-2%

A risk assessment has been performed, and it has been determined that the inherent and

control risks are low.

Required:

a) With reference to the background information of ABC:

i. Identify the events or conditions {risk indicators) at the financial statement

level

(8)

ii. For each identified event or condition {risk indicator) describe the risks of

material misstatement present in the financial statements of ABC.

(17}

Present your answer as follows:

(a) Events or conditions/ (risk indicators)

(1 mark each)

1 .......................

(b) Description of risks of material

misstatement (2 marks each)

1..................... ... .. ... ............................. .

b) With reference to financial information

i. Describe the steps that should be followed by the auditor to calculate the

planning materiality.

(5)

ii. Calculate planning materiality and substantiate your calculations with reasons

explaining why you used certain figures.

(10}

~rHE END~

7