|

FAM601Y-FINANCIAL MANAGEMENT 200-2ND OPP-DEC 2025 |

|

|

1 Page 1 |

▲back to top |

~

nAmlBIA UnlVERSITY

OF SCI En CE Ano TECH no LOGY

FACULTY OF COMMERCE, HUMAN SCIENCES & EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING & FINANCE

QUALIFICATION: BACHELOR OF ACCOUNTING (CHARTERED ACCOUNTANCY)

QUALIFICATION CODE: 07BACC

LEVEL: 6

COURSE CODE: FAM601Y

COURSE NAME: FINANCIAL MANAGEMENT 200

SESSION: DECEMBER 2025

DURATION: 2 HOURS 30 MINUTES

PAPER: PRACTICAL AND THEORY

MARKS: 100

EXAMINERS:

ASSESSMENT 6 - 2No OPPORTUNITY EXAMINATIONS

Mr. Immanuel-King Kenaruzo

MODERATOR: Mr. Simeon Nghiwilepo

INSTRUCTIONS

• This question consists of two questions with five (5) required.

• Answer All the questions in blue or black ink.

• Start each part of the required on a new page.

• Show all your work on the answer sheet.

• The use of a pencil is not allowed.

• Questions relating to this paper may be raised in the initial 30 minutes after the start

of the paper. Thereafter, candidates must use their initiative to deal with any

perceived error or ambiguities and any assumption made by the candidate should be

clearly stated.

PERMISSIBLE MATERIALS

Non-programmable calculator/financial calculator

THIS QUESTION PAPER CONSISTS OF 5 PAGES (Including this front page)

FAM601Y, Assessment 6 (2nd Opportunity)

Page 1 of 5

© NUST2025

|

|

2 Page 2 |

▲back to top |

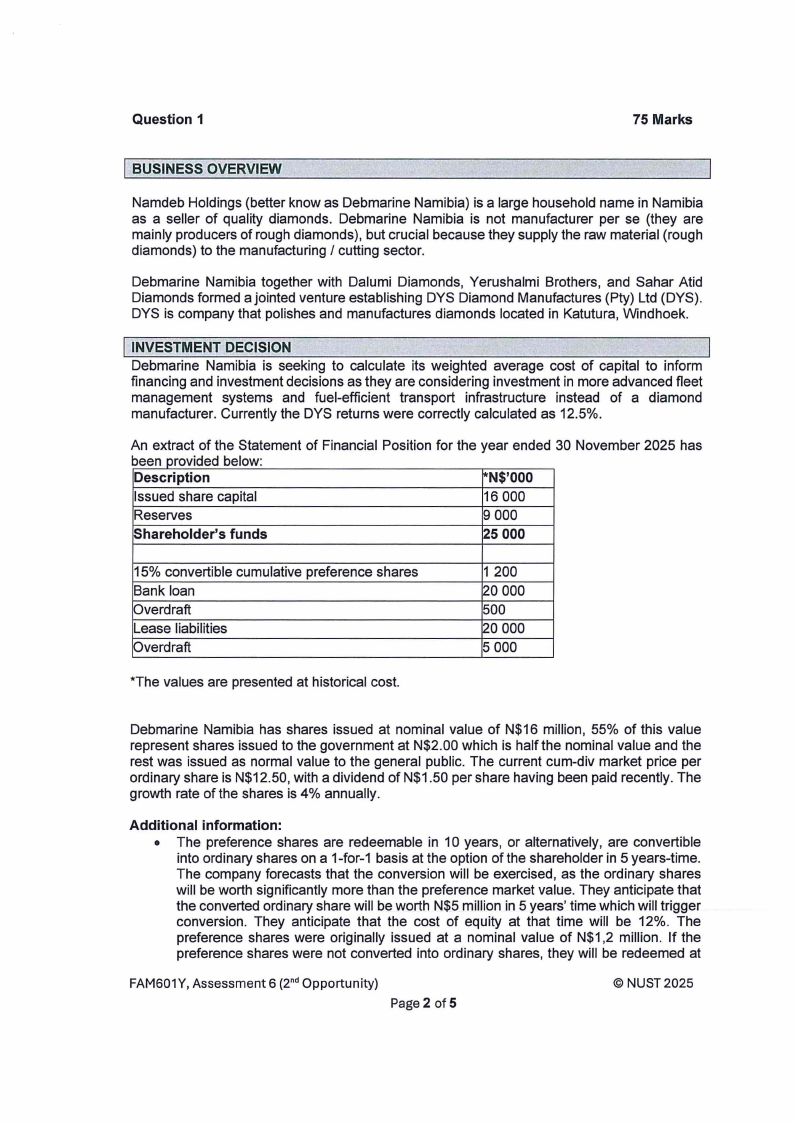

Question 1

75 Marks

I BUSINESS OVERVIEW

Namdeb Holdings (better know as Debmarine Namibia) is a large household name in Namibia

as a seller of quality diamonds. Debmarine Namibia is not manufacturer per se (they are

mainly producers of rough diamonds), but crucial because they supply the raw material (rough

diamonds) to the manufacturing I cutting sector.

Debmarine Namibia together with Dalumi Diamonds, Yerushalmi Brothers, and Sahar Atid

Diamonds formed a jointed venture establishing DYS Diamond Manufactures (Pty) Ltd (DYS).

DYS is company that polishes and manufactures diamonds located in Katutura, Windhoek.

I INVESTMENT DECISION

Debmarine Namibia is seeking to calculate its weighted average cost of capital to inform

financing and investment decisions as they are considering investment in more advanced fleet

management systems and fuel-efficient transport infrastructure instead of a diamond

manufacturer. Currently the DYS returns were correctly calculated as 12.5%.

An extract of the Statement of Financial Position for the year ended 30 November 2025 has

been provided below:

Description

*N$'000

Issued share capital

16 000

Reserves

9 000

Shareholder's funds

25 000

15% convertible cumulative preference shares

Bank loan

Overdraft

Lease liabilities

Overdraft

1 200

20 000

500

20 000

5 000

*The values are presented at historical cost.

Debmarine Namibia has shares issued at nominal value of N$16 million, 55% of this value

represent shares issued to the government at N$2.00 which is half the nominal value and the

rest was issued as normal value to the general public. The current cum-div market price per

ordinary share is N$12.50, with a dividend of N$1.50 per share having been paid recently. The

growth rate of the shares is 4% annually.

Additional information:

• The preference shares are redeemable in 10 years, or alternatively, are convertible

into ordinary shares on a 1-for-1 basis at the option of the shareholder in 5 years-time.

The company forecasts that the conversion will be exercised, as the ordinary shares

will be worth significantly more than the preference market value. They anticipate that

the converted ordinary share will be worth N$5 million in 5 years' time which will trigger

conversion. They anticipate that the cost of equity at that time will be 12%. The

preference shares were originally issued at a nominal value of N$1,2 million. If the

preference shares were not converted into ordinary shares, they will be redeemed at

FAM601Y, Assessment 6 (2nd Opportunity)

Page 2 of 5

© NUST2025

|

|

3 Page 3 |

▲back to top |

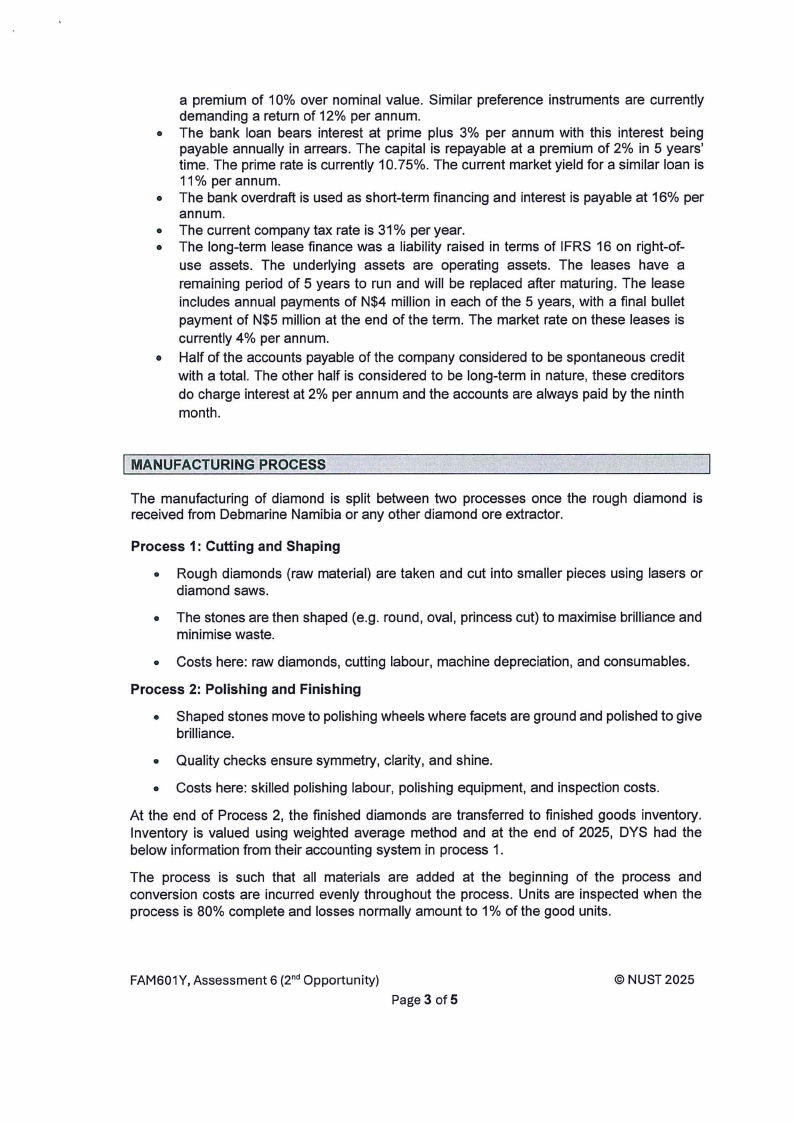

a premium of 10% over nominal value. Similar preference instruments are currently

demanding a return of 12% per annum.

• The bank loan bears interest at prime plus 3% per annum with this interest being

payable annually in arrears. The capital is repayable at a premium of 2% in 5 years'

time. The prime rate is currently 10.75%. The current market yield for a similar loan is

11 % per annum.

• The bank overdraft is used as short-term financing and interest is payable at 16% per

annum.

• The current company tax rate is 31 % per year.

• The long-term lease finance was a liability raised in terms of IFRS 16 on right-of-

use assets. The underlying assets are operating assets. The leases have a

remaining period of 5 years to run and will be replaced after maturing. The lease

includes annual payments of N$4 million in each of the 5 years, with a final bullet

payment of N$5 million at the end of the term. The market rate on these leases is

currently 4% per annum.

• Half of the accounts payable of the company considered to be spontaneous credit

with a total. The other half is considered to be long-term in nature, these creditors

do charge interest at 2% per annum and the accounts are always paid by the ninth

month.

I MANUFACTURING PROCESS

The manufacturing of diamond is split between two processes once the rough diamond is

received from Debmarine Namibia or any other diamond ore extractor.

Process 1: Cutting and Shaping

• Rough diamonds (raw material) are taken and cut into smaller pieces using lasers or

diamond saws.

• The stones are then shaped (e.g. round, oval, princess cut) to maximise brilliance and

minimise waste.

• Costs here: raw diamonds, cutting labour, machine depreciation, and consumables.

Process 2: Polishing and Finishing

• Shaped stones move to polishing wheels where facets are ground and polished to give

brilliance.

• Quality checks ensure symmetry, clarity, and shine.

• Costs here: skilled polishing labour, polishing equipment, and inspection costs.

At the end of Process 2, the finished diamonds are transferred to finished goods inventory.

Inventory is valued using weighted average method and at the end of 2025, DYS had the

below information from their accounting system in process 1.

The process is such that all materials are added at the beginning of the process and

conversion costs are incurred evenly throughout the process. Units are inspected when the

process is 80% complete and losses normally amount to 1% of the good units.

FAM601Y, Assessment 6 (2nd Opportunity)

Page 3 of 5

© NUST2025

|

|

4 Page 4 |

▲back to top |

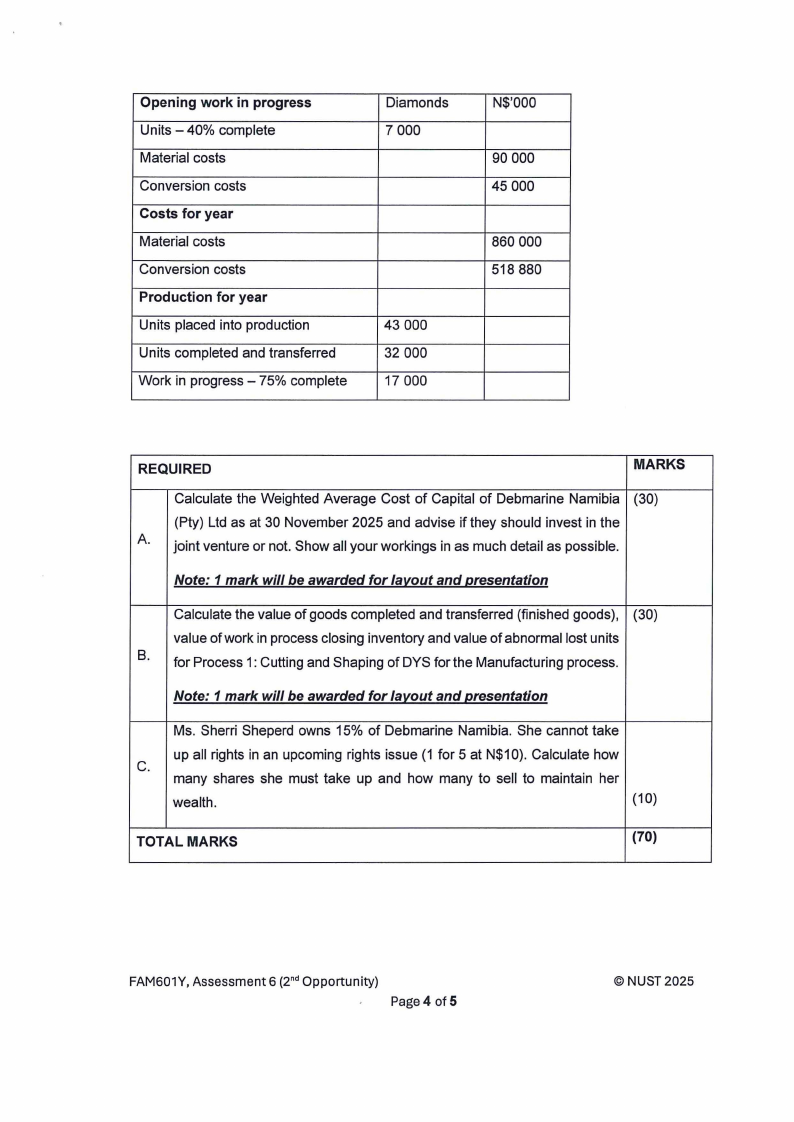

Opening work in progress

Units - 40% complete

Material costs

Conversion costs

Costs for year

Material costs

Conversion costs

Production for year

Units placed into production

Units completed and transferred

Work in progress - 75% complete

Diamonds

7 000

43 000

32 000

17 000

N$'000

90 000

45 000

860 000

518 880

REQUIRED

MARKS

Calculate the Weighted Average Cost of Capital of Debmarine Namibia (30)

(Pty) Ltd as at 30 November 2025 and advise if they should invest in the

A. joint venture or not. Show all your workings in as much detail as possible.

Note: 1 mark will be awarded for la'l.,out and 12.resentation

Calculate the value of goods completed and transferred (finished goods), (30)

value of work in process closing inventory and value of abnormal lost units

B. for Process 1: Cutting and Shaping of DYS for the Manufacturing process.

Note: 1 mark will be awarded for /a'f..OUt and 12.resentation

Ms. Sherri Sheperd owns 15% of Debmarine Namibia. She cannot take

up all rights in an upcoming rights issue (1 for 5 at N$10). Calculate how

C.

many shares she must take up and how many to sell to maintain her

wealth .

(10)

TOTAL MARKS

(70)

FAM601Y, Assessment 6 (2nd Opportunity)

Page 4 of 5

© NUST 2025

|

|

5 Page 5 |

▲back to top |

QUESTION 2 (Adapted from NWU)

[30 MARKS]

Accrow Manufactures CC is an emerging entity based in Grootfontein, Otjozondjupa region.

The CC manufactures motor vehicle spare parts and targets specifically vehicles that originate

from Japan. The management of the CC believes this is a niche market as they are in close

proximity with Botswana which imports a lot of these vehicles from Japan directly.

The CC opened its doors in February 2024 and its financial year ends on 31 December of

each year. On 31 December 2024, stock take records showed inventory valued at N$140 000,

N$96 000 and N$85 000 in their Material Control, Work-in-Progress and Finished goods

respectively. Creditors had been settled in full, and there were no Accounts Receivables

either.

Other information on the transactions for the year ended 31 December 2025 included:

■ Direct material had been purchased for N$110 000, on credit (the amount was settled

before year end).

■ Direct Material issued to the production department in the year amounted to

N$150 000.

■ Salaries and wages of the factory personnel were:

o Direct labour - N$55 000

o Indirect labour - N$35 000

■ Depreciation of plant and equipment for the year amounted to N$28 000

■ Other indirect manufacturing overheads amounted N$13 500 and were settled in

cash

■ The total manufacturing overheads and direct labour costs incurred were fully

absorbed in the production process.

■ Products transferred to finished goods had a manufacturing cost of N$220 000.

■ Sales for the year amounted to N$332 000, and these products had a production

cost of N$135 000

■ Selling and Administrative expenses for the year amount to N$102 000

REQUIRED (32 Marks)

MARKS

A Prepare the Income Statement for Accrow Manufacturers CC for the (22)

year ended 31 December 2025

Note: 1 mark will be awarded for lay,.out and ll,resentation

B Explain the difference between job, process, joint and batch costing (8)

and provide an example.

FAM601Y, Assessment 6 (2nd Opportunity)

Page 5 of 5

© NUST 2025