|

FAM601Y-FINANCIAL MANAGEMENT 200-1ST OPP-NOV 2025 |

|

|

1 Page 1 |

▲back to top |

'9

nAm I BI A un IVE RSITY

OF SCI En CE An □ TECHn OLOGY

FACULTY OF COMMERCE, HUMAN SCIENCES & EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING & FINANCE

QUALIFICATION: BACHELOR OF ACCOUNTING (CHARTERED ACCOUNTANCY)

QUALIFICATION CODE: 07BACC

LEVEL: 6

COURSE CODE: FAM601Y

COURSE NAME: FINANCIAL MANAGEMENT 200

SESSION: OCTOBER/NOVEMBER 2025

DURATION: 2 HOURS 20 MINUTES

PAPER: PRACTICAL AND THEORY

MARKS: 100

ASSESSMENT 6 - FIRST OPPORTUNITY EXAMINATIONS

EXAMINERS: Mr. Immanuel-King Kenaruzo

MODERATOR: Mr. Simeon Nghiwilepo

INSTRUCTIONS

• This question consists of two questions with five (5) required.

• Start each part of the required on a new page.

• Answer All the questions in blue or black ink.

• Show all your work on the answer sheet.

• The use of a pencil is not allowed.

• Questions relating to this paper may be raised in the initial 30 minutes after the start

of the paper. Thereafter, candidates must use their initiative to deal with any

perceived error or ambiguities and any assumption made by the candidate should be

clearly stated.

PERMISSIBLE MATERIALS

Non-programmable calculator/financial calculator

THIS QUESTION PAPER CONSISTS OF 8 PAGES (Including this front page)

FAM601 Y, Assessment 6 (1 sr Opportunity)

©NUST2025

1

|

|

2 Page 2 |

▲back to top |

Question 1

75 Marks

I BUSINESS OVERVIEW

NamPower, Namibia's national power utility, has for decades been a mainstay of the nation's

economy and is now positioned, in a free, independent and stable Namibia, to be a main driver

of Vision 2030, Namibia's blueprint for broad-based , sustainable economic growth.

NamPower's core business is the generation, transmission and energy trading, which takes

place within the Southern African Power Pool (SAPP) , the largest multilateral energy platform

on the African continent. NamPower supplies bulk electricity to Regional Electricity Distributors

(REDs), Mines, Farms and Local Authorities (where REDs are not operational) throughout

Namibia.

I CENORED

CENORED is the 3rd licensed regional electricity distribution company to be established in

Namibia, after NORED and Erongo RED in 2002 and 2004 respectively.

CE NORED license area covers the Otjozondjupa, part of Oshikoto and Omaheke and Kunene

regions and has a customer base of approximately 34,000 customers in its main supply area

(plus some 3,300 in the Omaheke Region and some 6,400 in Okahandja), ranging from large

power users to single-phase prepayment clients over an area of approximately 120 000 square

kilometres and 8 000 kilometres line infrastructure.

CENORED runs a coal-fired cogeneration (CHP) plant on the outskirts of Ruacana Waterfalls

(RW). The plant jointly produces:

• Electricity (sold into the grid), and

• Process steam (sold to nearby industrial clients).

• It also generates minor by-products (fly ash and gypsum) which are saleable.

Which are produced in three processes:

Process 1 - Fuel Preparation

At RW coal-fired cogeneration plant, the production process begins with fuel preparation .

Large consignments of raw coal are received, screened, crushed, and stored in silos before

being conveyed to the boiler bunkers. During this stage, normal handling losses such as dust

and moisture evaporation are expected of 2% of input with no scarp value. There is no opening

or closing inventory in any given month in this process.

Process 2 - Boiler & HP Steam Generation

• Prepared coal is burned to produce high-pressure (HP) steam

• Water treatment chemicals and demineralised water added; blowdown and

evaporation losses occur with normal loss as 5% of input and scrap value of N$40 per

tonne.

• Material and conversion cost both occur evenly throughout the process, with inspection

done when material & conversion are 50% complete.

FAM601Y, Assessment 6 (1 5r Opportunity)

2

© NUST2025

|

|

3 Page 3 |

▲back to top |

• Output measure: tonnes of HP steam transferred to Process 3 and inventory is valued

at weighted average.

Fuel Preparation - Process 1

Units placed in production in the current period

Costs incurred during the g_eriod

Finish goods

Normal loss

Boiler & HP Steam - Process 2

Work in process - beginning

Materials (40% completed)

Conversion (60% to be completed)

Previous process

Direct material

Conversion costs

Units placed in production in the current period

Costs incurred during the g_eriod

Previous process cost

Direct material

Conversion costs

Work in process - ending

Materials (50% completed)

Conversion (30% completed)

Normal loss

Units (kg)

Cost (N$)

50 000

52 500 000

49 000

?

1 000

?

Units (tonnes) Cost (N$)

20 000

19 950 000

2 273 500

6 851 375

?

?

45 660 000

12 600 000

5 000

?

Units completed and transferred to following process

?

Process 3 - Turbine-Generator with Steam Extraction (Joint split-off)

The steam produced is carried forward into the turbine hall, where the combined turbine and

generator convert its thermal energy into electricity. At the same time, part of the steam is

extracted at an intermediate pressure and sold directly to nearby industrial clients, marking

the split-off point for joint products. After this point, electricity is measured, transmitted into the

national grid, and subject to wheeling and system operator charges, while the process steam

is distributed through insulated pipelines to customers, incurring pumping and metering costs

along the way.

FAM601Y, Assessment 6 (1 5r Opportunity)

3

© NUST 2025

|

|

4 Page 4 |

▲back to top |

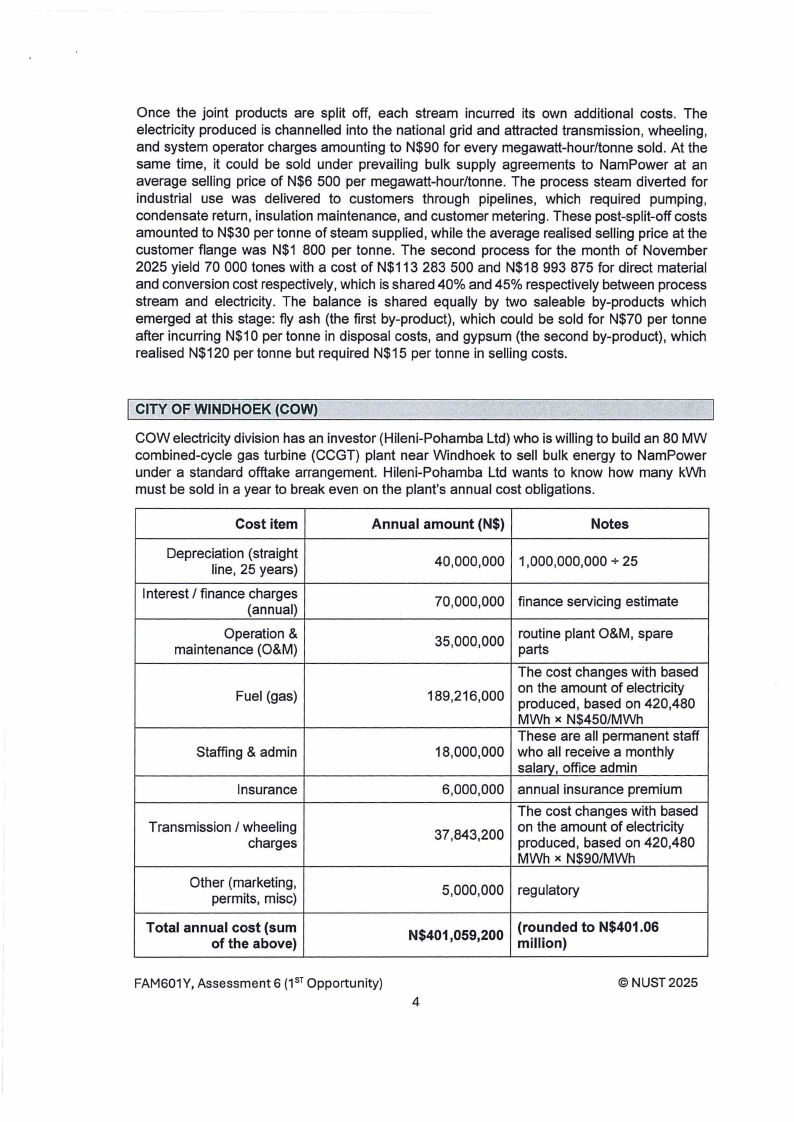

Once the joint products are split off, each stream incurred its own additional costs. The

electricity produced is channelled into the national grid and attracted transmission, wheeling,

and system operator charges amounting to N$90 for every megawatt-hour/tonne sold. At the

same time, it could be sold under prevailing bulk supply agreements to NamPower at an

average selling price of N$6 500 per megawatt-hour/tonne. The process steam diverted for

industrial use was delivered to customers through pipelines, which required pumping ,

condensate return, insulation maintenance, and customer metering. These post-split-off costs

amounted to N$30 per tonne of steam supplied , while the average realised selling price at the

customer flange was N$1 800 per tonne. The second process for the month of November

2025 yield 70 000 tones with a cost of N$113 283 500 and N$18 993 875 for direct material

and conversion cost respectively, which is shared 40% and 45% respectively between process

stream and electricity. The balance is shared equally by two saleable by-products which

emerged at this stage: fly ash (the first by-product), which could be sold for N$70 per tonne

after incurring N$10 per tonne in disposal costs, and gypsum (the second by-product), which

realised N$120 per tonne but required N$15 per tonne in selling costs.

I CITY OF WINDHOEK (COW)

COW electricity division has an investor (Hileni-Pohamba Ltd) who is willing to build an 80 MW

combined-cycle gas turbine (CCGT) plant near Windhoek to sell bulk energy to NamPower

under a standard offtake arrangement. Hileni-Pohamba Ltd wants to know how many kWh

must be sold in a year to break even on the plant's annual cost obligations.

Cost item

Depreciation (straight

line, 25 years)

Interest I finance charges

(annual)

Operation &

maintenance (O&M)

Fuel (gas)

Staffing & admin

Insurance

Transmission / wheeling

charges

Other (marketing ,

permits, misc)

Total annual cost (sum

of the above)

Annual amount (N$)

Notes

40,000,000 1,000,000,000 + 25

70,000,000 finance servicing estimate

35,000,000

routine plant O&M, spare

parts

189,216,000

18,000,000

The cost changes with based

on the amount of electricity

produced , based on 420,480

MWh x N$450/MWh

These are all permanent staff

who all receive a monthly

salary, office admin

6,000,000 annual insurance premium

37,843,200

The cost changes with based

on the amount of electricity

produced , based on 420,480

MWh x N$90/MWh

5,000,000 regulatory

N$401,059,200

(rounded to N$401.06

million)

FAM601Y, Assessment 6 (1 5r Opportunity)

4

©NUST2025

|

|

5 Page 5 |

▲back to top |

Reporting period : one year, the construction and installation cost of the plant is N$1 billion.

Assume the plant operates at an average utilisation that yields an overall production of

electricity shown below.

Technical assumptions

• Nameplate capacity: 80 MW.

• Hours per year: 8,760.

• Assumed plant utilisation factor: 60% (i.e. average output = 80 x 8,760 x 0.60).

• Annual generation (calculated): 420,480 MWh = 420,480,000 kWh.

• Selling price per MWh is N$2,061.10 per MWh.

I FINANCING BY INVESTOR

The investor of the 80 MW combined-cycle plant requires N$1 billion to fund construction.

Hileni-Pohamba Ltd is considering three financing routes:

1. Loan - Hileni-Pohamba Ltd has approached a consortium of local banks that has offered

them 10 year loan of the capital required repayable at the expiration of the loan with 12%

interest per annum, payable annually.

2. Preference shares - As an alternative, the company is considering issuing perpetual

preference shares to institutional investors with a current market price expected to N$95 per

share at issue and nominal value of N$100 per share and yielding returns of 11 %.

3.Right issue -The company has 150 million shares in issue with a historical value of N$15

each . The current trading price of the shares are N$25 and will be issued at N$20 to raise the

capital, they have sufficient authorise shares for the rights issue. The proposed rights issue is

1:2. The company's beta is 1.2 and expected market return of 14%. Government bonds

redeemable in 2029 and 2033 are yielding a return of 6% and 7%.

I CENORED, KING LLC & NAMPOWER

CENORED, one of Namibia's reg ional electricity distributors, faced mounting pressure to

expand and modernise its distribution infrastructure to reduce frequent outages in semi-urban

and rural areas. However, the company was struggling with liquidity constraints and already

carried significant arrears in payments owed to NamPower, its main supplier of bulk electricity.

To raise capital, CENORED entered into negotiations with a foreign private lnvestor(King

LLC), promising high returns on a new electrification and smart-metering project. In order to

persuade King LLC , CENORED presented projections showing unusually low bulk electricity

tariffs from NamPower. These tariffs were portrayed as "preferential rates" based on

CENORED's "strategic partnership" with the utility. However, in reality, no such preferential

agreement existed, and NamPower had in fact refused requests to lower tariffs, citing its own

financial sustainability challenges.

King LLC, convinced by the promised cost savings, agreed to inject over N$500 million into

the project. Contracts were signed , and funds were released. NamPower soon became aware

that its name and tariffs had been misrepresented in the Investor pitch. NamPower issued a

statement denying any preferential tariff arrangement with CENORED, which immediately

created tension between the entities. King LLC, upon learning of the misrepresentation,

FAM601Y, Assessment 6 (1 5r Opportunity)

© NUST 2025

5

|

|

6 Page 6 |

▲back to top |

threatened legal action but was locked into the financing agreement, exposing them to

potential losses.

At the same time, CENORED continued to enjoy the benefits of the financing and proceeded

with partial implementation of the project. In the· background, communities served by

CENORED began to worry that if the project failed or costs escalated, electricity tariffs might

increase further to cover losses. Local employees at CENORED also expressed discomfort,

as some had been asked to prepare promotional materials for the Investor that they knew

were misleading.

REQUIRED:

Sub-

total

A Calculate the value of goods completed and transferred (finished (24)

goods), value of work in process closing inventory units for Boiler &

HP Steam - Process 2.

Total

(25)

Presentation and lavout

(1)

B Hileni-Pohamba Ltd requires an annual return of 11 .5% of the capital

cost invested, calculate the minimum revenue that COW should (14) (14)

obtain to meet Hileni-Pohamba' Ltds request to break even.

C Based on the information under financing by investor, calculate:

(19)

1. The cheapest financing option

(20)

2. How many shares do the current shareholders of Hileni-Pohamba

Ltd need to maintain to keep their wealth as is before the rights issue.

Presentation and lavout

(1)

D . Using the ethical triangle, apply it on the information under heading (15)

"CENORED, King LLC & NamPower"

Presentation and la'i,OUt

(16)

(1)

TOTAL MARKS

75

FAM601Y, Assessment 6 (1 51 Opportunity)

6

© NUST2025

|

|

7 Page 7 |

▲back to top |

Question 2

25 Marks

I BUSINESS OVERVIEW

Angela Furniture Ltd is a medium-sized Namibian manufacturing company based in

Windhoek, Khomas Region. Founded by Angela lpinge in the early 2000s, the company

produces a range of solid wooden desks using locally sourced hardwood, which is polished

and finished in various designs. These desks are sold both locally and internationally.

Initially launched to complement the Namibia Trade Expo in 2016, where lead designer Henok

Brandt sponsored the office furniture section, the desks quickly gained popularity. As a result,

the company expanded its presence by participating in other national trade fairs and opening

four retail stores across Namibia.

Under the contract, the distributor will determine order volumes, and Angela Furniture Ltd will

fulfil the supply accordingly. The set price is N$2,800 per desk, consistent across both local

and export markets. However, Henok is hesitant, as she believes the company may be

capable of exporting directly to international retailers without relying on an intermediary.

I MANUFACTURING PROCESS

The production of a wooden desk begins with cutting kiln-dried hardwood planks into 2.5-

metre slabs using a precision saw. These slabs are then planed and polished to the required

smoothness, ensuring consistent quality.

Once prepared , the slabs are cut into specific patterns for the tabletop, drawers, and legs.

Additional fittings such as drawer handles, hinges, and screws are sourced separately. These

components are then assembled, beginning with frame construction , attaching legs, and

securing drawers, before sanding and staining for the final finish.

Each wooden desk takes approximately:

• 60 minutes for wood preparation and cutting,

• 90 minutes for assembly and joining,

The desks are sold individually and packaged for safe local and international transport.

Hardwood timber

Wood stain and varnish

Labour cost

Packaqinq (carton boxes)

Water and Electricity

Rent

Note 1

Note 2

Note 3

Note4

Note 5

Note 6

Notes:

1. Hardwood Timber: Angela Furniture Ltd sources high-quality hardwood planks from

Kavango Timbers. During the current financial year, the company acquired 36 000

metres of planks at a cost of N$95 per metre. An opening stock of 500 metres was

available from 2024 at N$90 per metre.

2. Stain and Varnish: The finishing process requires 500 millilitres of wood stain and

varnish per desk. Any purchased in the current and prior year were at N$60 per litre,

with 20 litres carried over as opening and closing stock each year.

FAM601Y, Assessment 6 (1 5r Opportunity)

©NUST2025

7

|

|

8 Page 8 |

▲back to top |

'<

3. Labour Costs:

a. Two qualified carpenters at N$35/hour,

b. Two assistant carpenters at N$18/hour,

c. A factory manager remunerated based on production volume (salary for 2025

was N$280,000).

4. Packaging : 15,500 cartons were purchased at N$8.00 each. Classified as insignificant,

excluded from production costing.

5. Utilities (Water & Electricity): Total annual cost= N$1, 108,200, apportioned as before

(50% fixed , variable split 70/30 between factorv and admin):

Month

Total meter reading

Total cost {R)

September

1,180

87,200

October

1,460

95,800

November

1,050

83,600

December

1,720

106,500

January

1,390

93,400

February

1,640

102,800

March

760

74,200

April

1,880

111 ,700

May

1,530

98,600

June

1,210

89,900

July

1,350

92,700

August

690

71 ,800

6. Rent: Facility rent for 250 m2 building= N$135,000. 210 m2 allocated to factory.

During the year, 14,500 desks were produced, of which 7,200 desks were sold, owing to the

effectiveness of the marketing strategy. There was no opening inventory of finished goods.

The company values inventory on a FIFO basis . No work-in-progress inventory at the start or

end of the year.

REQUIRED:

Sub-

total

A Prepare Angela Furniture Ltd's statement of goods manufactured for (24)

the year ended 31 August 2025.

Presentation and layout

(1)

Total

(25)

FAM601 Y, Assessment 6 (1 sr Opportunity)

8

© NUST2025