|

AUD701Y-AUDITING 300-2ND OPP-NOV 2025 |

|

|

1 Page 1 |

▲back to top |

nAmlBIA unlVERS.ITY

0 F SC IEn CE An D TECH n OLO.G Y

FACULTY OF COMMERCE, HUMAN SCIENCES AND EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING AND FINANCE

QUALIFICATION: BACHELOR OF ACCOUNTING (CHARTERED ACCOUNTANCY)

QUALIFICATION CODE: 07BACC

COURSE CODE: AUD701Y/ADA701Y

LEVEL: 7

COURSE NAME: AUDITING 300

SESSION: 15 NOVEMBER 2025

DURATION: 180 MINUTES

PAPER: THEORY AND PRACTICAL

MARKS: 100

SECOND OPPORTUNITY EXAMINATION QUESTION PAPER

EXAMINERS

MS M CLOETE

INTERNAL MODERATOR:

MS A GUSTAV

EXTERNAL MODERATOR:

MS E GROBBELAAR

INSTRUCTIONS:

1. This paper consists of EIGHT pages (Including this cover page). If your paper does not

contain all the pages, please put up your hand so that a replacement paper can be

handed to you.

2. Answer all the questions in blue or black ink only.

3. Each question should be answered on a separate page.

4. Questions relating to the paper may be raised in the initial 30 minutes after the start of

the paper. Thereafter, candidates must use their initiative to deal with any perceived

error or ambiguities & any assumption made by the candidate should be clearly stated.

5. Permissible materials include stationery and a non-programmable calculator only.

6. The neatness, disclosure and presentation of your answers will be considered when

marking your paper.

7. The scenarios presented are fictitious and any similarities, real or imagined, to real

events, people, places, organisations are purely coincidental and should be interpreted as

such.

1

|

|

2 Page 2 |

▲back to top |

QUESTION 1

{42 MARKS)

You are a third year trainee of an audit team, currently engaged on the audit of Fabrics {Pty) Ltd

{hereafter referred to as Fabrics). Fabrics is a clothing manufacturer and distributor, well known in

the retail industry for supplying quality clothing to stores such as Mr. Price, Woolworths and Pep.

The company has a large warehouse, situated in Prosperita, Windhoek. The company has a 30 June

year end.

The following working papers have been prepared by the audit team:

Woking paper reference

ABl00

CD200

Working paper description

Details of company equipment

Payroll controls, policies and procedures

Client: Fabrics (Pty) Ltd

Prepared by: r/.7'Ull«ee

AB100 Period end: 30 June 2025

Date: 20 July 2025

Reviewed by:

Date:

Details of Company Equipment

In October 2020, Fabrics purchased the land located in Prosperita, on which its clothing

n,anufacturing plant and various storage facilities are built. Due to the nature of its operations, the

~ompany has a substantial amount of equipment. The factory manager, Daniel Adam, provided the

pelow details:

1. Accounting Policy for Equipment

Fabrics accounts for its equipment using the cost model, in relation to IAS 16.

2. Additions

The company acquired additions for the current financial year end 30 June 2025 to the

amount of N$6 932 541. New equipment is purchased from both local suppliers, as well as

international suppliers.

Included in the additions amount above is a fast sewing machine, which is expected to

increase production of clothing tenfold. This machine was purchased from a French supplier,

who shipped the sewing machine (FOB) on 30 October 2024 from France. The machine

arrived at Fabrics on 6 December 2024, through delivery by a local shipping agent, DHL.

Fabrics makes use of DHL to administer all its shipping and customs admin for all its

imported PPE. DHL pays for all shipping and customs costs on behalf of Fabrics as they occur,

and thereafter invoices Fabrics to recover these costs, including DH L's service fees.

During December the staff of Fabrics installed the sewing machine in the warehouse of

Fabrics on a specially designed floor prepared for the sewing machine. Various tests were

performed by a specialist firm, TestaCon (Pty) Ltd, to ensure it operates as intended. The

French supplier was paid in full on 31 December 2024, for the invoiced price of 278 000

Euros. The entity provided the following exchange rates:

L

|

|

3 Page 3 |

▲back to top |

30 October 2024

6 December 2024

31 December 2024

1 euro = N$19.50

1 euro = N$19.20

1 euro = N$19.83

The sewing machine was brought into use on 3 January 2025.

3. Disposals

Due to numerous technological advancements in the current year, the company disposed of

various equipment. This was done to ensure the company stays up to date with changes in

the market. Disposals are handled by the chief warehouse manager.

4. Impairments

The company recognized an impairment for the current financial year, relating to one

printing machine, used to print wording and images on clothing. This machine has a carrying

value of N$467 950 as at 30 June 2025, however, as the specific laser part of the machine is

not manufactured by its supplier anymore, and has become quite worn out, this machine

can no longer be used. Auto Traders, a car part dealership, has agreed to buy this machine

from Fabrics for N$55 566 on 1 July 2025, as they can disassemble the machine and use its

various parts.

Client: Fabrics (Pty) Ltd

Prepared by: r/. 7 ~

Reviewed by:

Period end: 30 June 2025

Date: 15 July 2025

..

Date:

CD200

Payroll controls, policies and procedures

-abrics employs a number of salaried and wages employees. The audit team has noted the below

ontrols, policies and procedures implemented by the company:

1. For an employee to be successfully entered on the employee Masterfile, a valid income tax

number and identity number for the new employee must be entered in the designated field .

2. All new employees in the payroll section must write a computer literacy test and

demonstrate their computer skills and undergo training if needed .

3. The company has a computerised (biometric automated application control scanner)

timekeeping system; every morning, the factory manager reviews an on-screen report that

lists the name and section of any employee absent from or late for work.

4. The company's network is linked to its bank via the Internet; the bank's software that

enables this access and facilitates the payment of wages and salaries by EFT, is loaded on

only two terminals at Fabrics (Pty) Ltd.

5. Before the payroll is processed, the factory manager approves the schedule of overtime

hours recorded on the payroll software.

3

|

|

4 Page 4 |

▲back to top |

During the audit of Fabrics, you checked up on the junior audit trainee who is responsible for the

audit of the wages expense account of Fabrics. You asked the junior trainee about the assertions

applicable to this account, and he provided you with the following response:

"The shareholders are making the following assertions relating to this wage expense:

• Valuation = the value of the wages paid for the year is N$ 2 956 800.

• Completeness= all wages earned for the year are included in the amount.

• Existence= all employees who earned these wages exist at the reporting date.

• Rights = Fabrics has the right to pay wages at hourly rates as it sees fit, provided it is in line

with the labour law of Namibia.

YOU ARE REQUIRED TO:

QUESTION 1

TO BE ANSWERED ON A SEPARATE PAGE

MARKS

(a) With reference to working paper AB100, describe the substantive audit

(5)

procedures you would perform in respect of the existence assertion

applicable to the equipment at 30 June 2025.

(b) With reference to working paper AB100, describe the substantive audit

{10)

procedures you would perform to verify that the cost at which the new

sewing machine has been included in the financial records is

appropriate in terms of IFRS.

(c) With reference to working paper AB100, describe the substantive audit

procedures you will perform to:

i)

Obtain sufficient and appropriate audit evidence relating to

the impairment loss recorded in terms of the printing

machine.

ii)

Satisfy yourself that no other impairment losses relating to

PPE are required.

(d) With reference to working paper CD200:

i)

Indicate whether each control/policy/procedure listed is a

general control or automated application control. Where

you have identified a general control, specify the category

of general control into which it falls.

ii)

For each item listed (1 - 5), explain briefly whether each of

the controls is a preventative or detective control.

(e) Discuss, giving reasons, whether you agree with the response provided

by the junior trainee in relation to the wages expense. Ensure all

relevant assertions are addressed.

TOTAL MARKS: QUESTION 1

(5)

(4)

(5)

(5)

(8)

(42)

4

|

|

5 Page 5 |

▲back to top |

QUESTION 2

(58 MARKS)

You are an audit manager at PWX Inc, currently engaged on the audit of Proteas Limited (hereafter

referred to as Proteas). Proteas is a company that supplies flowers and bouquets to customers,

including events such as weddings, funerals or simply as office decor. The company has a 31 March

financial year end.

The following email and its related attachment, are the only communications sent to shareholders

regarding the Proteas annual general meeting (AGM):

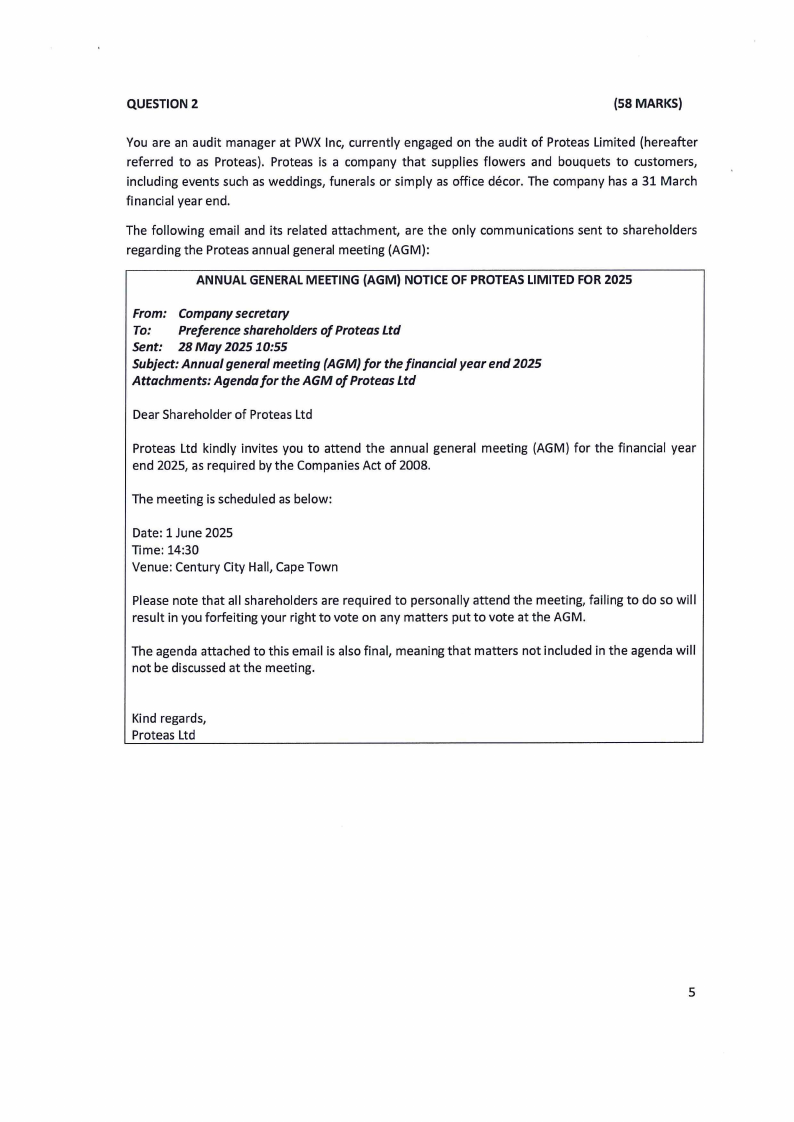

ANNUAL GENERAL MEETING (AGM) NOTICE OF PROTEAS LIMITED FOR 2025

From: Company secretary

To: Preference shareholders of Proteas Ltd

Sent: 28 May 202510:55

Subject: Annual general meeting (AGM) for the financial year end 2025

Attachments: Agendafor the AGM of Proteas Ltd

Dear Shareholder of Proteas Ltd

Proteas Ltd kindly invites you to attend the annual general meeting (AGM) for the financial year

end 2025, as required by the Companies Act of 2008.

The meeting is scheduled as below:

Date: 1 June 2025

Time: 14:30

Venue : Century City Hall, Cape Town

Please note that all shareholders are required to personally attend the meeting, failing to do so will

result in you forfeiting your right to vote on any matters put to vote at the AGM.

The agenda attached to this email is also final, meaning that matters not included in the agenda will

not be discussed at the meeting.

Kind regards,

Proteas Ltd

5

|

|

6 Page 6 |

▲back to top |

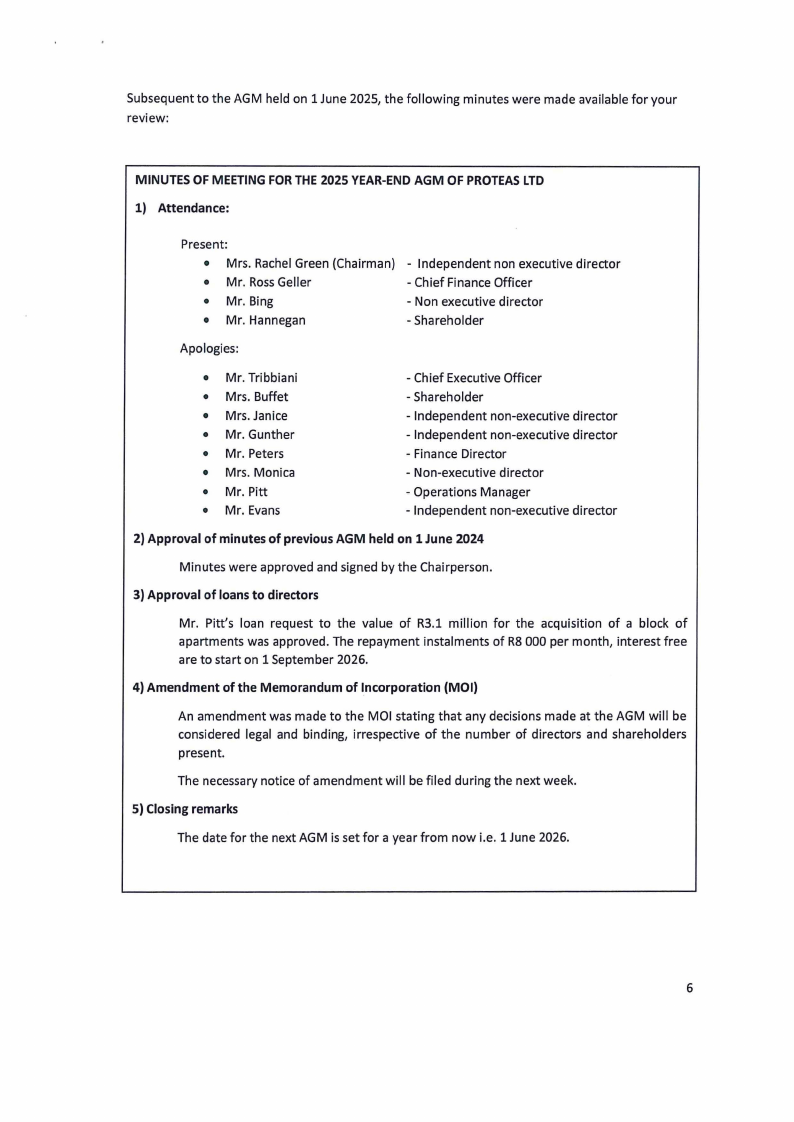

Subsequent to the AGM held on 1 June 2025, the following minutes were made available for your

review:

MINUTES OF MEETING FOR THE 2025 YEAR-END AGM OF PROTEAS LTD

1) Attendance:

Present:

• Mrs. Rachel Green (Chairman)

• Mr. Ross Geller

• Mr. Bing

• Mr. Hannegan

- Independent non executive director

- Chief Finance Officer

- Non executive director

- Shareholder

Apologies:

• Mr. Tribbiani

• Mrs. Buffet

• Mrs. Janice

• Mr. Gunther

• Mr. Peters

• Mrs. Monica

• Mr. Pitt

• Mr. Evans

- Chief Executive Officer

- Shareholder

- Independent non-executive director

- Independent non-executive director

- Finance Director

- Non-executive director

- Operations Manager

- Independent non-executive director

2) Approval of minutes of previous AGM held on 1 June 2024

Minutes were approved and signed by the Chairperson.

3) Approval of loans to directors

Mr. Pitt's loan request to the value of R3.1 million for the acquisition of a block of

apartments was approved. The repayment instalments of R8 000 per month, interest free

are to start on 1 September 2026.

4) Amendment of the Memorandum of Incorporation (MOI)

An amendment was made to the MOI stating that any decisions made at the AGM will be

considered legal and binding, irrespective of the number of directors and shareholders

present.

The necessary notice of amendment will be filed during the next week.

5) Closing remarks

The date for the next AGM is set for a year from now i.e. 1 June 2026.

6

|

|

7 Page 7 |

▲back to top |

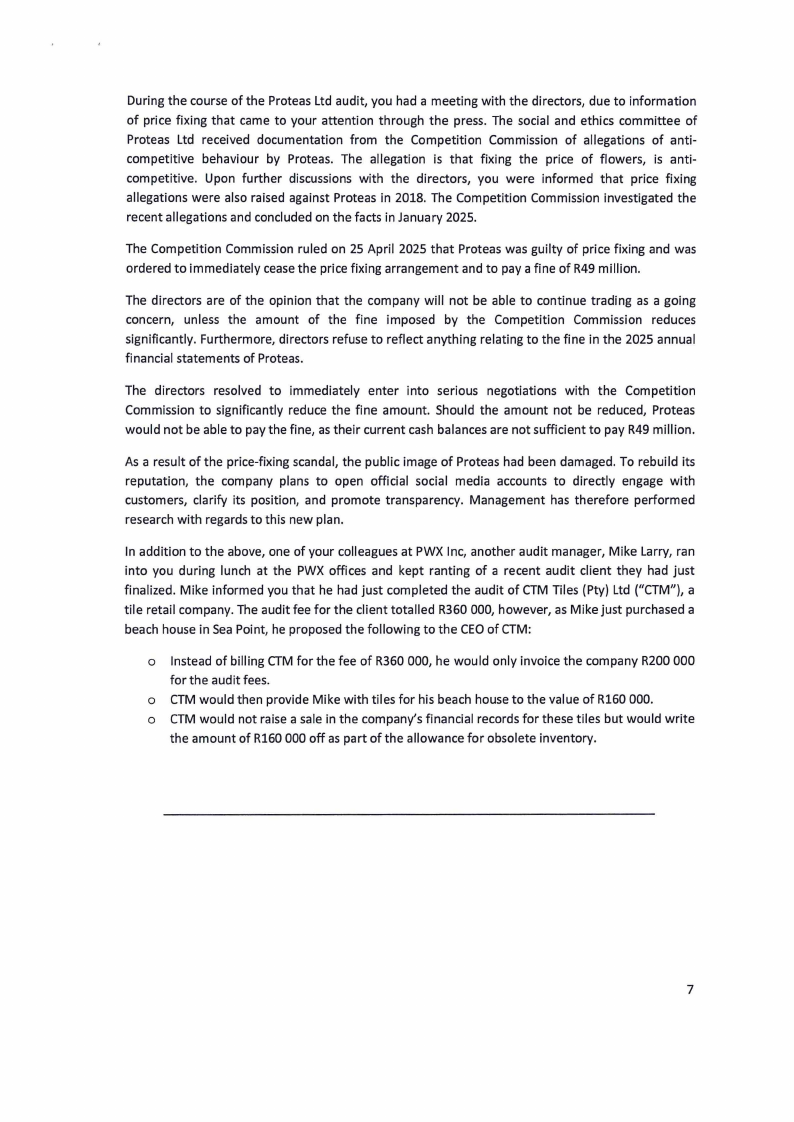

During the course of the Proteas Ltd audit, you had a meeting with the directors, due to information

of price fixing that came to your attention through the press. The social and ethics committee of

Proteas Ltd received documentation from the Competition Commission of allegations of anti-

competitive behaviour by Proteas. The allegation is that fixing the price of flowers, is anti-

competitive. Upon further discussions with the directors, you were informed that price fixing

allegations were also raised against Proteas in 2018. The Competition Commission investigated the

recent allegations and concluded on the facts in January 2025.

The Competition Commission ruled on 25 April 2025 that Proteas was guilty of price fixing and was

ordered to immediately cease the price fixing arrangement and to pay a fine of R49 million.

The directors are of the opinion that the company will not be able to continue trading as a going

concern, unless the amount of the fine imposed by the Competition Commission reduces

significantly. Furthermore, directors refuse to reflect anything relating to the fine in the 2025 annual

financial statements of Proteas.

The directors resolved to immediately enter into serious negotiations with the Competition

Commission to significantly reduce the fine amount. Should the amount not be reduced, Proteas

would not be able to pay the fine, as their current cash balances are not sufficient to pay R49 million.

As a result of the price-fixing scandal, the public image of Proteas had been damaged. To rebuild its

reputation, the company plans to open official social media accounts to directly engage with

customers, clarify its position, and promote transparency. Management has therefore performed

research with regards to this new plan.

In addition to the above, one of your colleagues at PWX Inc, another audit manager, Mike Larry, ran

into you during lunch at the PWX offices and kept ranting of a recent audit client they had just

finalized. Mike informed you that he had just completed the audit of CTM Tiles (Pty) Ltd ("CTM"), a

tile retail company. The audit fee for the client totalled R360 000, however, as Mike just purchased a

beach house in Sea Point, he proposed the following to the CEO of CTM:

o Instead of billing CTM for the fee of R360 000, he would only invoice the company R200 000

for the audit fees.

o CTM would then provide Mike with tiles for his beach house to the value of R160 000.

o CTM would not raise a sale in the company's financial records for these tiles but would write

the amount of R160 000 off as part of the allowance for obsolete inventory.

7

|

|

8 Page 8 |

▲back to top |

I•

-

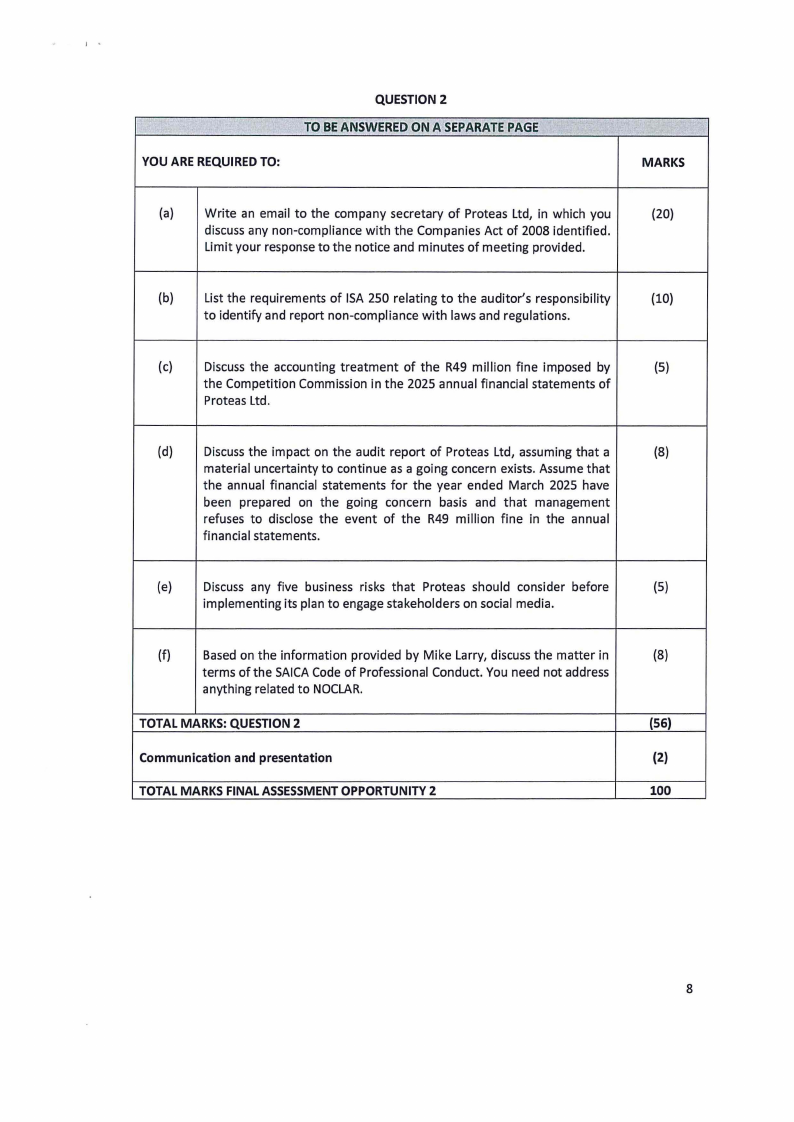

YOU ARE REQUIRED TO:

QUESTION 2

TO BE ANSWERED ON A SEPARATE PAGE

MARKS

(a) Write an email to the company secretary of Proteas Ltd, in which you

(20)

discuss any non-compliance with the Companies Act of 2008 identified.

Limit your response to the notice and minutes of meeting provided.

(b) List the requirements of ISA 250 relating to the auditor's responsibility

(10)

to identify and report non-compliance with laws and regulations.

(c) Discuss the accounting treatment of the R49 million fine imposed by

(5)

the Competition Commission in the 2025 annual financial statements of

Proteas Ltd.

(d) Discuss the impact on the audit report of Proteas Ltd, assuming that a

(8)

material uncertainty to continue as a going concern exists. Assume that

the annual financial statements for the year ended March 2025 have

been prepared on the going concern basis and that management

refuses to disclose the event of the R49 million fine in the annual

financial statements.

(e) Discuss any five business risks that Proteas should consider before

(5)

implementing its plan to engage stakeholders on social media.

(f)

Based on the information provided by Mike Larry, discuss the matter in

(8)

terms of the SAICA Code of Professional Conduct. You need not address

anything related to NOCLAR.

TOTAL MARKS: QUESTION 2

(56)

Communication and presentation

(2)

TOTAL MARKS FINAL ASSESSMENT OPPORTUNITY 2

100

8