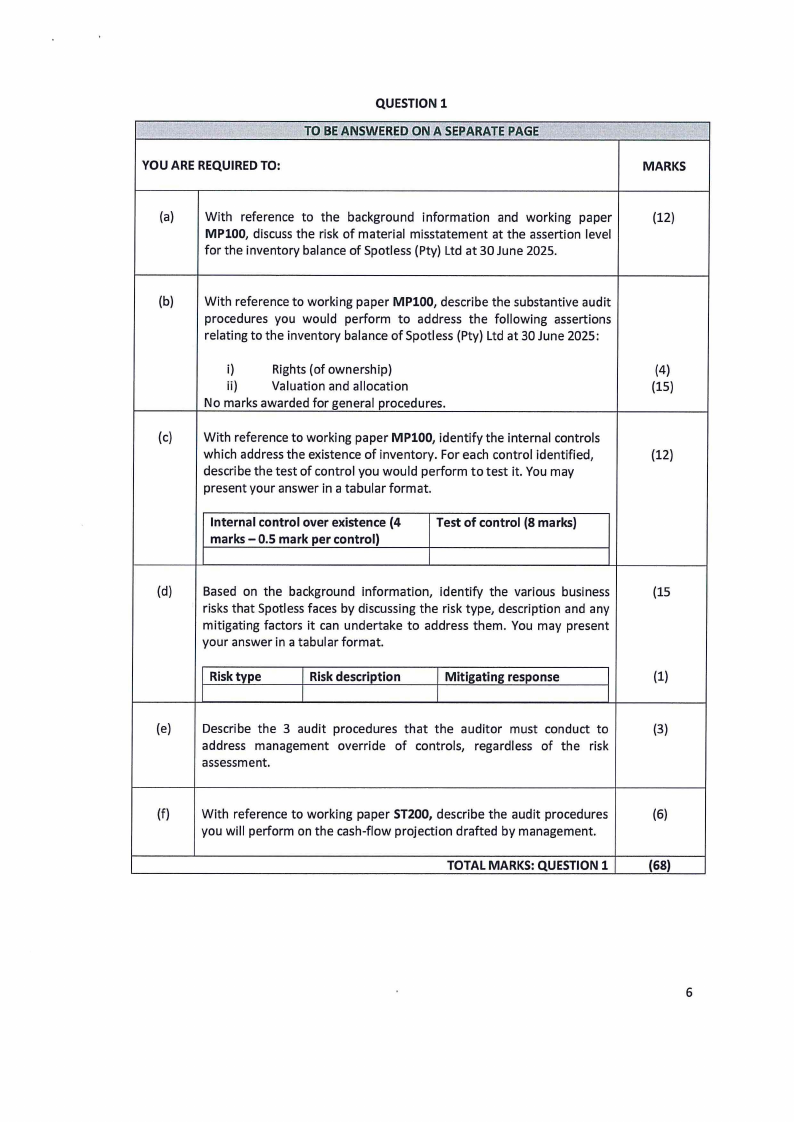

QUESTION 1

(68 MARKS)

You are a member of the audit team, currently engaged on the audit of Spotless {Pty) Ltd {hereafter

referred to as Spotless). Spotless is a manufacturing company that specializes in the production of all

goods relating to personal care and hygiene. The company has a 30 June financial year end.

Background information

Spotless operates from a huge warehouse, situated in Northern Industry in Windhoek, with a factory

situated right next to the warehouse. The factory allows the company to manufacture its products

seamlessly, while the warehouse serves as a storage facility for raw materials, work-in-progress and

finished goods, as well as a serves as the store outlet for customers.

Spotless' products include items such as soap, toothpaste, hand soap, shampoo, facecloths, cotton

buds, and many more hygienic goods. Some of the hygienic products it sells, such as specific scented

soaps and shampoos are imported from Europe, due to the quality of ingredients used in these

products. Due to the wide range of hygiene items it sells, Spotless has a customer base that entails

both corporate entities and personal homes. Corporate companies can place bulk orders in advance.

The company was established in 2011, and due to the Covid pandemic, there was a huge increase in

the demand for its products. This surge resulted in the company performing well for the pandemic

period, but simultaneously lead to many other hygiene companies entering the market to tap into

the worldwide pandemic and its impact on preventing the spread of Covid. Since Covid, many of the

competitors have remained in the market, and this saturation has led to Spotless's financial

performance deteriorating. As a result of this weakened performance, Spotless had to take out a

loan from Medium Bank during February 2025. Additionally, the new market entrants have

introduced various hygiene products that cater to the younger Gen Z's, whereas the product base of

Spotless has remained similar since its inception.

The company has a sound internal control process, however, management is anxious that the

company's financial situation be presented as favorably as possible.

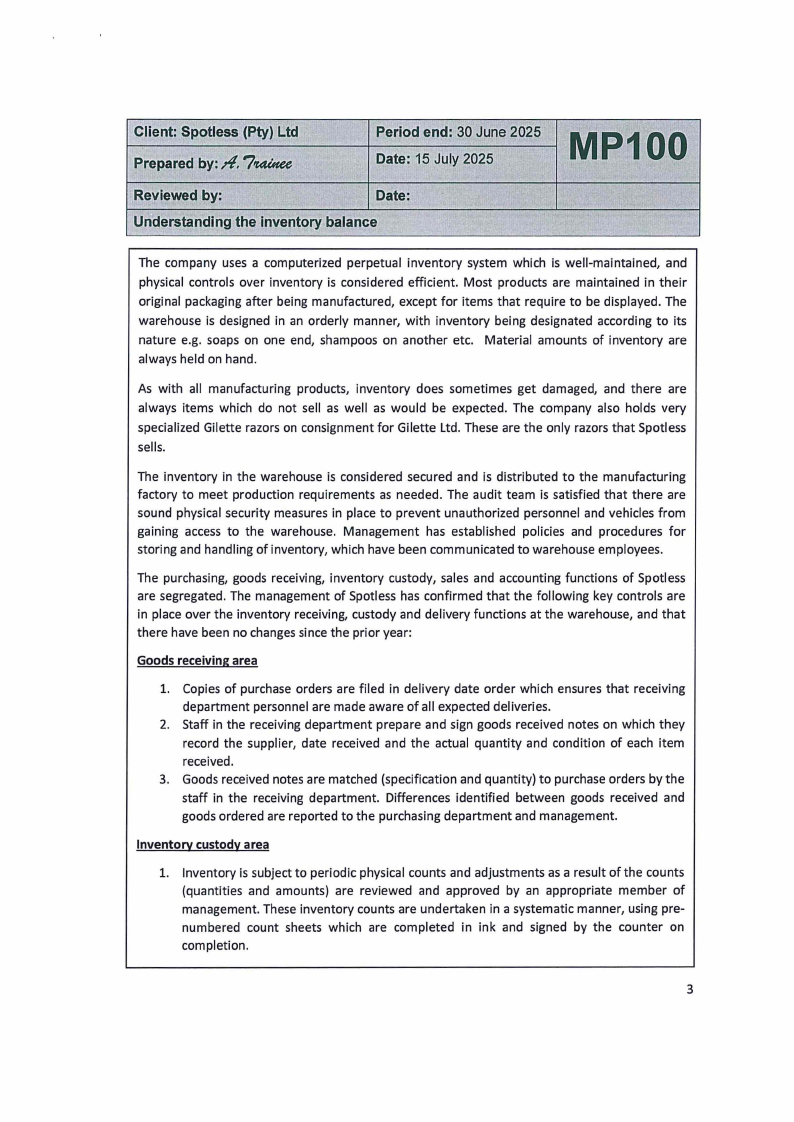

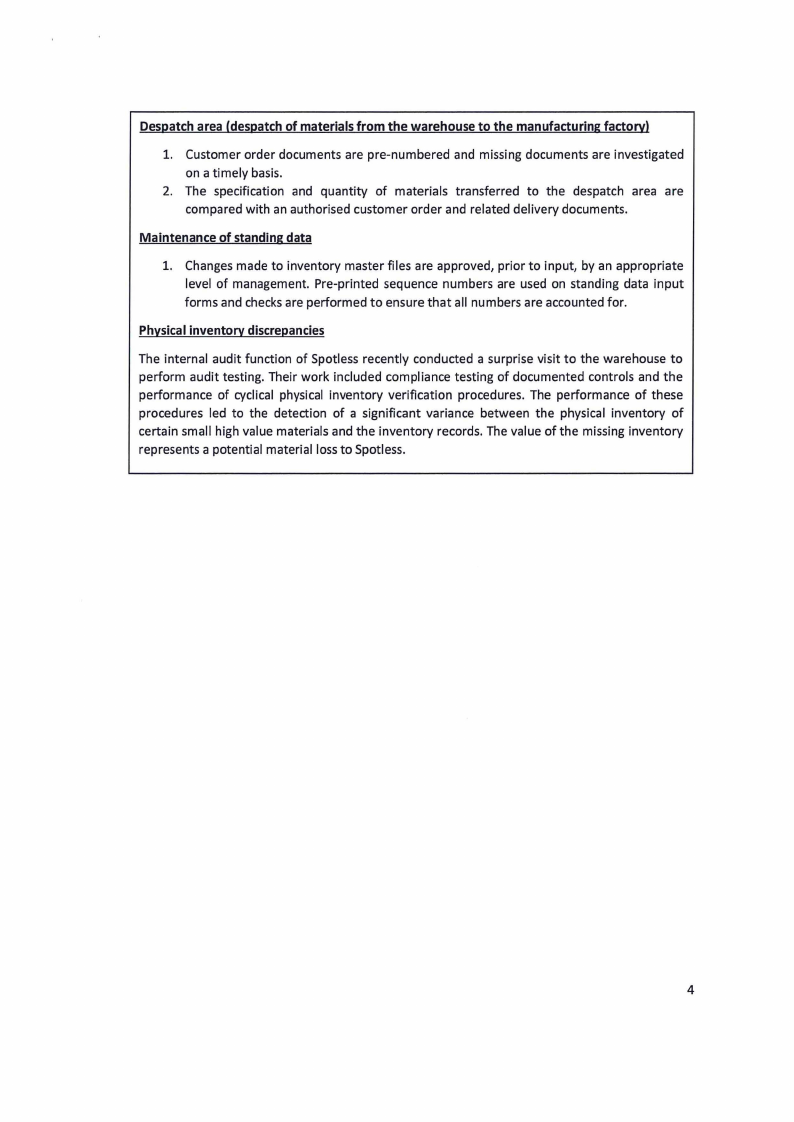

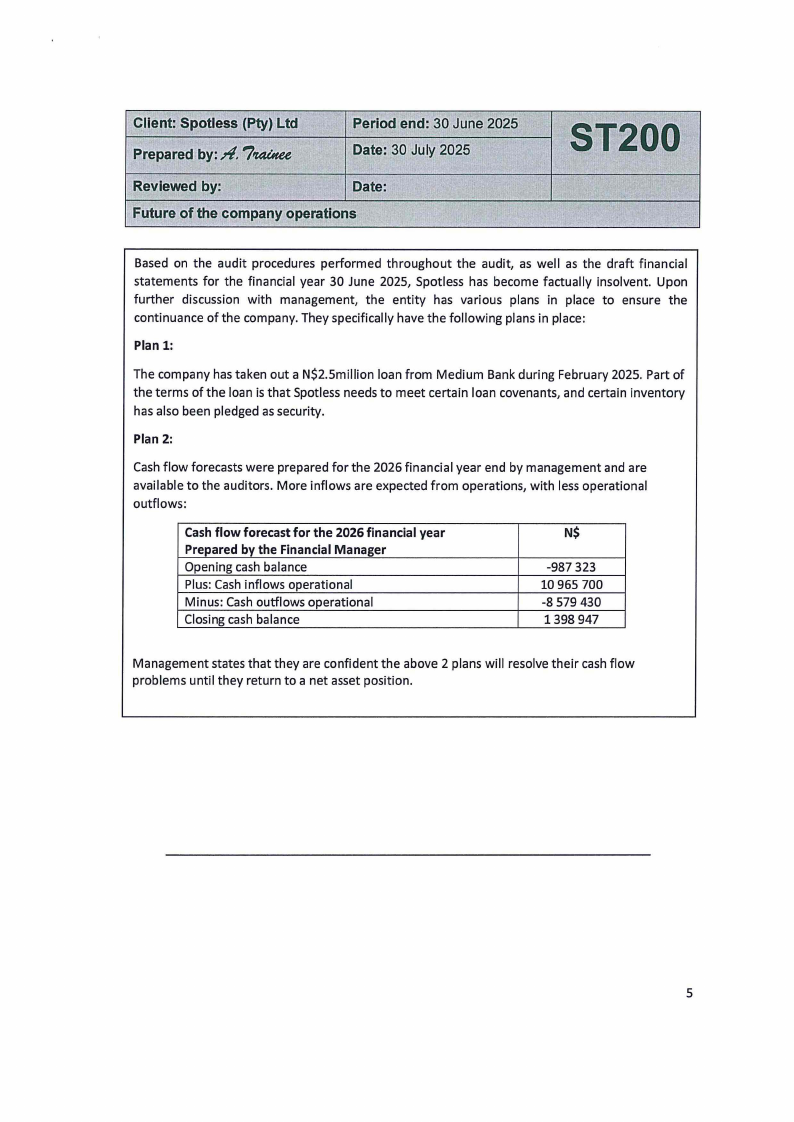

The following working papers have been prepared by the audit team:

Woking paper reference

MP100

ST200

Working paper description

Understanding the inventory balance

Future of the company operations

2