FINANCIAL MANAGEMENT FAM701Y (FAM300) NOVEMBER 2025 FIRST OPPORTUNITY

ASSESSMENT

I MEDIA REPORTS

Report 1: Whale Rock plans to acquire Schwenk Namibia, 18 March 2025

In March 2025, Whale Rock Cement {Pty) Ltd, the parent company of Cheetah Cement, has

filed a notice to acquire Schwenk Namibia, which holds a majority stake in Ohorongo Cement.

Ohorongo Cement serves both the local Namibian market and exports to neighbouring

countries like Angola, South Africa, Zambia, Botswana and Zimbabwe.

If successful, the transaction, filed with the Namibian Competition Commission {NCC) would

give Whale Rock Cement complete control over cement production in Namibia.

The deal involves Whale Rock Cement acquiring the entire issued share capital of Schwenk

Namibia from SCHWENK Zement International GmbH & Co KG. Schwenk Namibia holds a

69.83 per cent stake in Ohorongo Cement, with the remaining shares held by Industrial Corp

South Africa {14.27 per cent), Development Bank of Namibia {11 .73 per cent) and

Development Bank of Southern Africa {4.17 per cent).

The company is not the first to attempt acquisition of Schwenk Namibia. In 2020, a proposed

merger between Schwenk Namibia and West China Cement Ltd was blocked due to concerns

over collusion between two cement producers. It followed a SGD1.5bn {US$1126.87m)

acquisition announcement by Singapore-listed International Cement Group that did not

materialise.

Source: Whale Rock plans to acquire Schwenk Namibia from International Cement Review

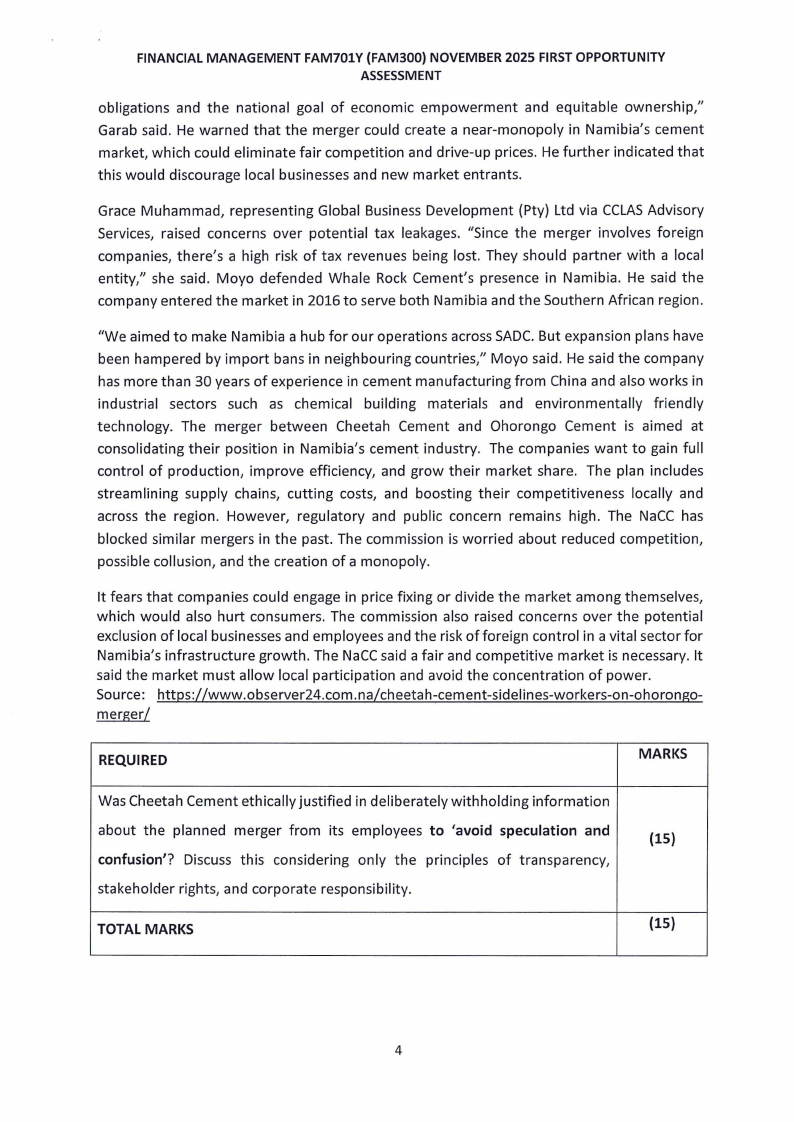

Report 2: Cheetah Cement sidelines workers on Ohorongo merger

Cheetah Cement did not inform its workers about the planned merger with Ohorongo

Cement. This came to light during a stakeholders' conference held in Windhoek by the

Namibian Competition Commission {NaCC). Cheetah Cement said it deliberately withheld the

information from workers. A spokesperson for the company, Tabby Moyo, stated that they

deliberately withheld the information to prevent speculation and confusion . "The decision is

to avoid speculations and confusion among employees," Moyo said . Meanwhile, Meyer van

den Berg, the legal representative of Ohorongo Cement, informed their employees about the

planned acquisition through a memo. The proposed merger has faced rejection from several

stakeholders at the conference. Most raised concerns about a monopoly forming in the

cement sector. Others questioned why local companies were not given a chance to buy

Ohorongo Cement, which is owned by Schwenk Namibia {Pty) Ltd.

George Garab, representing Otavi Cement Group {Pty) Ltd, said local ownership is key and

that the merger goes against government efforts to promote it. "Even though Otavi Cement

Group owns the licence to the farm where Ohorongo Cement operates, we were never given

an opportunity to purchase Ohorongo," said Garab.

He said Ohorongo Cement was supported by the Otavi Town Council and other authorities to

obtain an operational license. Now, he claimed, the company is being sold off in secret,

excluding local investors and the government. "This undermines the spirit of its foundational

3