|

PAR812S-PUBLIC SECTOR FINANCIAL ACCOUNTING AND REPORTING-1ST OPP-NOV 2024 |

|

|

1 Page 1 |

▲back to top |

nAmlBIA UnlVERSITY

OF SCIEn CE Ano TECHn OLOGY

FACULTY OF COMMERCE, HUMAN SCIENCES AND EDUCATION

DEPARTMENT OF ACCOUNTING, ECONOMICS AND FINANCE

QUALIFICATION: BACHELOR OF ACCOUNTING HONORS

QUALIFICATION CODE: 08BOAH LEVEL: 8

COURSE CODE: PAR812S

COURSE NAME: PUBLIC SECTOR FINANCIAL

ACCOUNTING AND REPORTING

DATE: November 2024

DURATION: 3 HOURS

PAPER:THEORYAND CALCULATIONS

MARKS: 100

1st OPPORTUNITY EXAMINATION

EXAMINER(S) Dr. S. Dzomira

MODERATOR: Mr. Mutonga Samuel Mukelebai

INSTRUCTIONS

1. Capture your full name, student number and assessment number on the first page

2. Answer ALL the questions and manage yourtime properly.

3. Number each page correctly

4. Write clearly and neatly.

5. Do not write in pencil and do not use tip-ex, as this will not be marked.

6. The names of people and businesses used throughout this assessment do not reflect

the reality and may be purely coincidental.

7. Use a non-programmable calculator.

8. SHOW ALL WORKINGS!

THIS QUESTION PAPER CONSISTS OF 3 PAGES (excluding this front page)

Page 1 of4

|

|

2 Page 2 |

▲back to top |

Question 1 (60 marks)

Below are the transactions of the consolidated fund for the year ended 31 December 2023

Dr

Cr

N$

N$

Taxes Paid by Individual

15,731,289

Taxes Paid by Companies

11,468,455

Other Direct taxes

6,765,102

Excises

9,433,578

Taxes on Goods and Services

8,021,037

Taxes on Exports

5,350,772

Program Grant

8,148,127

Project Grant

4,988,181

District Development

4,941,719

Property Income

8,758,558

Sales of Goods and Services

5,763,905

Fines, Penalties and Forfeiture

4,963,027

Established Position

12,138,953

Non Established Position

729,399

Allowances

2,192,931

13% SSF

7,195

Utilities

1,125,614

General Cleaning

392,137

Rentals

18,706

Travel and Transport

284,023

Training, Seminar and Conference

72,618

Consultancies

2,431,582

Materials and Consumables

1,754,361

Social Benefit

3,687,172

Capitation Grant Subsides

293,414

Fertilizer Subsidy

292,134

Schools Subsidy

99,381

Utility Subsidy

831,291

Other Expenditure

1,965,089

Consumption of Plant and Equipment

10,005,389

GETFUND

587,683

District Assembly Common Fund

989,171

Trust Monies

10,200,478

Cash and Cash Equivalent

9,341,283

Loans

2,313,142

Equity Investment

4,921,314

Advances

1,231,162

Domestic Loans

13,203,380

External Loans

20,095,386

Page 2 of4

|

|

3 Page 3 |

▲back to top |

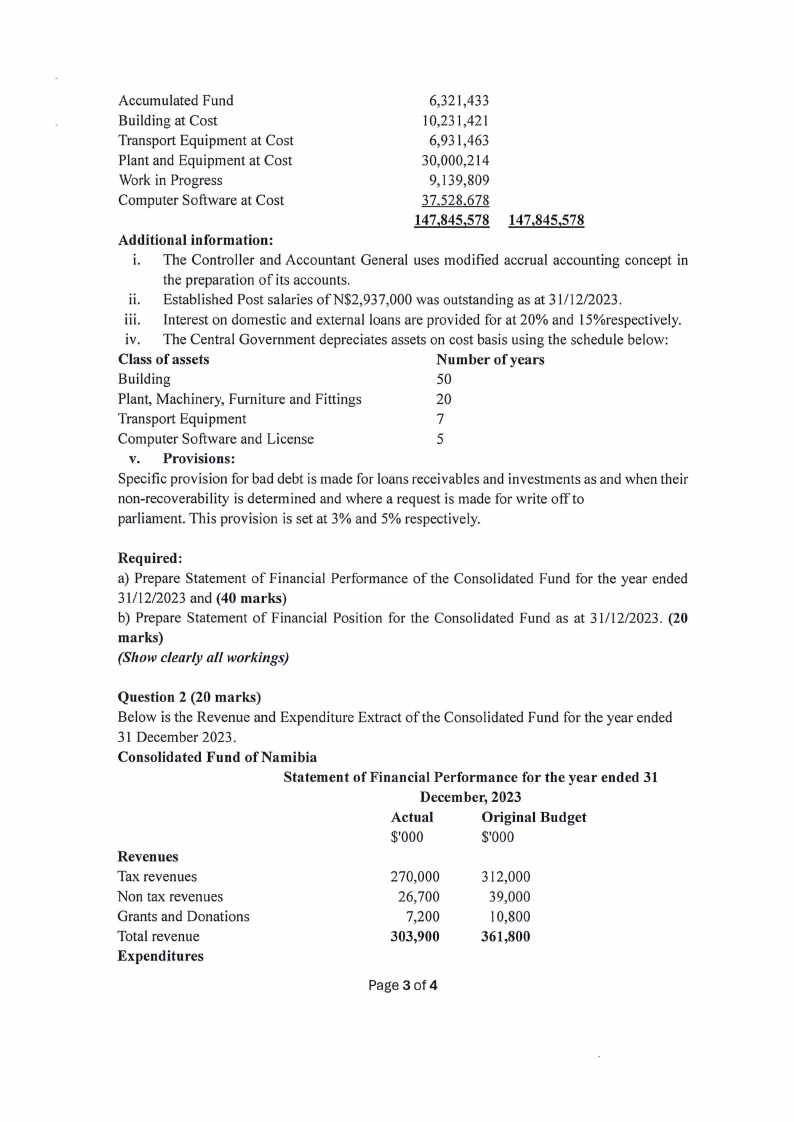

Accumulated Fund

6,321,433

Building at Cost

10,231,421

Transport Equipment at Cost

6,931,463

Plant and Equipment at Cost

30,000,214

Work in Progress

9,139,809

Computer Software at Cost

37,528,678

147,845,578 147,845,578

Additional information:

i. The Controller and Accountant General uses modified accrual accounting concept in

the preparation of its accounts.

ii. Established Post salaries ofN$2,937,000 was outstanding as at 31/12/2023.

iii. Interest on domestic and external loans are provided for at 20% and 15%respectively.

iv. The Central Government depreciates assets on cost basis using the schedule below:

Class of assets

Number of years

Building

50

Plant, Machinery, Furniture and Fittings

20

Transport Equipment

7

Computer Software and License

5

v. Provisions:

Specific provision for bad debt is made for loans receivables and investments as and when their

non-recoverability is determined and where a request is made for write off to

parliament. This provision is set at 3% and 5% respectively.

Required:

a) Prepare Statement of Financial Performance of the Consolidated Fund for the year ended

31/12/2023 and (40 marks)

b) Prepare Statement of Financial Position for the Consolidated Fund as at 31/12/2023. (20

marks)

(Show clearly all workings)

Question 2 (20 marks)

Below is the Revenue and Expenditure Extract of the Consolidated Fund for the year ended

31 December 2023.

Consolidated Fund of Namibia

Statement of Financial Performance for the year ended 31

Decem her, 2023

Actual

Original Budget

$'000

$'000

Revenues

Tax revenues

270,000

312,000

Non tax revenues

26,700

39,000

Grants and Donations

7,200

10,800

Total revenue

303,900

361,800

Expenditures

Page 3 of 4

|

|

4 Page 4 |

▲back to top |

Compensation of employees

121,500

124,800

Goods and Services

54,000

120,700

Consumption of fixed capital

1,950

Interest

81,000

82,100

Social benefit cost

1,500

1,800

Subsidies

1,080

1,170

Grants

2,700

2,910

Other expenditure

34,020

32,000

Total expenditure

297,750

365,480

Net Operating result

6,150

(3,680)

Additional information:

The Minister for Finance, has presented a mid-year budget review to Parliament that included

a supplementary (additional) budget fl or 2023. The Minister has cited several local and

international reasons for the budget adjustments. The approved supplementary budget is as

follows:

N$'000

Compensation of employees

11,500

Goods and services

17,000

Interest

2,500

Social benefit cost

1,500

Subsidies

180

Total expenditure

32,680

Required:

Prepare a Budget Performance Statement (20 marks)

Question 3 (20 marks)

a) Accounting Concepts and Bases are broad basic assumptions, which underlie the preparation

of the periodic financial statements of entities in the public sector. Unless stated, it would be

assumed that they have been adhered to when preparing financial statements.

Required:

Explain THREE (4) key characteristics of each of the following Accounting Bases used in

Public Sector Accounting:

i) Commitment accounting

ii) Accrual accounting

iii) Cash accounting (12 marks)

b) One objective of Public Sector Accounting is accountability. Accountability requires that

government justifies how public resources are raised and utilized by means of Financial

Reporting. Financial Reporting helps to improve the performance of, and trust in, the public

sector.

Required:

Explain FOUR (4) other objectives of Financial Reporting in public sector organisations. (8

marks)

Page4 of 4