|

PAR812S-PUBLIC SECTOR FINANCIAL ACCOUNTING AND REPORTING-1ST OPP-NOV 2025 |

|

|

1 Page 1 |

▲back to top |

n Am I BI A u n IVE RS ITV

OF SCIEnCE Ano TECHnOLOGY

FACULTY OF COMMERCE, HUMAN SCIENCES AND EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING & FINANCE

QUALIFICATION: BACHELOR OF ACCOUNTING {HONOURS)

QUALIFICATION CODE: 08BOAH

COURSE CODE: PAR812S

LEVEL: 8

COURSE NAME: PUBLIC SECTOR FINANCIAL

ACCOUNTING & REPORTING

SESSION: NOVEMBER 2025

DURATION: 3 HOURS

PAPER: THEORY AND APPLICATION

MARKS: 100

FIRST OPPORTUNITY EXAMINATION QUESTION PAPER

EXAMINERS: Mr. Kuhepa Tjondu

MODERATOR: Mr. Emmanuel Milijala

INSTRUCTIONS

• This question paper is made up of THREE (3) questions.

• Answer All the questions and in blue or black ink.

• Show all your working in the answer sheet.

• Start each question on a new page in your answer booklet and show all your workings.

• Questions relating to this paper may be raised in the initial 30 minutes after the start of

the paper. Thereafter, candidates must use their initiative to deal with any perceived error

or ambiguities and any assumption made by the candidate should be clearly stated.

PERMISSIBLE MATERIALS

Non-programmable calculator/financial calculator

THIS QUESTION PAPER CONSISTS OF 6 PAGES {Including this front page)

1

|

|

2 Page 2 |

▲back to top |

QUESTION 1

[25 MARKS]

A public sector entity purchases a site to be used for landfill waste disposal. The

purchase includes the land and bu ildings on the site. The public sector entity assumes

the liability to restore the site at the end of its useful life. No staff or processes are

transferred as a result of the purchase .

Required:

(a) Does the purchase of the landfill waste disposal site constitute a public sector

combination? Explain your reasoning .

(5 marks)

The territorial boundaries of two existing municipalities, A and B, are redrawn by

Parliament through legislation; neither Parliament nor Central Government controls A

or B. Responsibility for part of each municipality's former territory is transferred to a

new municipality, C. Operations in respect of the transferred territories are combined

to form C.

A and B remain otherwise unchanged and retain their governing bodies. A new

governing body (unrelated to the governing bodies of A and B) is elected for C to

manage the operations that are transferred from the other municipalities.

(b) Should this public sector combination above be classified as an amalgamation

or an acquisition?

(5 marks)

(c) List 10 Disclosures made in respect of the GGS in line with IPSAS 22, Disclosure

of Financial Information about the General Government Sector.

(10 marks)

(d) What are the conditions that must be satisfied for Revenue from the sale of

goods to be Recognised in line with IPSASs 9 Revenue from Exchange

Transactions?

(5 marks)

2

|

|

3 Page 3 |

▲back to top |

QUESTION 2

[25 MARKS]

a) Discuss the objectives and scope of IPSAS 33 First-time Adoption of Accrual

Basis International Public Sector Accounting Standards (IPSASs).

(10 marks)

b) What are some of the advantages and arguments if favour of adopting accrual

basis IPSASs.

(5 mark)

c) What are the challenges that must be addressed when adopting IPSASs for

the first time?

(5 marks)

d) What are the Critical Success Factors when it comes to the implementation of

IPSASs?

(5 marks)

3

|

|

4 Page 4 |

▲back to top |

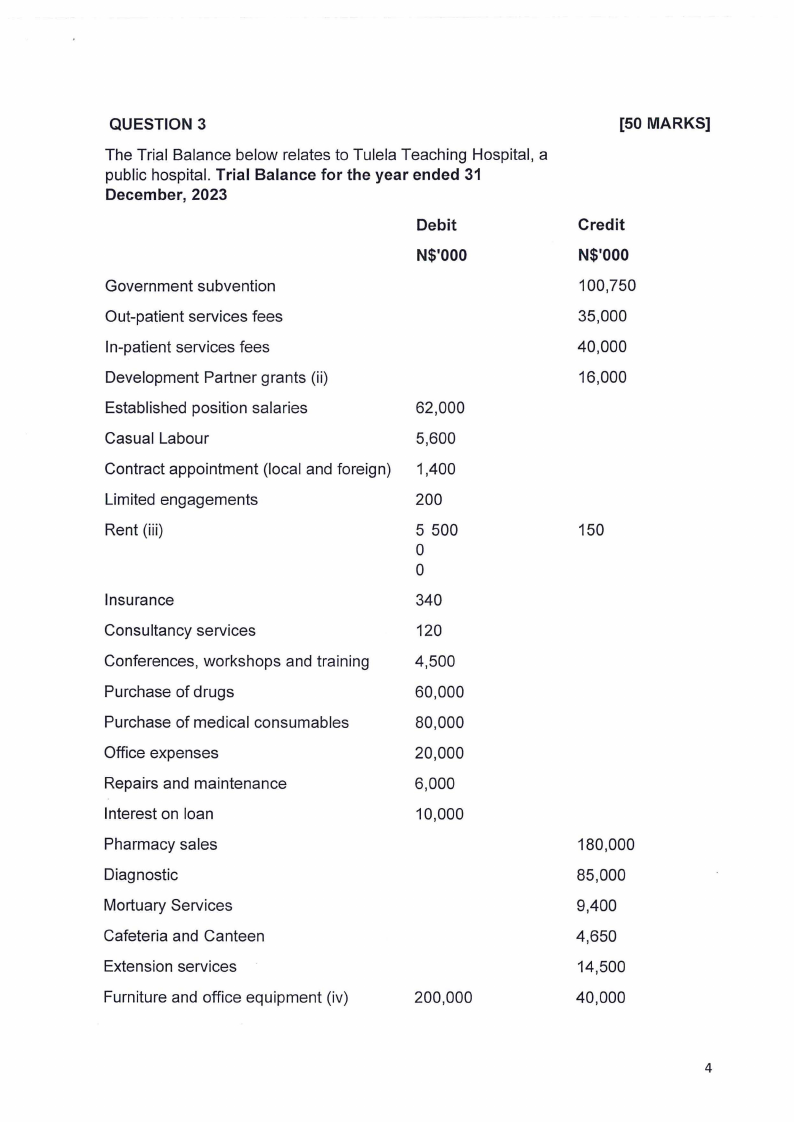

QUESTION 3

The Trial Balance below relates to Tulela Teaching Hospital, a

public hospital. Trial Balance for the year ended 31

December, 2023

Debit

N$'000

Government subvention

Out-patient services fees

In-patient services fees

Development Partner grants (ii)

Established position salaries

62,000

Casual Labour

5,600

Contract appointment (local and foreign) 1,400

Limited engagements

200

Rent (iii)

5 500

0

0

Insurance

340

Consultancy services

120

Conferences, workshops and training

4,500

Purchase of drugs

60,000

Purchase of medical consumables

80,000

Office expenses

20,000

Repairs and maintenance

6,000

Interest on loan

10,000

Pharmacy sales

Diagnostic

Mortuary Services

Cafeteria and Canteen

Extension services

Furniture and office equipment (iv)

200,000

[50 MARKS]

Credit

N$'000

100,750

35,000

40,000

16,000

150

180,000

85,000

9,400

4,650

14,500

40,000

4

|

|

5 Page 5 |

▲back to top |

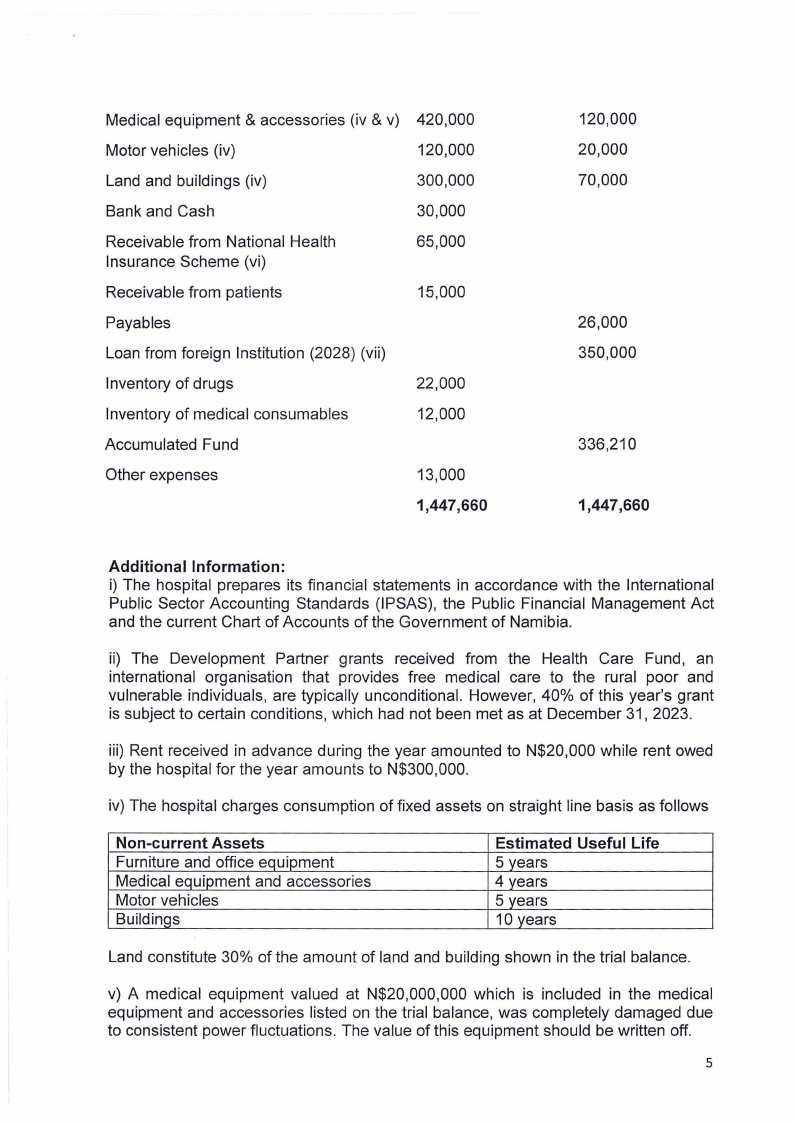

Medical equipment & accessories (iv & v) 420,000

Motor vehicles (iv)

120,000

Land and buildings (iv)

300,000

Bank and Cash

30,000

Receivable from National Health

Insurance Scheme (vi)

65 ,000

Receivable from patients

15,000

Payables

Loan from foreign Institution (2028) (vii)

Inventory of drugs

22,000

Inventory of medical consumables

12,000

Accumulated Fund

Other expenses

13 ,000

1,447,660

120,000

20,000

70,000

26,000

350,000

336,210

1,447,660

Additional Information:

i) The hospital prepares its financial statements in accordance with the International

Public Sector Accounting Standards (IPSAS), the Public Financial Management Act

and the current Chart of Accounts of the Government of Namibia.

ii) The Development Partner grants received from the Health Care Fund, an

international organisation that provides free medical care to the rural poor and

vulnerable individuals, are typically unconditional. However, 40% of this year's grant

is subject to certain conditions, which had not been met as at December 31, 2023.

iii) Rent received in advance during the year amounted to N$20,000 while rent owed

by the hospital for the year amounts to N$300,000.

iv) The hospital charges consumption of fixed assets on straight line basis as follows

Non-current Assets

Furniture and office equipment

Medical equipment and accessories

Motor vehicles

Buildings

Estimated Useful Life

5 years

4 years

5 years

10 years

Land constitute 30% of the amount of land and building shown in the trial balance.

v) A medical equipment valued at N$20,000,000 which is included in the medical

equipment and accessories listed on the trial balance, was completely damaged due

to consistent power fluctuations . The value of this equipment should be written off.

5

|

|

6 Page 6 |

▲back to top |

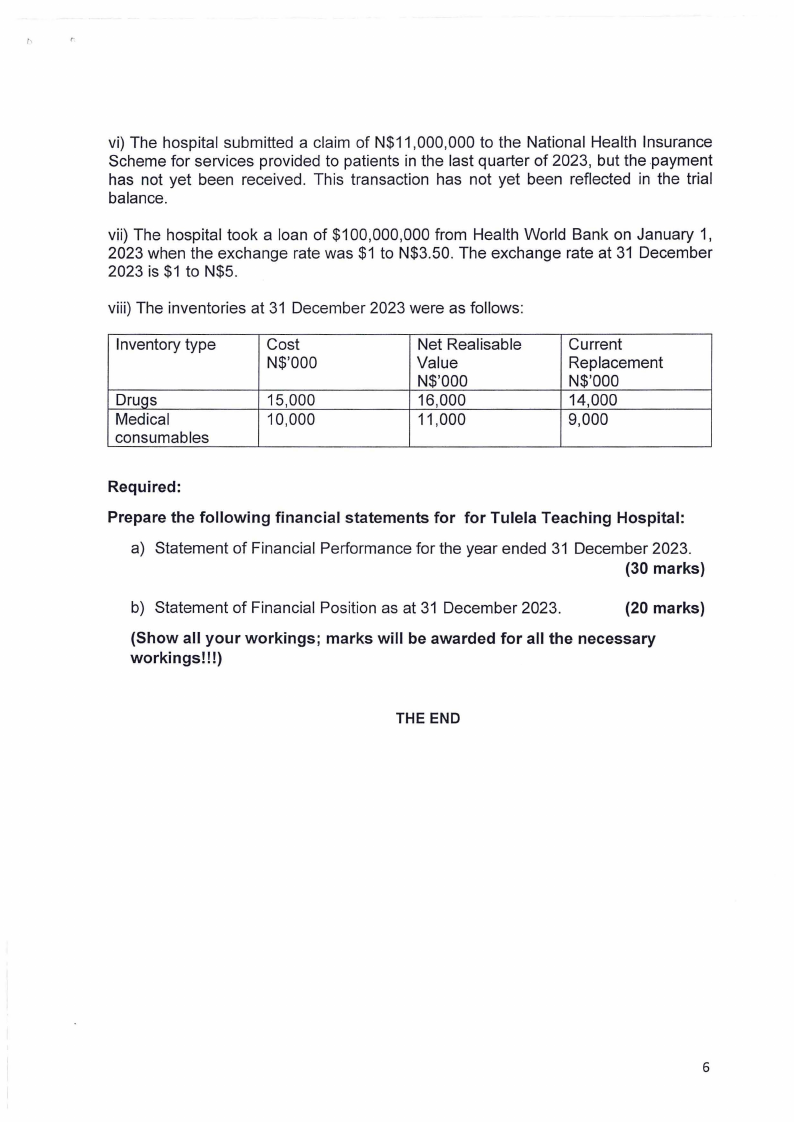

vi) The hospital submitted a claim of N$11,000,000 to the National Health Insurance

Scheme for services provided to patients in the last quarter of 2023, but the payment

has not yet been received . This transaction has not yet been reflected in the trial

balance.

vii) The hospital took a loan of $100,000,000 from Health World Bank on January 1,

2023 when the exchange rate was $1 to N$3.50. The exchange rate at 31 December

2023 is $1 to N$5.

viii) The inventories at 31 December 2023 were as follows:

Inventory type

DruQs

Medical

consumables

Cost

N$'000

15,000

10,000

Net Realisable

Value

N$'000

16,000

11,000

Current

Replacement

N$'000

14,000

9,000

Required:

Prepare the following financial statements for for Tulela Teaching Hospital:

a) Statement of Financial Performance for the year ended 31 December 2023.

(30 marks)

b) Statement of Financial Position as at 31 December 2023.

(20 marks)

(Show all your workings; marks will be awarded for all the necessary

workings!!!)

THE END

6