|

AUT621S-AUDITING 202-2ND OPP- JAN 2025 |

|

|

1 Page 1 |

▲back to top |

nAmlBIA unlVERSITY

OF SCIEn CE Ano TECHn OLOGY

FACULTYOF COMMERCE, HUMAN SCIENCESAND EDUCATION

DEPARTMENTOF ECONOMICS,ACCOUNTINGAND FINANCE

QUALIFICATION:BACHELOROF ACCOUNTING

QUALIFICATIONCODE: 07 BOAC

LEVEL: 6

COURSECODE: AUT 621S

COURSENAME: AUDITING 202

SESSION: JANUARY/FEBRUARY2025

DURATION: 3 HOURS

PAPER:THEORY

MARKS: 100

SECOND OPPORTUNITY EXAMINATION QUESTION PAPER

EXAMINER(S) P.ERKIE

MODERATOR: W. GERTZE

INSTRUCTIONS

1. This test paper is made up of three (3) questions.

2. Answer ALL Question in blue or black ink.

3. Start each question on a new page in your answer sheet.

4. The names of people and businesses used throughout this assessment do not reflect

the reality and may be purely coincidental.

5. Questions relating to this paper may be raised in the initial 30 minutes after the start

of the paper. Thereafter, candidates must use their initiative to deal with any

perceived error or ambiguities & any assumption made by the candidate should be

clearly stated.

THIS QUESTION PAPERCONSISTSOF 4 PAGES(excluding this cover page)

|

|

2 Page 2 |

▲back to top |

QUESTION 1 (40 MARKS)

a) Describe in your own words, what is auditing?

(2)

b) Name the stages of the audit process.

(4)

c) Audit procedures are designed to assess the accuracy and reliability of financial

information, verifying compliance with applicable standards and regulations.

Name two types of audit procedures.

(2)

d) Fill in the missing words.

In Namibia, the Auditor-General is appointed by the 1........ ........ on recommendations

of the 2..................... ..and the approval of the 3.....................

(3)

e) The auditor should consider the statutory and ethical requirements and make sure that all

the requirements have been complied with before accepting the audit client.

Define statutory requirement and give an example.

(2)

f) Describe the elements of an assurance engagement.

(10)

g) Internal controls play a vital role in any organization, serving as a framework for achieving

various goals.

i) What are the objectives of internal controls?

(5)

ii) Name components of internal controls.

. (4)

h) The audit Practitioner performing assurance engagement must always comply with the

ethical principles as contained in the SAICA Code of Professional conduct (CPC).

Name and explain the five (5) fundamental principles of the SAICA (CPC)

(10)

i) The preliminary audit engagement stage is a very important stage of an audit. During the

preliminary audit engagement stage, an audit firm should focus on several critical activities

to lay the groundwork for an effective audit.

Name and explain 4 activities to consider in the preliminary audit engagement stage. (8)

|

|

3 Page 3 |

▲back to top |

QUESTION 2 {30 MARKS)

1. Introduction

Firezone Ltd ('Firezone ') is a wholesaler of numerous products related to domestic snd

industrial heating, fire extinguishers and other fire fighting chemicals and equipment's.

2. New wholesalers

Firezone searched for suitable property to build and open a new wholesaler. In May 2024, a

suitable property was identified near Okahandja Town Council, for which Firezone secured

funding approval from NERD Bank. However, it was later discovered that the property was

zoned for agricultural use only and could not be used for commercial developments.

At Firezone 's board meeting on 2 June 2024, Ms Clere Daniels (CEO) requested that Firezone

allocate an amount of N$ 500 000 to her. She subsequently paid the N$500 000 to key

councillors at the Okahandja Town Council municipality, after which they immediately secured

re-zoning approval of the property for commercial use. Later, it was established that Ms Clere

had a 50% ownership in the property, which she failed to disclose at the board meeting on 2

June 2024.

3. Governance

Firezone is of the opinion that only an audit committee is necessary for it to adhere to King

IV. Its existing audit committee meets once a year. The minutes of its most recent audit

committee meeting are presented in Annexure A.

AnnexureA

Minutes of Firezone 's Audit committee meeting: 05 August 2024 at 09h00

Audit committee attendees

Name

Clere Daniels

Anne Beukes

Zane Mulla

Role on audit

committee

Chair

Member

Member

Other role(s) on

Firezone 's board

CEO, Chair of the board

None

None

Period serving on

Firezone 's audit

committee as at 5

August 2024

5 years

22 years

2 weeks

No Absentees.

Opening

Clere Daniels welcomed all attendees and thanked them for a 100% attendance and their

dedication to the annual audit committee meeting. She also welcomed Zane to her first meeting.

1. Matters from previous meeting

As no minutes were kept at last year's audit committee meeting, none of the board members

could remember whether any previous matters required follow up.

|

|

4 Page 4 |

▲back to top |

2. Resignation of previous and appointment of new audit committee member

Clere informed the rest of the committee that Monicah Jonas CA(NAM) resigned from

Firezone 's audit committee and Firezone 's board with effect 31 March 2024. Monicah did not

have any time to keep her technical knowledge up to date. Since the board did not allow the

audit committee to consult with external specialists due to budgetary constraints, Monicah

decided to resign.

Clere subsequently appointed the Chief Operating Officer's daughter, Zane, as director and

third member of the audit committee, commencing on 22 July 2024. Zane is the only member

in the committee with financial background.

Closure

The meeting closed at 09h30.

Required:

a) Based on Ms Clere's N$500 000 payment to Okahandja Town Council's councillors in 2:

New wholesaler

i) Discuss with reasons, whether there is a reportable inegularity under the Auditing

Profession Act 2005.

(8)

ii) Assuming there is a reportable inegularity, specify the action(s) that the auditors

would have had to take?

(8)

b) With reference to Annexure A, discuss your concerns in terms of the King IV Code of

Corporate Governance.

i) Composition of the Audit Committee

(10)

ii) Composition of the Governing Body

(4)

|

|

5 Page 5 |

▲back to top |

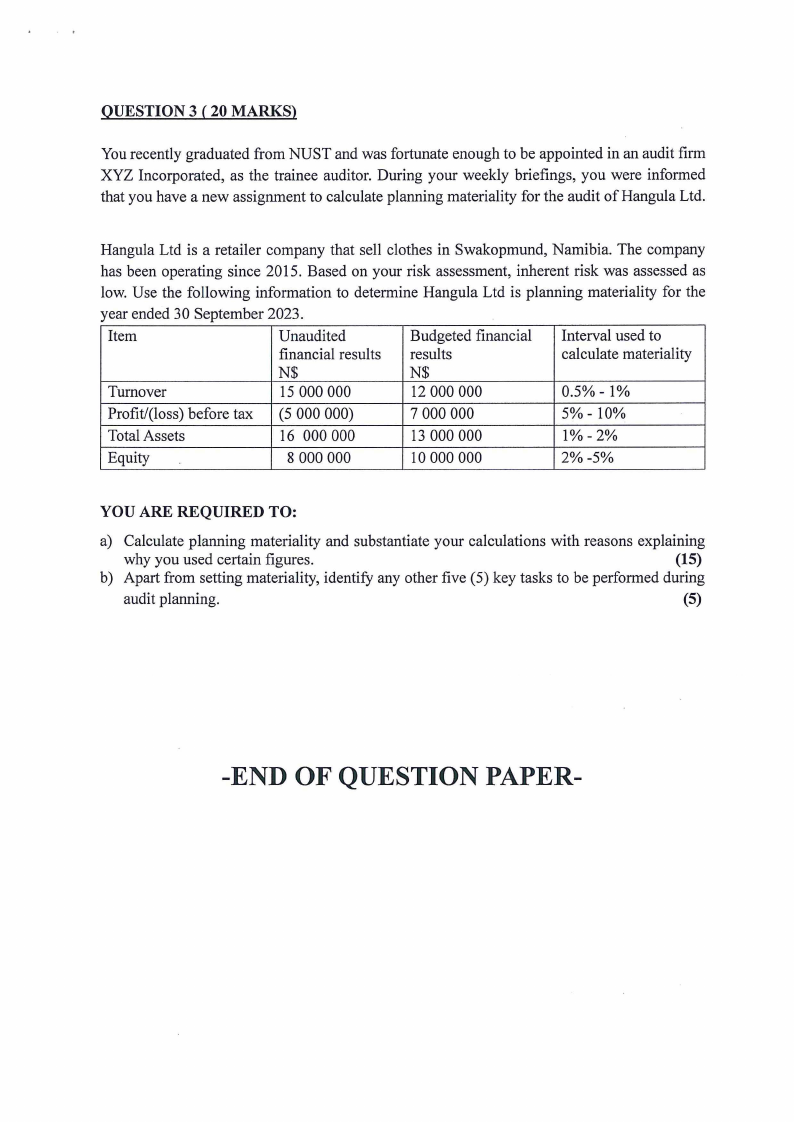

QUESTION 3 ( 20 MARKS)

You recently graduated from NUST and was fortunate enough to be appointed in an audit firm

XYZ Incorporated, as the trainee auditor. During your weekly briefings, you were informed

that you have a new assignment to calculate planning materiality for the audit of Hangula Ltd.

Hangula Ltd is a retailer company that sell clothes in Swakopmund, Namibia. The company

has been operating since 2015. Based on your risk assessment, inherent risk was assessed as

low. Use the following information to determine Hangula Ltd is planning materiality for the

year ended 30 September 2023.

Item

Turnover

Unaudited

financial results

N$

15 000 000

Budgeted financial

results

N$

12 000 000

Interval used to

calculate materiality

0.5%- 1%

Profit/(loss) before tax (5 000 000)

7 000 000

5%- 10%

Total Assets

16 000 000

13 000 000

1%-2%

Equity

8 000 000

10 000 000

2%-5%

YOU ARE REQUIRED TO:

a) Calculate planning materiality and substantiate your calculations with reasons explaining

why you used certain figures.

(15)

b) Apart from setting materiality, identify any other five (5) key tasks to be performed during

audit planning.

(5)

-END OF QUESTION PAPER-