|

ECM - ECONOMETRICS - 2ND OPP - JAN 2020 |

|

|

1 Page 1 |

▲back to top |

NAMIBIA UNIVERSITY

OF SCIENCE AND TECHNOLOGY

FACULTY OF MANAGEMENT SCIENCES

DEPARTMENT OF ACCOUNTING, ECONOMICS AND FINANCE

QUALIFICATION: BACHELOR OF ECONOMICS

QUALIFICATION CODE: 12BECO

LEVEL: 7

COURSE CODE: ECM712S

COURSE NAME: ECONOMETRICS

SESSION: JAN 2020

DURATION: 3 HOURS

PAPER: THEORY

MARKS: 100

SUPPLEMENTARY/ SECOND OPPORTUNITY EXAMINATION

EXAMINER(S)

MODERATOR:

MR EDEN TATE SHIPANGA

MR PINEHAS NANGULA

DR R. KAMATI

INSTRUCTIONS

1. Answer ALL the questions.

2. Write clearly and neatly.

3. Number the answers clearly.

PERMISSIBLE MATERIALS

1. PEN,

PENCIL

3. CALCULATOR

THIS QUESTION PAPER CONSISTS OF 2 PAGES (Including this front page)

|

|

2 Page 2 |

▲back to top |

QUESTION 1 [25 marks]

1. Why do we study econometrics as a separate discipline?

(9)

2. Explain eight steps on how econometricians proceed in their analysis of an economic problem? (10)

3. Mention three ambiguities that must be address when constructing an econometrics model

(6)

Question 2 [25 marks]

¥ = EY |X) +4 Describe the various components of the function

(2)

Discuss the two types of error that arise in hypothetical conclusions

(6)

State the two distinct features of the interceptless model.

(4)

One of the “consequences of error of measurement in the regressand is increased variance of the estimators”.

Formulate a scenario and provide proof of this statement.

(4)

5. Consider a two-variable model where consumption as a regressand and income as a regressor.

(a) Name the parameter that is used to measure the spread of the values from their expected values?

(2)

(b) Suppose, a researcher is interested in measuring the strength of the relationship between consumption and

income, name the parameter one can use to quantify this relationship?

(2)

6. Assuming a three-variable model Y; = a, + a@2X2+a3X3, where «a, andaz3are partial regression

coefficients. You have been asked in a job interview to briefly describe the meaning of the two parameters in

this context.

(5)

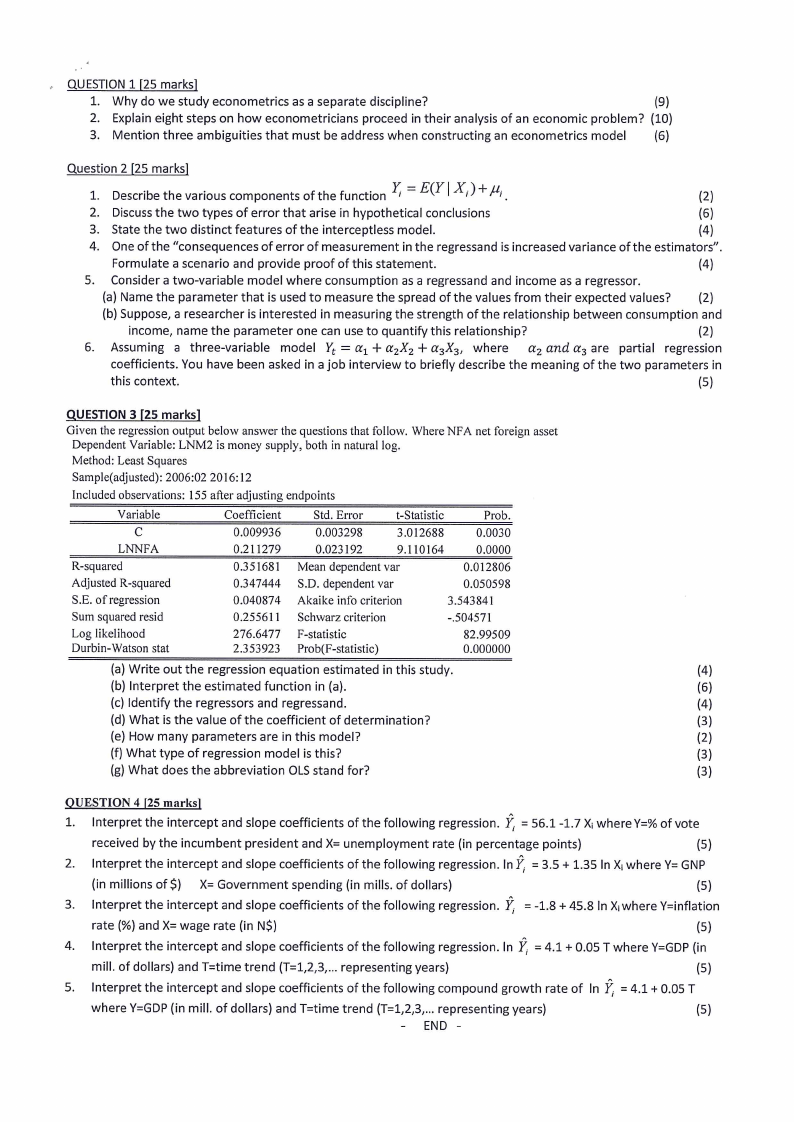

QUESTION 3 [25 marks]

Given the regression output below answer the questions that follow. Where NFA

Dependent Variable: LNM2 is money supply, both in natural log.

Method: Least Squares

Sample(adjusted): 2006:02 2016:12

Included observations: 155 after adjusting endpoints

net foreign asset

Variable

Cc

LNNFA

R-squared

Adjusted R-squared

S.E. of regression

Sum squared resid

Log likelihood

Durbin- Watson stat

Coefficient

Std. Error

t-Statistic

Prob.

0.009936

0.211279

0.003298

0.023192

3.012688

9.110164

0.0030

0.0000

0.351681 Mean dependent var

0.012806

0.347444 §.D. dependent var

0.050598

0.040874 Akaike info criterion

3.543841

0.255611 Schwarz criterion

-.504571

276.6477 _ F-statistic

82.99509

2.353923 Prob(F-statistic)

0.000000

(a) Write out the regression equation estimated in this study.

(4)

(b) Interpret the estimated function in (a).

(6)

(c) Identify the regressors and regressand.

(4)

(d) What is the value of the coefficient of determination?

(3)

(e) How many parameters are in this model?

(2)

(f) What type of regression model is this?

(3)

(g) What does the abbreviation OLS stand for?

(3)

QUESTION 4 [25 marks]

1. Interpret the intercept and slope coefficients of the following regression. Y, = 56.1 -1.7 Xi where Y=% of vote

received by the incumbent president and X= unemployment rate (in percentage points)

(5)

Interpret the intercept and slope coefficients of the following regression. In Y, = 3.54 1.35 In Xi where Y= GNP

(in millions of S) X= Government spending (in mills. of dollars)

(5)

Interpret the intercept and slope coefficients of the following regression. y, = -1.8 + 45.8 In Xiwhere Y=inflation

rate (%) and X= wage rate (in NS)

(5)

Interpret the intercept and slope coefficients of the following regression. In Y, = 4,1 + 0.05 T where Y=GDP (in

mill. of dollars) and T=time trend (T=1,2,3,... representing years)

(5)

Interpret the intercept and slope coefficients of the following compound growth rate of In ¥ =4,1+0.05 T

where Y=GDP (in mill. of dollars) and T=time trend (T=1,2,3,... representing years)

(5)

- END -