|

GTA711S- TAXATION 310-1ST OPP -JUNE 2025 |

|

|

1 Page 1 |

▲back to top |

n Am I 8 I A Un IVERS ITY

OF SCIEnCE Ano TECHnOLOGY

FACULTY OF COMMERCE, HUMAN SCIENCES& EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING AND FINANCE

QUALIFICATION: BACHELOROF ACCOUNTING

QUALIFICATION CODE: 07BAOC

COURSE CODE: GTA711S

LEVEL: 7

COURSE NAME: TAXATION 310

SESSION: JUNE 2025

PAPER: THEORY& APPLICATION

DURATION: 3 HOURS

MARKS: 100

FIRST OPPORTUNITY EXAMINATION QUESTION PAPER

EXAMINER(S) Mrs. Y van Wyk, Mr. J Erastus & Mrs. G Meintjies

MODERATOR: Ms. F Haimbala

INSTRUCTIONS

1. This question paper is made up of THREE(3) questions.

2. Answer ALL the questions and in blue or black ink.

3. Start each question on a new page in your answer booklet.

4. Draw a line through all unused spaces in your answer booklet.

5. The names of people and businesses used throughout this examination paper do not

reflect reality and may be purely coincidental.

6. Questions relating to this examination may be raised in the initial 30 minutes after the

start of the paper. Thereafter, candidates must use their initiative to deal with any

perceived error or ambiguities & any assumption made by the candidate should be

clearly stated.

THIS QUESTION PAPER CONSISTS OF 7 PAGES (excluding this front page)

|

|

2 Page 2 |

▲back to top |

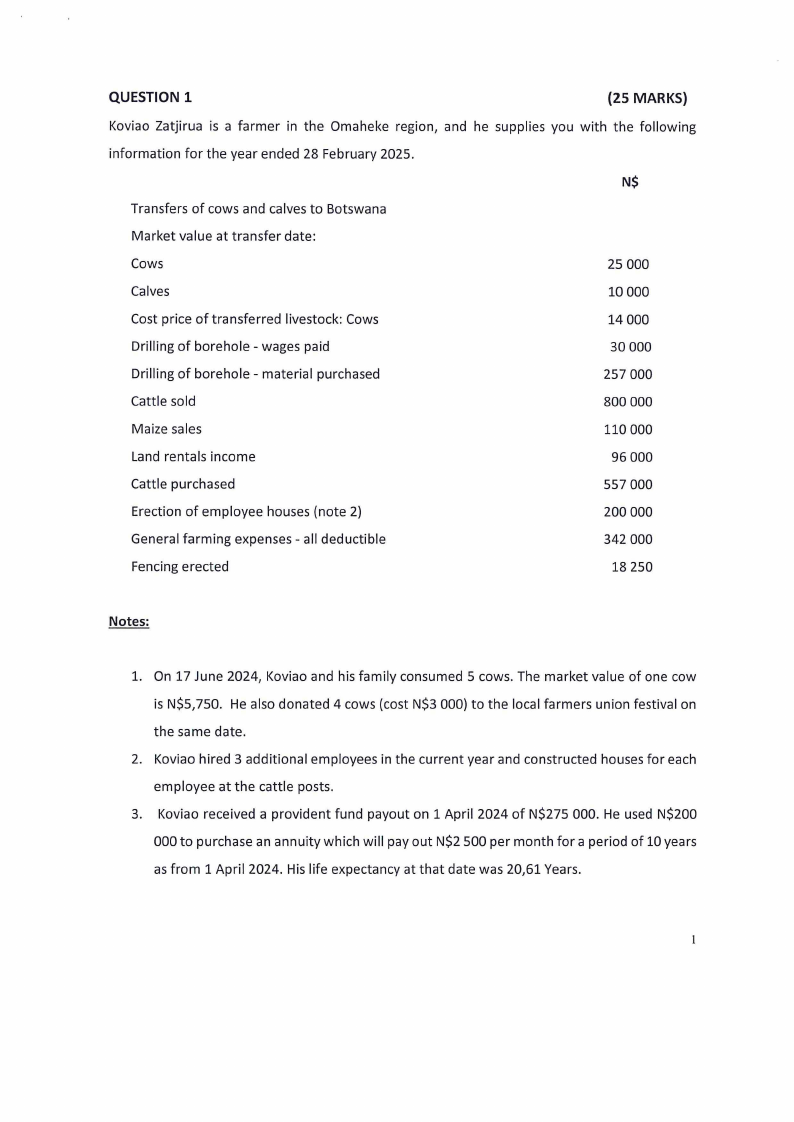

QUESTION 1

(25 MARKS)

Koviao Zatjirua is a farmer in the Omaheke region, and he supplies you with the following

information for the year ended 28 February 2025.

N$

Transfers of cows and calves to Botswana

Market value at transfer date:

Cows

25 000

Calves

10 000

Cost price of transferred livestock: Cows

14 000

Drilling of borehole - wages paid

30000

Drilling of borehole - material purchased

257 000

Cattle sold

800 000

Maize sales

110 000

Land rentals income

96 000

Cattle purchased

557 000

Erection of employee houses (note 2)

200 000

General farming expenses - all deductible

342 000

Fencing erected

18 250

Notes:

1. On 17 June 2024, Koviao and his family consumed 5 cows. The market value of one cow

is N$5,750. He also donated 4 cows (cost N$3 000) to the local farmers union festival on

the same date.

2. Koviao hired 3 additional employees in the current year and constructed houses for each

employee at the cattle posts.

3. Koviao received a provident fund payout on 1 April 2024 of N$275 000. He used N$200

000 to purchase an annuity which will pay out N$2 500 per month for a period of 10 years

as from 1 April 2024. His life expectancy at that date was 20,61 Years.

|

|

3 Page 3 |

▲back to top |

He transferred the remaining N$75 000 of the provident fund payout into another

approved Provident fund.

REQUIRED:

Calculate the taxable income of Koviao Zatjirua for the year of assessment ending 28 February

2025. Provide reasons for the exclusion of any amount from your calculation. Show all workings.

Round off all amounts to the nearest Namibian dollars (N$).

(25)

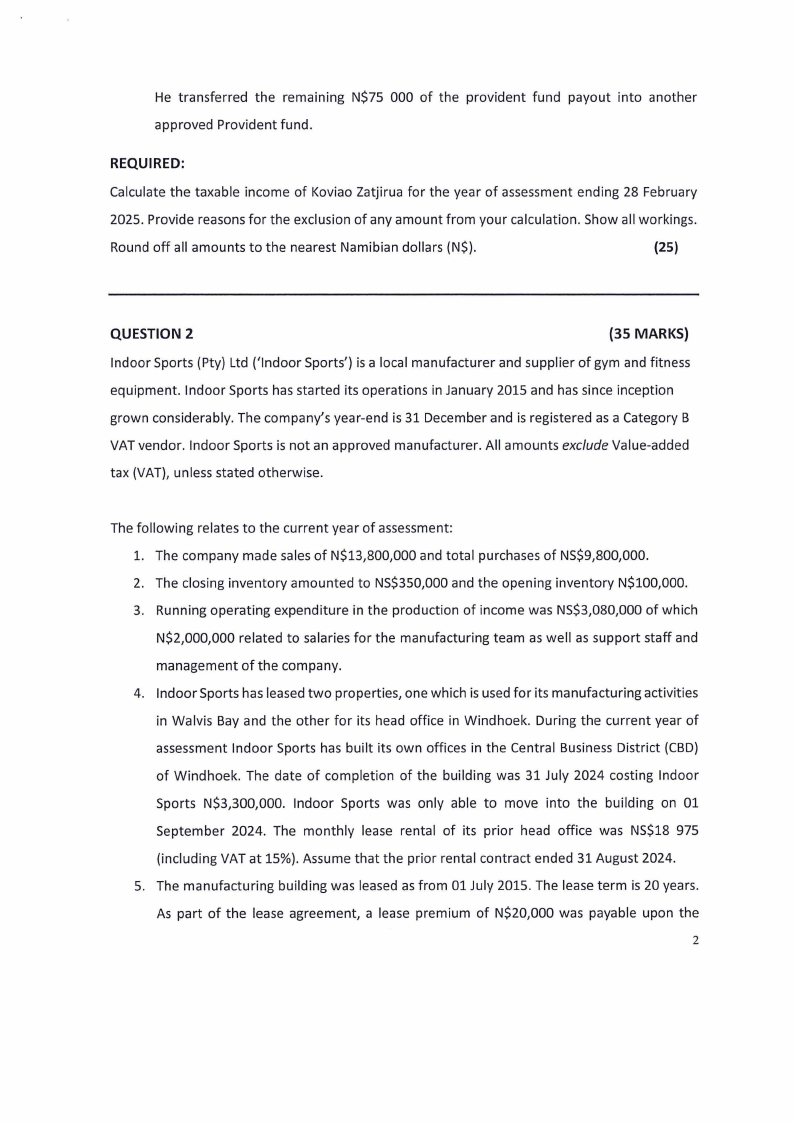

QUESTION 2

{35 MARKS)

Indoor Sports (Pty) Ltd ('Indoor Sports') is a local manufacturer and supplier of gym and fitness

equipment. Indoor Sports has started its operations in January 2015 and has since inception

grown considerably. The company's year-end is 31 December and is registered as a Category B

VAT vendor. Indoor Sports is not an approved manufacturer. All amounts exclude Value-added

tax (VAT), unless stated otherwise.

The following relates to the current year of assessment:

l. The company made sales of N$13,800,000 and total purchases of NS$9,800,000.

2. The closing inventory amounted to NS$350,000 and the opening inventory N$100,000.

3. Running operating expenditure in the production of income was NS$3,080,000 of which

N$2,000,000 related to salaries for the manufacturing team as well as support staff and

management of the company.

4. Indoor Sports has leased two properties, one which is used for its manufacturing activities

in Walvis Bay and the other for its head office in Windhoek. During the current year of

assessment Indoor Sports has built its own offices in the Central Business District (CBD)

of Windhoek. The date of completion of the building was 31 July 2024 costing Indoor

Sports N$3,300,000. Indoor Sports was only able to move into the building on 01

September 2024. The monthly lease rental of its prior head office was NS$18 975

(including VAT at 15%}. Assume that the prior rental contract ended 31 August 2024.

5. The manufacturing building was leased as from 01 July 2015. The lease term is 20 years.

As part of the lease agreement, a lease premium of N$20,000 was payable upon the

2

|

|

4 Page 4 |

▲back to top |

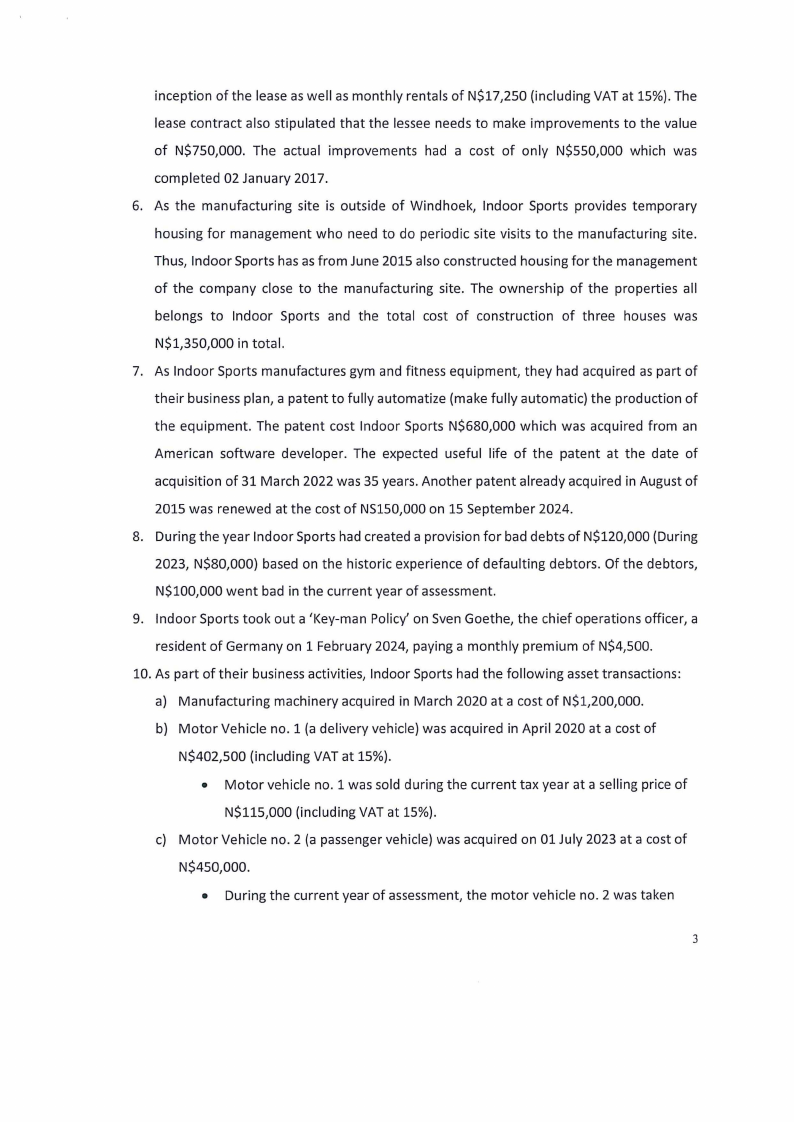

inception of the lease as well as monthly rentals of N$17,250 (including VAT at 15%). The

lease contract also stipulated that the lessee needs to make improvements to the value

of N$750,000. The actual improvements had a cost of only N$550,000 which was

completed 02 January 2017.

6. As the manufacturing site is outside of Windhoek, Indoor Sports provides temporary

housing for management who need to do periodic site visits to the manufacturing site.

Thus, Indoor Sports has as from June 2015 also constructed housing for the management

of the company close to the manufacturing site. The ownership of the properties all

belongs to Indoor Sports and the total cost of construction of three houses was

N$1,350,000 in total.

7. As Indoor Sports manufactures gym and fitness equipment, they had acquired as part of

their business plan, a patent to fully automatize (make fully automatic) the production of

the equipment. The patent cost Indoor Sports N$680,000 which was acquired from an

American software developer. The expected useful life of the patent at the date of

acquisition of 31 March 2022 was 35 years. Another patent already acquired in August of

2015 was renewed at the cost of NS150,000 on 15 September 2024.

8. During the year Indoor Sports had created a provision for bad debts of N$120,000 (During

2023, N$80,000) based on the historic experience of defaulting debtors. Of the debtors,

N$100,000 went bad in the current year of assessment.

9. Indoor Sports took out a 'Key-man Policy' on Sven Goethe, the chief operations officer, a

resident of Germany on 1 February 2024, paying a monthly premium of N$4,500.

10. As part of their business activities, Indoor Sports had the following asset transactions:

a) Manufacturing machinery acquired in March 2020 at a cost of N$1,200,000.

b) Motor Vehicle no. 1 (a delivery vehicle) was acquired in April 2020 at a cost of

N$402,500 (including VAT at 15%).

• Motor vehicle no. 1 was sold during the current tax year at a selling price of

N$115,000 (including VAT at 15%).

c) Motor Vehicle no. 2 (a passenger vehicle) was acquired on 01 July 2023 at a cost of

N$450,000.

• During the current year of assessment, the motor vehicle no. 2 was taken

3

|

|

5 Page 5 |

▲back to top |

out of use to donate it to a former employee of the company as a gift for his

long service.

• The market value at the date of donation was N$200,000.

d) Motor Vehicle no. 3 (a passenger vehicle) was acquired in April 2024 at a cost of

N$550,000 (including VAT at 15%).

e) Furniture and Fittings acquired in August of 2023 at a cost of N$69,000 (including

VAT at 15%).

REQUIRED:

Calculate the normal tax liability of Indoor Sports (Pty) Ltd for the year of assessment ended 31

December 2024. Provide reasons for nil effects. Show all workings. Round off all amounts to the

nearest Namibian dollars (N$).

(35)

QUESTION 3

(40 MARKS)

Cookie Lyon, 56-year-old Namibian citizen was an employee of "Empire State Records"

since 1 March 2004. During the year she decided she has had enough and resigned on 31

January 2025.

Her receipts and accruals for the 2025 year of assessment include:

1. A monthly salary of N$60 000.

2. She received a motor vehicle allowance of N$146 000 for the year whilst

employed. Cost Price of the vehicle when bought in the 2023 tax year was N$210

000. Fuel costs for the year was N$24100, maintenance and insurance were N$19

000. The total kilometers travelled for the year was 41,000 of which 27,000 was

for business purposes.

3. She also received a housing allowance of N$11 000 per month. An approved

housing scheme with the NAMRA is in place.

4. A cellular phone allowance of N$400 per month. Her business calls amounted to

N$4 000 for the year. Cookie kept all the relevant records.

4

|

|

6 Page 6 |

▲back to top |

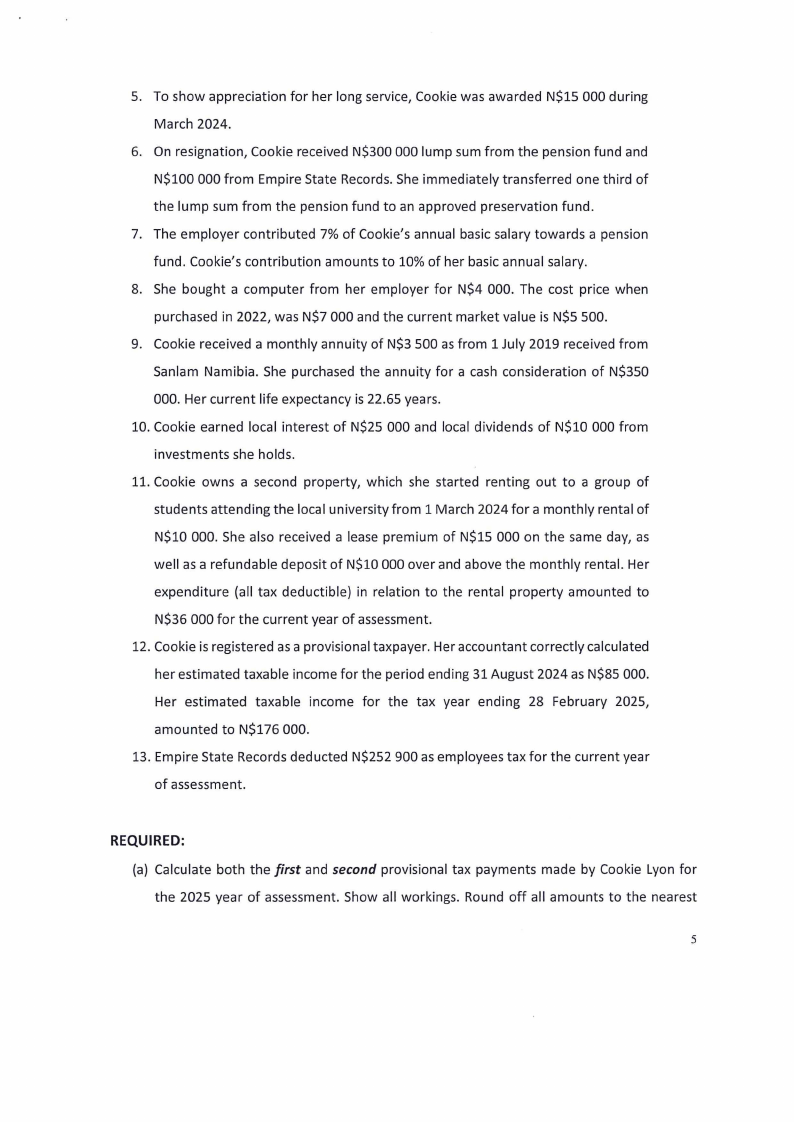

5. To show appreciation for her long service, Cookie was awarded N$15 000 during

March 2024.

6. On resignation, Cookie received N$300 000 lump sum from the pension fund and

N$100 000 from Empire State Records. She immediately transferred one third of

the lump sum from the pension fund to an approved preservation fund.

7. The employer contributed 7% of Cookie's annual basic salary towards a pension

fund. Cookie's contribution amounts to 10% of her basic annual salary.

8. She bought a computer from her employer for N$4 000. The cost price when

purchased in 2022, was N$7 000 and the current market value is N$5 500.

9. Cookie received a monthly annuity of N$3 500 as from 1 July 2019 received from

Sanlam Namibia. She purchased the annuity for a cash consideration of N$350

000. Her current life expectancy is 22.65 years.

10. Cookie earned local interest of N$25 000 and local dividends of N$10 000 from

investments she holds.

11. Cookie owns a second property, which she started renting out to a group of

students attending the local university from 1 March 2024 for a monthly rental of

N$10 000. She also received a lease premium of N$15 000 on the same day, as

well as a refundable deposit of N$10 000 over and above the monthly rental. Her

expenditure (all tax deductible) in relation to the rental property amounted to

N$36 000 for the current year of assessment.

12. Cookie is registered as a provisional taxpayer. Her accountant correctly calculated

her estimated taxable income for the period ending 31 August 2024 as N$85 000.

Her estimated taxable income for the tax year ending 28 February 2025,

amounted to N$176 000.

13. Empire State Records deducted N$252 900 as employees tax for the current year

of assessment.

REQUIRED:

(a) Calculate both the first and second provisional tax payments made by Cookie Lyon for

the 2025 year of assessment. Show all workings. Round off all amounts to the nearest

5

|

|

7 Page 7 |

▲back to top |

Namibian dollars (N$).

(10)

(b) Calculate the normal tax liability of Cookie Lyon for the 2025 year of assessment. Show

all workings. Round off all amounts to the nearest Namibian dollars (N$).

(30)

6

|

|

8 Page 8 |

▲back to top |

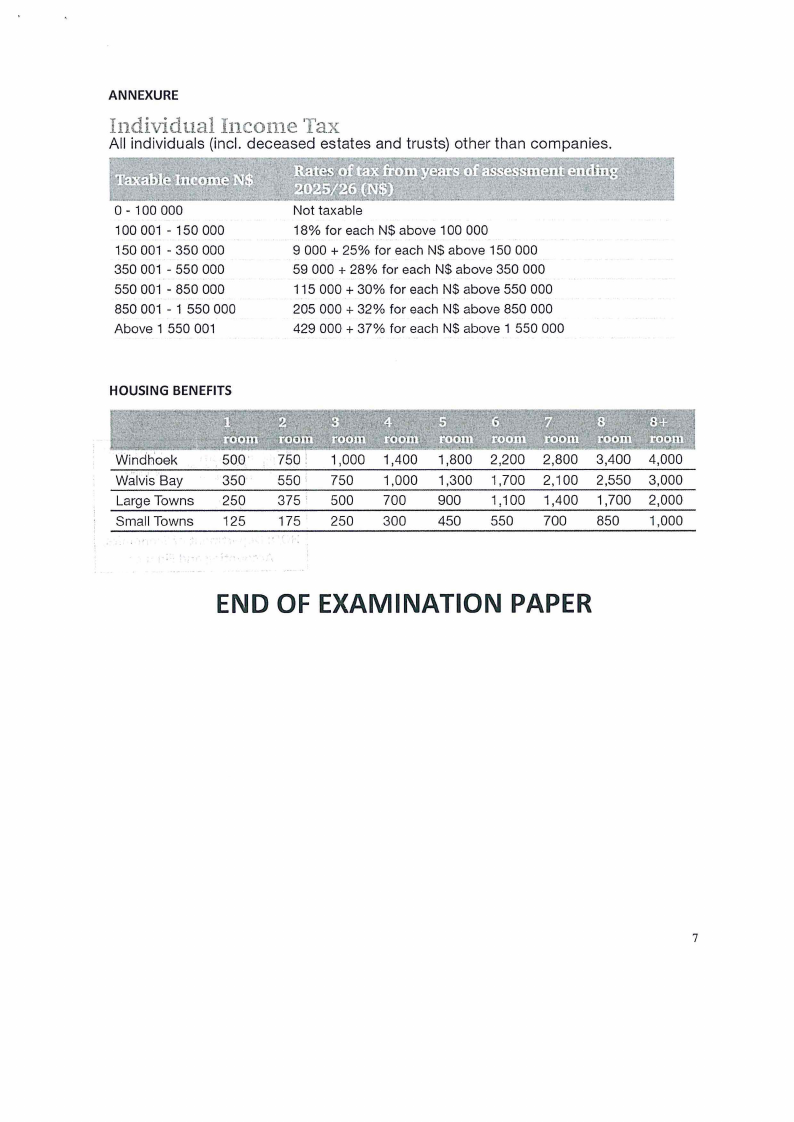

ANNEXURE

Individual Inco1ne Tax

All individuals (incl. deceased estates and trusts) other than companies.

0 - 100 000

100 001 - 150 000

150 001 - 350 000

350 001 - 550 000

550 001 - 850 000

850 001 - 1 550 000

Above 1 550 001

HOUSING BENEFITS

Not taxable

18% for each N$ above 100 000

9 000 + 25% for each N$ above 150 000

59 000 + 28% for each N$ above 350 000

115 000 + 30% for each N$ above 550 000

205 000 + 32% for each N$ above 850 000

429 000 + 37% for each N$ above 1 550 000

Windh'oek

500

Walvis Bay

350

Large Towns 259

Small Towns 125

750: 1,000 1,400 1,800 2,200 2,800 3,400 4,000

550

750

1,000 1,300 1,700 2,100 2,550 3,000

375' 500

700

900

1,100 1,400 1,700 2,000

175 250 300

450

550 700

850

1,000

END OF EXAMINATION PAPER

7