|

FAC501Y-FINANCIAL ACCOUNTING 100-2ND OPP-DEC 2025 |

|

|

1 Page 1 |

▲back to top |

nAmlBIA unlVERSITY

OF SCI En CE An □ TECH no LOGY

FACULTY OF COMMERCE, HUMAN SCIENCES AND EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING AND FINANCE

QUALIFICATION : BACHELOR OF ACCOUNTING (CHARTERED ACCOUNTANCY)

QUALIFICATION CODE: 07BACC

COURSE CODE: FACS0lY

LEVEL: 5

COURSE

NAME:

ACCOUNTING 100

FINANCIAL

DATE: DECEMBER 2025

PAPER: THEORY AND PRACTICAL

TOTAL DURATION: 180 MINUTES

MARKS: 100

SECOND OPPORTUNITY EXAMINATION QUESTION PAPER

EXAMINERS

MS Z STELLMACHER

MODERATOR:

MS M CLOETE

INSTRUCTIONS:

1. This paper consists of EIGHT (8) pages (Including this cover page). If your paper does not contain all the pages, please put

up your hand so that a replacement paper can be handed to you.

2. This paper consists of FOUR (4) questions. Answer ALL questions.

3. Answer all the questions in blue or black ink only.

4. Each question should be answered on a separate page.

5. Questions relating to the paper may be raised in the initial 30 minutes after the start of the paper. Thereafter,

candidates must use their initiative to deal with any perceived error or ambiguities & any assumption made by the

candidate should be clearly statedPermissible materials include stationery and a non-programmable calculator only

6. The neatness, disclosure and presentation of your answers will be considered when marking your paper.

7. The scenarios presented are fictitious and any similarities, real or imagined, to real events, people, places, organisations

are purely coincidental and should be interpreted as such

8. Show ALL calculations clearly.

1

|

|

2 Page 2 |

▲back to top |

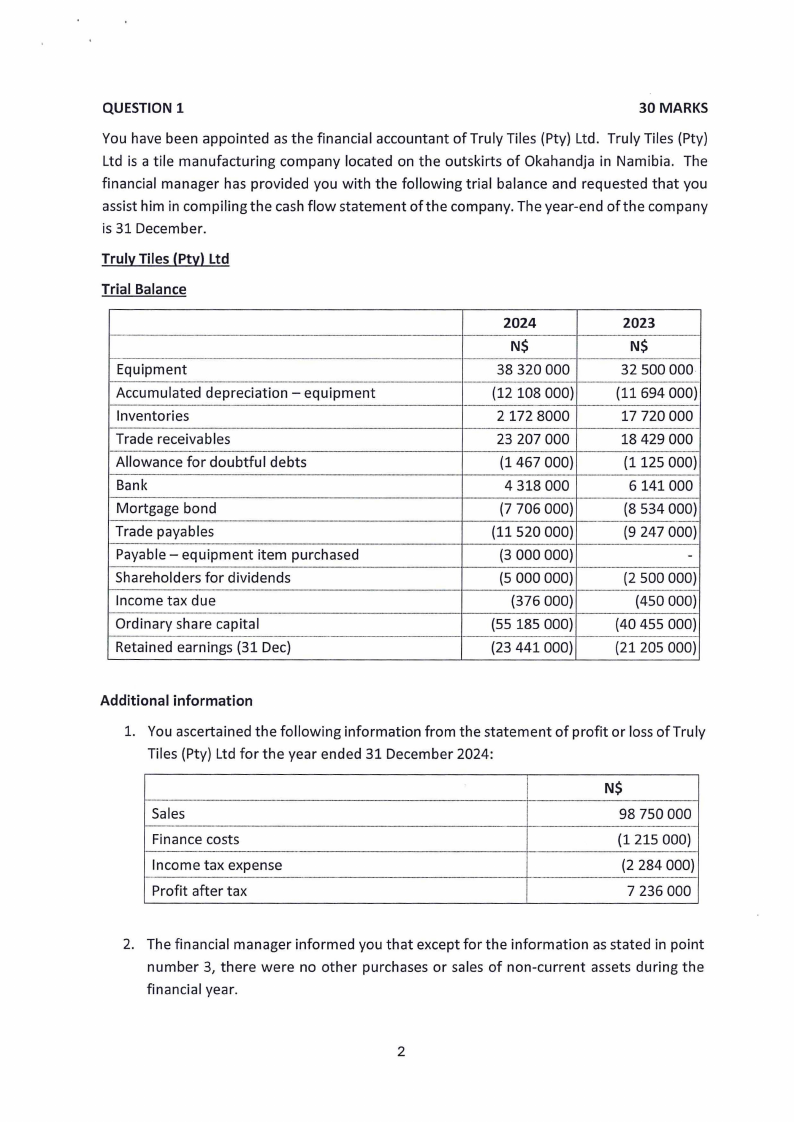

QUESTION 1

30 MARKS

You have been appointed as the financial accountant of Truly Tiles (Pty) Ltd. Truly Tiles (Pty)

Ltd is a tile manufacturing company located on the outskirts of Okahandja in Namibia. The

financial manager has provided you with the following trial balance and requested that you

assist him in compiling the cash flow statement of the company. The year-end of the company

is 31 December.

Truly Tiles (Pty) Ltd

Trial Balance

Equipment

Accumulated depreciation - equipment

Inventories

Trade receivables

Allowance for doubtful debts

Bank

Mortgage bond

Trade payables

Payable - equipment item purchased

Shareholders for dividends

Income tax due

Ordinary share capital

Retained earnings (31 Dec)

2024

N$

38 320 000

(12 108 000)

2172 8000

23 207 000

(1467 000)

4 318 000

(7 706 000)

(11520 000)

(3 000 000)

(5 000 000)

(376 000)

(55 185 000)

(23 441000)

2023

N$

32 500 000

{11694000)

17 720 000

18 429 000

{1125 000)

6141000

(8 534 000)

(9 247 000)

-

(2 500 000)

(450 000)

(40 455 000)

(21205 000)

Additional information

1. You ascertained the following information from the statement of profit or loss of Truly

Tiles (Pty) Ltd for the year ended 31 December 2024:

Sales

Finance costs

Income tax expense

Profit after tax

N$

98 750 000

(1 215 000)

(2 284 000)

7 236 000

2. The financial manager informed you that except for the information as stated in point

number 3, there were no other purchases or sales of non-current assets during the

financial year.

2

|

|

3 Page 3 |

▲back to top |

3. Equipment

3.1 On 31 August 2024, an equipment item with a cost price of N$ 2 880 000 and

accumulated depreciation of N$ 2 808 000, as at that date, was withdrawn and

scrapped.

3.2 On 25 October 2024, an order to the amount of N$ 4 200 000 was issued to replace

the above-mentioned equipment item. The replacing equipment item was

received on 29 November 2024 and put into service by Truly Tiles (Pty) Ltd on 1

December 2024. On 1 December 2024 an amount of N$ 1 200 000 was paid to

the supplier. The outstanding amount of N$ 3 000 000 is payable on 31 January

2025.

4. The finance cost in the Statement of Profit or Loss refers to the interest expense

incurred on the mortgage bond. This interest is not included in mortgage bonds

balances as per the Trial Balance above.

QUESTION 1

TO BE ANSWERED ON A SEPARATE PAGE '

YOU ARE REQUIRED TO:

MARKS

(a)

Calculate the following numbers as they will appear in the Cash

Flow Statement of Truly Tiles (Pty) Ltd for the year ended 31

December 2024:

i)

Cash receipts from customers

(3)

ii)

Income tax paid

(3)

iii) Dividends paid

(4)

iv) Purchase of equipment to replace

(2)

v)

Purchase of equipment (excluding replacement

(3)

equipment)

vi) Mortgage bond repayment

(3)

Note:

Ignore VAT.

Disclose only the note "Cash generated from operations" to the

(b)

Cash Flow Statement of Truly Tiles (Pty) Ltd for the reporting

(12)

period ended 31 December 2024.

TOTAL MARKS: QUESTION 1

(30)

3

|

|

4 Page 4 |

▲back to top |

QUESTION 2

20 MARKS

Battery Box (Pty) Ltd is a private company which sells a variety of vehicle batteries. The

company is a registered VAT vendor, and its year-end is 30 June. Battery Box (Pty) Ltd uses

the periodic inventory system.

On 4 April 2025 the company received an order from Vinnie's Vehicles. The order was as

follows:

• 25 Bakkie Batteries@ N$ 2 737 each (VAT inclusive)

• 20 Sedan Batteries@ 2 070 each (VAT inclusive)

The batteries were delivered to Vinnie's Vehicles on 11 April 2025. The outstanding amount

is payable on or before 30 April 2024. Vinnie's Vehicles has an excellent payment record. All

customers qualify for a 2 % discount if the payment is done within 7 days of delivery. Payment

is only made on 24 April 2025.

QUESTION 2

TO BE ANSWERED ON A SEPARATE PAGE

YOU ARE REQUIRED TO:

MARKS

(a)

Write a memorandum to the management of Battery Box (Pty)

{13)

Ltd in which you explain whether revenue should be recognized

for the year ended 30 June 2025, in terms of IFRS 15: Revenue

from contracts with customers. You do not have to discuss the

requirements for a contract.

Prepare the journal entries in the records of Battery Box (Pty)

(b)

Ltd for the above transaction assuming payment is made on 24

(7)

April 2025, which is more than 7 days later.

TOTAL MARKS: QUESTION 2

(20)

QUESTION 3

35 MARKS

Jones Ltd is a listed company and VAT vendor involved in various sectors of the Namibian

economy. The company has a 30 June year end . This question has TWO interrelated parts:

PART A

20 MARKS

Jones Ltd signed a contract to purchase a warehouse, which is situated at nr 70 Nickel Street,

Prosperita, Windhoek, on 11 February 2024. The cost of the property amounted to N$ 4 890

4

|

|

5 Page 5 |

▲back to top |

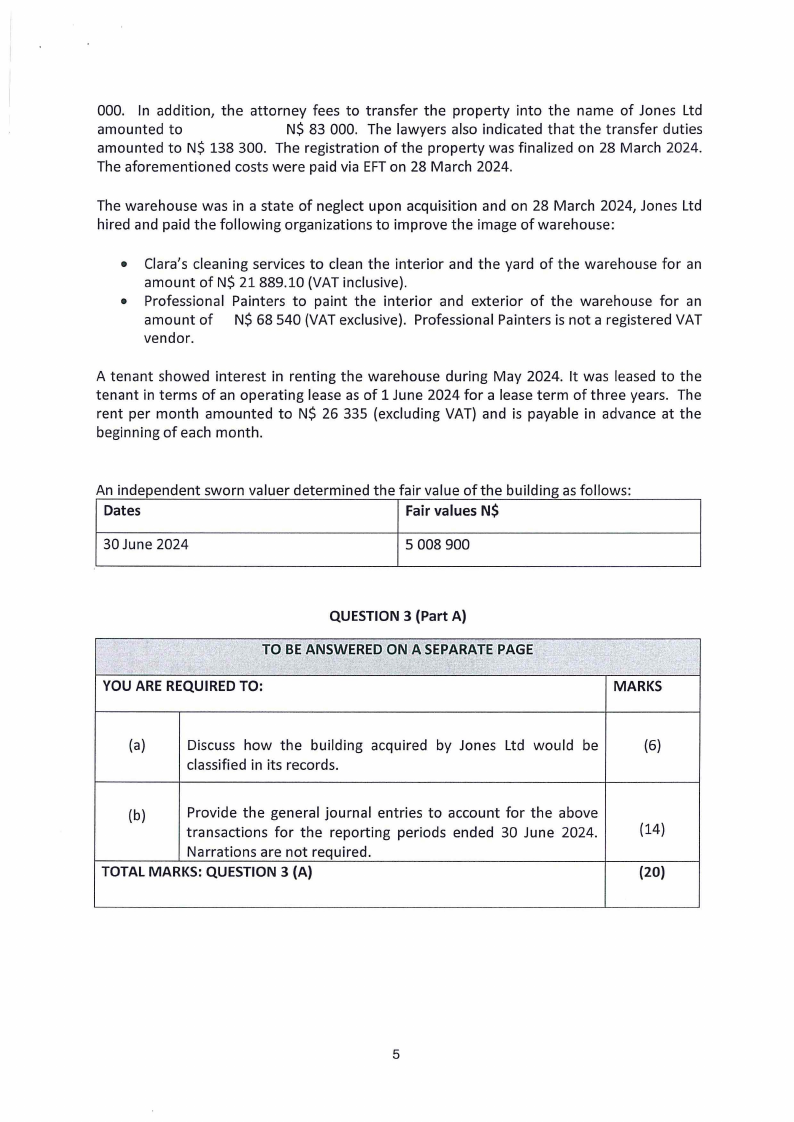

000. In addition, the attorney fees to transfer the property into the name of Jones Ltd

amounted to

N$ 83 000. The lawyers also indicated that the transfer duties

amounted to N$ 138 300. The registration of the property was finalized on 28 March 2024.

The aforementioned costs were paid via EFT on 28 March 2024.

The warehouse was in a state of neglect upon acquisition and on 28 March 2024, Jones Ltd

hired and paid the following organizations to improve the image of warehouse:

• Clara's cleaning services to clean the interior and the yard of the warehouse for an

amount of N$ 21889.10 (VAT inclusive).

• Professional Painters to paint the interior and exterior of the warehouse for an

amount of N$ 68 540 (VAT exclusive). Professional Painters is not a registered VAT

vendor.

A tenant showed interest in renting the warehouse during May 2024. It was leased to the

tenant in terms of an operating lease as of 1 June 2024 for a lease term of three years. The

rent per month amounted to N$ 26 335 (excluding VAT) and is payable in advance at the

beginning of each month.

An independent sworn valuer determined the fair value of the building as follows:

Dates

Fair values N$

30 June 2024

5 008 900

r"

,,. "

QUESTION 3 (Part A)

TO BE ANSWERED ON A SEPARATE PAGE

YOU ARE REQUIRED TO:

'

..

.,

MARKS

(a)

Discuss how the building acquired by Jones Ltd would be

(6)

classified in its records.

(b)

Provide the general journal entries to account for the above

transactions for the reporting periods ended 30 June 2024.

(14)

Narrations are not required.

TOTAL MARKS: QUESTION 3 (A)

(20)

5

|

|

6 Page 6 |

▲back to top |

PARTB

15 MARKS

Investment in Jessy Ltd

• On 1 August 2023 Jones purchased a 75% interest in the 500 000 ordinary shares in

issue of Jessy Ltd for N$ 3 000 000. The shares were paid for via EFT on the same day.

• Jessy Ltd had a limited number of staff members on 1 August 2023 and Jones Ltd

assisted the company by providing administrative and management services for an

amount of N$ 138 000 (VAT inclusive) until 30 June 2024.

• Jessy Ltd declared a dividend of 10 cents per ordinary share on 15 June 2024. This

dividend was paid on 18 August 2024.

Investment in Jona (Pty) Ltd

• Jones Ltd purchased 80,000 unlisted shares in Jona (Pty) Ltd at a cost of N$ 2.50 per

share via bank transfer on 1 April 2024. At acquisition date, the issued share capital

of Jona (Pty) Ltd was 800 000 ordinary shares.

• During May 2024, the auditors informed the Board of Directors of Jona (Pty) Ltd that

the accountant defrauded the company with several million dollars. By 30 June 2024,

the value of each share of Jona (Pty) Ltd fell to N$ 2.10 per share.

It is the accounting policy of Jones Ltd to measure investments in listed shares at fair value

through profit and loss, while investments in unlisted shares are measured using the cost

model.

QUESTION 3 (Part B)

•'

TO BE ANSWERED ON A SEPARATE PAGE

YOU ARE REQUIRED TO:

~

MARKS

(a)

Prepare all the general journal entries relating to the

(10)

investments in Jessy Ltd and Jona (Pty) Ltd for the reporting

period ended 30 June 2024. Narrations are not required.

(b)

Disclose the following notes to the financial statements of

Jones Ltd for the reporting period ending 30 June 2024,

include applicable information from PART A:

i) Income from subsidiary

(2)

ii) Investment in subsidiary

(2)

iii) Other financial investments

(1)

TOTAL MARKS: QUESTION 3 (B)

(15)

6

|

|

7 Page 7 |

▲back to top |

QUESTION 4

15 MARKS

The bank statement of Sunny Stores, a registered VAT vendor, reflected an unfavorable

bank balance of N$ 4 970 on 30 April 2024. Sunny Stores is a general dealer owned by

Sunny. Recently Sunny also started to perform minor repairs and maintenance for

businesses in the area. The preliminary trial balance extracted on 30 April indicated no

differences but upon further investigation the accountant gained the following information

pertaining to April 2024:

i)

A deposit of N$ 5 180 was made on 30 April 2024 and did not reflect in the bank

statement.

ii) Sunny Stores rents a portion of its premises to other businesses. A tenant deposited

the monthly rent for April amounting to N$ 7 360 directly into the bank account of

Sunny Stores.

iii) A deposit of N$ 14 200 was recorded as N$ 12 400 in the cash receipts journal. This

deposit pertains to repairs done by Sunny Stores.

iv) Insurance premiums amounting to N$ 1 200 were deducted from the business bank

account via debit order. These premiums were not yet recorded in the cash payments

journal.

v)

Interest on the bank overdraft of N$ 160 and bank charges amounting to N$ 200

appeared in the bank statement but were not recorded in the cash payments journal.

vi) A withdrawal of N$ 1 000 appears on the bank statement as N$ 100.

vii) A withdrawal of N$ 2 200 was made by Sunnie's Steakhouse and incorrectly debited

to Sunny Stores by the bank.

viii) A cash purchase of inventory amounting to N$ 11 800 was recorded in the cash

payments journal as N$ 18 100.

ix) The bank account in the general ledger ot"sunny Stores reflects a credit balance of N$

12 400 (prior to any of the above adjustments) on 30 April 2024.

QUESTION 4

TO BE ANSWERED ON A SEPARATE PAGE

YOU ARE REQUIRED TO:

MARKS

(a)

Prepare the bank account in the general ledger of Sunny Stores

(7)

for April 2024.

(b)

Prepare the bank reconciliation for Sunny Stores for April

(3)

2024. The reconciliation should commence with the balance

7

|

|

8 Page 8 |

▲back to top |

per bank statement. Round up any numbers to the nearest

dollar.

(c)

List 5 controls to ensure the protection of cash in a business.

TOTAL MARKS: QUESTION 4

TOTAL MARKS: EXAMINATION PAPER

(5)

(15)

(100)

END OF ASSESSMENT

8