|

FAC511S-FINANCIAL ACCOUNTING 101-1ST OPP-NOV 2025 |

|

|

1 Page 1 |

▲back to top |

nAmlBIA UnlVERSITY

OF SCIEnCE Ano TECHnOLOGY

FACULTY OF COMMERCE, HUMAN SCIENCES AND EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING AND FINANCE

QUALIFICATION: BACHELOR OF LOGISTICS AND SUPPLY CHAIN MANAGEMENT AND

BACHELOR OF MARKETING

QUALIFICATION CODE: 07BLSC AND

07MARB

LEVEL: 5

COURSE : FINANCIAL ACCOUNTING 101

COURSE CODE: FACSllS

SESSION: NOVEMBER 2025

DURATION: 3 Hours

PAPER: THEORY & CALCULATIONS

MARKS: 100

FIRST OPPORTUNITY EXAMINATION QUESTION PAPER

EXAMINERS:

MODERATOR:

Ms H Kangala

Mr C Mahindi

INSTRUCTIONS TO CANDIDATES

1. Answer all questions in blue or black ink.

2. Round off all amounts to the nearest Namibian Dollar, where applicable.

3. A non-programmable calculator is permissible .

4. Show all your workings {where applicable) .

This Question paper is made up of 4 Pages (Excluding the front page)

0

|

|

2 Page 2 |

▲back to top |

Question 1

{30 marks)

PART A

{20 Marks)

Answer the questions below. Only write the question number and letter for the correct

answer in your answer book. Each question carries 2 marks.

1. Which of the following best describes the accounting cycle?

a) A process of classifying and summarising financial information into financial

statements

b) A process of preparing cash flow statements for decision-making

c) A process of identifying, recording, summarizing and communicating financial

information

d) A process of calculating profit and preparing tax returns at the end of the year

e) None of the above

2. What is the first step in the accounting cycle?

a) Recording journal entries

b) Identifying transactions

c) Preparing financial statements

d) Posting entries to the general ledger

e) Preparing the trial balance

f) None of the above

3. Which of the following steps follows posting to the ledger?

a) Preparing the trial balance

b) Identifying transactions

c) Preparing financial statements

d) Recording adjusting entries

e) Preparing closing entries

f) None of the above

4. Why are adjusting entries prepared at the end of the accounting period?

a) To adjust the accounting balances for tax purposes

b) To ensure revenues and expenses are recorded in the proper period

c) To transfer balances from income and expense accounts to capital

d) To prepare the trial balance before financial statements

e) None of the above

5. Which of the following is NOT a qualitative characteristic of useful financial

information?

a) Relevance

b) Faithful representation

c) Prudence

d) Comparability

|

|

3 Page 3 |

▲back to top |

e) Timeliness

f) None of the above

6. The entity theory assumes that:

a) The business is not separable from its owners

b) The business is a separate economic unit from its owners

c) Owners' personal expenses must be reported in business accounts

d) The business and owner share the same capital account

e) None of the above

7. Under the historical cost concept, assets should be recorded:

a) At the fair market value at acquisition date

b) At the purchase price paid to acquire the asset

c) At the expected selling price in the future

d) At the replacement cost of similar assets today

e) At the present value of expected cashflow

f) None of the above

8. Which of the following highlight the meaning of the going concern concept?

a) Assumes the business will continue to operate in the foreseeable future

b) Assumes the business will close after the accounting year ends

c) Requires assets to be valued at liquidation values

d) Requires profits to be distributed immediately to owners

e) Transactions are recorded when they occur and not when cash is received or paid.

f) None of all

9. The duality concept (double entry) means:

a) Every transaction affects the balance sheet

b) Every transaction has equal debit and credit effects

c) Every transaction must be recorded twice in the journal

d) Every transaction involves at least one asset and one liability

e) None of the above

10. The matching principle ensures that:

a) Revenues are recorded when cash is received, and expenses when cash is paid

b) Expenses are recorded in the same period as the revenues they help to generate

c) Revenues are recorded in the same period as expenses are paid

d) Expenses are recorded at the time they are approved by management

e) None of the above

2

|

|

4 Page 4 |

▲back to top |

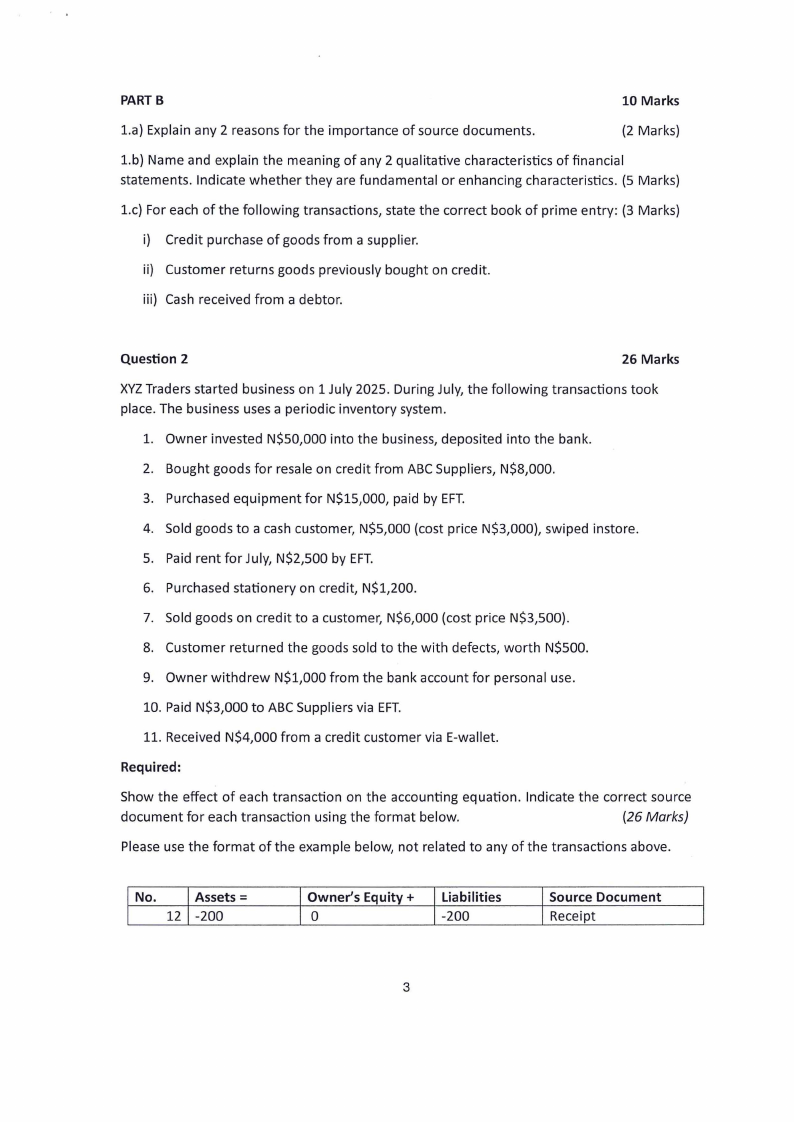

PARTB

10 Marks

1.a) Explain any 2 reasons for the importance of source documents.

(2 Marks)

1.b) Name and explain the meaning of any 2 qualitative characteristics of financial

statements . Indicate whether they are fundamental or enhancing characteristics. (5 Marks)

l.c) For each of the following transactions, state the correct book of prime entry : (3 Marks)

i) Credit purchase of goods from a supplier.

ii) Customer returns goods previously bought on credit.

iii) Cash received from a debtor.

Question 2

26 Marks

XYZ Traders started business on 1 July 2025. During July, the following transactions t ook

place. The business uses a period ic inventory system .

1. Owner invested N$50,000 into the business, deposited into the bank.

2. Bought goods for resale on credit from ABC Suppliers, N$8,000.

3. Purchased equipment for N$15,000, paid by EFT.

4. Sold goods to a cash customer, N$5,000 (cost price N$3,000), swiped instore.

5. Paid rent for July, N$2,500 by EFT.

6. Purchased stationery on credit, N$1,200.

7. Sold goods on credit to a customer, N$6,000 (cost price N$3,500).

8. Customer returned the goods sold to the with defects, worth N$500.

9. Owner withdrew N$1,000 from the bank account for personal use.

10. Paid N$3,000 to ABC Suppliers via EFT.

11. Received N$4,000 from a credit customer via E-wallet.

Required:

Show the effect of each transaction on the accounting equation. Indicate the correct source

document for each transaction using the format below.

(26 Marks)

Please use the format of the example below, not related to any of the transactions above.

No.

Assets=

12 -200

I I Owner's Equity+ Liabilities

Io

I -200

I Source Document

I Receipt

3

|

|

5 Page 5 |

▲back to top |

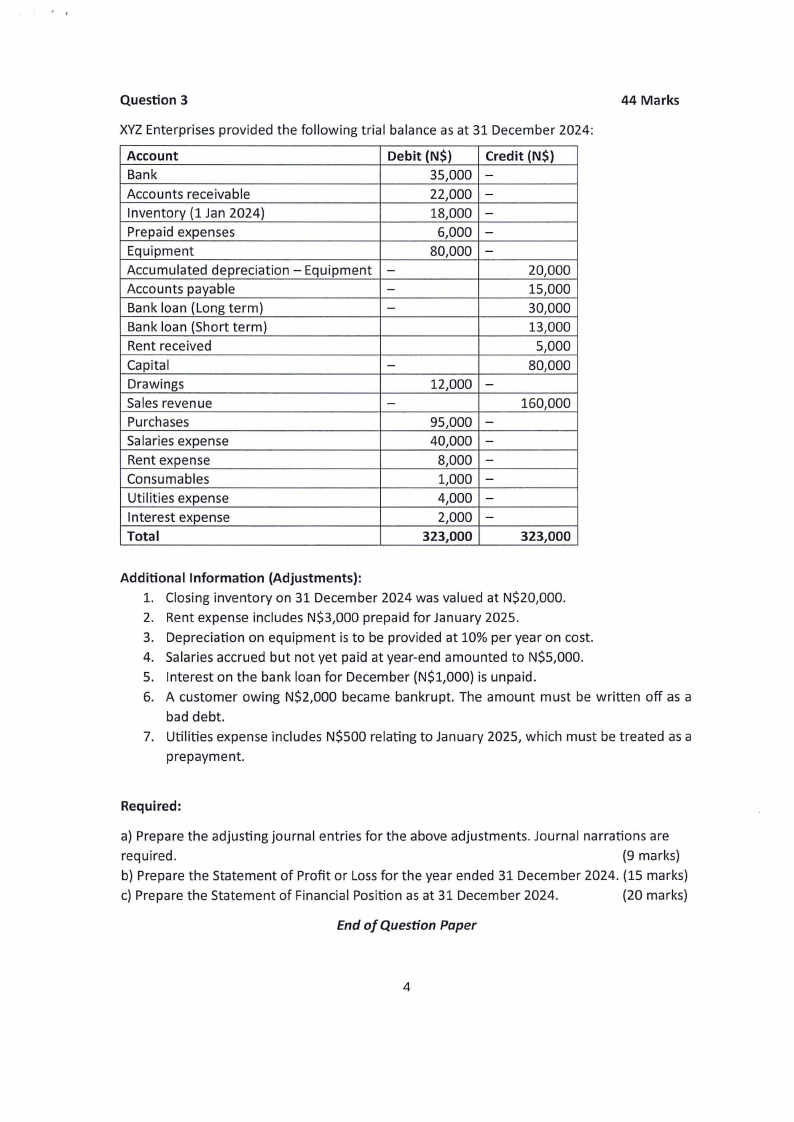

Question 3

XYZ Enterprises provided the following trial balance as at 31 December 2024:

Account

Bank

Accounts receivable

Inventory (1 Jan 2024)

Prepaid expenses

Equipment

Accumulated depreciation - Equipment

Accounts payable

Bank loan (Long term)

Bank loan (Short term)

Rent received

Capital

Drawings

Sales revenue

Purchases

Salaries expense

Rent expense

Consumables

Utilities expense

Interest expense

Total

Debit (N$)

35,000

22,000

18,000

6,000

80,000

-

-

-

-

12,000

-

95,000

40,000

8,000

1,000

4,000

2,000

323,000

Credit (N$)

-

-

-

-

-

20,000

15,000

30,000

13,000

5,000

80,000

-

160,000

-

-

-

-

-

-

323,000

44 Marks

Additional Information (Adjustments):

1. Closing inventory on 31 December 2024 was valued at N$20,000.

2. Rent expense includes N$3,000 prepaid for January 2025.

3. Depreciation on equipment is to be provided at 10% per year on cost.

4. Salaries accrued but not yet paid at year-end amounted to N$5,000.

5. Interest on the bank loan for December (N$1,000) is unpaid.

6. A customer owing N$2,000 became bankrupt. The amount must be written off as a

bad debt.

7. Utilities expense includes N$500 relating to January 2025, which must be treated as a

prepayment.

Required:

a) Prepare the adjusting journal entries for the above adjustments. Journal narrations are

required.

(9 marks)

b) Prepare the Statement of Profit or Loss for the year ended 31 December 2024. (15 marks)

c) Prepare the Statement of Financial Position as at 31 December 2024.

(20 marks)

End of Question Paper

4