|

FAC612S-FINANCIAL ACCOUNTING 202-1ST OPP-NOV 2025 |

|

|

1 Page 1 |

▲back to top |

~

n Am I BI A u n IVER s: ITY

OF SCIEnCE AnD TECHnOLOGY

FACULTY OF COMMERCE, HUMAN SCIENCES AND EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING AND FINANCE

QUALIFICATION: BACHELOR OF ACCOUNTING

QUALIFICATION CODE: 07BGAC

LEVEL: 6

COURSE CODE: FAC612S

COURSE NAME: FINANCIAL ACCOUNTING 202

DATE: October 2025

DURATION: 3 HOURS

PAPER: THEORY AND CALCULATIONS

MARKS: 100

EXAMINER(S)

FIRST OPPORTUNITY EXAMINATION PAPER

Dr. D. R. Muzir9, Ms. A Gustav, Ms. V. Ueitele, Mr. M, Nghiludile and Mr. C.

Mahindi

MODERATOR: Dr. S. Dzomira

INSTRUCTIONS

1. Capture your full name, student number and assessment number on the first page.

2. Answer ALL the questions and manage your time properly.

3. Number each page correctly

4. Write clearly and neatly.

5. Do not write in pencil and do not use tip-ex, as this will not be marked.

6. The names of people and businesses used throughout this assessment do not reflect the

reality and may be purely coincidental.

7. SHOWALLWORKINGSI

THIS QUESTION PAPER CONSISTS OF 4 PAGES (excluding this front page)

|

|

2 Page 2 |

▲back to top |

QUESTION 1

(25 marks)

Part A

(15 marks)

Erongo Pharma (Pty) Ltd is a pharmaceutical manufacturing and distribution company based

in Swakopmund, Namibia, with a financial year-end of 30 June.

During the final stages of the audit for the year ended 30 June 2025, the following

independent events were identified for consideration under IAS 37 - Provisions, Contingent

Liabilities and Contingent Assets:

Case 1: Possible Contamination of Medicines

In May 2025, management of Erongo Pharma received a report from one of their regional

distribution managers indicating that certain refrigerated medicines (mainly vaccines and

insulin products) may have been stored outside the required temperature range during transit

due to a refrigerated truck malfunction.

Although there were no reported customer complaints or returns by 30 June 2025, internal

quality control flagged a small batch as potentially unsafe. Based on past practices and internal

safety policies, management decided to quietly remove the affected batch from pharmacies

in early July and conduct voluntary quality testing at an estimated cost of N$750,000. The cost

of these tests and removal had already begun by 30 June 2025, although no public

announcement or formal recall occurred.

Case 2: Dispute with Logistics Provider

In July 2025, Erongo Pharma terminated a logistics contract with a third-party provider,

Namibian Med Logistics, after repeated delivery delays of critical medicines. MedLogistics is

claiming damages of N$1,100,000, alleging wrongful termination. Legal counsel advised that

although the outcome is uncertain, it is possible Erongo Pharma may have to pay a partial

settlement, but the claim is unlikely to succeed in full.

Required:

a) Discuss how the cases should be classified in terms of IAS 37 - Provisions, Contingent

Liabilities and Contingent Assets, and motivate your classification.

(8)

b) Prepare journal entries for the year ended 30 June 2025, if no journal entry is to be

passed explain why?

(3)

c) Disclose the cases(where applicable) in the notes to the financial statements for the

year ended 30 June 2025 in terms of IFRS.

(4)

1

|

|

3 Page 3 |

▲back to top |

Part B

(10 marks)

Erongo Pharma (Pty) Ltd (year-end 30 June 2025} financial statements were issued for

authorization on 25 July 2025. You have been presented with the following events:

1. On 2 July 2025, the company discovered that a batch of insulin shipped on 28 June 2025

was stored outside the recommended temperature range. Corrective testing and disposal

costs are estimated at N$600,000.

2. On 10 July 2025, the company's share price fell by 20% due to a general stock market

decline.

3. On 15 July 2025, a customer filed a lawsuit for a contract breach that occurred on 5 May

2025. Legal counsel advised that a settlement may be required.

4. On 1 August 2025, the company announced plans to expand its manufacturing facility next

year, with estimated costs of N$5 million.

5. On 5 August 2025, one of the company's major suppliers filed for bankruptcy, which may

affect future supply of raw pharmaceutical ingredients.

Required:

For each of the above events, indicate whether it is an Adjusting Event or a Non-Adjusting

Event according to IAS 10 - Events After the Reporting Period, and briefly explain why. (10}

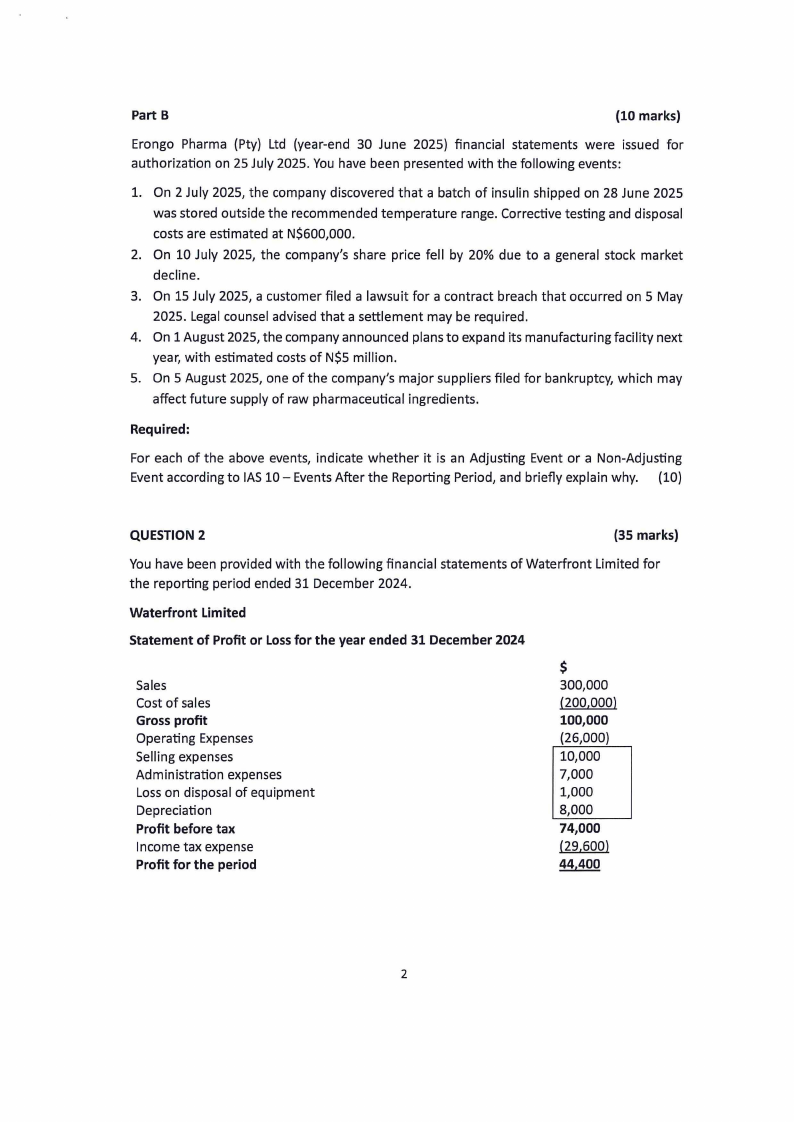

QUESTION 2

(35 marks)

You have been provided with the following financial statements of Waterfront Limited for

the reporting period ended 31 December 2024.

Waterfront Limited

Statement of Profit or Loss for the year ended 31 December 2024

Sales

Cost of sales

Gross profit

Operating Expenses

Selling expenses

Administration expenses

Loss on disposal of equipment

Depreciation

Profit before tax

Income tax expense

Profit for the period

$

300,000

(200,000)

100,000

(26,000}

10,000

7,000

1,000

8,000

74,000

(29,600)

44,400

2

|

|

4 Page 4 |

▲back to top |

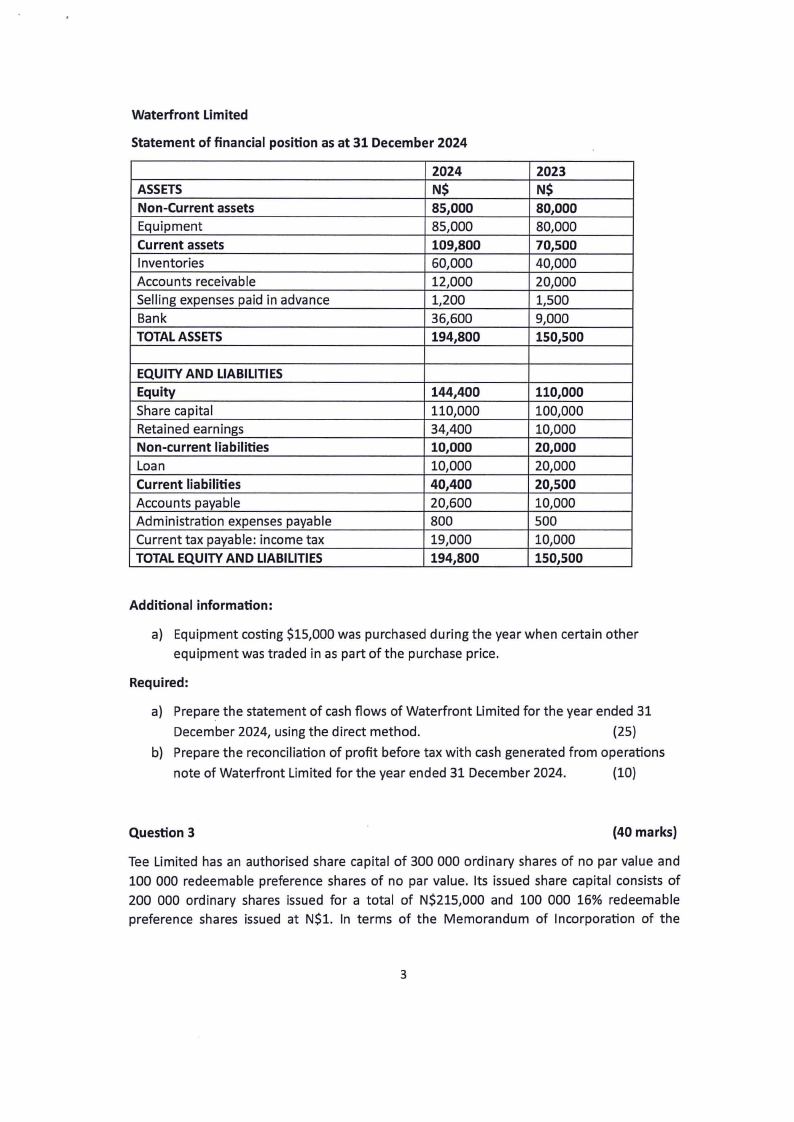

Waterfront Limited

Statement of financial position as at 31 December 2024

ASSETS

Non-Current assets

Equipment

Current assets

Inventories

Accounts receivable

Selling expenses paid in advance

Bank

TOTAL ASSETS

2024

N$

85,000

85,000

109,800

60,000

12,000

1,200

36,600

194,800

EQUITY AND LIABILITIES

Equity

Share capital

Retained earnings

Non-current liabilities

Loan

Current liabilities

Accounts payable

Administration expenses payable

Current tax payable: income tax

TOTAL EQUITY AND LIABILITIES

144,400

110,000

34,400

10,000

10,000

40,400

20,600

800

19,000

194,800

2023

N$

80,000

80,000

70,500

40,000

20,000

1,500

9,000

150,500

110,000

100,000

10,000

20,000

20,000

20,500

10,000

500

10,000

150,500

Additional information:

a) Equipment costing $15,000 was purchased during the year when certain other

equipment was traded in as part of the purchase price.

Required:

a) Prepare the statement of cash flows of Waterfront Limited for the year ended 31

December 2024, using the direct method.

(25)

b) Prepare the reconciliation of profit before tax with cash generated from operations

note of Waterfront Limited for the year ended 31 December 2024.

(10)

Question 3

(40 marks)

Tee Limited has an authorised share capital of 300 000 ordinary shares of no par value and

100 000 redeemable preference shares of no par value. Its issued share capital consists of

200 000 ordinary shares issued for a total of N$215,000 and 100 000 16% redeemable

preference shares issued at N$1. In terms of the Memorandum of Incorporation of the

3

|

|

5 Page 5 |

▲back to top |

company, the preference shares are redeemable at a premium of 3% of the issue price at the

option of the company any time after 1 April 2023.

The preference shares were redeemed at a premium of 3% of the issue price on 30 June 2025.

All dividends due had been paid on 29 June 2025. The dividends on preference shares were

discretionary (non-mandatory}.

In order to finance the redemption, on 30 June 2025 the company issued 30 000 N$1

debentures at a discount of 2% and the minimum number of ordinary shares required at

N$1.25

The directors are satisfied that the company's assets, fairly valued, exceed its liabilities and

that the company will be able to pay its debts as they become due.

Retained earnings at 30 June 2024 amounted to 60 000. The profit for the year ending 30 June

2025 has been correctly calculated as N$80,000.

Required:

a) Discuss how the preference shares will be classified in the records of Tee Limited.

(5}

b) Provide the general journal entries to account for the redemption of the preference

shares on 30 June 2025.

(10}

Workings

(4)

c} Show the relevant extracts of the following financial statements in terms of the

International Financial Reporting Standards. (Notes are not required but comparatives

are required}

i. the statement of financial position as at 30 June 2025, and

(9 .5}

ii. the statement of changes in equity for the reporting period ended 30 June 2025.

(11.5}

END OF EXAMINATION QUESTION PAPER

4