|

GRE811S-CORPORATE GOVERNANCE RISK MANAGEMENT AND ETHICS- 1ST OPP- JUNE 2025 |

|

|

1 Page 1 |

▲back to top |

nAmlBIA UnlVERSITY

OF SCIEnCE Ano TECHn OLOGY

FACULTY OF COMMERCE, HUMAN SCIENCESAND EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING & FINANCE

QUALIFICATION : BACHELOR OF ACCOUNTING {HONOURS)

QUALIFICATION CODE: 08BOAH

COURSE CODE: GRE 811S

LEVEL: 8

COURSE NAME: CORPORATE GOVERNANCE,

RISK MANAGEMENT AND ETHICS

DATE: JUNE 2025

DURATION: 3 HOURS

PAPER: THEORY AND APPLICATION

MARKS: 100

EXAMINER:

MODERATOR:

FIRST OPPORTUNITY EXAMINATION

Dumisani R. Muzira

Marko Tandota

INSTRUCTIONS

• This question paper is made up of FOUR (4) questions.

• Start each question on a new page.

• Answer All the questions and in blue or black ink.

• You are advised to pay due attention to expression and presentation. Failure to do so

will cost you marks.

• Start each question on a new page in your answer booklet

PERMISSIBLE MATERIALS

Non-programmable calculator/financial calculator

THIS QUESTION PAPER CONSISTS OF 5 PAGES {Including this front page)

pg.1

|

|

2 Page 2 |

▲back to top |

Question 1

Tom Co is a family business that has been wholly-owned and controlled by the Tom family

since 1920. The current chief executive, Mr Peter Tom, is the great grandson of the

company's founder and has himself been in post as CEOsince 1998. Because the Tom family

wanted to maintain a high degree of control, they operated a two-tier board structure: four

members of the Tom family comprised the supervisory board and the other eight non-family

directors comprised the operating board.

Despite being quite a large company with 5,000 employees, Tom Co never had any non-

executive directors because they were not required in privately-owned companies in the

country in which Tom Co was situated.

The four members of the Tom family valued the control ofthe supervisory board to ensure

that the full Tom family's wishes (being the only shareholders) were carried out. This also

enabled decisions to be made quickly, without the need to take everything before a meeting

of the full board.

Starting in 2008, the two tiers of the board met in joint sessions to discuss a flotation

(issuing public shares on the stock market) of 80% of the company. The issue of the family

losing control was raised by the CEO'sbrother, Mr Crispin Tom. He said that if the company

became listed, the Tom family would lose the freedom to manage the company as they

wished, including supporting their own long-held values and beliefs. These values, he said,

were managing for the long term and adopting a paternalistic management style. Other

directors said that the new listing rules that would apply to the board, including compliance

with the stock market's corporate governance codes of practice, would be expensive and

difficult to introduce.

The flotation went ahead in 2011. In order to comply with the new listing rules, Tom Co took

on a number of nonexecutive directors (NEDs) and formed a unitary board. A number of

problems arose around this time with NEDsfeeling frustrated at the culture and

management style in Tom Co, whilst the Tom family members found it difficult to make the

transition to managing a public company with a unitary board. Peter Tom said that it was

very different from managing the company when it was privately owned by the Tom family.

The human resources manager said that an effective induction programme for NEDs and

some relevant continuing professional development (CPD)for existing executives might help

to address the problems.

Required

(a) Compare the typical governance arrangements between a family business and a listed

company, and assess Crispin's view that the Tom family will 'lose the freedom to manage the

company as they wish' after the flotation. (10 marks)

(b) Assessthe benefits of introducing an induction programme for the new NEDs,and

requiring continual professional development (CPD)for the existing executives at Tom Co

after its flotation. (8 marks)

(c) Distinguish between unitary and two-tier boards, and discuss the difficulties that the Tom

family might encounter when introducing a unitary board. (7 marks)

pg.2

|

|

3 Page 3 |

▲back to top |

Question 2

A major corporate governance code contains the following entry on audit committees.

The board should establish formal and transparent arrangements for considering how they

should apply the corporate reporting and risk management and internal control principles

and for maintaining an appropriate relationship with the company's external auditors.

The board should establish an audit committee of at least three, or in the case of smaller

companies, two, independent non-executive directors. In smaller companies the company

chairman may be a member of, but not chair, the committee in addition to the independent

non-executive directors, provided he or she was considered independent on appointment as

chairman. All audit committee members should be considered independent upon

appointment to the committee. The board should satisfy itself that at least one member of

the audit committee has recent and relevant financial experience.

When Hasted Company floated on the stock exchange, it attempted to establish the audit

committee required by the listing rules. It was unable to recruit a non-executive director

with the requisite financial experience so it appointed experienced non-executive director,

Pauline Rar, as the committee chairman. Pauline Rar was a technical engineer. She was

appointed to the board of Hasted because of her expertise in the technology used by Hasted

and she understood the company's business model and its systems. But she did not

understand financial matters.

Pauline Rar told colleagues that she did not understand much about the concept of

independence. She said that in her own field of engineering, colleagues inside and outside a

certain company often supported each other and that this was often encouraged. As a

community of specialists, they often found that helping each other was an important part of

professional life over the years. Accordingly, she said she did not really understand why

independence was important for audit committee members. She also said that she did not

understand much about the company's relationship with the external auditors.

Required

(a) Define 'independence' in the context of audit committees, and explain why audit

committee members should be 'considered independent' at the time of their appointment.

(8 marks)

(b) Discuss how the inability of Hasted Company to recruit a person with 'recent and

relevant financial experience' might threaten the effectiveness of the audit committee's

contribution to shareholder value. (8 marks)

(c) Explain the nature of an 'appropriate relationship with the company's external auditors'

and discuss how Hasted Company's audit committee should respond if it believes the

relationship to be too close. (9 marks)

pg.3

|

|

4 Page 4 |

▲back to top |

Question 3

The risk committee at Northern Continents Company (NCC)met to discuss a report by its risk

manager, Stellar Field. The report focused on a number of risks that applied to a chemicals

factory recently acquired by SCCin another country, Southland. She explained that the new

risks related to the security of the factory in Southland in respect of burglary, to the supply

of one of the key raw materials that experienced fluctuations in world supply and also an

environmental risk. The environmental risk, Stellar explained, was to do with the possibility

of poisonous emissions from the Southland factory.

The SCCchief executive, Koor Chung, who chaired the risk committee, said that the

Southland factory was important to him for two reasons. First, he said it was strategically

important to the company. Second, it was important because his own bonuses depended

upon it. He said that because he had personally negotiated the purchase of the Southland

factory, the remunerations committee had included a performance bonus on his salary

based on the success of the Southland investment. He told Stellar that a performance-

related bonus was payable when and if the factory achieved a certain level of output that

Koor considered to be ambitious. 'I don't get any bonus at all until we reach a high level of

output from the factory,' he said. 'So I don't care what the risks are, we will have to manage

them.'

Stellar explained that one of her main concerns arose because the employees at the factory

in Southland were not aware of the importance of risk management to SCC.She said that

the former owner of the factory paid less attention to risk issues and so the staff was not as

aware of risk as Stellar would like them to be. 'I would like to get risk awareness embedded

in the culture at the Southland factory,' she said.

Koor Chung said that he knew from Stella r's report whatthe risks were, but that he wanted

somebody to explain to him what strategies SCCcould use to manage the risks. He was wary

of excessive costs and therefore wanted Northern Continents to employ practical strategies

to reduce risk as much as was reasonable.

Required

(a) Describe four strategies that can be used to manage risk and identify, with reasons, an

appropriate strategy for each of the three risks mentioned in the case. (12 marks)

(b) Explain the meaning of Stellar's comment: 'I would like to get risk awareness embedded

in the culture at the Southland factory.' (5 marks)

(c) Explain the benefits of performance-related pay in rewarding directors and critically

evaluate the implications of the package offered to Koor Chung. (8 marks)

pg.4

|

|

5 Page 5 |

▲back to top |

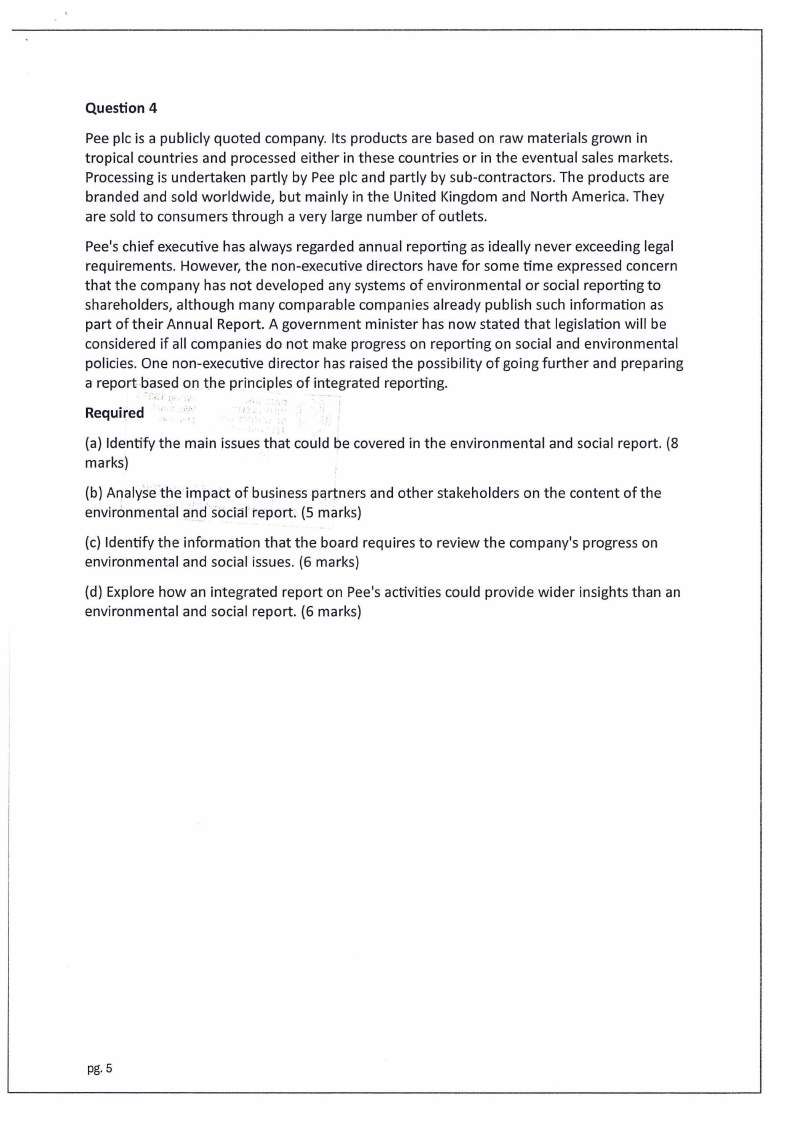

Question 4

Pee pie is a publicly quoted company. Its products are based on raw materials grown in

tropical countries and processed either in these countries or in the eventual sales markets.

Processing is undertaken partly by Pee pie and partly by sub-contractors. The products are

branded and sold worldwide, but mainly in the United Kingdom and North America. They

are sold to consumers through a very large number of outlets.

Pee's chief executive has always regarded annual reporting as ideally never exceeding legal

requirements. However, the non-executive directors have for some time expressed concern

that the company has not developed any systems of environmental or social reporting to

shareholders, although many comparable companies already publish such information as

part of their Annual Report. A government minister has now stated that legislation will be

considered if all companies do not make progress on reporting on social and environmental

policies. One non-executive director has raised the possibility of going further and preparing

a report-~ased on t_heprinciples of integrated reporting.

Required

(a) Identify the main issues that could be covered in the environmental and social report. {8

marks)

(b) Analyse the impact of business p·cirtnersand other stakeholders on the content of the

environmental and·sodal report. (5 marks)

(c) Identify the information that the board requires to review the company's progress on

environmental and social issues. (6 marks)

(d) Explore how an integrated report on Pee's activities could provide wider insights than an

environmental and social report. (6 marks)

pg.5