|

ATX812S-ADVANCED TAXATION-2ND OPP-DEC 2025 |

|

|

1 Page 1 |

▲back to top |

n Am I BI A u n IVER s I TY

OF SCI En CE Ano TECH n OLOGY

FACULTY OF COMMERCE, HUMAN SCIENCES AND EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING & FINANCE

QUALIFICATION: BACHELOR OF ACCOUNTING HONOURS

QUALIFICATION CODE: 08BOAH

LEVEL: 8

COURSE CODE: ATX812S

COURSE NAME: ADVANCED TAXATION

DATE: DECEMBER 2025

DURATION: 3 HOURS

PAPER: PRACTICAL AND THEORY

MARKS: 100

EXAMINERS:

SECOND OPPORTUNITY EXAMINATION - QUESTION PAPER

E Hamukwaya

MODERATOR: MN Amakali

INSTRUCTIONS

• This question paper is made up of five (5) questions.

• Number each question correctly.

• Answer all the questions in blue or black ink only.

• Round of all amounts to the nearest Namibian Dollar (N$)

• You are advised to pay due attention to expression and presentation. Failure to do so will

cost you marks.

• Start each question on a new page in your answer booklet and show all your workings.

• Questions relating to this paper may be raised in the initial 30 minutes after the start of

the paper. Thereafter, candidates must use their initiative to deal with any perceived error

or ambiguities and any assumption made by the candidate should be clearly stated.

• Clearly state (any) assumptions made (where applicable)

PERMISSIBLE MATERIALS

Non-programmable calculator

Namibian Value Added Tax Act No 10 of 2000

Namibian Income Tax Act No 24 of 1981

THIS QUESTION PAPER CONSISTS OF 8 PAGES {Including this front page)

|

|

2 Page 2 |

▲back to top |

QUESTION 1

(20 marks; 36 minutes)

Gladys Harambee is a single parent with four school going children under her care and her

salary was not enough for the size of her family. To supplement her salary, Gladys used her

savings to buy a house in the suburb of Katutura in Windhoek in 2008. She added three

bedrooms and two bathrooms to the house in order for her to receive higher rentals. Since

then, Gladys has been letting this house every year to students that come to Namibia from

Angola to study at the University of Namibia.

However, as from May 2024 Gladys has been finding it very difficult to find tenants for her

house due to the Namibian economy that was not performing well. This was worsened by the

Angolan students that stopped coming to Namibia due to their own financial challenges.

Gladys has had periods where her house was vacant for 6 months and this has been causing

her severe financial challenges. One of her close friends has advised her to sell the house and

invest the money in an interest bearing bank account offering interest rates of 9% per annum.

So in January 2025, Gladys took the advise, started advertising her house and she has found

a buyer willing to buy the house for N$ 1 200 000.00. Gladys is however unsure on whether

she will be taxed from the proceeds received from the sale of this house.

QUESTION 1 REQUIRED

Advice Gladys on whether she will be taxed on the N$ 1 200 000 that she will

receive from the sale of her Katutura house should she decide to sell it by looking

at all components of the gross income definition.

Support your answer with relevant case law and legislation

Communication skills - layout and logical argument

TOTAL MARKS

Marks

19

1

20

|

|

3 Page 3 |

▲back to top |

QUESTION 2

40 Marks (72 Minutes)

JP Electricals (Pty) Ltd (hereafter JP Electricals) is a company based in Windhoek that

manufactures and sells electrical gadgets on a cash and credit basis to the public and

wholesalers. The company has provided you with the following information for the year

ending 31 March 2025:

Notes

N$

Sales

2 000 000

Rental income

1

50 000

Dividends received

2

38 000

Profits from an Angolan business

3

350 000

Government stock interest received

4

7 000

TOTAL INCOME

2 445 000

Less expenses:

Purchases

400 000

Stationery expenses

40 000

Depreciation

5

130000

Salaries and wages

6

280 000

Transport costs

7

140 000

Bad debts provision

8

30 000

Annuity paid

9

30 000

Restraint of trade payment

10

200 000

Legal expenses

11

10 000

Leasehold improvements

12

275 000

Lease premium

12

23 000

Rent expense

12

200 000

|

|

4 Page 4 |

▲back to top |

Notes

1. JP Electricals has some offices in Okahandja that it lets out to tenants . JP Electricals

bought these offices in the year 2000, when property prices were low.

2. JP Electricals received this dividend from its investment in ABC Furniture (Pty) Ltd, a

Namibian based company that sells furniture around Namibia.

3. JP Electricals has a subsidiary company that operates in Angola and these are the

profits realised during the year from the Angolan business.

4. JP Electricals received interest during the year from Government stock that it

purchased.

5. The following are the assets of JP Electricals:

Asset

Date of purchase

Cost-N$

Machinery

05/01/2025

330 000

Delivery truck

03/03/2024

250 000

Motor vehicle

17/12/2015

200 000

6. 20% of salaries and wages are paid to staff who are directly involved in the

manufacturing process.

7. 100% of transport costs were incurred in transporting materials used in the

manufacturing activities.

8. The accountant provided for bad debts at N$ 180 000 for the current year. The

allowance for the prior year was N$ 150 000. JP Electricals's provision relates to a

specific list of debtors.

9. JP Electricals pays an annuity to one of its former employees that left the company

due to ill-health.

10. JP Electricals entered into a 5 year restraint of trade agreement with John Kennedy

the former manufacturing manager when he resigned from their business.

11. Lawyer's fees paid for the collection of debts.

12. JP Electricals rents the building that it uses for its offices and manufacturing activities.

In terms ofthe lease agreement, JP Electricals were obliged to make improvements of

N$ 250 000 to the building. The lease agreement became effective on 01/05/2024 for

10 years and the improvements were completed on 01/03/2025. In addition, JP

Electricals had to pay a lease premium to occupy the offices and the warehouse.

Rentals of N$ 20 000 were being paid per month .

|

|

5 Page 5 |

▲back to top |

Notes

13. Inventory on hand as at 31 March 2024 was N$ 200 000. Inventory on hand as at 31

March 2025 was N$ 300 000.

14. The assessed loss brought forward from 2024 was N$ 66 000.

REQUIRED

Marks

Calculate the taxable income of JP Electricals (Pty) Ltd for the year ended 31 March

2025 . Ignore VAT.

Provide your answer in column format with reference to applicable reasons of the

40

Income Tax Act No. 24 of 1981 for the inclusion, deduction or omission of each item in

your answer.

QUESTION 3

10 Marks (18 Minutes)

Voolies (Pty) Ltd is a company incorporated in Australia and is managed and controlled in

Australia. It has substantive business operations in Namibia, which it operates through

branches. The following information relates to Voolies trading in Namibia for the year of

assessment ending 30 June 2020:

Notes N$

Sales in Namibia

471000

Sales - export to Australia

321000

Foreign exchange gain

1

6 321

Dividends declared to Voolies

2

44 000

Less: expenditure

Directors fees

Other deductible expenses

3

6 000

141000

5

|

|

6 Page 6 |

▲back to top |

Notes

1.

The foreign exchange gain was realised on a transaction which involved the export

of goods to Australia.

2.

Voolies used some of its surplus funds to buy shares in a Company based in

Namibia and these are the gross dividends declared to Voolies.

3.

The managing director of the international company, Mr Silas who is based in

Australia came for a board meeting in Namibia and was paid these fees.

REQUIRED:

MARKS

a) Calculate the total taxes due by Voolies in Namibia and clearly state the type of

8

the taxes payable.

b) Briefly explain if Mr Silas will be taxed in Namibia and if so, how much is the tax.

2

TOTAL MARKS

10

QUESTION 4

10 Marks (18 Minutes)

Joshua Anderson and Jonathan Rhys, both residents, had for many years successfully operated

a business in partnership. They had shared profits and suffered losses equally. At the

commencement of the 2025 year of assessment, they incorporated their company. The

reasons for this were:

1.

To limit their personal liabilities;

2. To give the business an opportunity for perpetual succession;

3.

To be able to change the profit or loss sharing ratios; and

4.

To reduce their personal tax liabilities.

Their business' market value was in excess of its net asset value. This meant that a goodwill

account was created in the company. Peter and Paul then advanced funds to the company so

it could pay the partnership for the newly formed company. The creation of the company

resulted in a tax saving for both the former partners.

The Commissioner has informed Joshua and Jonathan that he is going to raise the provisions

of section 95 against them on the grounds that the incorporation of their company was an

impermissible tax avoidance arrangement.

REQUIRED:

MARKS

Discuss whether the Commissioner can apply the General Anti-Avoidance provisions in

15

terms of section 95 in respect of the above operation

6

|

|

7 Page 7 |

▲back to top |

QUESTION 5

20 Marks (36 Minutes)

Vicky Haufiku is a Labour Lawyer for a local company Legal Shield (Pty} Ltd. Mrs Haufiku has

been working for this company for the last 25 years of her life.

Mrs Haufiku has two children, one being her biological son of 21 years of age and the other

being her step-daughter of 25 years of age. For the purpose of providing them a post-school

qualification at a reputable University, she took out an education policy for each of her

children . She pays a monthly premium of N$ 1,200 on the policy for her 21 year-old son, and

N$ 2,500 on the 2nd policy for her 25 year-old step daughter. Her step daughter is partially

dependant on Mrs Haufiku as she still lives with Mrs Haufiku and her father and receives

maintenance and support but holds a waitressing job at the local bistro. You can assume that

she is not liable for normal tax. During the year, on 31 December 2024, the 2nd policy on Mrs

Haufiku's step-daughter matured, paying out N$ 150,000 for the purpose of acquiring an

education. Assume that the premium payments ended with the maturity of this 2nd policy. As

Mrs Haufiku has recently purchased a new home, instead of using the Education policy pay-

out for the education of her step-daughter, she used the money and paid it into her home

loan.

Legal Shield (Pty) Ltd gives Mrs Haufiku a travel allowance of N$ 6,900 per month for purposes

of travelling for business purposes around the country. Mrs Haufiku keeps a comprehensive

and accurate logbook of her business kilometres travelled and expenses incurred . The original

cost including VAT of her vehicle, purchased 01 March 2015, was N$ 430,000. Her total

kilometres travelled for business and private purposes were 98,110 kilometres, of which

23,550 kilometres were for private purposes. The following costs were incurred throughout

the year of assessment:

•

Repairs and Maintenance: N$ 15 100.

•

Total Fuel & oil costs: N$ 21,100.

•

Licence renewal: N$ 450.

•

Car Insurance at N$ 1,550 per month. You can assume the car insurance contract was

entered into on N$ 01 March 2015.

During the year-end function in December 2024, Mrs Haufiku was nominated as the most

productive employee of the year. As Mrs Haufiku wanted to take a short holiday to reward

herself for her hard work during the year, Legal Shield provided a weekend away in

Swakopmund. The weekend comprised of three nights' accommodation, including breakfast

and dinner, at the Seaside Hotel & Spa. The cost per night comprised of N$ 2 500 for two

people sharing a room . Mrs Haufiku only needed to cover her own fuel and lunch expenses.

During the current year of assessment, Mrs Haufiku purchased an annuity at Metropolitan of

N$ 350,000 on 01 March 2024. The annuity only started paying out from 01 May 2024, at N$

1,285 per month . It will pay out for 30 years

7

|

|

8 Page 8 |

▲back to top |

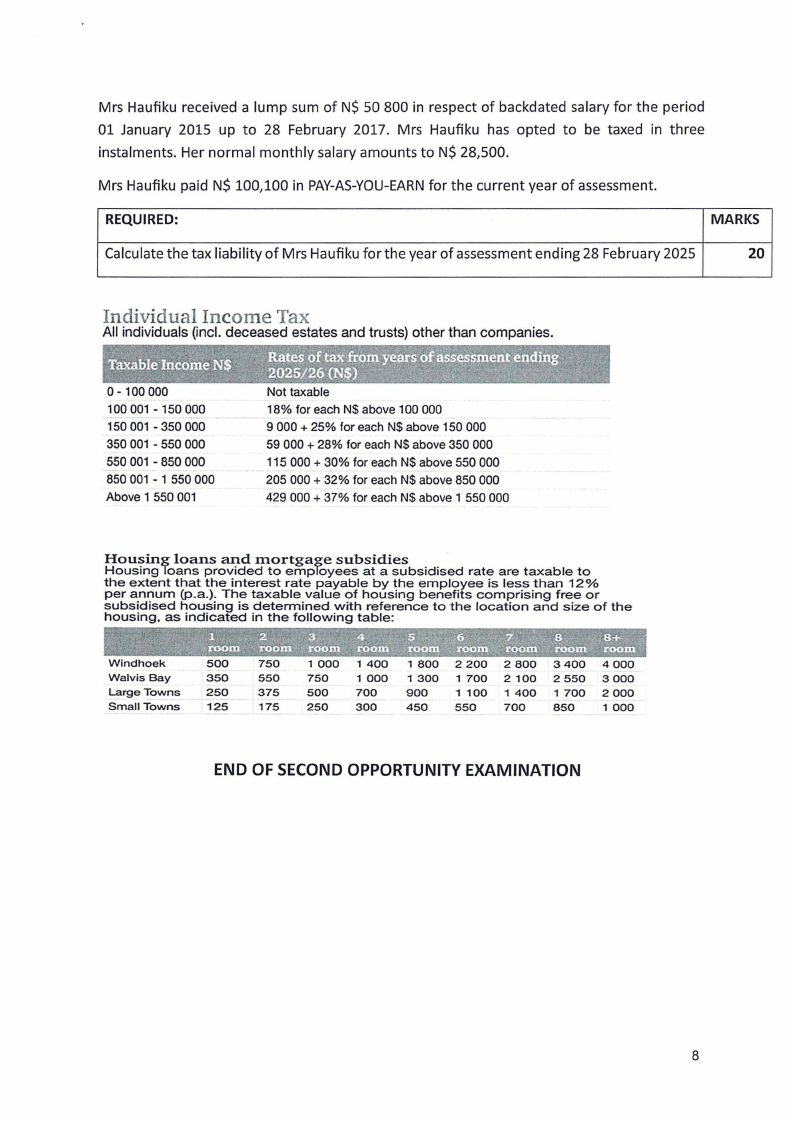

Mrs Haufiku received a lump sum of N$ 50 800 in respect of backdated salary for the period

01 January 2015 up to 28 February 2017. Mrs Haufiku has opted to be taxed in three

instalments. Her normal monthly salary amounts to N$ 28,500.

Mrs Haufiku paid N$ 100,100 in PAY-AS-YOU-EARN for the current year of assessment.

REQUIRED:

MARKS

Calculate the tax liability of Mrs Haufiku for the year of assessment ending 28 February 2025

20

Individual Incon1e Tax

All individuals (incl. deceased estates and trusts) other than companies.

0-100 000

100 001 - 150 000

150 001 - 350 000

350 001 - 550 000

550 001 - 850 000

-·

.

850 001 - 1 550 000

Above 1 550 001

Not taxable

18% for each N$ above 100 000

9 000 + 25% for each N$ above 150 000

59 000 + 28% for each N$ above 350 000

115 000 + 30% for each N$ above 550 000

205 000 + 32% for each N$ above 850 000

429 000 + 37% for each N$ above 1 550 000

Housing loans and mortgage subsidies

Housing Toans provided to empfoyees at a subsidised rate are taxable to

the extent that the interest rate payable by the employee is less than 12%

per annum (p.a .). The taxable value of housing benefits comprising free or

subsidised housing is determined with reference to the location and size of the

housing, as indicated in the following table:

Windhoek

Walvis Bay

Large Tow_ns

Small Towns

500

350

250

125

750

550

375

175

1 000

750

500

250

1 400

1 000

700

300

1 800

1 300

900

450

2 200

1 700

1 100

550

2 800

2 100

1 400

700

3 400

2 550

1 700

850

4 000

3 000

2 000

1 000

END OF SECOND OPPORTUNITY EXAMINATION

8