|

FAC701Y-FINANCIAL ACCOUNTING 300-1ST OPP-NOV 2025 |

|

|

1 Page 1 |

▲back to top |

nAmlBIA UnlVERSITY

OF SCI En CE Ano TECH n OLOGY

FACULTY OF COMMERCE, HUMAN SCIENCES AND EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING AND FINANCE

QUALIFICATION : BACHELOR OF ACCOUNTING {CHARTERTED ACCOUNTANCY)

COURSE CODE: FAC701Y

DATE: 09 OCTOBER 2025

COURSE NAME: FINANCIAL ACCOUNTING

300

PAPER: PRACTICAL AND THEORY

DURATION: 180 MINUTES (3 HOURS)

READING TIME: 30 MINUTES

WRITING TIME: 150 MINUTES

MARKS: 100

ASSESSMENT 6 2025 - OPPORTUNITY 1- INFORMATION

EXAMINERS:

MODERATOR:

G. Kafula

Z. Stellmacher

Z. Patel

INSTRUCTIONS

• This question paper is made up of TWO (2) questions.

• Answer BOTH questions in blue or black ink only. NO PENCIL.

• You are allowed to use a non-programmable or financial calculator and the IFRS standards

during the assessment.

• You are advised to pay due attention to expression and presentation. Failure to do so will cost

you marks.

• Start each question on a new page in your answer booklet and number your answers correctly.

• Show all your workings and where relevant, round all answers to two decimal places.

• Questions relating to this paper may be raised in the initial 30 minutes after the start of the

assessment. Thereafter, candidates must use their initiative to deal with any perceived errors or

ambiguities and any assumption made by the candidate should be clearly stated .

• Please take note that all names and case studies used are fictional.

THIS QUESTION PAPER CONSISTS OF 8 PAGES (Including this front page)

1

|

|

2 Page 2 |

▲back to top |

QUESTION 1

47 MARKS

Snap Ltd (Snap) is a photography company that was established in the early 2000's. The

company specialises in photography of events, portraits and fashion . The staff complement

has grown over the years, and Snap has become a well-known name in the photography

circles, both in Namibia and internationally. You are assisting the reporting team to finalise

the Snap Ltd Group (Snap Group) financial statements for the year ended 30 September 2024.

The following companies are part of Snap's portfolio.

Snap holds 75% of the ordinary share capital in lnsta. It acquired control of lnsta in 2019. lnsta

is involved in digital printing. The company was also established in the 2000's when the

demand for professional photography printing was increasing.

Shortly after acquisition, lnsta started selling inventory to Snap. lnsta charges a mark-up of

25% on cost price. Total sales for the current year amounted to N$ 978 000 (2023: N$789 500).

On 30 September 2024, Snap had inventory on hand purchased from lnsta of N$164 500

(2023: N$255 000).

lnsta wanted to expand its network and grow its footprint within the photography space. lnsta

approached companies that are external to the Snap Group - Lebelo (Pty) Ltd (Lebelo) and

Codak (Pty) Ltd (Codak). lnsta, Lebelo and Codak contractually agreed to form a new company

named TacTic (Pty) Ltd (TacTic) and have joint control over it. TacTic will oversee the marketing

and brand awareness of the companies. TacTic is a separate juristic person and registered as

a company in terms of the Companies Act. The financial year end was agreed to be same as

the other companies within the group.

All three parties manage TacTic and act collectively to direct the activities that significantly

affect the returns of the arrangement. All decisions about the relevant activities require the

unanimous consent of lnsta, LebeloF and Codak. Any cash flow shortages of TacTic will be

financed by the parties in accordance with their ownership interest. TacTic will own all its

assets and liabilities and none of the three parties have rights to the residual interest ofTicTac.

Each party paid N$56 000 for a 33,3% share of the equity shares of TacTic. No gain on bargain

purchase nor goodwill arose from this transaction. Operations in TacTic began on 1 February

2024. TacTic incurred a loss of N$66 500 for the period ended 30 September 2024.

Snap acquired a 48% interest in Gramalot on 1 April 2024. At that date, Gramalot had a share

capital of N$500 000. The purchase consideration of N$1 600 000 will be settled in cash on 1

December 2024. The other two shareholders, Athi Quthing (AthiQ) and Khaya Noah hold a

20% and 32% interest, respectively. Each share entitles the holder to one vote. Any decisions

regarding the operating and financial activities of Gramalot require majority vote.

AthiQ's involvement in the entity is minimal due to her various commitments and she signed

an agreement on 28 May 2024, with Snap, appointing Snap as her proxy for her vote for all

shareholder meetings as of 1 June 2024. AthiQ is still entitled to her share of returns generated

by Gramalot.

2

|

|

3 Page 3 |

▲back to top |

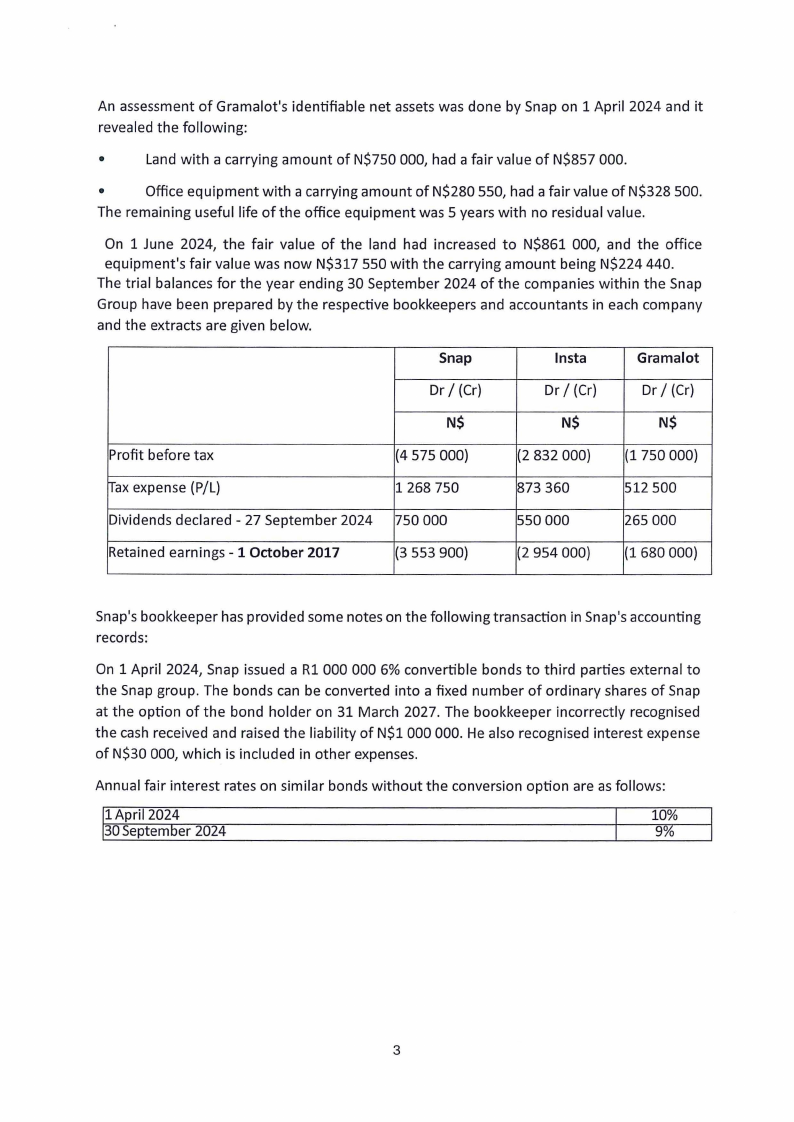

An assessment of Gramalot's identifiable net assets was done by Snap on 1 April 2024 and it

revealed the following:

•

Land with a carrying amount of N$750 000, had a fair value of N$857 000.

•

Office equipment with a carrying amount of N$280 550, had a fair value of N$328 500.

The remaining useful life of the office equipment was 5 years with no residual value.

On 1 June 2024, the fair value of the land had increased to N$861 000, and the office

equipment's fair value was now N$317 550 with the carrying amount being N$224 440.

The trial balances for the year ending 30 September 2024 of the companies within the Snap

Group have been prepared by the respective bookkeepers and accountants in each company

and the extracts are given below.

Snap

lnsta

Gramalot

Dr I (Cr}

Dr/ (Cr}

Dr I (Cr}

N$

N$

N$

Profit before tax

(4 575 000}

(2 832 000} (1750000}

Tax expense (P/L}

1268 750

873 360

512 500

Dividends declared - 27 September 2024 750 000

550 000

265 000

Retained earnings - 1 October 2017

(3 553 900}

(2 954 000} (1680 000}

Sn ap's bookkeeper has provided some notes on the following transaction in Snap's accounting

records:

On 1 April 2024, Snap issued a Rl 000 000 6% convertible bonds to third parties external to

the Snap group. The bonds can be converted into a fixed number of ordinary shares of Snap

at the option of the bond holder on 31 March 2027. The bookkeeper incorrectly recognised

the cash received and raised the liability of N$1 000 000. He also recognised interest expense

of N$30 000, which is included in other expenses.

Annual fair interest rates on similar bonds without the conversion option are as follows:

11 April 2024

10%

30 September 2024

9%

3

|

|

4 Page 4 |

▲back to top |

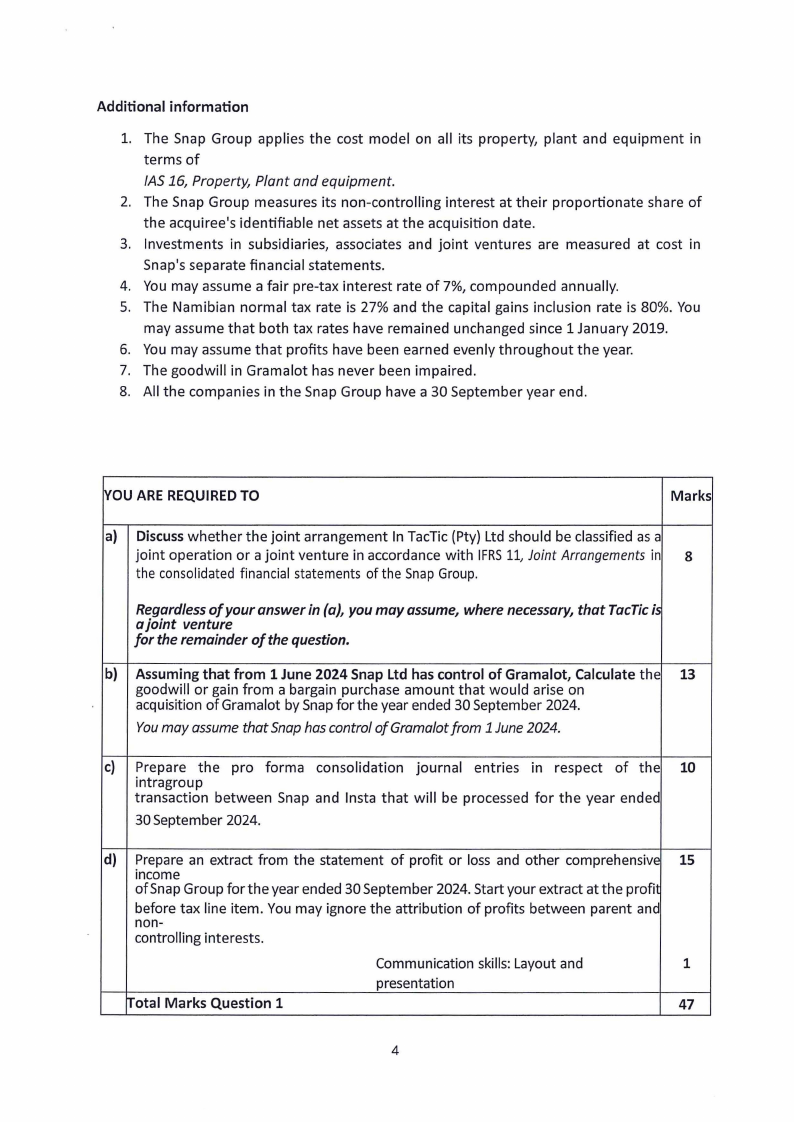

Additional information

1. The Snap Group applies the cost model on all its property, plant and equ ipment in

terms of

/AS 16, Property, Plant and equipment.

2. The Snap Group measures its non-controlling interest at their proportionate share of

the acquiree's identifiable net assets at the acquisition date.

3. Investments in subsidiaries, associates and joint ventures are measured at cost in

Snap's separate financial statements.

4. You may assume a fair pre-tax interest rate of 7%, compounded annually.

5. The Namibian normal tax rate is 27% and the capital gains inclusion rate is 80%. You

may assume that both tax rates have remained unchanged since 1 January 2019.

6. You may assume that profits have been earned evenly throughout the year.

7. The goodwill in Gramalot has never been impaired.

8. All the companies in the Snap Group have a 30 September year end.

r,,ou ARE REQUIRED TO

Marks

a) Discuss whether the joint arrangement In TacTic (Pty} Ltd should be classified as a

joint operation or a joint venture in accordance with IFRS 11, Joint Arrangements in 8

the consolidated financial statements of the Snap Group.

Regardless of your answer in (a), you may assume, where necessary, that TacTic is

a joint venture

for the remainder of the question.

b) Assuming that from 1 June 2024 Snap Ltd has control of Gramalot, Calculate the 13

goodwill or gain from a bargain purchase amount that would arise on

acquisition of Gramalot by Snap for the year ended 30 September 2024.

You may assume that Snap has control of Gramalot from 1 June 2024.

c) Prepare the pro forma consolidation journal entries in respect of the 10

intragroup

transaction between Snap and lnsta that will be processed for the year ended

30 September 2024.

d) Prepare an extract from the statement of profit or loss and other comprehensive 15

income

of Snap Group for the year ended 30 September 2024. Start your extract at the profit

before tax line item. You may ignore the attribution of profits between parent and

non-

controlling interests.

Communication skills: Layout and

1

presentation

Total Marks Question 1

47

4

|

|

5 Page 5 |

▲back to top |

QUESTION 2

53 MARKS

Chocolat Ltd is a listed company, established in 2019, which produces organic chelate. The

founders of the company identified the gap in the market for chocolate with a limited sugar

content. The company's head office and manufacturing plant is based in Swakopmund. The

year-end of the company is 30 June.

Lease agreement - manufacturing machine

Chocolat Ltd entered a lease agreement to lease a new manufacturing machine from Lezzee

Ltd at its cash price of N$1 250 000 for a period of three years as of 1 October 2021. The

terms of the contract are as follows:

• Lezzee Ltd granted Chocolat Ltd the right to use the manufacturing machine. Chocolat

Ltd will have exclusive use of the machine and make all decisions regarding the use of

the machine.

• Chocolat Ltd would make bi-annual payments of N$ 250 000 to Lezzee Ltd. These

payments will be made in advance, starting on 1 October 2021.

• Ownership of the manufacturing machine will be transferred to Chocolat Ltd on 30

September 2024, after payment of a guaranteed residual value of N$ 50 000.

• The manufacturing machine was available for use, as intended by management on 1

October 2021. On this date, an estimated useful life of four years and a residual value

of N$ nil for depreciation purposes was allocated to the manufacturing machine.

• On 1 October 2021, Chocolat Ltd incurred and paid legal fees amounting to N$ 24 000

in relation to the above agreement.

Acquisition of warehouse in Windhoek

On 1 October 2020, Chocolat Ltd purchased a warehouse in Windhoek for N$ 42 million to

store raw materials. The warehouse has an estimated useful life of 20 years with no residual

value and is accounted for using the cost model.

On 30 June 2022, the warehouse was damaged due to a fire. On that date, the warehouse's

value-in-use and fair value less disposal were assessed by an independent expert to be N$ 35

million and 33 million respectively.

Employee benefits

Chocolat Ltd paid annual salaries of N$ 5 000 000 to its employees for the 2021 and 2022

financial years. Due to the current financial crisis in the country no increases are expected in

the financial year.

It is the policy of the company to provide 20 working days leave to its employees. Chocolat

Ltd operates a five-day workweek. For the purpose of this question public holidays can be

ignored.

5

|

|

6 Page 6 |

▲back to top |

The following are the leave statistics for the employees:

• End of June an average of 9 days of the 2021 financial year leave were unused

• End of June an average of 14 days was used, coming from, on average:

✓ The 2021 leave entitlement: 5 days

✓ The 2022 leave entitlement: 9 days

The estimated future leave statistics for the year ending 2023 are as follows:

• An average of 12 days will be taken and on average this is expected to come from:

2021:

0

days

2022:

4

days

2023: 8 days

All three years consist of 365 calendar days each.

Issue of bonds

On 1 April 2022, Chocolat Ltd issued bonds to raise capital. D Ltd purchased 100 000 13,5%

bonds from Chocolat Ltd at their fair value of N$ 22 per bond. The bonds have a par value of

N$ 20 and pay coupon interest annually on 31 March. D Ltd incurred and paid transaction

costs of N$ 18 750 related to this transaction. The bonds are mandatorily redeemable on 31

March at their par value. The objective of D Ltd's business model, regarding the investment in

the Chocolat Ltd bonds, is to collect the future contractual cash flows of interest and principal

on specified dates. D Ltd has a 30 June year-end.

The credit risk on the investment in Chocolat Ltd's bonds was consistently assessed as low as

a result of the financial backing received by its parent, L Ltd. The 12-month weighted

probability of default on the bonds was assessed as 12% on 1 April and 14% on 30 June 2022.

In addition, the lifetime weighted probability of default on the bonds was assessed as 18% on

1 April 2022 and 22% on 30 June 2022.

Other investments

The investment portfolio of Chocolat Ltd on 30 June 2024, includes the following

investments:

• Government bonds which are redeemable in two years time, were purchased at an

amount of N$ 1 400 000 (Face value: N$ 1 500 000) on 1 July 2019 by Chocolat Ltd.

The coupon interest rate is 10 % per annum, payable bi-annually on the face value of

the bonds. The bonds were redeemed on 30 June 2021 at N$ 1 800 000.

6

|

|

7 Page 7 |

▲back to top |

The effective interest rate is 16.32688 % per annum on the bonds (8.16444 % bi-

annual interest rate). The market related interest rate for the year amounted to

12.45 %.

• Investment in listed shares of Cocoa Ltd which are actively traded .

• Investment in convertible debentures. The debentures were issued on 1 July 2021 at

a face value of N$ 10 each (considered to be fair value on issue date). The

debentures offer interest based on a coupon rate of 12 %. The debenture holder has

the option to convert the debentures into 2 000 ordinary shares on 30 June 2024. If

the debentures are not converted, they will be redeemed on this date at N$ 10 each .

Taxation

Assume a normal tax rate of 27%.

The Namibian Revenue Agency (NAM RA} grants an allowance of 40% on the cost price of the

manufacturing machine not apportioned for part of the year in which the machine is

purchased.

VOU ARE REQUIRED TO

Marks

a) Disclose the information given above pertaining the manufacturing machine's 10

lease, in the profit before tax note to the annual financial statements of Chocolat

Ltd for the financial year ended 30 June.

You may assume an annual interest rate of 19.04 % per annum.

Show all calculations as marks may be awarded thereto.

b)

Calculate the deferred tax balance relating to the manufacturing machine, to be

presented in the statement of financial position of Chocolat Ltd at 30 June 2022.

6

~ou must indicate whether the deferred tax balance is an asset or liability.

c)

Explain and calculate how the warehouse damage on 30 June 2022 should be 10

accounted for in Chocolat's financial statements, if at all. Ignore any tax

implications.

d) Calculate the leave-pay liability for Chocolat Ltd's financial year ended 30 June

if:

3

• annual leave is accumulating and available for use in the next financial year.

It is vesting at the end of the year following the next year, if unused .

1

• annual leave is accumulating and available for use in the next financial year.

It is non-vesting if unused by the end of the next financial year.

e) Write a memorandum to the Chief Executive Officer of Chocolat Ltd in which you 10

explain the classification of the financial instruments in the investment portfolio.

Exclude the bonds issued by Chocolat Ltd in you answer.

7

|

|

8 Page 8 |

▲back to top |

f)

Prepare all the journal entries relating to the investment in the Chocolat Ltd 13

bonds in the accounting records of D Ltd for the financial year ended 30 June.

Uournal narrations are not required .

rrotal Marks Question 2

53

UN/SA (Adapted)

END

8