|

GFA712S-FINANCIAL ACCOUNTING 320-1ST OPP-NOV 2025 |

|

|

1 Page 1 |

▲back to top |

nAm I BI A un IVERSITY

OF SCI En CE Ano TECH n OLOGY

FACULTY OF COMMERCE, HUMAN SCIENCES AND EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING AND FINANCE

QUALIFICATION: BACHELOR OF ACCOUNTING

QUALIFICATION CODE: 07 BOAC

LEVEL: 7

COURSE CODE: GFA 7125

COURSE NAME: FINANCIAL ACCOUNTING 320

SESSION: Oct/Nov 2025

PAPER: THEORY AND CALCULATIONS

DURATION: 3 hours

MARKS: 100

pt OPPORTUNITY/ FINAL EXAMINATION - QUESTION PAPER

EXAMINER(S} D Kamotho & S Dzomira

MODERATOR: M Tondota

INSTRUCTIONS

1. Answer ALL questions in blue or black ink only.

2. Read all the questions carefully before answering.

3. Please ensure that your writing is legible, neat and presentable.

4. Start each question on a new page and number the answers clearly.

5. No programmable calculators are allowed .

6. The names of people and businesses used throughout this assessment do not reflect the

reality and may be purely coincidental.

7. Questions relating to the paper may be raised in the initial 30 minutes after the start of

the paper. Thereafter, candidates must use their initiative to deal with any perceived

error or ambiguities & any assumption made by the candidate should be clearly stated.

8. Do not write in pencil and do not use tip-ex, as this will not be marked.

9. SHOW All WORKINGS!

THIS QUESTION PAPER CONSISTS OF 7 PAGES (excluding the front page)

|

|

2 Page 2 |

▲back to top |

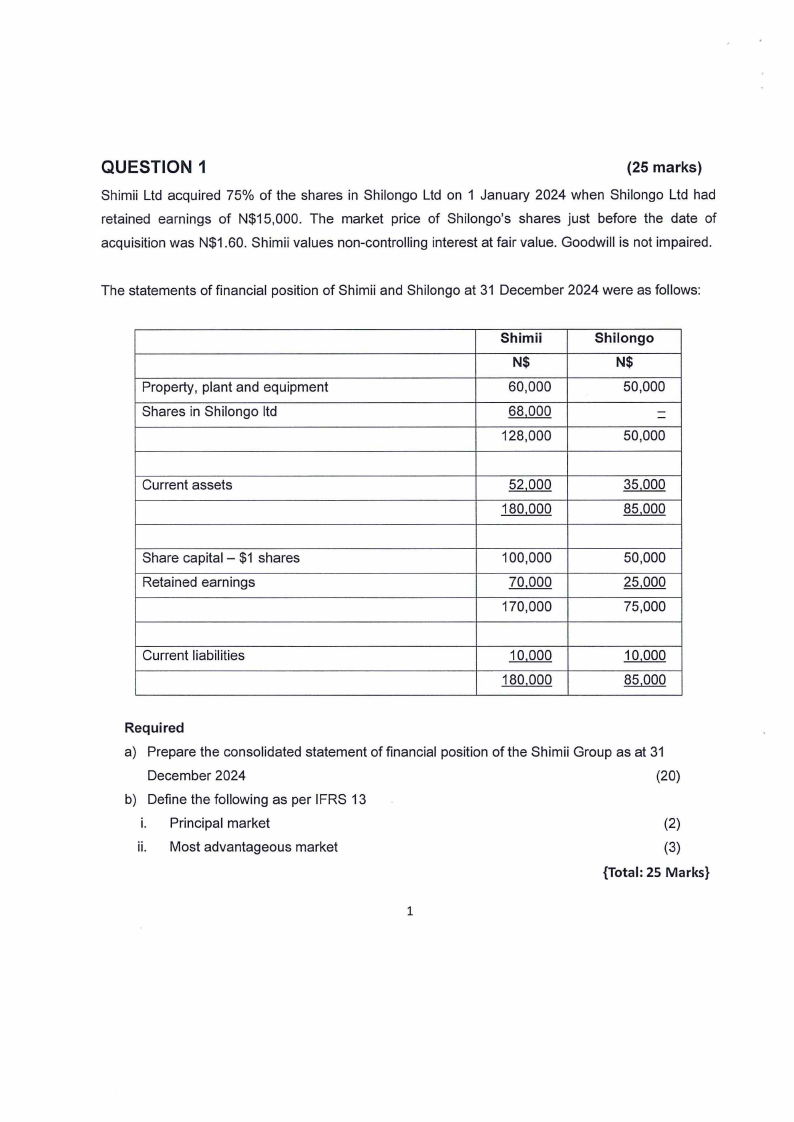

QUESTION 1

(25 marks)

Shimii Ltd acquired 75% of the shares in Shilongo Ltd on 1 January 2024 when Shilongo Ltd had

retained earnings of N$15,000. The market price of Shilongo's shares just before the date of

acquisition was N$1.60. Shimii values non-controlling interest at fair value. Goodwill is not impaired.

The statements of financial position of Shimii and Shilongo at 31 December 2024 were as follows:

Property, plant and equipment

Shares in Shilongo ltd

Shimii

N$

60,000

68,000

128,000

Shilongo

N$

50 ,000

--

50 ,000

Current assets

52,000

180,000

35,000

85,000

Share capital - $1 shares

Retained earnings

100,000

70,000

170,000

50,000

25,000

75,000

Current liabilities

10,000

180,000

10,000

85,000

Required

a) Prepare the consolidated statement of financial position of the Shimii Group as at 31

December 2024

(20)

b) Define the following as per IFRS 13

i. Principal market

(2)

ii. Most advantageous market

(3)

{Total: 25 Marks}

1

|

|

3 Page 3 |

▲back to top |

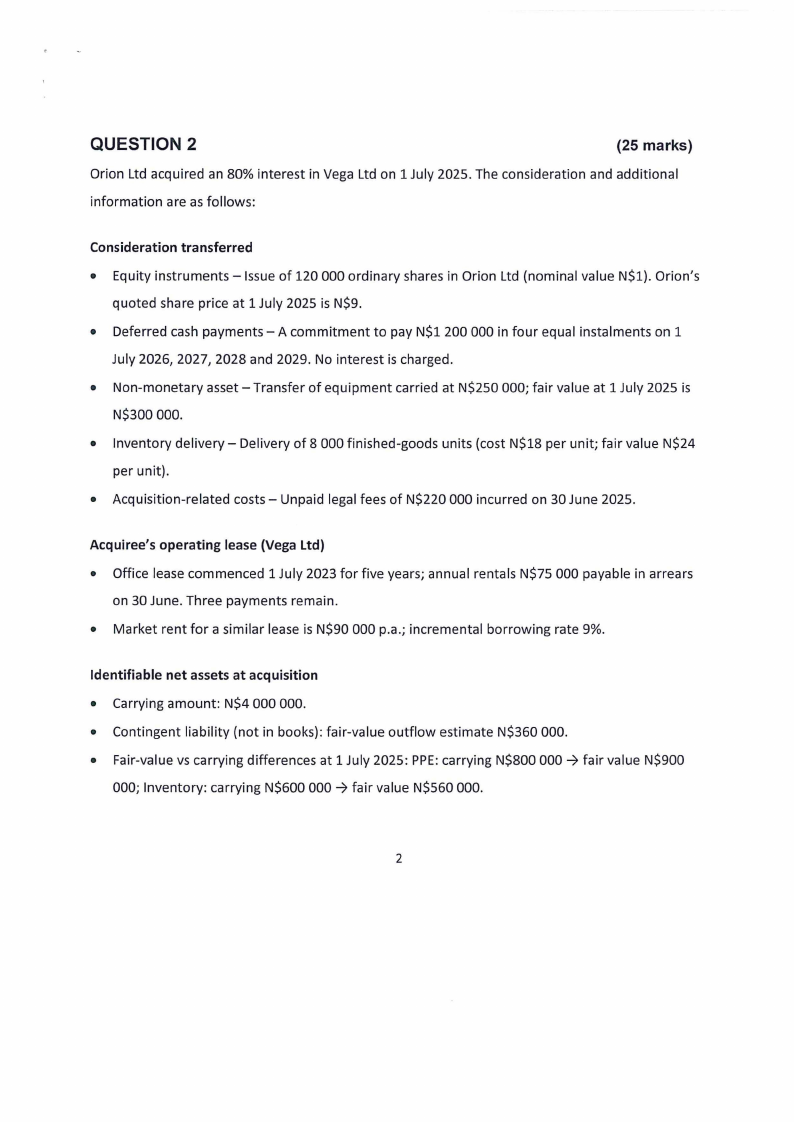

QUESTION 2

(25 marks)

Orion Ltd acquired an 80% interest in Vega Ltd on 1 July 2025. The consideration and additional

information are as follows:

Consideration transferred

• Equity instruments - Issue of 120 000 ordinary shares in Orion Ltd (nominal value N$1). Orion's

quoted share price at 1 July 2025 is N$9.

• Deferred cash payments -A commitment to pay N$1 200 000 in four equal instalments on 1

July 2026, 2027, 2028 and 2029 . No interest is charged .

• Non-monetary asset - Transfer of equipment carried at N$250 000; fair value at 1 July 2025 is

N$300 000.

• Inventory delivery- Delivery of 8 000 finished-goods units (cost N$18 per unit; fair value N$24

per unit).

• Acquisition-related costs - Unpaid legal fees of N$220 000 incurred on 30 June 2025.

Acquiree's operating lease {Vega Ltd}

• Office lease commenced 1 July 2023 for five years; annual rentals N$75 000 payable in arrears

on 30 June. Three payments remain.

• Market rent for a similar lease is N$90 000 p.a.; incremental borrowing rate 9%.

Identifiable net assets at acquisition

• Carrying amount: N$4 000 000.

• Contingent liability (not in books): fair-value outflow estimate N$360 000.

• Fair-value vs carrying differences at 1 July 2025: PPE: carrying N$800 000 ➔ fair value N$900

000; Inventory: carrying N$600 000 ➔ fair value N$560 000.

2

|

|

4 Page 4 |

▲back to top |

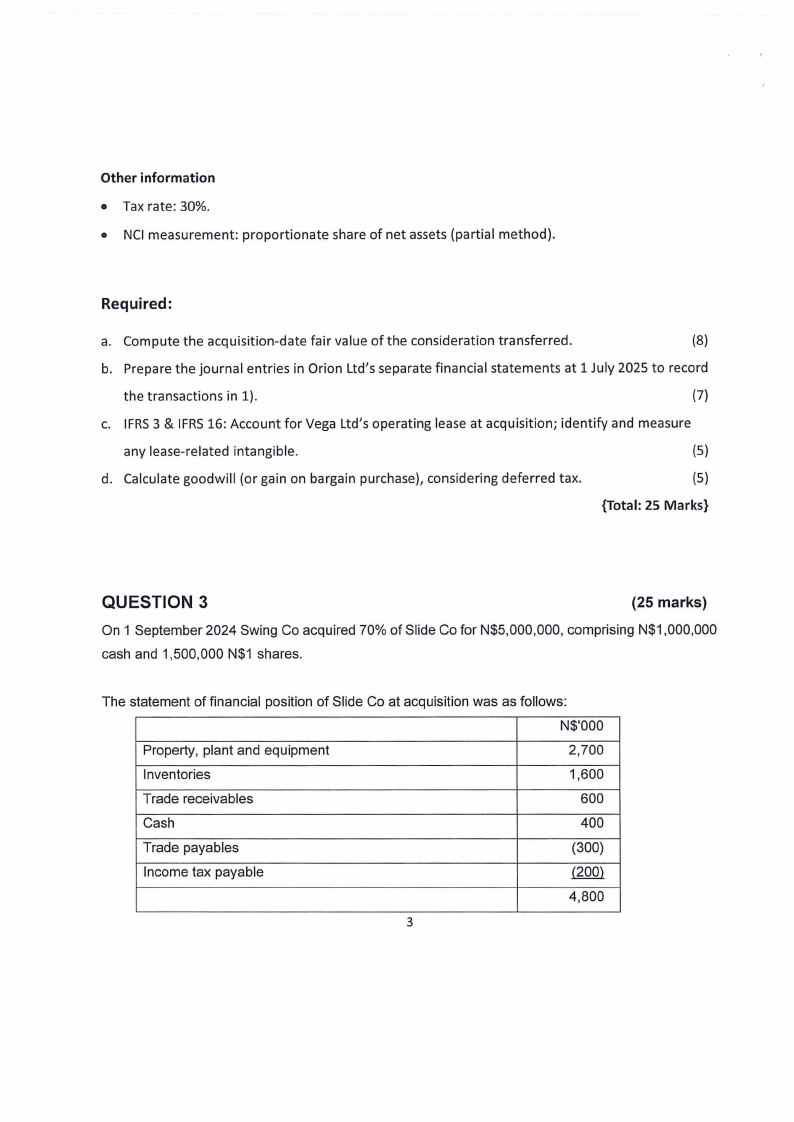

Other information

• Tax rate : 30%.

• NCI measurement: proportionate share of net assets (partial method).

Required:

a. Compute the acquisition-date fair value of the consideration t ransferred .

(8)

b. Prepare the journal entries in Orion Ltd's separate financial statements at 1 July 2025 to record

the transactions in 1).

(7)

c. IFRS 3 & IFRS 16: Account for Vega Ltd's operating lease at acqu isition; identify and measure

any lease-related intangible.

(5)

d. Calculate goodwill (or ga in on bargain purchase), considering deferred tax.

(5)

{Total: 25 Marks}

QUESTION 3

(25 marks)

On 1 September 2024 Swing Co acquired 70% of Slide Co for N$5,000,000, comprising N$1 ,000,000

cash and 1,500,000 N$1 shares.

The statement of financial position of Slide Co at acquisition was as follows:

N$'000

Property, plant and equipment

2,700

Inventories

1,600

Trade receivables

600

Cash

400

Trade payables

(300)

Income tax payable

(200)

4,800

3

|

|

5 Page 5 |

▲back to top |

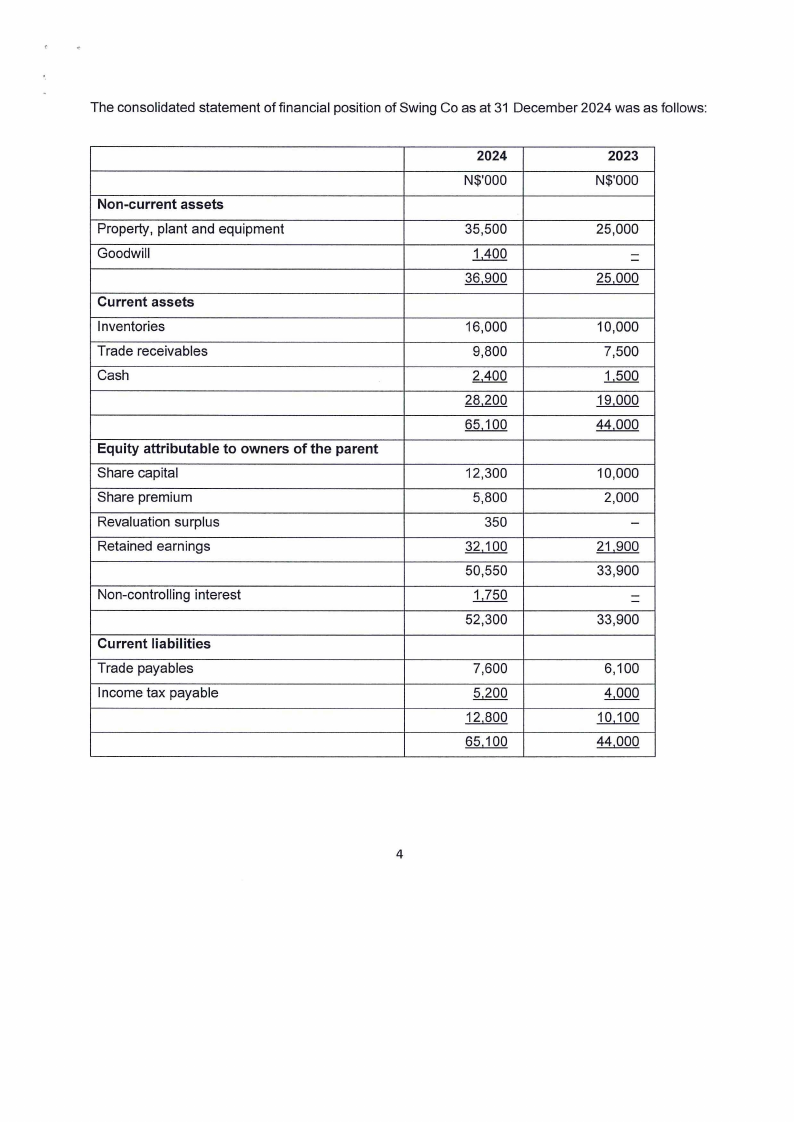

The consolidated statement of financial position of Swing Co as at 31 December 2024 was as follows:

Non-current assets

Property, plant and equipment

Goodwill

Current assets

Inventories

Trade receivables

Cash

Equity attributable to owners of the parent

Share capital

Share premium

Revaluation surplus

Retained earnings

Non-controlling interest

Current liabilities

Trade payables

Income tax payable

2024

N$'000

35,500

1,400

36,900

16,000

9,800

2,400

28,200

65,100

12,300

5,800

350

32,100

50,550

1,750

52,300

7,600

5,200

12,800

65,100

2023

N$'000

25,000

--

25,000

10,000

7,500

1,500

19,000

44,000

10,000

2,000

-

21,900

33,900

--

33,900

6,100

4,000

10,100

44,000

4

|

|

6 Page 6 |

▲back to top |

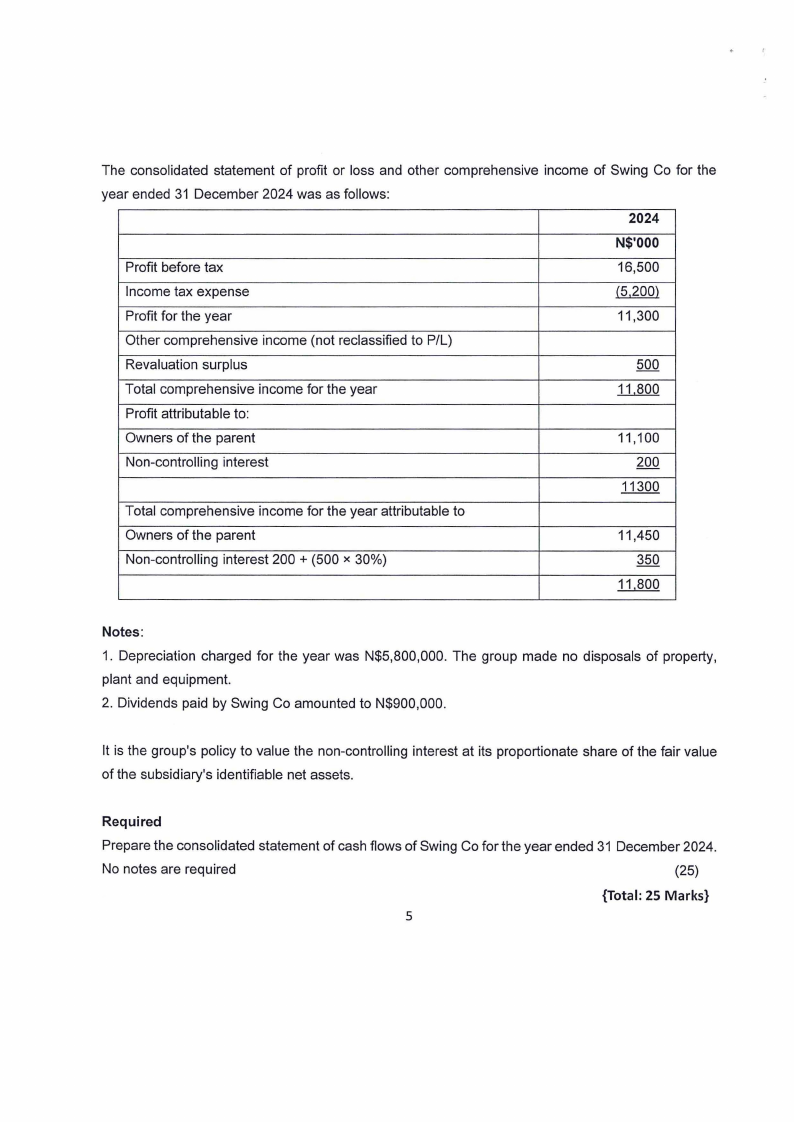

The consolidated statement of profit or loss and other comprehensive income of Swing Co for the

year ended 31 December 2024 was as follows :

2024

N$'000

Profit before tax

16,500

Income tax expense

(5,200}

Profit for the year

11,300

Other comprehensive income (not reclassified to P/L)

Revaluation surplus

500

Total comprehensive income for the year

11,800

Profit attributable to:

Owners of the parent

11,100

Non-controlling interest

200

11300

Total comprehensive income for the year attributable to

Owners of the parent

11,450

Non-controlling interest 200 + (500 x 30%)

350

11,800

Notes:

1. Depreciation charged for the year was N$5,800,000. The group made no disposals of property,

plant and equipment.

2. Dividends paid by Swing Co amounted to N$900,000.

It is the group's policy to value the non-controlling interest at its proportionate share of the fair value

of the subsidiary's identifiable net assets.

Required

Prepare the consolidated statement of cash flows of Swing Co for the year ended 31 December 2024.

No notes are required

(25)

{Total: 25 Marks}

5

|

|

7 Page 7 |

▲back to top |

!

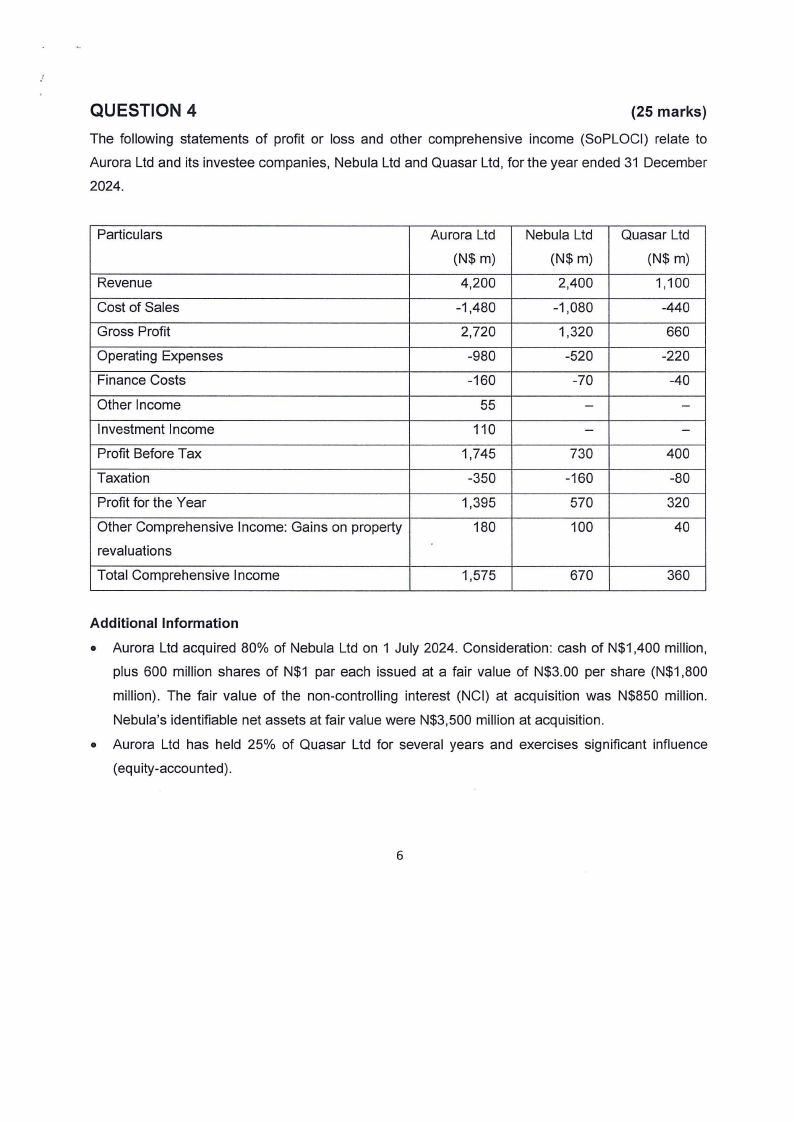

QUESTION 4

(25 marks)

The following statements of profit or loss and other comprehensive income (SoPLOCI) relate to

Aurora Ltd and its investee companies, Nebula Ltd and Quasar Ltd, for the year ended 31 December

2024.

Particulars

Revenue

Cost of Sales

Gross Profit

Operating Expenses

Finance Costs

Other Income

Investment Income

Profit Before Tax

Taxation

Profit for the Year

Other Comprehensive Income: Gains on property

revaluations

Total Comprehensive Income

Aurora Ltd

(N$ m)

4,200

-1,480

2,720

-980

-160

55

110

1,745

-350

1,395

180

1,575

Nebula Ltd

(N$ m)

2,400

-1,080

1,320

-520

-70

-

-

730

-160

570

100

670

Quasar Ltd

(N$ m)

1,100

-440

660

-220

-40

-

-

400

-80

320

40

360

Additional Information

• Aurora Ltd acquired 80% of Nebula Ltd on 1 July 2024. Consideration: cash of N$1,400 million,

plus 600 million shares of N$1 par each issued at a fair value of N$3.00 per share (N$1,800

million). The fair value of the non-controlling interest (NCI) at acquisition was N$850 million.

Nebula's identifiable net assets at fair value were N$3,500 million at acquisition.

• Aurora Ltd has held 25% of Quasar Ltd for several years and exercises significant influence

(equity-accounted).

6

|

|

8 Page 8 |

▲back to top |

• On acquisition, Nebula's property's fair value exceeded carrying amount by N$120 million.

Remaining useful life: 20 years . Additional depreciation related to this fair value step-up is charged

to cost of sales.

• During the post-acquisition period, Nebula sold goods to Aurora for N$80 million at a profit margin

of 25% on selling price. Thirty percent (30%) of these goods remained in Aurora's closing

inventory at year-end .

• Aurora provides management services to Nebula for an annual fee of N$5 million, recognised by

Aurora in "Other income" and by Nebula as part of "Operating expenses". The fee accrues evenly

throughout the year.

• Goodwill was tested for impairment at year-end; an impairment loss of N$60 million is recognised

in group operating expenses.

• All revaluation gains were recorded in the post-acquisition period. Unless otherwise stated,

income and expenses accrued evenly throughout the year.

Required:

a. Calculate:

(i) The goodwill arising on the acquisition of Nebula Ltd by Aurora Ltd; and

(ii) The amount of goodwill that should appear in the consolidated Statement of Financial

Position as at 31 December 2024.

(5)

b. Prepare the Consolidated Statement of Profit or Loss and Other Comprehensive Income for the

Aurora Group for the year ended 31 December 2024, showing the composition of your figures.

(20)

{Total: 25 Marks}

END OF QUESTION PAPER

7