|

FMG620S - FINANCIAL MANAGEMENT FOR NATURE CONSERVATION - 1ST OPP -NOV 2022 |

|

|

1 Page 1 |

▲back to top |

n Am I BI A u n IVER s I TY

OF SCIEnCE Ano TECHnOLOGY

FACULTY OF HEALTH, NATURAL RESOURCES AND APPLIED SCIENCES

DEPARTMENT OF AGRICULTURE AND NATURAL RESOURCES SCIENCES

QUALIFICATION: BACHELOROF NATURALRESOURCEMSANAGEMENT(NATURECONSERVATION)

QUALIFICATION CODE: 07BNRS

COURSE CODE: FMG620S

LEVEL: 6

COURSE NAME: FINANCIALMANAGEMENTFORNATURE

CONSERVATION

DATE: NOVEMBER 2022

DURATION: 3 HOURS

MARKS: 100

FIRST OPPORTUNITY EXAMINATION QUESTION PAPER

EXAMINER(S)

M LUBINDA

MODERATOR:

S KALUNDU

INSTRUCTIONS

1. Answer ALL the questions.

2. Write clearly and neatly.

3. Number the answers clearly.

PERMISSIBLE MATERIALS

1. Examination question paper

2. Answering book

3. Calculator

THIS QUESTION PAPER CONSISTS OF 4 PAGES (Excluding this front page)

|

|

2 Page 2 |

▲back to top |

Financial Management

FMG620S

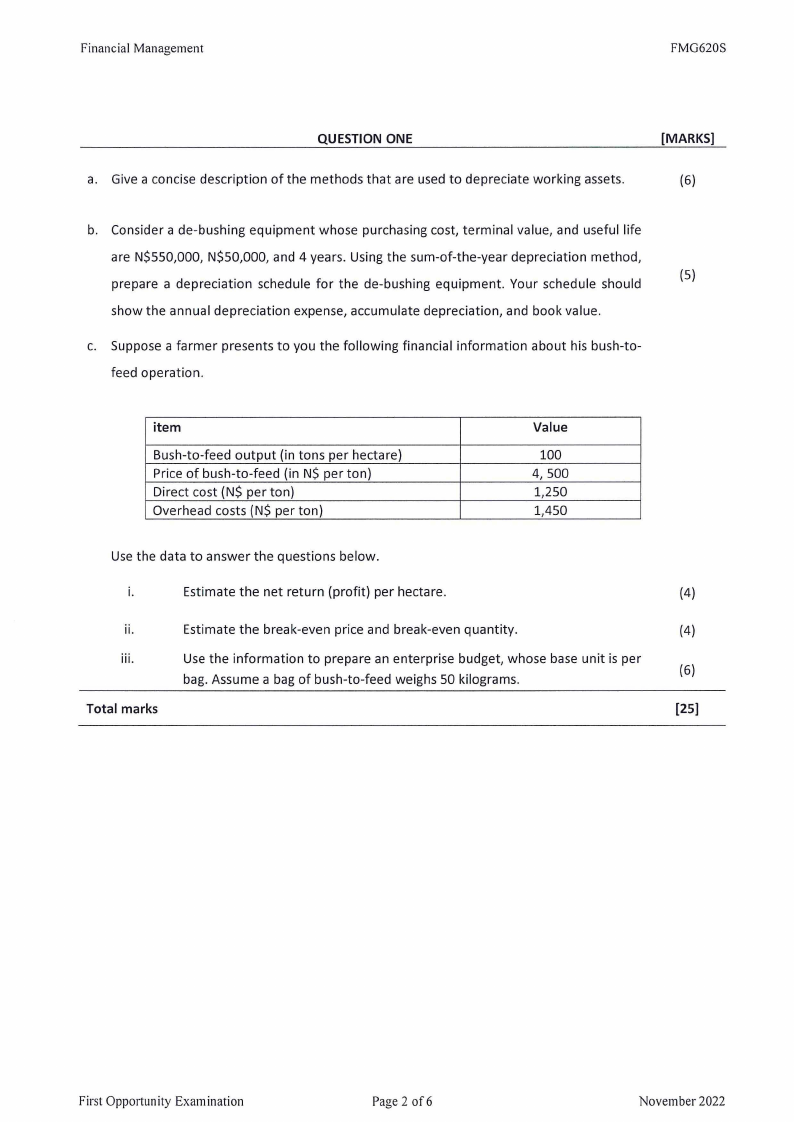

QUESTION ONE

a. Give a concise description of the methods that are used to depreciate working assets.

[MARKS]

(6)

b. Consider a de-bushing equipment whose purchasing cost, terminal value, and useful life

are N$550,000, N$50,000, and 4 years. Using the sum-of-the-year depreciation method,

prepare a depreciation schedule for the de-bushing equipment. Your schedule should

(S)

show the annual depreciation expense, accumulate depreciation, and book value.

c. Suppose a farmer presents to you the following financial information about his bush-to-

feed operation.

item

Bush-to-feed output (in tons per hectare)

Price of bush-to-feed (in N$ per ton)

Direct cost (N$ per ton)

Overhead costs (N$ per ton)

Value

100

4,500

1,250

1,450

Use the data to answer the questions below.

i.

Estimate the net return (profit) per hectare.

(4)

ii.

Estimate the break-even price and break-even quantity.

(4)

iii.

Use the information to prepare an enterprise budget, whose base unit is per

bag. Assume a bag of bush-to-feed weighs 50 kilograms.

(6)

Total marks

[25)

First Oppo11unityExamination

Page 2 of6

November 2022

|

|

3 Page 3 |

▲back to top |

Financial Management

FMG620S

QUESTION TWO

[MARKS]

a. Give a concise description of the double entry system.

(5)

b. The accompanying table shows scrambled income statement and balance sheet

accounts for Conservancy for the year ended December 31, 2019.

Item

Sales revenue

Accounts payable

Accounts receivable

Marketing expense

Common stock

Accumulated Depreciation

Capital gain

Buildings and equipment

Cash

Cost of goods sold

Depreciation expense

General and administration

Inventories

Land

Long-term debts

Miscellaneous expenses

Interest expense

Notes payable

Equipment

Taxes

Retained earnings

Accruals

expenses

Value (N$),

December 31,

2019

160,000

22,000

25,000

16,000

32,000

32,000

7,500

90,000

1,500

106,000

10,000

10,000

45,500

26,000

94,450

1,000

6,100

47,000

116,000

4,360

26,550

50,000

i. Use the appropriate accounts to prepare an income statement for Conservancy for

the year ended December 31, 2019. The income statement should show all the

(lO)

relevant sections.

ii. Use the appropriate accounts to prepare a balance sheet for Conservancy for the

year ended December 31, 2019. The income statement should show all the relevant

(10)

sections.

TOTAL MARKS

[25]

First Opportunity Examination

Page 3 of6

November 2022

|

|

4 Page 4 |

▲back to top |

Financial Management

FMG620S

QUESTION THREE

[MARKS]

a. Suppose you have been asked to give a talk on financial statements to members of a

conservancy. Based on what you have learned in this course, what would be the main

(S}

points in your presentation?

b. A Community Forest recorded sales of N$60,000 in September. For the months of

October through December, Community Forest forecasts sales of N$70,000 per

month. At the beginning of October, the Community Forest had a cash balance of

N$30,000. Additional information about the timing of the cash receipts and payments

for Community Forest are as follows:

• The Community Forest receives 80% of its sales in cash and collects the

remaining 20% in the following month.

• Expected monthly cash purchases are estimated at N$45,000 for October

through December.

• Other monthly expenses are estimated at 20% of the current month's sales.

• A loan repayment of N$43,000 is due in November.

• A N$26,000 cash purchase of equipment is expected in October.

Using the information provided above, prepare a cash flow budget for Glen Enterprise

for the months of October, November, and December. Furthermore, based on the cash

flow budget you have prepared, estimate the cash deficit/surplus that is expected to

{20}

be experienced by the Community Forest during the period October to December.

TOTAL MARKS

[25]

First Oppo11unity Examination

Page 4 of6

November 2022

|

|

5 Page 5 |

▲back to top |

Financial Management

FMG620S

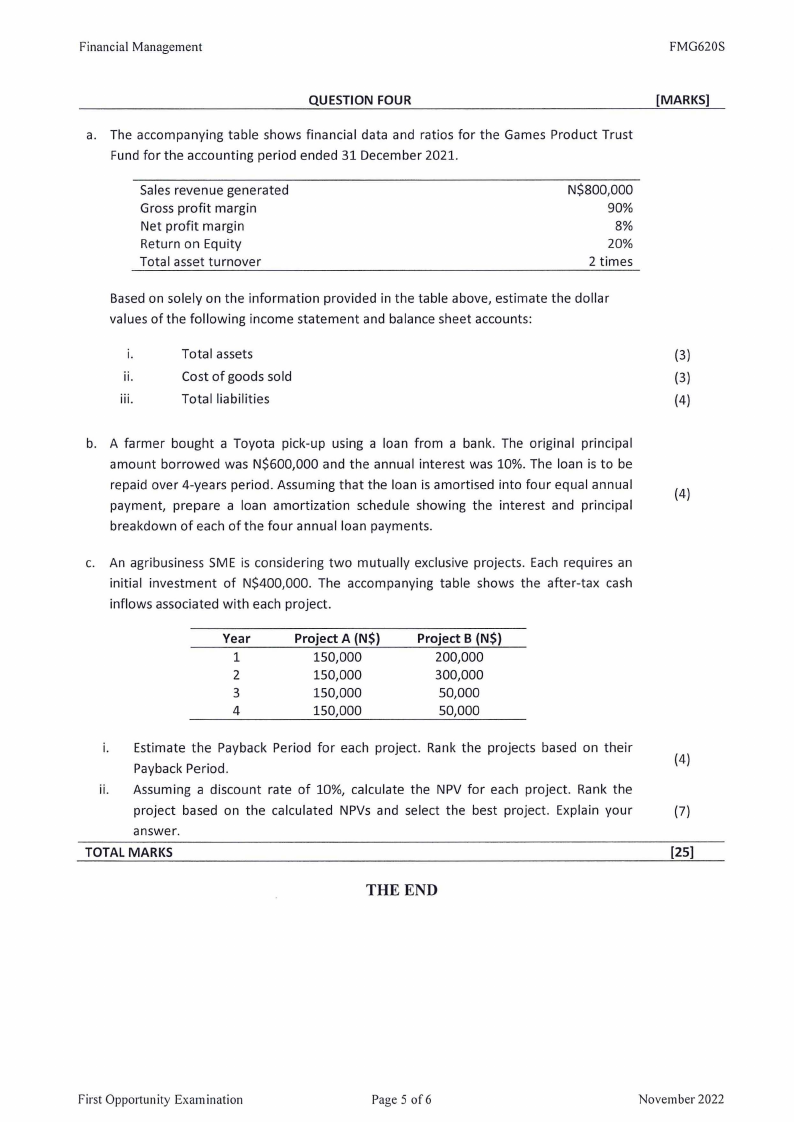

QUESTION FOUR

[MARKS]

a. The accompanying table shows financial data and ratios for the Games Product Trust

Fund for the accounting period ended 31 December 2021.

Sales revenue generated

Gross profit margin

Net profit margin

Return on Equity

Total asset turnover

N$800,000

90%

8%

20%

2 times

Based on solely on the information provided in the table above, estimate the dollar

values of the following income statement and balance sheet accounts:

i.

Total assets

(3)

ii.

Cost of goods sold

(3)

iii.

Total liabilities

(4)

b. A farmer bought a Toyota pick-up using a loan from a bank. The original principal

amount borrowed was N$600,000 and the annual interest was 10%. The loan is to be

repaid over 4-years period. Assuming that the loan is amortised into four equal annual

(4)

payment, prepare a loan amortization schedule showing the interest and principal

breakdown of each of the four annual loan payments.

c. An agribusiness SME is considering two mutually exclusive projects. Each requires an

initial investment of N$400,000. The accompanying table shows the after-tax cash

inflows associated with each project.

Year

1

2

3

4

Project A {N$)

150,000

150,000

150,000

150,000

Project B {N$)

200,000

300,000

50,000

50,000

i. Estimate the Payback Period for each project. Rank the projects based on their

Payback Period.

(4)

ii. Assuming a discount rate of 10%, calculate the NPV for each project. Rank the

project based on the calculated NPVs and select the best project. Explain your

(7)

answer.

TOTAL MARKS

(25]

THE END

First Opportunity Examination

Page 5 of6

November 2022

|

|

6 Page 6 |

▲back to top |

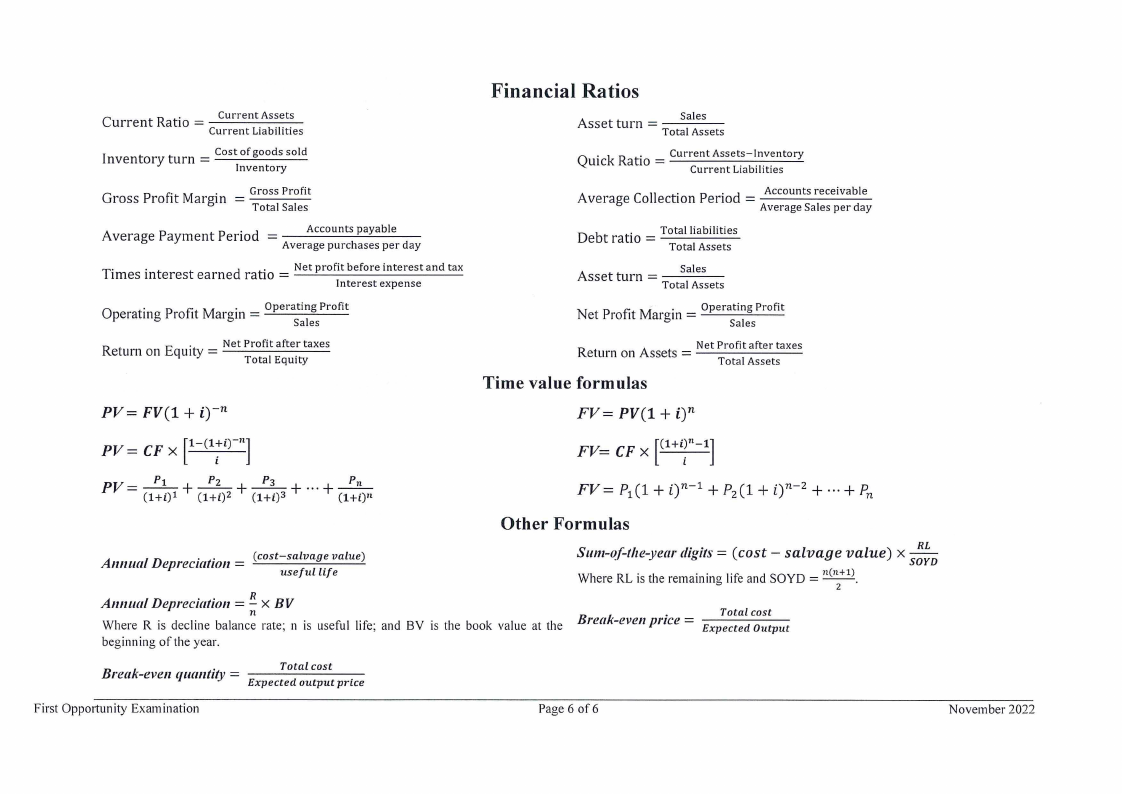

Current Ratio = Current Assets

Current Liabilities

Inventory turn = Cost of goods sold

Inventory

Gross Profit Margin = Gross Profit

Total Sales

Average Payment Period =

Accounts payable

Average purchases per day

Times interest earned ratio = Net profit before interest and tax

Interest expense

Operating Profit Margin = Operating Profit

Sales

Return on Equity = Net Profit after taxes

Total Equity

PV= FV(l + i)-n

PV = CF x [1-c1;0-"]

Financial Ratios

Sales

Asset turn = Total Assets

Current Assets-Inventory

Quick Ratio = current Liabilities

A verage

Co IIec t 1. 0n

p eno.

d

=

Accounts receivable

Average Sales per day

De btrat10.

Total liabilities

= -----

Total Assets

Sales

Asset turn=---

Total Assets

. Operating Profit

Net Profit Margm = ---~--

Sales

R eturn

on A ssets

=

-N--e-t--PTrootfailt

after taxes

Assets

Time value formulas

FV= PV(l + i)n

FV= CF x [(1+1i]t-

+ + + ...+ PV- P1

- (l+i)l

Pz

(l+i)Z

P3

(l+i)3

Pn

(l+i)"

FV= Pi(l + 0n-1 + P2(l + 0n-2 + ...+ Pn

Other Formulas

= Annual Depreciation (cost-salvage value)

useful life

A1111uaD/ epreciation = !n!.x BV

Where R is decline balance rate; n is useful life; and BY is the book value at the

beginning of the year.

Sum-of-the-year digits= (cost - salvage value) x __!!!:_

SOYD

Where RL is the remaining life and SOYD = n(n+l)_

2

= Total cost

Break-even price Expected Output

= Break-even quantit.y

Total cost

Expected output price

First Oppo1iunity Examination

Page 6 of6

November 2022