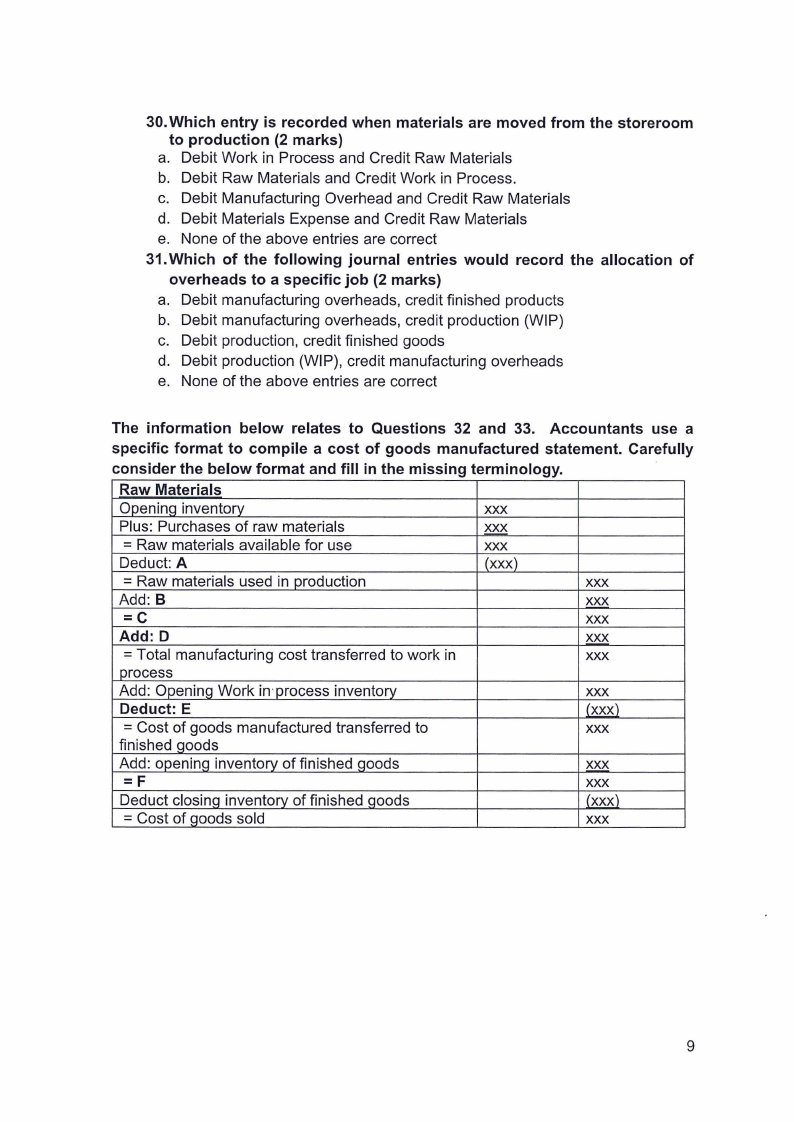

44. Based on question 43, calculate the under or over-allocation of

overheads (1 mark)

a. N$3,456 Over-allocated

b. N$3,456 under-allocated

c. N$3,500 under- allocated

d. N$3,500 over-allocated

e. None of the above

45.A company produces three types of products- product A, product Band

product C. Product A requires 200 machine hours. Product B requires

400 machine hours. Product C requires 620 machine hours. The

company uses machine hours as a cost driver. The total overhead cost

assigned to that cost pool was $183,000. The machine hours overhead

assigned to each of the products were (3 marks):

a. N$61,000 for A; N$61,000 for B; N$61,000 for C

b. N$61,000 for A; N$30,500 for B; N$91,500 for C

c. N$30,000 for A; N$60,000 for B; N$93,000 for C

d. N$30,000 for A; N$63,000 for B; N$90,000 for C

e. None of the above

The following information relates to Questions 46 to 51. These balances were obtained

from the company's records for the year ended 30 June 2024:

Raw material (1 July 2023)

380,000

Raw material (30 June 2024)

396,000

Work in process (1 July 2023)

270,000

Work in process (30 June 2024)

248,000

Finished Goods (1 July 2023)

280,000

Finished Goods (30 June 2024)

400,000

Raw Material purchased

700,000

Direct labour

400,000

Indirect labour

156,000

Factory ManaQers' salary

216,000

Other Factory overheads

209,000

Indirect material used

46,000

Selling and administrative costs

108,000

46. Use the above information and calculate the prime cost (3 marks)

a. N$1,084,000

b. N$1,080,000

c. N$780,000

d. N$700,000

e. None of the above

47. Use the above information and calculate the period cost (1 mark)

a. N$209,000

b. N$46,000

c. N$108,000

d. N$156,000

e. None of the above

13