|

CMA611S-COST AND MANAGEMENT ACCOUNTING 201-2ND OPP-JULY 2025 |

|

|

1 Page 1 |

▲back to top |

nAmlBIA UnlVERSITY

OF SCIEnCE Ano TECHnOLOGY

FACULTY OF COMMERCE, HUMAN SCIENCESAND EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING AND FINANCE

QUALIFICATION: BACHELOR OF ACCOUNTING

QUALIFICATION CODE: 07BGAC

LEVEL: 6

COURSE CODE: CMA611S

COURSE NAME: COST& MANAGEMENT ACCOUNTING201

SESSION: JULY2025

DURATION: 3 HOURS

PAPER: THEORYAND CALCULATIONS

MARKS: 100

SECOND OPPORTUNITY EXAMINATION QUESTION PAPER

EXAMINERS

Mrs Modestus, M., Ms Mkhulisi, M., Ms Shikoyeni, F .and Mr Sheehama, K.G.H.

MODERATOR Ms Kangala, H.

INSTRUCTIONS

• Answer ALL the questions in blue or black ink only. NO PENCIL.

• Start each question on a new page, number the answers correctly and clearly.

• Write clearly, and neatly showing all your workings/assumptions.

• Work with at least four (4) decimal places in all your calculations and only round off final

answers to two (2) decimal places.

• Questions relating to this examination may be raised in the initial 30 minutes after the

start of the examination. Thereafter, candidates must use their initiative to deal with any

perceived errors or ambiguities and any assumptions made by the candidate should be

clearly stated.

PERMISSIBLE MATERIALS

• Silent, non-programmable calculators

THIS QUESTION PAPER CONSISTS OF_ 4_ PAGES (excluding this front page)

0

|

|

2 Page 2 |

▲back to top |

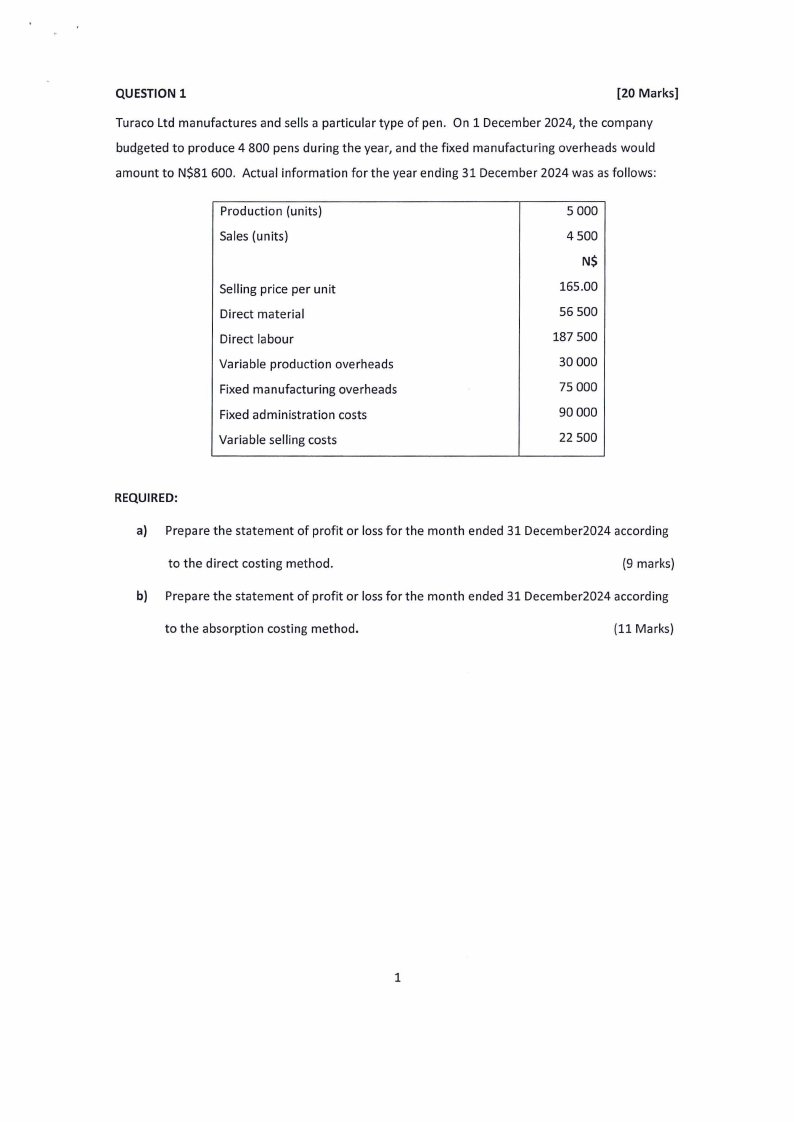

QUESTION 1

[20 Marks]

Turaco Ltd manufactures and sells a particular type of pen. On 1 December 2024, the company

budgeted to produce 4 800 pens during the year, and the fixed manufacturing overheads would

amount to N$81 600. Actual information for the year ending 31 December 2024 was as follows:

Production (units)

Sales (units)

Selling price per unit

Direct material

Direct labour

Variable production overheads

Fixed manufacturing overheads

Fixed administration costs

Variable selling costs

5 000

4 500

N$

165.00

56 500

187 500

30 000

75 000

90 000

22 500

REQUIRED:

a) Prepare the statement of profit or loss for the month ended 31 December2024 according

to the direct costing method.

(9 marks)

b) Prepare the statement of profit or loss for the month ended 31 December2024 according

to the absorption costing method.

(11 Marks)

1

|

|

3 Page 3 |

▲back to top |

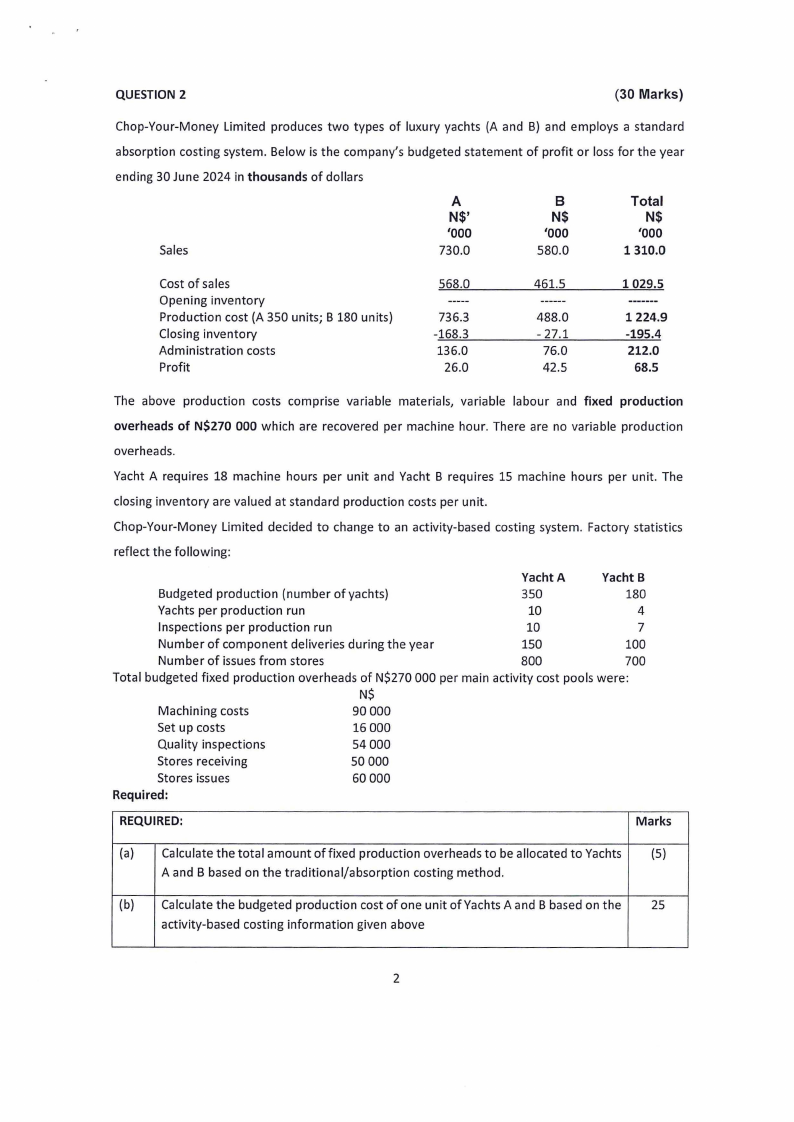

QUESTION 2

(30 Marks)

Chop-Your-Money Limited produces two types of luxury yachts (A and B) and employs a standard

absorption costing system. Below is the company's budgeted statement of profit or loss for the year

ending 30 June 2024 in thousands of dollars

Sales

A

N$'

'000

730.0

B

N$

'000

580.0

Total

N$

'000

1310.0

Cost of sales

Opening inventory

Production cost (A 350 units; B 180 units)

Closing inventory

Administration costs

Profit

568.0

736.3

-168.3

136.0

26.0

461.5

488.0

- 27.1

76.0

42.5

1029.5

1224.9

-195.4

212.0

68.5

The above production costs comprise variable materials, variable labour and fixed production

overheads of N$270 000 which are recovered per machine hour. There are no variable production

overheads.

Yacht A requires 18 machine hours per unit and Yacht B requires 15 machine hours per unit. The

closing inventory are valued at standard production costs per unit.

Chop-Your-Money Limited decided to change to an activity-based costing system. Factory statistics

reflect the following:

Yacht A

Yacht B

Budgeted production (number of yachts)

350

180

Yachts per production run

10

4

Inspections per production run

10

7

Number of component deliveries during the year

150

100

Number of issues from stores

800

700

Total budgeted fixed production overheads of N$270 000 per main activity cost pools were:

N$

Machining costs

90000

Set up costs

16000

Quality inspections

54000

Stores receiving

50000

Stores issues

60 000

Required:

REQUIRED:

Marks

(a) Calculate the total amount offixed production overheads to be allocated to Yachts (5)

A and B based on the traditional/absorption costing method.

(b) Calculate the budgeted production cost of one unit of Yachts A and B based on the

25

activity-based costing information given above

2

|

|

4 Page 4 |

▲back to top |

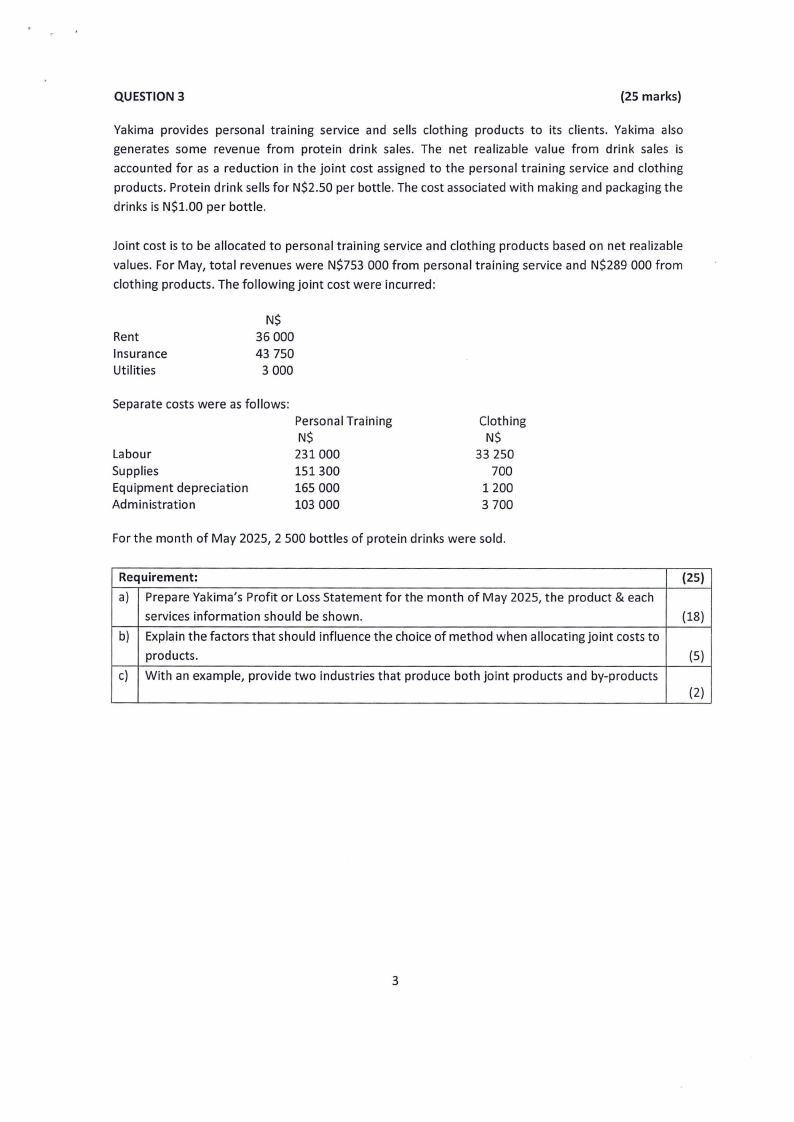

QUESTION 3

{25 marks)

Yakima provides personal training service and sells clothing products to its clients. Yakima also

generates some revenue from protein drink sales. The net realizable value from drink sales is

accounted for as a reduction in the joint cost assigned to the personal training service and clothing

products. Protein drink sells for N$2.50 per bottle. The cost associated with making and packaging the

drinks is N$1.00 per bottle.

Joint cost is to be allocated to personal training service and clothing products based on net realizable

values. For May, total revenues were N$753 000 from personal training service and N$289 000 from

clothing products. The following joint cost were incurred:

Rent

Insurance

Utilities

N$

36 000

43 750

3 000

Separate costs were as follows:

Personal Training

N$

Labour

231000

Supplies

151300

Equipment depreciation

165 000

Administration

103 000

Clothing

N$

33 250

700

1200

3 700

For the month of May 2025, 2 500 bottles of protein drinks were sold.

Requirement:

(25)

a) Prepare Yakima's Profit or Loss Statement for the month of May 2025, the product & each

services information should be shown.

(18)

b) Explain the factors that should influence the choice of method when allocating joint costs to

products.

(5)

c) With an example, provide two industries that produce both joint products and by-products

(2)

3

|

|

5 Page 5 |

▲back to top |

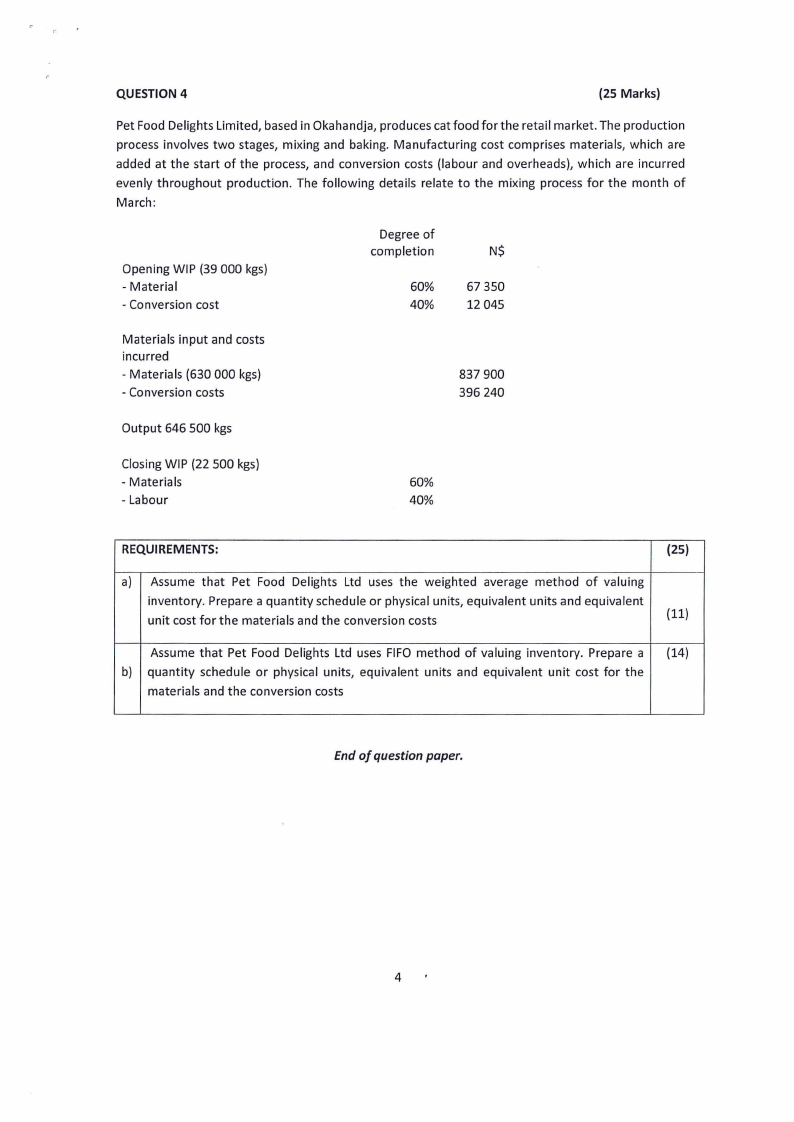

QUESTION 4

(25 Marks)

Pet Food Delights Limited, based in Okahandja, produces cat food for the retail market. The production

process involves two stages, mixing and baking. Manufacturing cost comprises materials, which are

added at the start of the process, and conversion costs (labour and overheads), which are incurred

evenly throughout production. The following details relate to the mixing process for the month of

March:

Opening WIP (39 000 kgs)

- Material

- Conversion cost

Degree of

completion

60%

40%

N$

67 350

12 045

Materials input and costs

incurred

- Materials (630 000 kgs)

- Conversion costs

837 900

396 240

Output 646 500 kgs

Closing WIP (22 500 kgs)

- Materials

- Labour

60%

40%

REQUIREMENTS:

(25)

a) Assume that Pet Food Delights Ltd uses the weighted average method of valuing

inventory. Prepare a quantity schedule or physical units, equivalent units and equivalent

unit cost for the materials and the conversion costs

(11)

Assume that Pet Food Delights Ltd uses FIFO method of valuing inventory. Prepare a (14)

b) quantity schedule or physical units, equivalent units and equivalent unit cost for the

materials and the conversion costs

End of question paper.

4