|

FAR811S-ADVANCED FINANCIAL ACCOUNTING AND REPORTING-2ND OPP-JULY 2025 |

|

|

1 Page 1 |

▲back to top |

nAmlBIA unlVERSITY

OF SCIEn CE Ano TECHn OLOGY

FACULTY OF COMMERCE, HUMAN SCIENCESAND EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING AND FINANCE

QUALIFICATION : BACHELOR OF ACCOUNTING HONOURS

QUALIFICATION CODE: 08 BOAH

COURSE CODE: FAR811S

SESSION: July 2025

LEVEL: 8

COURSE NAME: ADVANCEDFINANCIALACCOUNTING

AND REPORTING

PAPER: THEORYAND CALCULATIONS

DURATION: 3 hours

MARKS: 100

EXAMINER(S)

SUPPLEMENTARY ASSESSMENT- 2nd Opportunity

D W Kamotho

MODERATOR: Dr E Wealth

INSTRUCTIONS

1. Answer ALL questions in blue or black ink only.

2. Write clearly and neatly.

3. Start each question on a new page and number the answers clearly.

4. No programmable calculators are allowed.

5. Questions relating to the paper may be raised in the initial 30 minutes after the start of

the paper. Thereafter, candidates must use their initiative to deal with any perceived

error or ambiguities & any assumption made by the candidate should be clearly stated.

6. Any resemblance to any people, places, organisations or anything is purely

coincidental.

THIS QUESTION PAPER CONSISTS OF 5 PAGES (excluding the front page)

|

|

2 Page 2 |

▲back to top |

Question 1

40 marks

This question consists of four independent parts. For each scenario, advise the lessor on

the accounting treatment in accordance with IFRS 16. Support your responses with

detailed journal entries where appropriate.

(a) Finance Lease

Alpha Limited, a lessor of industrial machinery, entered into a lease agreement on 1 January

2021 with Beta Corp. The lease has a term of 5 years and transfers substantially all the risks

and rewards of ownership. The present value of the lease payments is $800,000, while the

fair value of the machine is N$850,000. Alpha's carrying amount of the machine is

N$750,000. In addition, at the end of the lease, Beta Corp has a bargain purchase option

with an exercise price of N$50,000. Annual lease payments of N$180,000 are payable at the

beginning of each year.

Advise Alpha on:

- The classification of the lease under IFRS 16.

- The initial measurement of the lease receivable and derecognition of the underlying asset;

and

- The subsequent accounting treatment, including recognition of interest income.

Illustrate your responses with appropriate journal entries.

(10 marks)

(b) Operating Lease Modification

Gamma Ltd is a lessor that originally entered into an operating lease on 1 July 2021 for

office equipment with Delta Inc. The lease was for 4 years with fixed annual payments of

N$100,000. In 2022, due to changed market conditions, Gamma and Delta agree to modify

the contract so that Delta will pay N$120,000 per year for the remaining 3 years, and the

lease term is extended by one additional year.

Explain how Gamma should account for this modification under IFRS 16. In your answer,

address:

- The impact on the measurement of the lease receivable and any reclassification; and

- The journal entries necessary to reflect the modification.

(10 marks)

(c) Sale and Leaseback Transaction

On 31 December 2021, Omega Ltd sold a piece of land for N$1,200,000. Simultaneously,

Omega entered into a leaseback arrangement to lease the land for 10 years. At the date of

the transaction, the fair value of the land was N$1,300,000, and Omega carried the land at

N$1,000,000. The leaseback is classified as an operating lease.

1

|

|

3 Page 3 |

▲back to top |

Advise Omega on:

- The accounting treatment for the sale and leaseback under IFRS 16;

- How to measure any gain or loss on the sale; and

- The subsequent recognition of lease payments, including any adjustments.

Include the relevant journal entries.

(12 marks)

(d) Variable Lease Payments and Initial Direct Costs

On 1 October 2021, Zeta Leasing entered into an operating lease for a fleet of vehicles for

a period of 3 years. The contract includes variable lease payments based on the

customer's usage levels. Although the estimated annual lease payment is N$50,000 on

average, actual usage in the first year resulted in a payment of N$60,000. Zeta also

incurred initial direct costs of N$20,000 to secure the contract.

Explain how Zeta should:

- Account for the variable lease payments; and

- Treat the initial direct costs in accordance with IFRS 16.

Illustrate your answer with the necessary journal entries.

(8 marks)

Note. Mark a/locations are indicated against each part (Total = 40 marks).

2

|

|

4 Page 4 |

▲back to top |

Question 2

30 marks

This questions contains four independent parts. For each part, provide clear explanations

and, where applicable, illustrative examples or journal entries to support your discussion.

Your answers should reflect a deep understanding of the Conceptual Framework 2018 and

its practical implications in financial reporting.

(a) Objective of Financial Reporting

Explain the primary objective of financial reporting as set out in the Conceptual Framework

2018. In your answer, discuss how this objective supports the decision-making needs of

users and the role that financial reports play in providing information about an entity's

performance, position, and cash flows.

(5 marks)

(b) Qualitative Characteristics of Financial Information

XYZ Ltd is considering redesigning its financial reporting presentation to improve its

comparability with its peers. Using the Conceptual Framework 2018, discuss the

fundamental and enhancing qualitative characteristics of financial information. Explain how

each characteristic is relevant to achieving comparability and overall usefulness of financial

reports.

(10 marks)

(c) Materiality, Faithful Representation, and Recognition Decisions

ABC Ltd is evaluating whether to capitalize a significant cost related to the development of a

new product line.

(i) Explain how the concepts of materiality and faithful representation, as described in the

Conceptual Framework 2018, influence recognition and measurement decisions.

(ii) Discuss the factors ABC Ltd should consider when deciding whether to expense or

capitalize the cost, supporting your answer with reference to the qualitative characteristics

and the overall objective of financial reporting.

(10 marks)

(d) Definitions of Assets, Liabilities, and Related Challenges

The Conceptual Framework 2018 provides definitions for assets and liabilities. Critically

evaluate these definitions by:

(i) Summarising the key elements that constitute an asset and a liability;

(ii) Using a hypothetical sale and leaseback transaction, explain one potential challenge

that may arise when applying these definitions in practice; and

(iii) Suggest any improvements or clarifications that might be needed in the definitions to

enhance their application.

(5 marks)

Note. Mark a/locations are indicated against each part (Total = 30 marks).

3

|

|

5 Page 5 |

▲back to top |

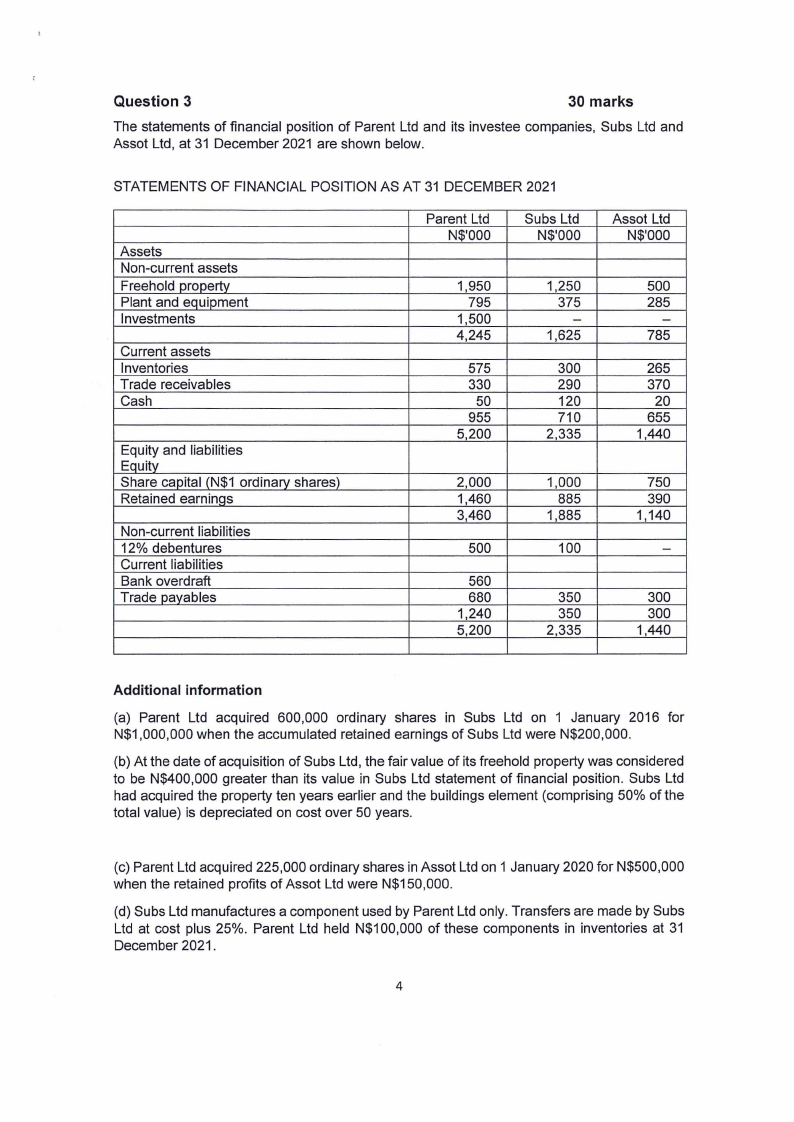

Question 3

30 marks

The statements of financial position of Parent Ltd and its investee companies, Subs Ltd and

Assot Ltd, at 31 December 2021 are shown below.

STATEMENTS OF FINANCIAL POSITION AS AT 31 DECEMBER 2021

Assets

Non-current assets

Freehold property

Plant and equipment

Investments

Current assets

Inventories

Trade receivables

Cash

Equity and liabilities

Equity

Share capital (N$1 ordinary shares)

Retained earninas

Non-current liabilities

12% debentures

Current liabilities

Bank overdraft

Trade pavables

Parent Ltd

N$'000

Subs Ltd

N$'000

1,950

795

1,500

4,245

575

330

50

955

5 200

1,250

375

-

1,625

300

290

120

710

2,335

2,000

1 460

3,460

500

560

680

1,240

5,200

1,000

885

1,885

100

350

350

2,335

Assot Ltd

N$'000

500

285

-

785

265

370

20

655

1,440

750

390

1,140

-

300

300

1,440

Additional information

(a) Parent Ltd acquired 600,000 ordinary shares in Subs Ltd on 1 January 2016 for

N$1,000,000 when the accumulated retained earnings of Subs Ltd were N$200,000.

(b) At the date of acquisition of Subs Ltd, the fair value of its freehold property was considered

to be N$400,000 greater than its value in Subs Ltd statement of financial position. Subs Ltd

had acquired the property ten years earlier and the buildings element (comprising 50% of the

total value) is depreciated on cost over 50 years.

(c) Parent Ltd acquired 225,000 ordinary shares in Assot Ltd on 1 January 2020 for N$500,000

when the retained profits of Assot Ltd were N$150,000.

(d) Subs Ltd manufactures a component used by Parent Ltd only. Transfers are made by Subs

Ltd at cost plus 25%. Parent Ltd held N$100,000 of these components in inventories at 31

December 2021.

4

|

|

6 Page 6 |

▲back to top |

(e) It is the policy of Parent Ltd to review goodwill for impairment annually. The goodwill in

Subs Ltd was written off in full some years ago. An impairment test conducted at the year-end

revealed impairment losses on the investment in Asset Ltd of N$92,000.

(f) It is the group's policy to value the non-controlling interest at acquisition at fair value. The

market price of the shares of the non-controlling shareholders just before the acquisition was

N$1.65.

REQUIRED

MARKS

a

Prepare, in a format suitable for inclusion in the annual report of the Parent

Group, the consolidated statement of financial position at 31 December 2021.

20

Show your workings

b

Under IFRS 10, a parent must consolidate all subsidiaries into a single set of

financial statements. Discuss the key consolidation issues and required

treatments when a subsidiary has:

10

• A non-contiguous year-end (e.g., three months earlier than the parent),

• Different accounting policies (e.g., depreciation methods, inventory

valuation), and

• Fair-value uplifts on acquisition that create temporary differences.

In your answer, cover:

• Year-end alignment and disclosures

• Policy harmonisation and consolidation adjustments

• Recognition of deferred tax on consolidation fair-value

adjustments

Total

30

END OF QUESTION PAPER

5