|

BAC521C-BUSINESS ACCOUNTING 1B-1ST OPP- JUNE 2025 |

|

|

1 Page 1 |

▲back to top |

nAmlBIA

UnlVERSITY

OF SCIEnCE

TECHnoLOGY

HP-65B

HAROLDPUPKEWITZ

GraduateSchoolof Business

FACULTY OF COMMERCE, HUMAN SCIENCESAND EDUCATION

HAROLD PUPKEWITZ GRADUATE SCHOOL OF BUSINESS

QUALIFICATION: DIPLOMA IN BUSINESS PROCESSMANAGEMENT

QUALIFICATION CODE: 06DBPM

COURSE CODE: BAC521C

LEVEL: 6

COURSE NAME: BUSINESS ACCOUNTING 1B

SESSION: JUNE 2025

PAPER: PAPER 1

DURATION: 3 HOURS

MARKS: 100

EXAMINER

FIRST OPPORTUNITY EXAMINATION QUESTION PAPER

Lameck Odada

MODERATOR Hendrina Kangala

INSTRUCTIONS

1. This question paper comprises FOUR (4) questions.

2. Answer ALL the questions in blue or black ink. NO pencil

3. Start each question on a new page in your answer booklet and show all your workings.

4. Unless otherwise stated, round off only final answers to two (2) decimal places where

necessary.

5. Questions relating to this examination may be raised in the initial 30 minutes after the

start of the paper. Thereafter, candidates must use their initiative to deal with any

perceived error or ambiguity & any assumption made by the candidate should be clearly

stated.

PERMISSIBLE MATERIALS

1. Silent, non-programmable calculators

THIS QUESTION PAPER CONSISTS OF 7 PAGES (including this front page)

|

|

2 Page 2 |

▲back to top |

QUESTION 1

[30 MARKS]

For questions 1.1-1.10, just write the answer only (the correct letter chosen) in your answer book and

not on the question paper. Do not copy the question again.

1.1 A company would classify the audit fee paid by a manufacturing company as:

a) Production overhead cost

b) Selling and distribution cost

c) Research and development cost

d) Administration cost

1.2 A hospital's records show that the cost of carrying out health checks in the last five accounting periods

have been as follows:

Period

Number of patients

Total cost (N$)

1

650

17125

2

940

17 800

3

1260

18 650

4

990

17 980

5

1150

18 360

What is the estimated cost of carrying out health checks on 850 patients in period 6 Using the high-

low method?

a) N$17 515

b) N$17 570

c) N$17 625

d) N$17 680

1.3 Which ONE of the following costs would NOT be classified as a production overhead cost in a food

processing company?

a) The cost of renting the factory building

b) The salary of the factory manager

c) The depreciation of equipment located in the materials store

d) The cost of ingredients

1.4 In the Formula Y =a+ bx; b refers to

a) Slope

b) Intercept

c) Dependent variable

d) Total variable costs

1

|

|

3 Page 3 |

▲back to top |

1.5 Which of the following costs remain constant in total when the level of the activity driver varies?

a) Conversion costs

b) Direct costs

c) Fixed costs

d) Mixed costs

1.6 Which of the following differentiates Financial Accounting from Managerial Accounting?

a) Financial Accounting emphasizes forecasts of future performance.

b) Financial Accounting summarizes information for the company as a whole.

c) Financial Accounting is private information for company managers

d) Financial Accounting emphasizes timeliness over precision.

1.7 Conversion costs include:

a) Manufacturing overhead costs

b) Direct material costs

c) Sales commission costs

d) Advertising costs

1.8 The following costs were incurred in September 2020:

Direct materials

N$39 000

Direct labour

N$23 000

Manufacturing overhead

N$17 000

Selling expenses

N$14 000

Administrative expenses

N$27 000

How much is total Prime costs for the month?

a) N$79 000

b) N$120 000

c) N$62 000

d) N$40 000

1.9 Which of the below methods is NOT used to estimate and separate mixed costs?

a) High Low method

b) Scatter Graph method

c) Least squares method

d) Contribution method

2

|

|

4 Page 4 |

▲back to top |

1.10

1.11

1.12

1.13

1.14

1.15

Which of the following costs is an example of a period rather than a product cost?

a) Depreciation on production equipment

b) Salaries of salespersons

c) Wages of production machine operators

d) Insurance on production equipment

Costs can be classified by the following EXCEPT.

a) Element

b) Behaviour

c) Importance to the business

d) Timing

Fixed costs that management can decide not to incur at any time are

a) Always variable costs

b) Unavoidable costs

c) Controllable costs

d) Discretionary costs

As volume changes, which of these costs could be considered a mixed cost?

a) Sales commission expense

b) Assembly line labour

c) Salaries of the accountant

d)_ Utilities at the manufacturing plant

The potential benefit of one alternative that is lost by choosing another alternative is known as

a) Sunk cost

b) Differential cost

c) Opportunity cost

d) Out-of-pocket cost

Manufacturing costs typically consist of

a) Direct materials, direct labour, and manufacturing overhead.

b) Production and shipping costs.

c) Production and marketing costs.

d) Direct materials, direct labour, and administrative costs. e. direct materials, direct labour,

marketing and administrative costs.

1 x 2 marks each = 30 marks

3

|

|

5 Page 5 |

▲back to top |

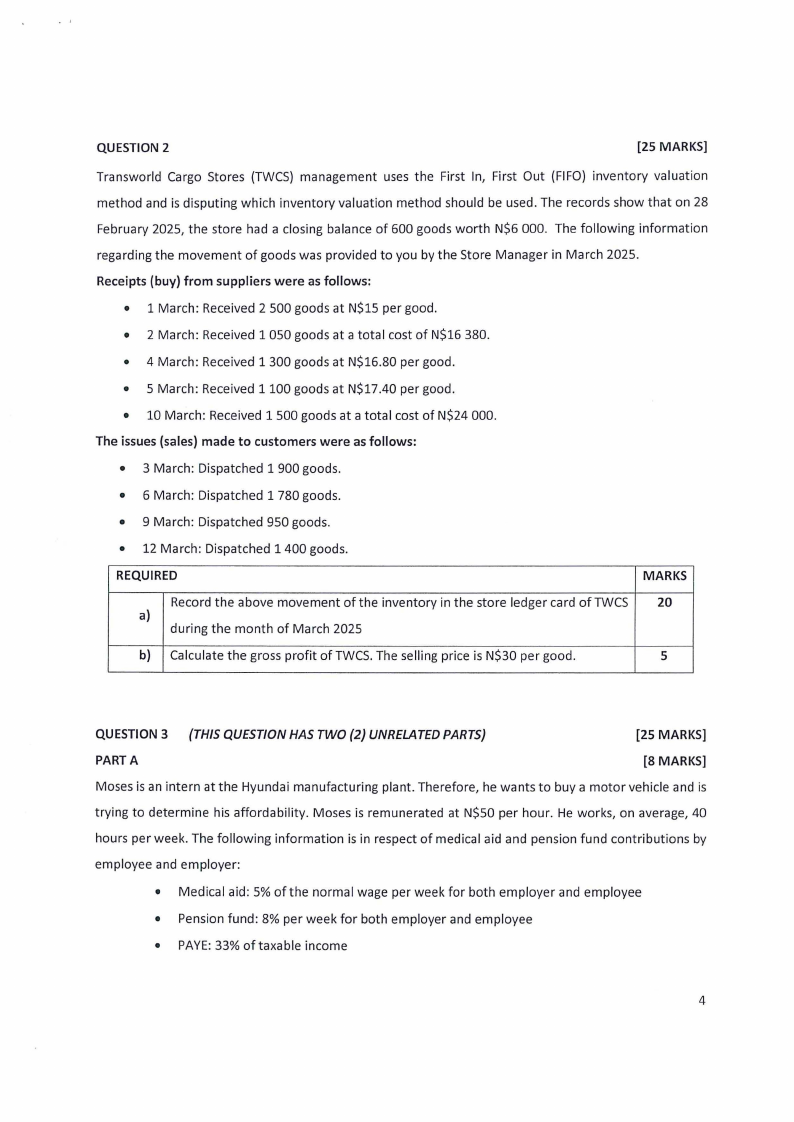

QUESTION 2

[25 MARKS]

Transworld Cargo Stores (TWCS) management uses the First In, First Out (FIFO) inventory valuation

method and is disputing which inventory valuation method should be used. The records show that on 28

February 2025, the store had a closing balance of 600 goods worth N$6 000. The following information

regarding the movement of goods was provided to you by the Store Manager in March 2025.

Receipts (buy) from suppliers were as follows:

• 1 March: Received 2 500 goods at N$15 per good.

• 2 March: Received 1 050 goods at a total cost of N$16 380.

• 4 March: Received 1 300 goods at N$16.80 per good.

• 5 March: Received 1100 goods at N$17.40 per good.

• 10 March: Received 1500 goods at a total cost of N$24 000.

The issues (sales) made to customers were as follows:

• 3 March: Dispatched 1 900 goods.

• 6 March: Dispatched 1 780 goods.

• 9 March: Dispatched 950 goods.

• 12 March: Dispatched 1400 goods.

REQUIRED

MARKS

Record the above movement of the inventory in the store ledger card of TWCS 20

a)

during the month of March 2025

b) Calculate the gross profit of TWCS.The selling price is N$30 per good.

5

QUESTION 3 {THISQUESTIONHAS TWO {2} UNRELATEDPARTS)

[25 MARKS]

PART A

[8 MARKS]

Moses is an intern at the Hyundai manufacturing plant. Therefore, he wants to buy a motor vehicle and is

trying to determine his affordability. Moses is remunerated at N$50 per hour. He works, on average, 40

hours per week. The following information is in respect of medical aid and pension fund contributions by

employee and employer:

• Medical aid: 5% of the normal wage per week for both employer and employee

• Pension fund: 8% per week for both employer and employee

• PAYE:33% of taxable income

4

|

|

6 Page 6 |

▲back to top |

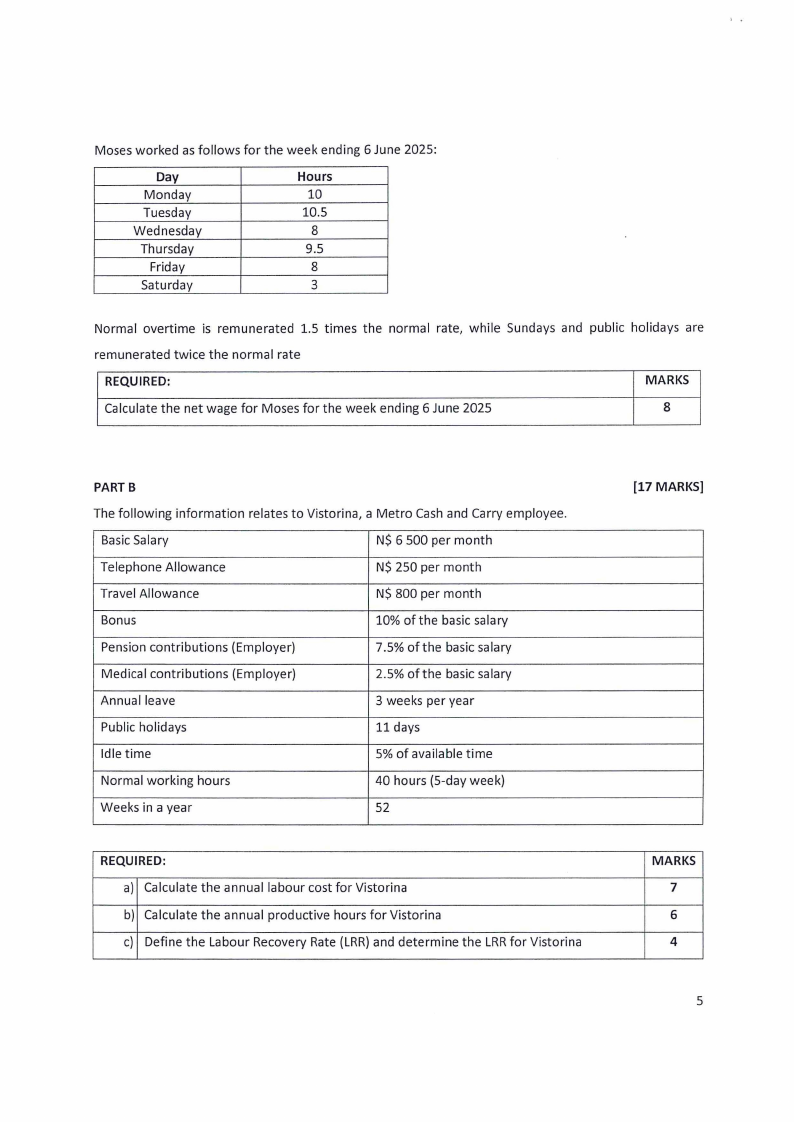

Moses worked as follows for the week ending 6 June 2025:

Day

Monday

Tuesday

Wednesday

Thursday

Friday

Saturday

Hours

10

10.5

8

9.5

8

3

Normal overtime is remunerated 1.5 times the normal rate, while Sundays and public holidays are

remunerated twice the normal rate

REQUIRED:

MARKS

Calculate the net wage for Moses for the week ending 6 June 2025

8

PARTB

The following information relates to Vistorina, a Metro Cash and Carry employee.

Basic Salary

N$ 6 500 per month

Telephone Allowance

N$ 250 per month

Travel Allowance

N$ 800 per month

Bonus

10% of the basic salary

Pension contributions (Employer)

7.5% of the basic salary

Medical contributions (Employer)

2.5% of the basic salary

Annual leave

3 weeks per year

Public holidays

11 days

Idle time

5% of available time

Normal working hours

40 hours (5-day week)

Weeks in a year

52

REQUIRED:

a) Calculate the annual labour cost for Vistorina

b) Calculate the annual productive hours for Vistorina

c) Define the Labour Recovery Rate (LRR)and determine the LRRfor Vistorina

[17 MARKS]

MARKS

7

6

4

5

|

|

7 Page 7 |

▲back to top |

,r

'

QUESTION 4

(20 MARKS]

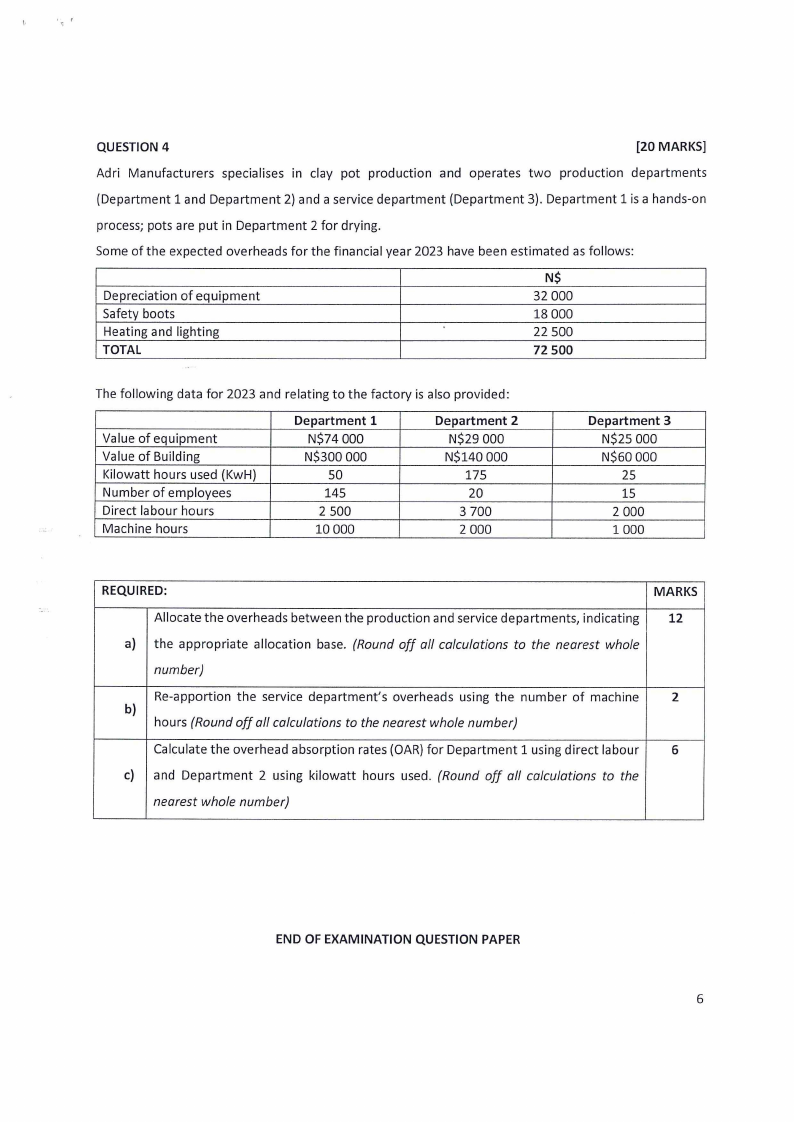

Adri Manufacturers specialises in clay pot production and operates two production departments

(Department 1 and Department 2) and a service department (Department 3). Department 1 is a hands-on

process; pots are put in Department 2 for drying.

Some of the expected overheads for the financial year 2023 have been estimated as follows:

Depreciation of equipment

Safety boots

Heating and lighting

TOTAL

N$

32 000

18 000

22 500

72 500

The following data for 2023 and relating to the factory is also provided:

Value of equipment

Value of Building

Kilowatt hours used (KwH)

Number of employees

Direct labour hours

Machine hours

Department 1

N$74 000

N$300 000

so

145

2 500

10 000

Department 2

N$29 000

N$140 000

175

20

3 700

2 000

Department 3

N$25 000

N$60 000

25

15

2 000

1000

REQUIRED:

MARKS

Allocate the overheads between the production and service departments, indicating

12

a) the appropriate allocation base. (Round off all calculations to the nearest whole

number)

Re-apportion the service department's overheads using the number of machine

2

b)

hours (Round off all calculations to the nearest whole number)

Calculate the overhead absorption rates (OAR) for Department 1 using direct labour

6

c) and Department 2 using kilowatt hours used. (Round off all calculations to the

nearest whole number)

END OF EXAMINATION QUESTION PAPER

6

|

|

8 Page 8 |

▲back to top |