|

GTA711S-TAXATION 310-2ND OPP- JULY 2025 |

|

|

1 Page 1 |

▲back to top |

n Am I BIA u n IVER s ITY

OF SCIEnCE Ano TECHn0L0GY

FACULTY OF COMMERCE, HUMAN SCIENCES& EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING AND FINANCE

QUALIFICATION: BACHELOROF ACCOUNTING

QUALIFICATION CODE: 07BAOC

LEVEL: 7

COURSE CODE: GTA7115

COURSE NAME: TAXATION 310

SESSION: JULY 2025

PAPER: THEORY& APPLICATION

DURATION: 3 HOURS

MARKS: 100

SECOND OPPORTUNITY EXAMINATION QUESTION PAPER

EXAMINER(S) Mrs. Y van Wyk, Mr. J Erastus & Mrs. G Meintjies

MODERATOR: Ms. F Haimbala

INSTRUCTIONS

1. This question paper is made up of THREE(3) questions.

2. Answer ALL the questions and in blue or black ink.

3. Start each question on a new page in your answer booklet.

4. Draw a line through all unused spaces in your answer booklet.

5. The names of people and businesses used throughout this examination paper do not

reflect reality and may be purely coincidental.

6. Questions relating to this examination may be raised in the initial 30 minutes after the

start of the paper. Thereafter, candidates must use their initiative to deal with any

perceived error or ambiguities & any assumption made by the candidate should be

clearly stated.

THIS QUESTION PAPER CONSISTS OF 7 PAGES (excluding this front page)

|

|

2 Page 2 |

▲back to top |

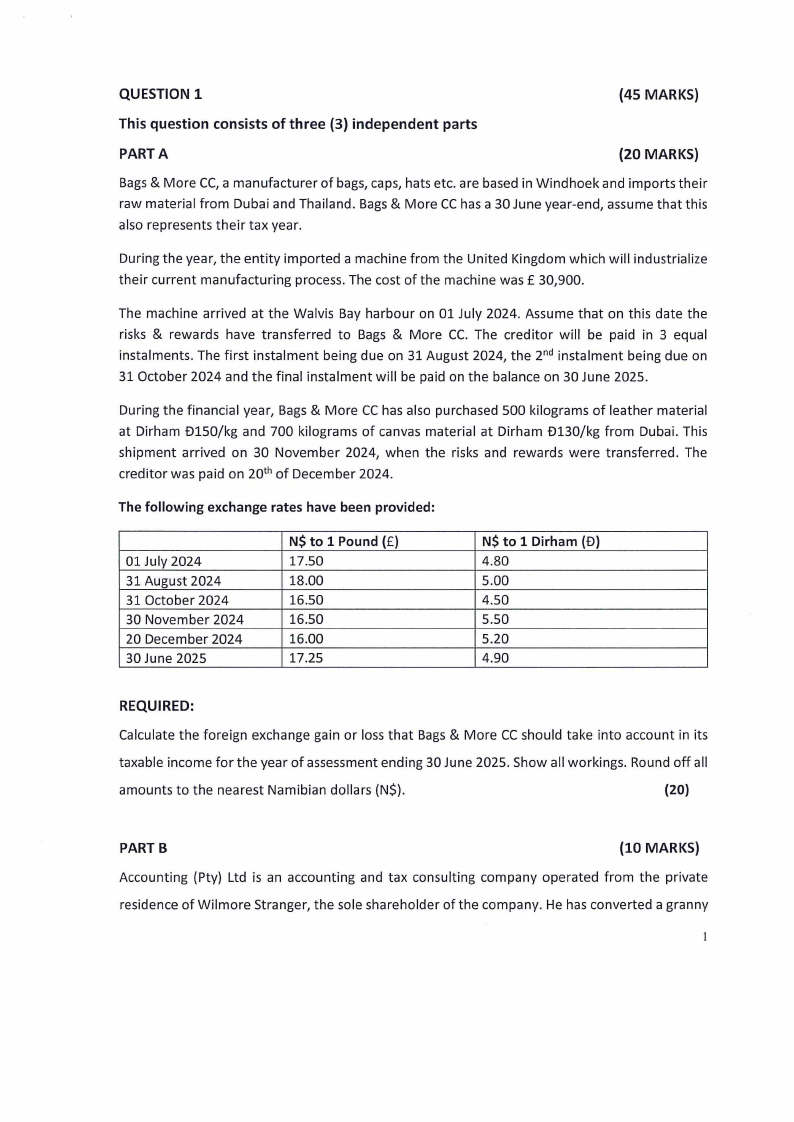

QUESTION 1

(45 MARKS)

This question consists of three (3) independent parts

PART A

(20 MARKS)

Bags& More CC,a manufacturer of bags, caps, hats etc. are based in Windhoek and imports their

raw material from Dubai and Thailand. Bags& More CChas a 30 June year-end, assume that this

also represents their tax year.

During the year, the entity imported a machine from the United Kingdom which will industrialize

their current manufacturing process. The cost of the machine was£ 30,900.

The machine arrived at the Walvis Bay harbour on 01 July 2024. Assume that on this date the

risks & rewards have transferred to Bags & More CC. The creditor will be paid in 3 equal

instalments. The first instalment being due on 31 August 2024, the 2nd instalment being due on

31 October 2024 and the final instalment will be paid on the balance on 30 June 2025.

During the financial year, Bags & More CC has also purchased 500 kilograms of leather material

at Dirham O150/kg and 700 kilograms of canvas material at Dirham O130/kg from Dubai. This

shipment arrived on 30 November 2024, when the risks and rewards were transferred. The

creditor was paid on 20th of December 2024.

The following exchange rates have been provided:

01 July 2024

31 August 2024

31 October 2024

30 November 2024

20 December 2024

30 June 2025

N$ to 1 Pound (£)

17.50

18.00

16.50

16.50

16.00

17.25

N$ to 1 Dirham (D)

4.80

5.00

4.50

5.50

5.20

4.90

REQUIRED:

Calculate the foreign exchange gain or loss that Bags & More CCshould take into account in its

taxable income for the year of assessment ending 30 June 2025. Show all workings. Round off all

amounts to the nearest Namibian dollars (N$}.

(20)

PARTB

(10 MARKS)

Accounting (Pty) Ltd is an accounting and tax consulting company operated from the private

residence of Wilmore Stranger, the sole shareholder of the company. He has converted a granny

|

|

3 Page 3 |

▲back to top |

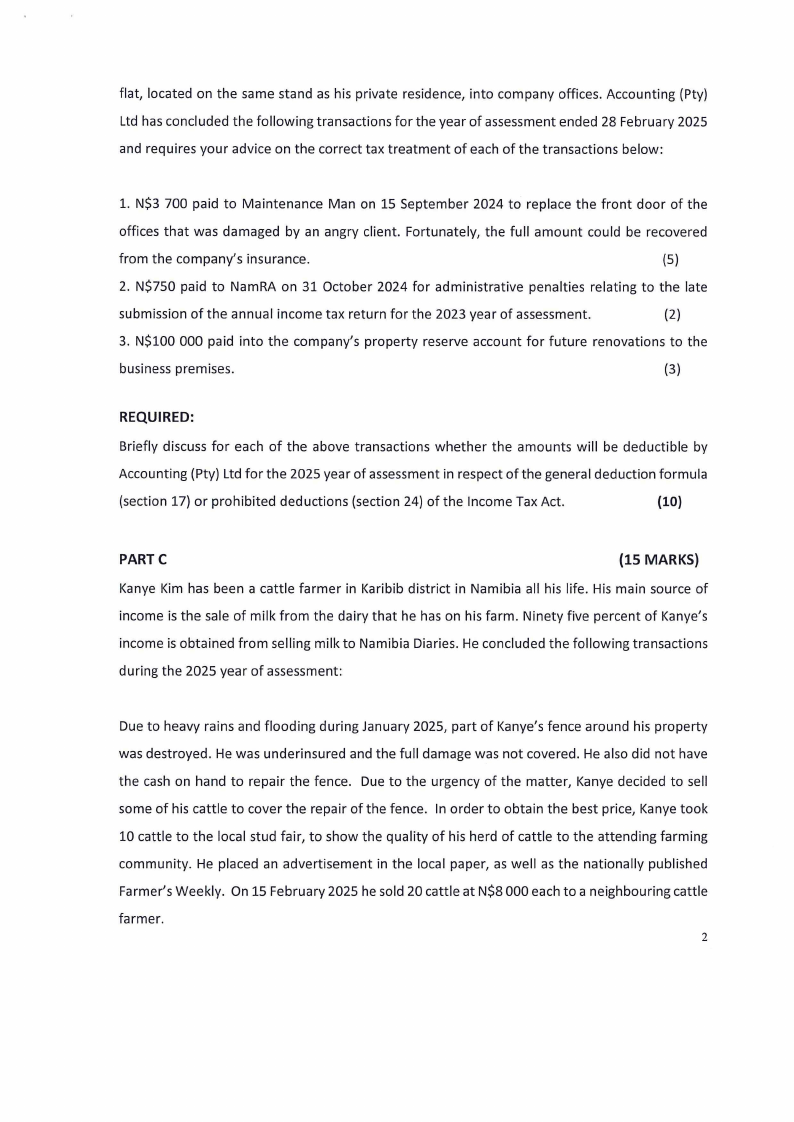

flat, located on the same stand as his private residence, into company offices. Accounting (Pty)

Ltd has concluded the following transactions for the year of assessment ended 28 February 2025

and requires your advice on the correct tax treatment of each of the transactions below:

1. N$3 700 paid to Maintenance Man on 15 September 2024 to replace the front door of the

offices that was damaged by an angry client. Fortunately, the full amount could be recovered

from the company's insurance.

(5)

2. N$750 paid to NamRA on 31 October 2024 for administrative penalties relating to the late

submission of the annual income tax return for the 2023 year of assessment.

(2)

3. N$100 000 paid into the company's property reserve account for future renovations to the

business premises.

(3)

REQUIRED:

Briefly discuss for each of the above transactions whether the amounts will be deductible by

Accounting (Pty) Ltd for the 2025 year of assessment in respect ofthe general deduction formula

(section 17) or prohibited deductions (section 24) of the Income Tax Act.

(10)

PARTC

(15 MARKS)

Kanye Kim has been a cattle farmer in Karibib district in Namibia all his life. His main source of

income is the sale of milk from the dairy that he has on his farm. Ninety five percent of Kanye's

income is obtained from selling milk to Namibia Diaries. He concluded the following transactions

during the 2025 year of assessment:

Due to heavy rains and flooding during January 2025, part of Kanye's fence around his property

was destroyed. He was underinsured and the full damage was not covered. He also did not have

the cash on hand to repair the fence. Due to the urgency of the matter, Kanye decided to sell

some of his cattle to cover the repair of the fence. In order to obtain the best price, Kanye took

10 cattle to the local stud fair, to show the quality of his herd of cattle to the attending farming

community. He placed an advertisement in the local paper, as well as the nationally published

Farmer's Weekly. On 15 February 2025 he sold 20 cattle at N$8 000 each to a neighbouring cattle

farmer.

2

|

|

4 Page 4 |

▲back to top |

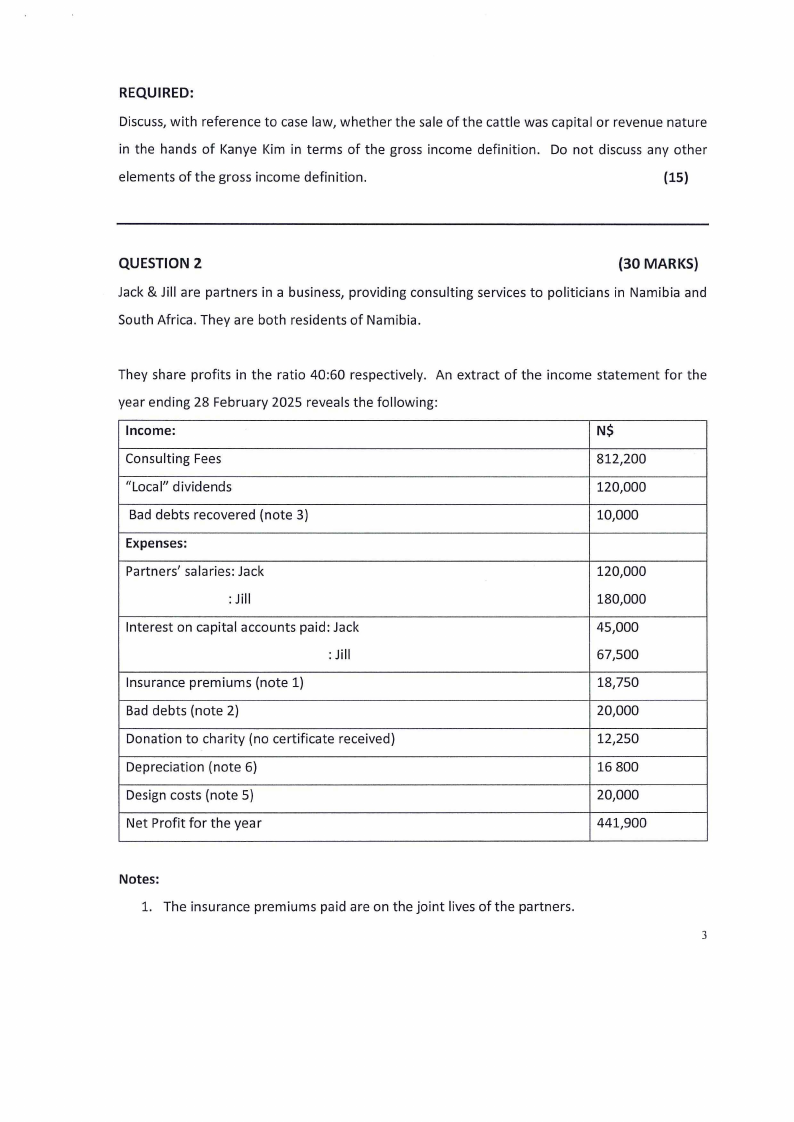

REQUIRED:

Discuss,with reference to case law, whether the sale of the cattle was capital or revenue nature

in the hands of Kanye Kim in terms of the gross income definition. Do not discuss any other

elements of the gross income definition.

(15)

QUESTION 2

(30 MARKS)

Jack & Jill are partners in a business, providing consulting services to politicians in Namibia and

South Africa. They are both residents of Namibia.

They share profits in the ratio 40:60 respectively. An extract of the income statement for the

year ending 28 February 2025 reveals the following:

Income:

N$

Consulting Fees

812,200

"Local" dividends

120,000

Bad debts recovered (note 3)

10,000

Expenses:

Partners' salaries: Jack

120,000

: Jill

180,000

Interest on capital accounts paid: Jack

45,000

: Jill

67,500

Insurance premiums (note 1)

18,750

Bad debts (note 2)

20,000

Donation to charity (no certificate received)

12,250

Depreciation (note 6)

16 800

Design costs (note 5)

20,000

Net Profit for the year

441,900

Notes:

1. The insurance premiums paid are on the joint lives of the partners.

3

|

|

5 Page 5 |

▲back to top |

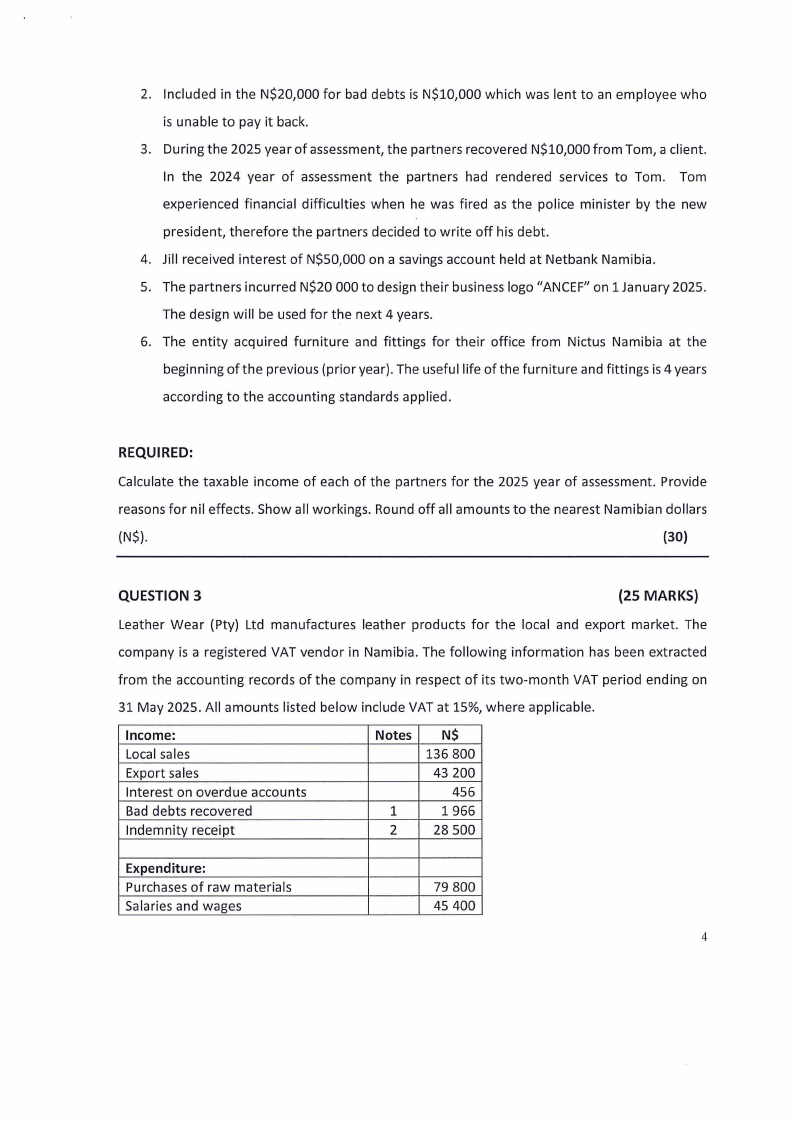

2. Included in the N$20,000 for bad debts is N$10,000 which was lent to an employee who

is unable to pay it back.

3. During the 2025 year of assessment, the partners recovered N$10,000 from Tom, a client.

In the 2024 year of assessment the partners had rendered services to Tom. Tom

experienced financial difficulties when he was fired as the police minister by the new

president, therefore the partners decided to write off his debt.

4. Jill received interest of N$50,000 on a savings account held at Netbank Namibia.

5. The partners incurred N$20 000 to design their business logo "ANCEF" on 1 January 2025.

The design will be used for the next 4 years.

6. The entity acquired furniture and fittings for their office from Nictus Namibia at the

beginning of the previous (prior year). The useful life of the furniture and fittings is 4 years

according to the accounting standards applied.

REQUIRED:

Calculate the taxable income of each of the partners for the 2025 year of assessment. Provide

reasons for nil effects. Show all workings. Round off all amounts to the nearest Namibian dollars

(N$).

(30)

QUESTION 3

{25 MARKS)

Leather Wear (Pty) Ltd manufactures leather products for the local and export market. The

company is a registered VAT vendor in Namibia. The following information has been extracted

from the accounting records of the company in respect of its two-month VAT period ending on

31 May 2025. All amounts listed below include VAT at 15%, where applicable.

Income:

Local sales

Export sales

Interest on overdue accounts

Bad debts recovered

Indemnity receipt

Notes

1

2

N$

136 800

43 200

456

1966

28 500

Expenditure:

Purchases of raw materials

Salaries and wages

79 800

45 400

4

|

|

6 Page 6 |

▲back to top |

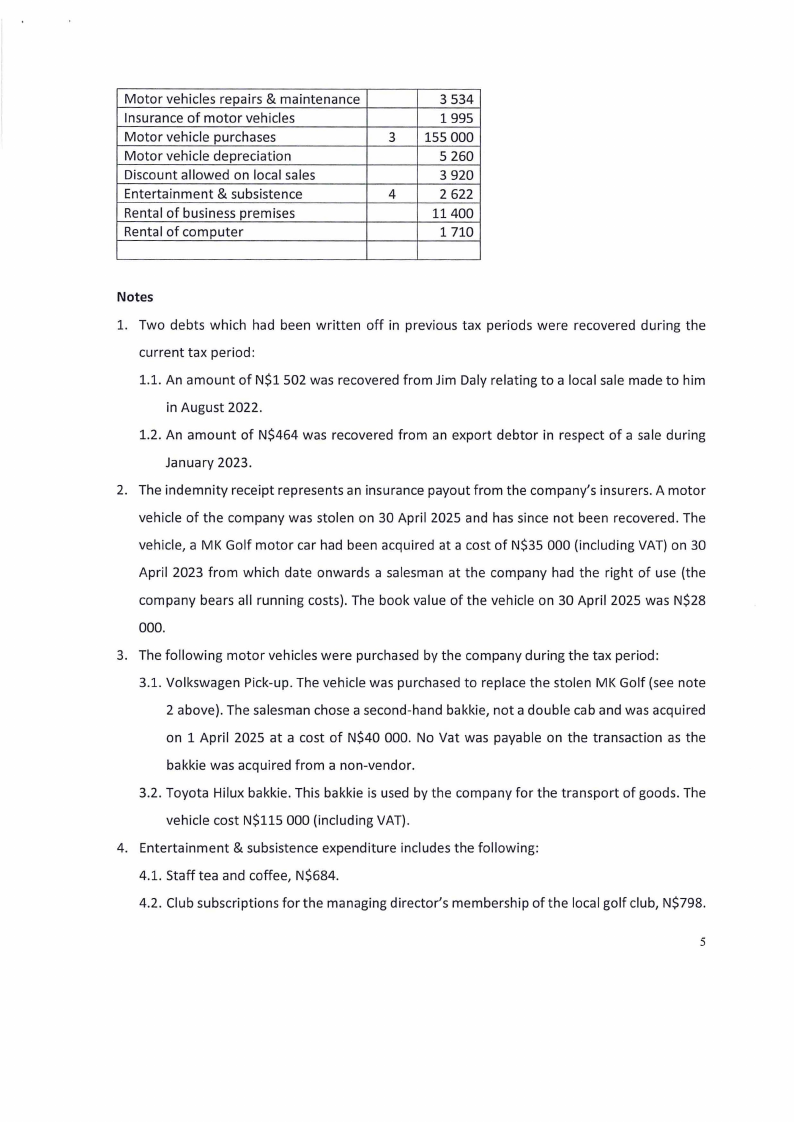

Motor vehicles repairs & maintenance

Insurance of motor vehicles

Motor vehicle purchases

Motor vehicle depreciation

Discount allowed on local sales

Entertainment & subsistence

Rental of business premises

Rental of computer

3 534

1995

3 155 000

5 260

3 920

4

2 622

11400

1 710

Notes

l. Two debts which had been written off in previous tax periods were recovered during the

current tax period:

1.1. An amount of N$1 502 was recovered from Jim Daly relating to a local sale made to him

in August 2022.

1.2. An amount of N$464 was recovered from an export debtor in respect of a sale during

January 2023.

2. The indemnity receipt represents an insurance payout from the company's insurers. A motor

vehicle of the company was stolen on 30 April 2025 and has since not been recovered. The

vehicle, a MK Golf motor car had been acquired at a cost of N$35 000 (including VAT) on 30

April 2023 from which date onwards a salesman at the company had the right of use (the

company bears all running costs). The book value of the vehicle on 30 April 2025 was N$28

000.

3. The following motor vehicles were purchased by the company during the tax period:

3.1. Volkswagen Pick-up. The vehicle was purchased to replace the stolen MK Golf (see note

2 above). The salesman chose a second-hand bakkie, not a double cab and was acquired

on 1 April 2025 at a cost of N$40 000. No Vat was payable on the transaction as the

bakkie was acquired from a non-vendor.

3.2. Toyota Hilux bakkie. This bakkie is used by the company for the transport of goods. The

vehicle cost N$115 000 (including VAT).

4. Entertainment & subsistence expenditure includes the following:

4.1. Staff tea and coffee, N$684.

4.2. Club subscriptions for the managing director's membership of the local golf club, N$798.

5

|

|

7 Page 7 |

▲back to top |

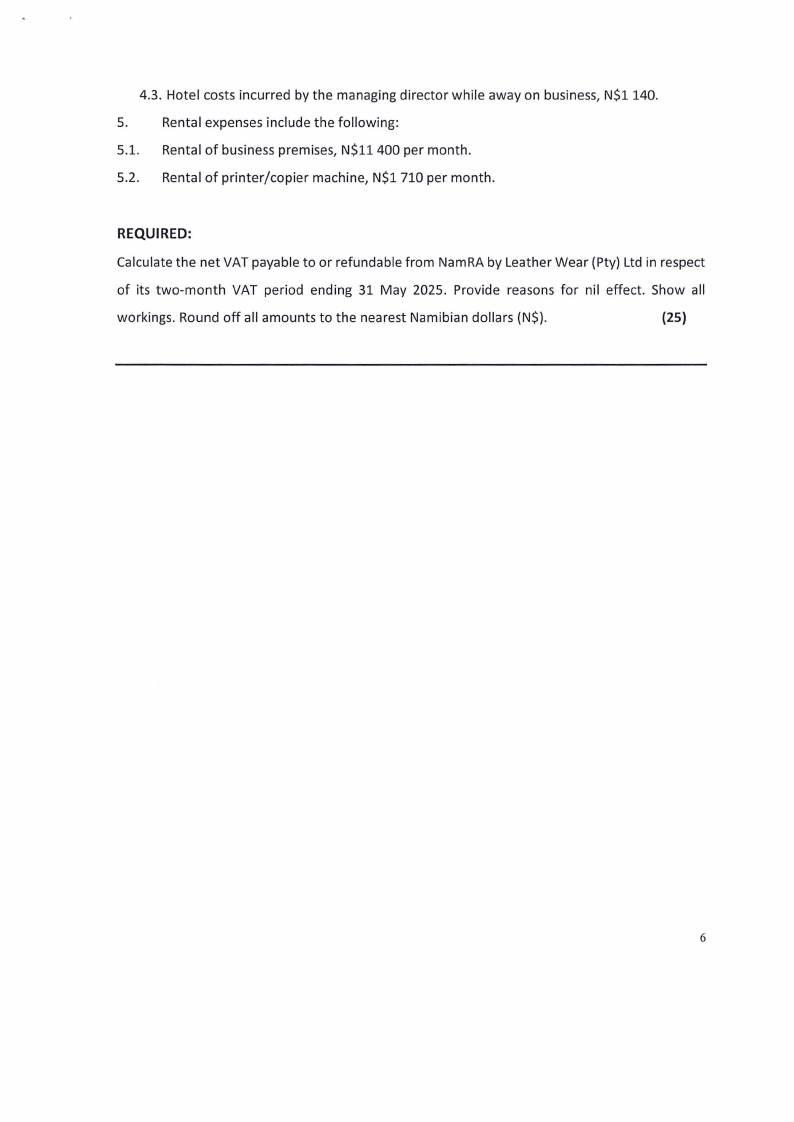

4.3. Hotel costs incurred by the managing director while away on business, N$1140.

5.

Rental expenses include the following:

5.1. Rental of business premises, N$11 400 per month.

5.2. Rental of printer/copier machine, N$1 710 per month.

REQUIRED:

Calculate the net VAT payable to or refundable from Nam RA by Leather Wear (Pty) Ltd in respect

of its two-month VAT period ending 31 May 2025. Provide reasons for nil effect. Show all

workings. Round off all amounts to the nearest Namibian dollars (N$).

(25)

6

|

|

8 Page 8 |

▲back to top |

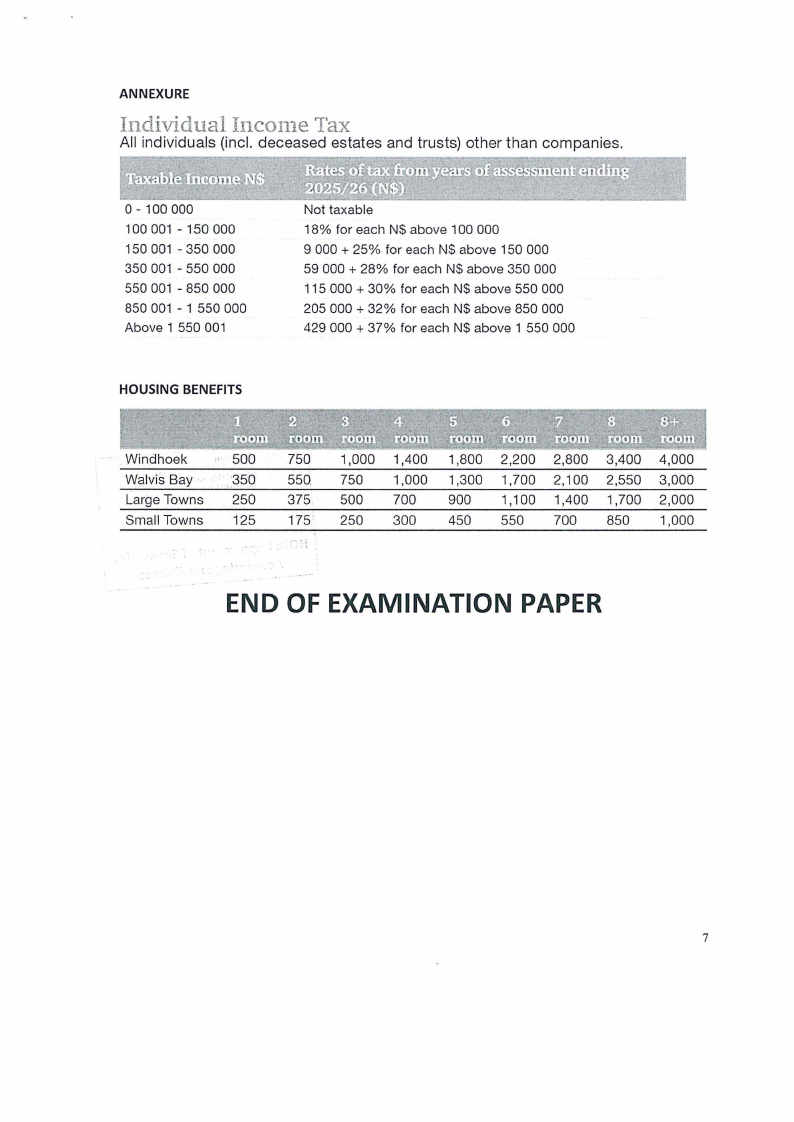

ANNEXURE

Individual Incorne Ta,-x

All individuals (incl. deceased estates and trusts) other than companies.

0 - 100 000

100 001 - 150 000

150 001 - 350 000

350 001 - 550 000

550 001 - 850 000

850 001 - 1 550 000

Above 1 550 001

HOUSING BENEFITS

Not taxable

18% for each N$ above 100 000

9 000 + 25% for each N$ above 150 000

59 000 + 28% for each N$ above 350 000

115 000 + 30% for each N$ above 550 000

205 000 + 32% for each N$ above 850 000

429 000 + 37% for each N$ above 1 550 000

Windhoek

Walvis Bay,

Large Towns

Small Towns

500

,:~50

250

125

750

550

375

175:

.~ • • I

1,000

750

500

250

1,400

1,000

700

300

1,800

1,300

900

450

2,200

1,700

1,100

550

2,800

2,100

1,400

700

3,400

2,550

1,700

850

4,000

3,000

2,000

1,000

END OF EXAMINATION PAPER

7