|

AEM810S-APPLIED ECONOMETRICS-2ND OPP-JULY 2025 |

|

|

1 Page 1 |

▲back to top |

nAmI BIA unIVERSITY

OF SCIEnCE Ano TECHnOLOGY

FACULTY OF COMMERCE, HUMAN SCIENCESAND EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING AND FINANCE

QUALIFICATION : BACHELOR OF ECONOMICS HONOURS

QUALIFICATION CODE: 08BECH

LEVEL: 8

COURSE CODE: AEM810S

COURSE NAME: APPLIED ECONOMETRICS

SESSION: JUNE/JULY 2025

DURATION: 3 HOURS

PAPER: PAPER2

MARKS: 100

EXAMINER

SECOND OPPORTUNITY EXAMINATION QUESTION PAPER

Dr. Valdemar J. Undji (NUST)

MODERATOR: Ms. Ndesheetelwa N. Shitenga (NUST)

INSTRUCTIONS

1. Read the questions carefully and answer ALL questions

2. Unless specified, all final answers must be round to 2 decimal places

3. Use 5% Significance level

4. Appendixes are attached

5. The use of a calculator is allowed

THIS QUESTION PAPER CONSISTS OF _7 _ PAGES (Including this front page)

|

|

2 Page 2 |

▲back to top |

QUESTION 1

(25 marks]

= xf e a) Consider the following non-linear model: y f]0 1 et.

Transform the above model into a linear model which can be estimated by means of an ordinary

least square (OLS).

(4)

b) Briefly differentiate between the Moving Average (MA) process, the Autoregressive (AR)

process, and the Autoregressive Moving Average (ARMA) process.

(9)

c) Comment on the meaning of the following terms:

(12)

i) Stochastic process

ii) Spurius regression

iii) Cointegration

iv) Stationarity

2

|

|

3 Page 3 |

▲back to top |

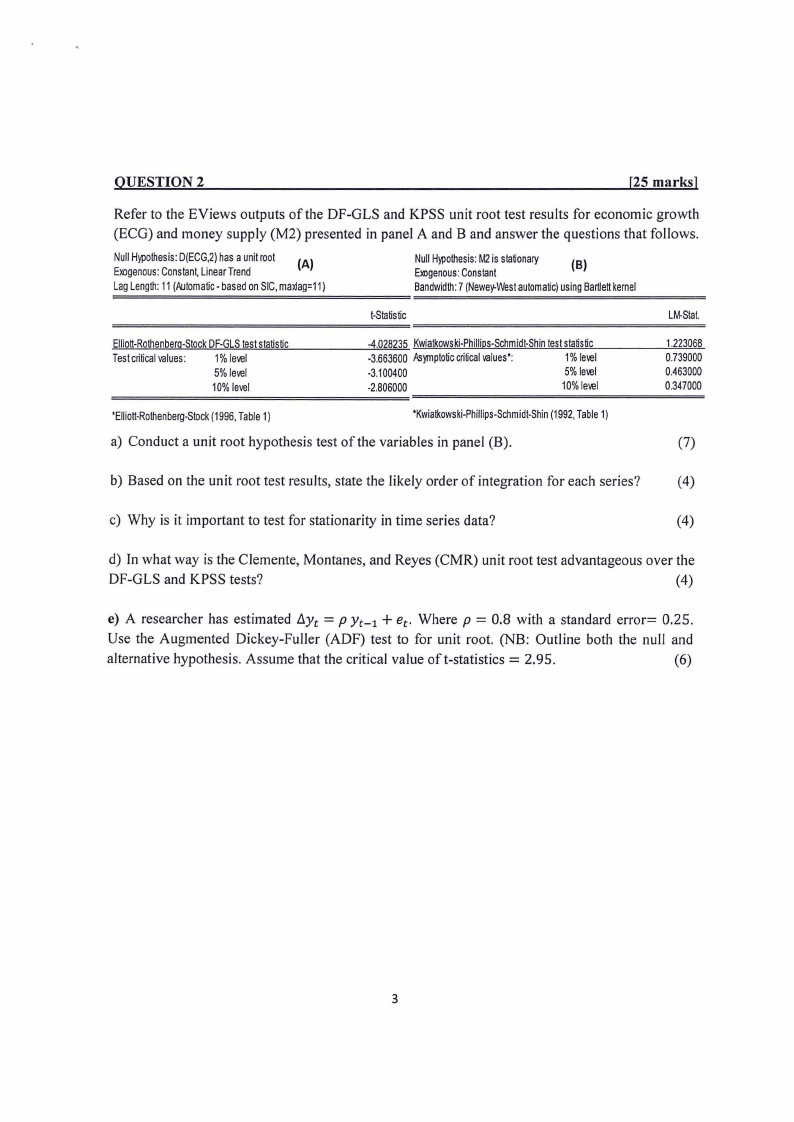

OUESTION2

[25 marks]

Refer to the EViews outputs of the DF-GLS and KPSS unit root test results for economic growth

(ECG) and money supply (M2) presented in panel A and Band answer the questions that follows.

NullHypothesDis(:ECG,2h)asaunitroot (A)

ExogenouCso: nstanLt,ineaTr rend

LagLength1:1(Automatibc-asedonSICm, ax!ag=11)

NullHypothesMis:2is stationary

EJOJgenoCuosn:stant

(B)

Bandwidt7h(:Newey-Waeustomatiucs) ingBartlektternel

I-Statistic

LM-Stat.

""'El""lio"'"tt-.!.!Ro""th""'e'""nb"'"ers,..,,.,__q,t-i.c.':-:-.-S--t"-"-o'-4c""'k.0-"-"D28'-"F"-2"3"G=K5Lw"i"a'Stk"o"'wtes"k'-is-Pt,.h.,il,lsip.,s,,-_Stcahtim,,.ti,de,·ts-tSsthaitnistic

Testcriticavlalues: 1%level

-3.663600.As}mploticcritvicaalul es':

1%level

5%level

-3.100400

5%level

10%level

-2.806000

10%level

1.223068

0.739000

0.463000

0.347000

'Elliott-Rolhenberg-S(1to9c9k6T, able1)

'Kwiatkowski-Phillips-Schmi(d1t9-S9h2Ti,nable1)

a) Conduct a unit root hypothesis test of the variables in panel (B).

(7)

b) Based on the unit root test results, state the likely order of integration for each series?

(4)

c) Why is it important to test for stationarity in time series data?

(4)

d) In what way is the Clemente, Montanes, and Reyes (CMR) unit root test advantageous over the

DF-GLS and KPSS tests?

(4)

e) A researcher has estimated l1yt = p Yt-i + et. Where p = 0.8 with a standard error= 0.25.

Use the Augmented Dickey-Fuller (ADF) test to for unit root. (NB: Outline both the null and

alternative hypothesis. Assume that the critical value oft-statistics= 2.95.

(6)

3

|

|

4 Page 4 |

▲back to top |

QUESTION3

[25 marks]

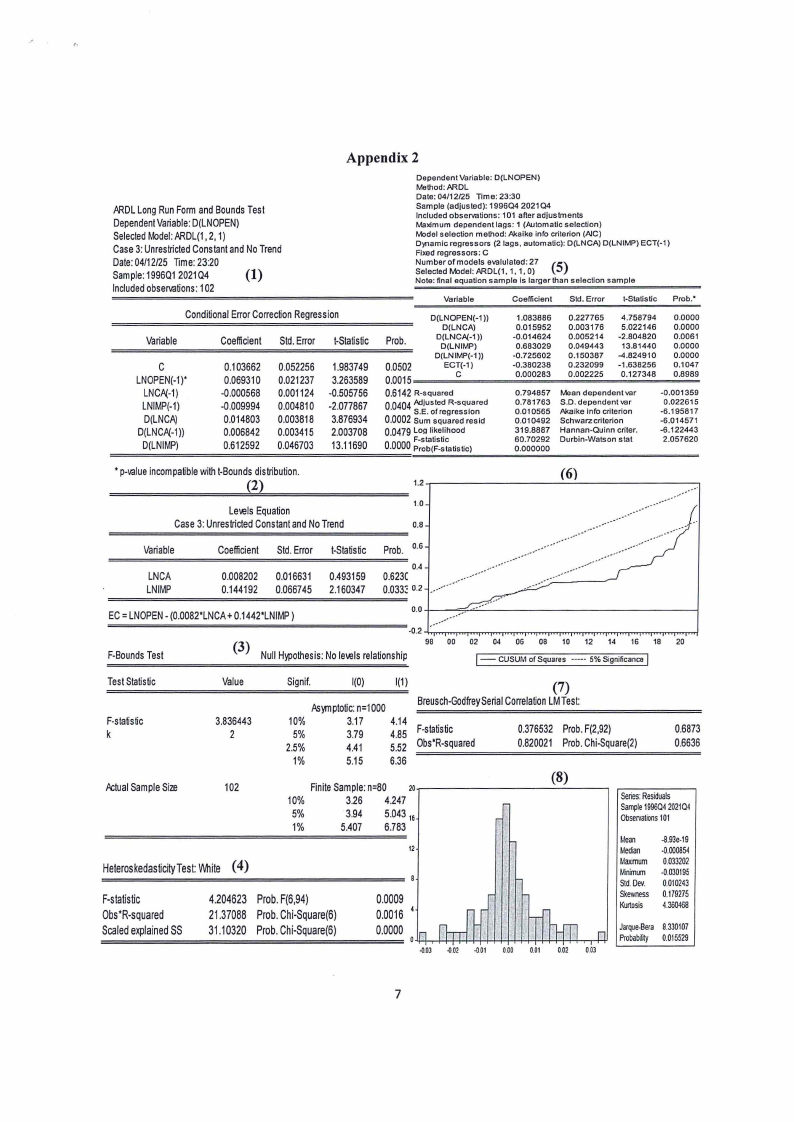

Refer to Appendix 2 showing the EViews output for the ARDL model examining the relationship

between log of trade openness (lnOPEN), log of current account balance (lnCA), and log of

imports (lnIMP).

a) Formulate a generic ARDL model framework to capture both the short-run and long-run

relationships among these variables.

(4)

b) Using the Bounds test results, conduct a hypothesis test to determine whether a long-run

relationship exists between the variables.

(6)

c) Interpret the long-run coefficient estimates. (Discuss the magnitude, sign, statistical significance

and economic meaning of each explanatory variable.)

(6)

d) Look at the error correction model (ECM) results. Report the error correction term (ECT)

coefficient and explain its purpose.

( 4)

e) Using the diagnostic test results in the appendix, say whether the model meets the basic

assumptions of a good regression model (like no serial correlation, constant variance, normal

errors). Explain what this means for how reliable the results are.

(5)

4

|

|

5 Page 5 |

▲back to top |

QUESTION 4

Consider the following multiple regression model specified as:

(25 marks]

Where, M2 represents money supply, NF A is net foreign assets, REPO is repo rate and GE is

government expenditure. To answer the questions that follow refer to Appendix I consisting of

output obtained using the EViews software.

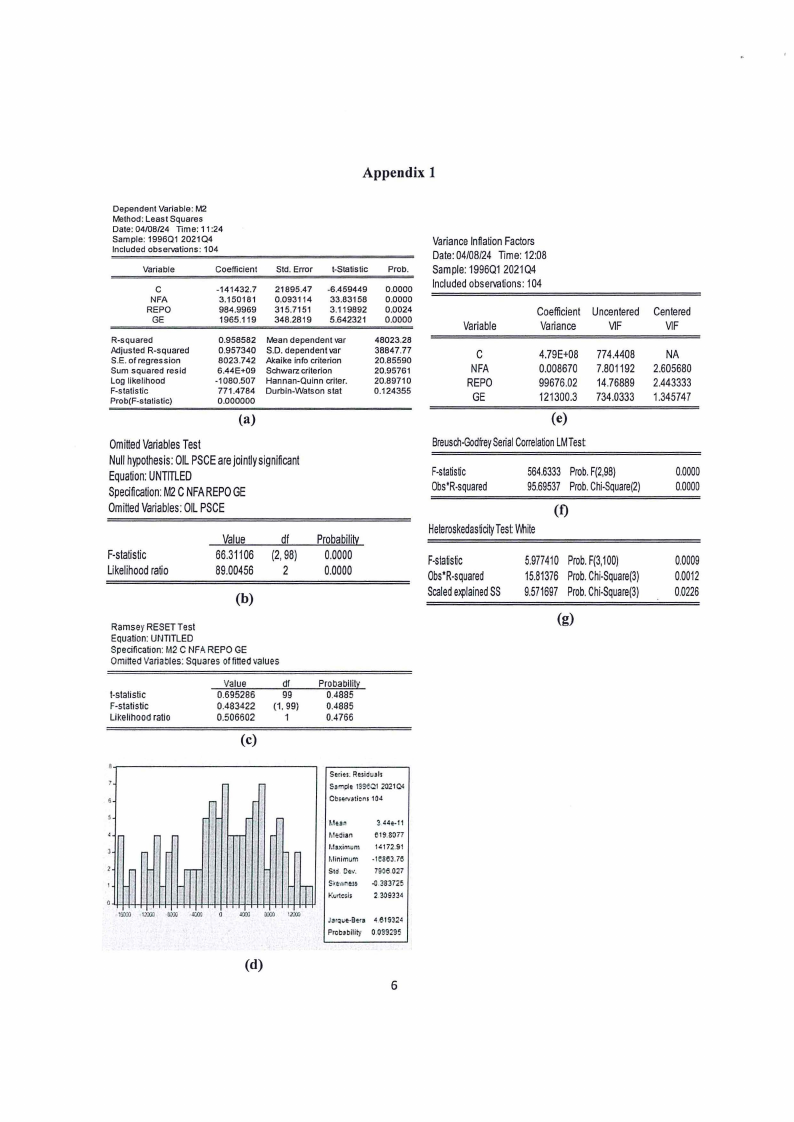

a) Refer to the output used to test for the hypothesis of multicolinearity in the model and interpret

it results.

(4)

b) How would you interpret the output of the omitted variable test. (Hint: Conduct the hypothesis

that the variables OIL and PSCE have jointly omitted from the original model).

(4)

c) How would you interpret the output for the Ramsey RESET test. (Hint: Conduct an hypothesis

test that the model is correctly specified).

(4)

d) Does the original model satisfy the normality assumption? Justify.

(4)

e) Are the residuals serially correlation?

(4)

f) Do you suspect any an issues regarding heteroskedasticity?

(5)

5

|

|

6 Page 6 |

▲back to top |

Appendix 1

Dependent Variable: M2

Method: Least Squares

Date: 04/08/24 Time: 11 :24

Sample: 199601 202104

Included observations: 104

Variable

Coefficient

Std. Error

t-Statistic

Prob.

C

NFA

REPO

GE

-141432.7

3.150181

984.9969

1965.119

21895.47

0.093114

315.7151

348.2819

-6.459449

33.83158

3.119892

5.642321

0.0000

0.0000

0.0024

0.0000

R-squared

Adjusted R-squared

S.E. of regression

Sum squared resid

Log likelihood

F-statistic

Prob(F-statistic}

0.958582

0.957340

8023.742

6.44E+09

-1080.507

771.4784

0.000000

(a)

Mean dependent var

S.D. dependent var

Akaike info criterion

Schwarz criterion

Hannan-Quinn criter.

Durbin-Watson stat

48023.28

38847.77

20.85590

20.95761

20.89710

0.124355

OmitteVdariableTsest

Nulhl ypothesOisI:LPSCEarejointlysignificant

EquatioUn:NTITLED

SpecificatioMn2:CNFAREPOGE

OmitteVdariableOs:ILPSCE

F-statistic

Likelihooradtio

Value df

66.31106 (2,98)

89.00456 2

Probability

0.0000

0.0000

(b)

RamseyRESETTest

Equation:UNTITLED

Specification:M2CNF.AR. EPOGE

OmittedVariables:Squares offittedvalues

I-statistic

F-statistic

Likelihood ratio

Value

0.695286

0.483422

0.506602

df

99

(1, 99)

1

(c)

Probabilitr:

0.4885

0.4885

0.4766

VariancIenflatioFnactors

Date0: 4/08/24TIme:12:08

Sample1:996Q21021Q4

Includeodbservation1s0:4

Variable

CoefficientUncenteredCentered

Variance \\/IF

\\/IF

C

NFA

REPO

GE

4.79E+08 774.4408 NA

0.008670 7.801192 2.605680

99676.02 14.76889 2.443333

121300.3 734.0333 1.345747

(e)

Breusch-GoSdefreiaCylorrelatLioMnTest

F-statistic

564.633P3robF.(2,98)

0.0000

Obs'R-squared 95.6953P7robC.hi-Square(2) 0.0000

(f)

HeleroskedaTsteicsiWt~ iile

F-slatistic

Obs'R-squared

ScaleedxplainSeSd

5.97741P0robF.(31,00)

0.0009

15.8137P6robC.hi-Square(3) 0.0012

9.57169P7robC.hi-Square(3) 0.0226

(g)

m'

:tOO:i 1~

T

(l))J

Jf.lJ)

1,

I

i I

l(Q)

S•mi:l• 1m<01 20210<

CbiE-rvaticnJ104

r;

Mun

i 4.4e-t1

Median

619.80;7

h.lsxin,um 1•172.91

Minimum -le863.76

Std. De,.·.

mS~ewnl!ss

Kurtosi1

7906.027

-0 2-83725

2 30g314

oo:ti 12:ill

J,rque-Beu 4 61532•

Probability 0.039295

(d)

6

|

|

7 Page 7 |

▲back to top |

Appendix 2

AADLLongRunFormandBoundsTest

DependeVntariableD: (LNOPEN)

SelecteMd odeAl:ADL(12,,1)

Case3:UnrestricteCdonstanatndNoTrend

Date0: 4/12/25nme:23:20

Sample1:996Q21021Q4

(1)

Includeodbservation1s0: 2

Dependent Variable: D(LNOPEN)

Method: ARDL

Date: 04/12/25 nme: 23:30

Sample (adjusted): 199604 202104

Included observations: 101 after adjustments

Maximum dependentlags: 1 (Automatic selection)

IV,odelselection method: Akaike info criterion (AIC)

D~amic regressors (2 lags, automatic): D(LNCA) D(LNIMP) ECT(-1)

Fixed regressors: C

Number of models evalulated: 27

Selected IV,odel:ARDL(1, 1, 1, 0)

(5)

Note: final equation sample Is larger than selection sample

Variable

Coefficient

Std. Error

I-Statistic Prob:

ConditionaElrrorCorrectioRnegresison

Variable

Coefficient Std.Error I-Statistic

C

LNOPEN(-1)'

LNC,A{-1)

LNIMP(-1)

D(LNCA)

D(LNC,A{-1))

D(LNIMP)

0.103662 0.052256 1.983749

0.069310 0.021237 3.263589

-0.000568 0.001124 -0.505756

-0.009994 0.004810 -2.077867

0.014803 0.003818 3.876934

0.006842 0.003415 2.003708

0.612592 0.046703 13.11690

Prob.

0.0502

D(LNOPEN(-1))

D(LNCA)

D(LNCA(-1))

D(LNIMP)

D(LNIMP(-1))

ECT(-1)

0.0015===c==========

0.6142R-squared

0_0404AS.dEju. sotef dregRre-ssqsuioanred

0.0002Sum squared resid

0,0479Log likelihood

F-statistic

0.0000Prob(F-statistic)

1.083886

0.015952

-0.014624

0.683029

-0.725602

-0.380238

0.000283

0.794857

0.781763

0.010565

0.010492

319.8887

60.70292

0.000000

0.227765

0.003176

0.005214

0.049443

0.150387

0.232099

0.002225

4.758794

5.022146

-2.804820

13.81440

-4.824910

-1.638256

0.127348

0.0000

0.0000

0.0061

0.0000

0.0000

0.1047

0.8989

Mean dependent var

S.D. dependent var

Akaike Info criterion

Schwarz criterion

Hannan-Quinn criter.

Durbin-Watson stat

-0.001359

0.022615

·6.195817

-6.014571

-6.122443

2.057620

• p-valueincompatibwleithI-Bounddsistribution.

(2)

Lewis Equation

Case3:UnrestricteCdonstanatndNoTrend

1.2----------------

1.0

0.8

Variable

LNCA

LNIMP

Coefficient Std.Error I-Statistic Prob. 0·6

0-4

0.008202 0.016631 0.493159 0.623(

0.144192 0.066745 2.160347 0.033~0-2

(6)

.... ..•··

..-··

__...-··

....•· ....-.·· ...··

__...-··_·,,.•·

..-····

EC=LNOPE•N(0.0082'LNC+A0.1442'LNIMP)

-0.2 --1-n-"TTI'"'"TT,,.,.,.,,.,..,...m-n.,.,,.,.rrn,.,,...,.m-n""TT...,.-.,.,.,.,...,.,..,...,,,..,.,..,.,.,

F-BoundTsest

(3)

98

NullHypothesiNs:olewisrelationship

00

02 04 06 08 10 12 14 16 18

j - I CUSUM of Squares •··•• 5% Significance

20

TestStatistic

Value

Signif.

1(0)

1(1)

(7)

ki~ptotic: n=1000

Breusch-GodfreySCeroiarrlelatioLnMTest:

F-statistic

k

3.836443

2

10%

5%

2.5%

3.17

3.79

4.41

4.14

4.85

F-statistic

5.52 Obs'R-squared

0.376532ProbF. (2,92)

0.820021ProbC. hi-Square(2)

0.6873

0.6636

1%

5.15 6.36

/lctuaSl ampleSize

102

FiniteSamplen:=80 20.,....---------------,

10%

3.26 4.247

5%

3.94 5.04316

1%

5.407 6.783

(8)

SeriesR: esiduals

Sampl1e99602402104

Observa1i1o0n1s

12

HeteroskedasticityWTeiitset: (4)

F-statistic

Obs*R-squared

ScaleedxplaineSdS

4.204623ProbF. (6,94)

21.37088ProbC. hi-Square(6)

31.10320ProbC. hi-Square(6)

0.0009

0.0016

0.0000

I.lean -ll.93e-19

Median -0.000854

1,laximum 0.033202

Minimum -0.030195

StdD. ev. 0.010243

Skewness 0.179275

Kurtosis 4.360468

Jarque-Ber8a.330107

Probabifrty 0.015529

--0.03 --0.02 --0.01 0.00 0.01 0.02 O.Ol

7

|

|

8 Page 8 |

▲back to top |