|

TAX601Y-TAXATION 201-1ST OPP-NOV 2025 |

|

|

1 Page 1 |

▲back to top |

~

nAm I BIA un IVE RSITY

OF SCI En CE Ano TECH n OLOGY

FACULTY OF COMMERCE, HUMAN SCIENCES & EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING AND FINANCE

QUALIFICATION : BACHELOR OF ACCOUNTING (CHARTERED ACCOUNTANCY)

QUALIFICATION CODE: 07BACC

LEVEL: 6

COURSE: TAXATION 201

COURSE CODE: TAX601Y

DATE: OCTOBER/NOVEMBER 2025

DURATION: 150 MINUTES

SESSION: THEORY & CALCULATIONS

MARKS: 100

ASSESSMENT 6 - FIRST OPPORTUNITY EXAMINATION

EXAMINER:

Mr I-K. Kenaruzo

MODERATOR: Mrs Y. van Wyk

INSTRUCTIONS TO CANDIDATES

1. This paper consists of 8 pages (including cover page and appendices).

2. You are reminded that answers may NOT be written in pencil. NO tippex may be used .

3. The marks shown against the requirement(s) for every question should be regarded as an

indication of the expected length and depth of your answer.

4. Answer the questions by the use of:

- Effective structure and presentation; clear explanations.

- Logical arguments; and clear and concise language.

5. Show all calculations clearly. Round off calculated amounts to the nearest NAD/ZAR.

Question

Mark(s)

Time allocated (minutes)

Legislation

1

45

2

30

3

25

68

South African Taxation

45

South African Taxation

37

Namibian Taxation

Total

100

150

1

TAX601Y, Assessment 6

© NUST2025

|

|

2 Page 2 |

▲back to top |

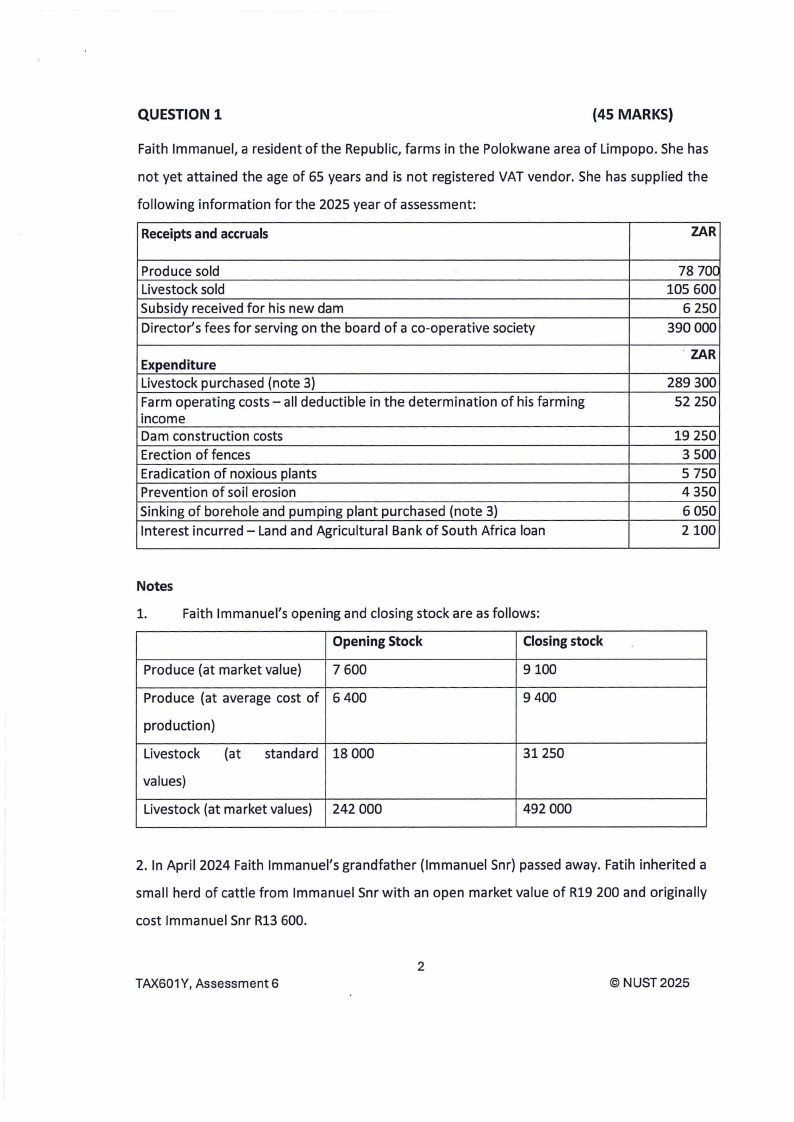

QUESTION 1

(45 MARKS)

Faith Immanuel, a resident of the Republic, farms in the Polokwane area of Limpopo. She has

not yet attained the age of 65 years and is not registered VAT vendor. She has supplied the

following information for the 2025 year of assessment:

Receipts and accruals

ZAR

Produce sold

Livestock sold

Subsidy received for his new dam

Director's fees for serving on the board of a co-operative society

Expenditure

Livestock purchased (note 3}

Farm operating costs - all deductible in the determination of his farming

income

Dam construction costs

Erection of fences

Eradication of noxious plants

Prevention of soil erosion

Sinking of borehole and pumping plant purchased (note 3}

Interest incurred - Land and Agricultural Bank of South Africa loan

78 70(

105 600

6 250

390 000

' ZAR

289 300

52 250

19 250

3 500

5 750

4350

6050

2100

Notes

1.

Faith Immanuel's opening and closing stock are as follows:

Opening Stock

Closing stock

Produce (at market value} 7 600

9100

Produce (at average cost of 6400

9400

production}

Livestock (at standard 18 000

31250

values)

Livestock (at market values) 242 000

492 000

2. In April 2024 Faith Immanuel's grandfather (Immanuel Snr) passed away. Fatih inherited a

small herd of cattle from Immanuel Snr with an open market value of R19 200 and originally

cost Immanuel Snr R13 600.

2

TAX601Y, Assessment 6

© NUST2025

|

|

3 Page 3 |

▲back to top |

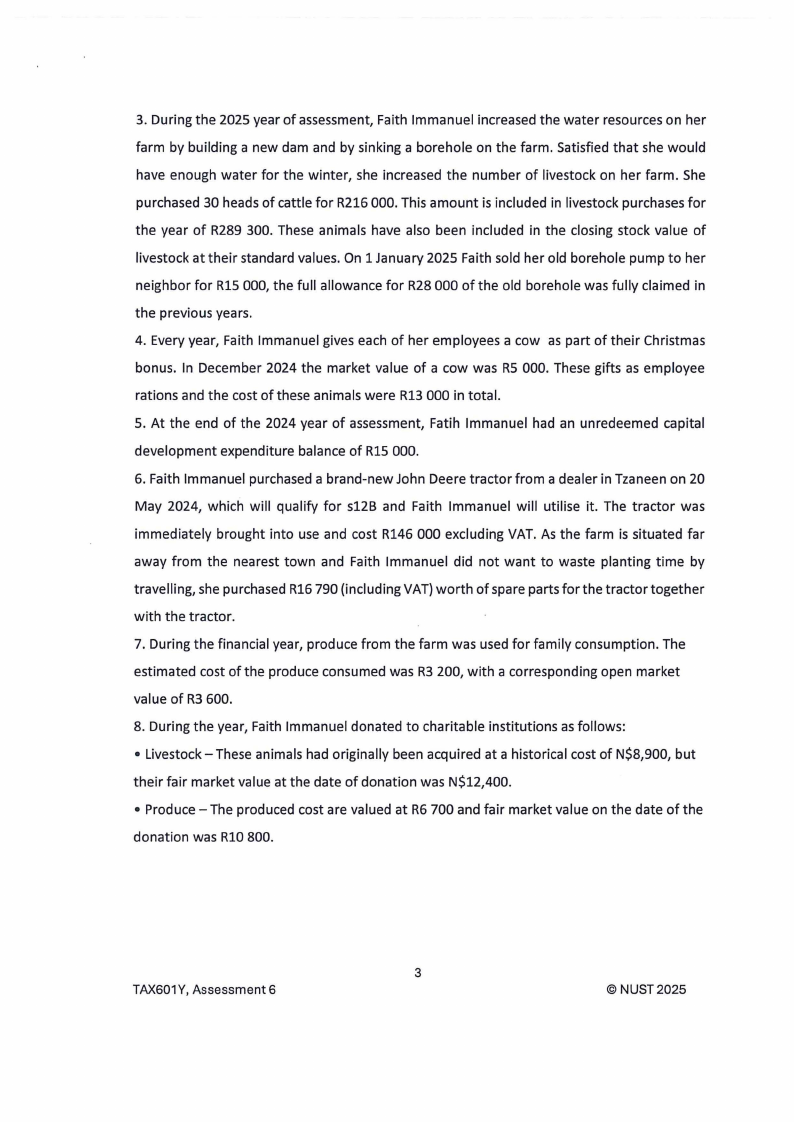

3. During the 2025 year of assessment, Faith Immanuel increased the water resources on her

farm by building a new dam and by sinking a borehole on the farm. Satisfied that she would

have enough water for the winter, she increased the number of livestock on her farm. She

purchased 30 heads of cattle for R216 000. This amount is included in livestock purchases for

the year of R289 300. These animals have also been included in the closing stock value of

livestock at their standard values. On 1 January 2025 Faith sold her old borehole pump to her

neighbor for RlS 000, the full allowance for R28 000 of the old borehole was fully claimed in

the previous years.

4. Every year, Faith Immanuel gives each of her employees a cow as part of their Christmas

bonus. In December 2024 the market value of a cow was RS 000. These gifts as employee

rations and the cost of these animals were R13 000 in total.

5. At the end of the 2024 year of assessment, Fatih Immanuel had an unredeemed capital

development expenditure balance of RlS 000.

6. Faith Immanuel purchased a brand-new John Deere tractor from a dealer in Tzaneen on 20

May 2024, which will qualify for s12B and Faith Immanuel will utilise it. The tractor was

immediately brought into use and cost R146 000 excluding VAT. As the farm is situated far

away from the nearest town and Faith Immanuel did not want to waste planting time by

travelling, she purchased R16 790 (including VAT) worth of spare parts for the tractor together

with the tractor.

7. During the financial year, produce from the farm was used for family consumption. The

estimated cost of the produce consumed was R3 200, with a corresponding open market

value of R3 600.

8. During the year, Faith Immanuel donated to charitable institutions as follows :

• Livestock- These animals had originally been acquired at a historical cost of N$8,900, but

their fair market value at the date of donation was N$12,400.

• Produce - The produced cost are valued at R6 700 and fair market value on the date of the

donation was RlO 800.

3

TAX601Y, Assessment 6

© NUST2025

|

|

4 Page 4 |

▲back to top |

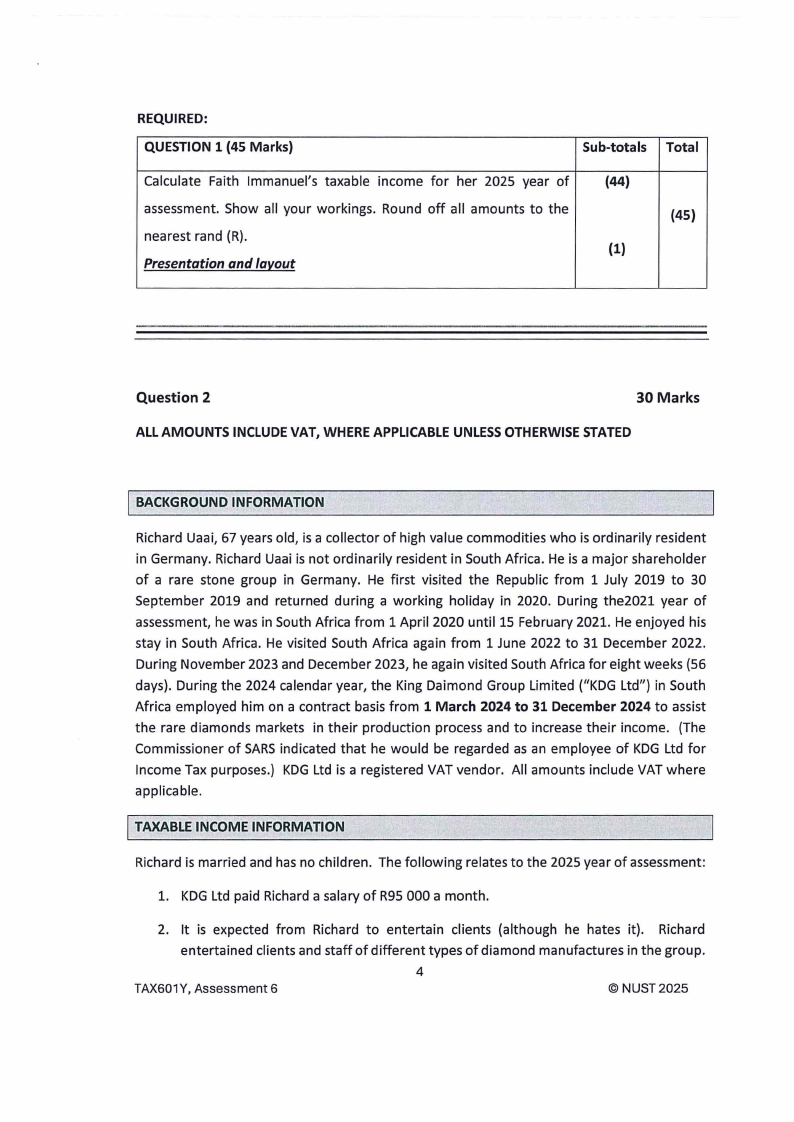

REQUIRED:

QUESTION 1 (45 Marks)

Sub-totals Total

Calculate Faith Immanuel's taxable income for her 2025 year of

(44)

assessment. Show all your workings. Round off all amounts to the

(45)

nearest rand (R).

(1)

Presentation and la'i_out

Question 2

30 Marks

ALL AMOUNTS INCLUDE VAT, WHERE APPLICABLE UNLESS OTHERWISE STATED

I BACKGROUND INFORMATION

Richard Uaai, 67 years old, is a collector of high value commodities who is ordinarily resident

in Germany. Richard Uaai is not ordinarily resident in South Africa. He is a major shareholder

of a rare stone group in Germany. He first visited the Republic from 1 July 2019 to 30

September 2019 and returned during a working holiday in 2020. During the2021 year of

assessment, he was in South Africa from 1 April 2020 until 15 February 2021. He enjoyed his

stay in South Africa. He visited South Africa again from 1 June 2022 to 31 December 2022.

During November 2023 and December 2023, he again visited South Africa for eight weeks (56

days). During the 2024 calendar year, the King Daimond Group Limited ("KDG Ltd") in South

Africa employed him on a contract basis from 1 March 2024 to 31 December 2024 to assist

the rare diamonds markets in their production process and to increase their income. (The

Commissioner of SARS indicated that he would be regarded as an employee of KDG Ltd for

Income Tax purposes.) KDG Ltd is a registered VAT vendor. All amounts include VAT where

applicable.

ITAXABLE INCOME INFORMATION

Richard is married and has no children. The following relates to the 2025 year of assessment:

1. KDG Ltd paid Richard a salary of R95 000 a month.

2. It is expected from Richard to entertain clients (although he hates it). Richard

entertained clients and staff of different types of diamond manufactures in the group.

4

TAX601Y, Assessment 6

© NUST2025

|

|

5 Page 5 |

▲back to top |

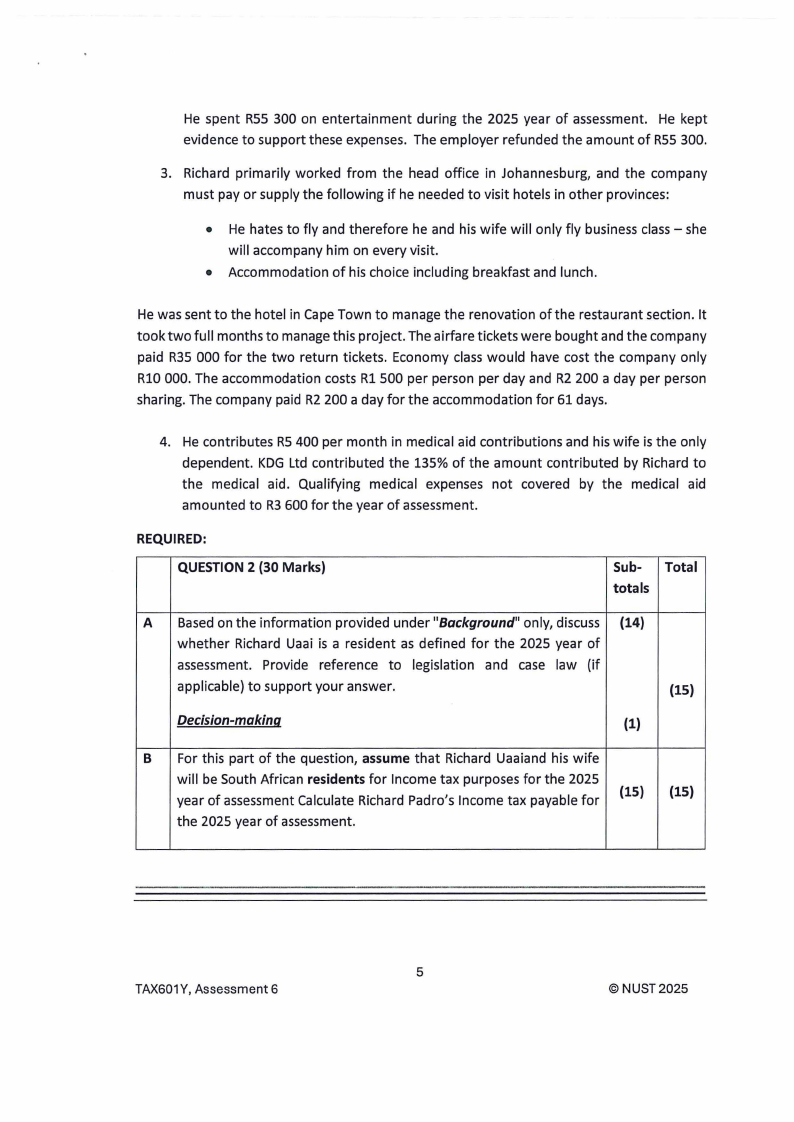

He spent RSS 300 on entertainment during the 2025 year of assessment. He kept

evidence to support these expenses. The employer refunded the amount of RSS 300.

3. Richard primarily worked from the head office in Johannesburg, and the company

must pay or supply the following if he needed to visit hotels in other provinces:

• He hates to fly and therefore he and his wife will only fly business class - she

will accompany him on every visit.

• Accommodation of his choice including breakfast and lunch.

He was sent to the hotel in Cape Town to manage the renovation of the restaurant section. It

took two full months to manage this project. The airfare tickets were bought and the company

paid R35 000 for the two return tickets. Economy class would have cost the company only

Rl0 000. The accommodation costs Rl 500 per person per day and R2 200 a day per person

sharing. The company paid R2 200 a day for the accommodation for 61 days.

4. He contributes RS 400 per month in medical aid contributions and his wife is the only

dependent. KDG Ltd contributed the 135% of the amount contributed by Richard to

the medical aid. Qualifying medical expenses not covered by the medical aid

amounted to R3 600 for the year of assessment.

REQUIRED:

QUESTION 2 {30 Marks)

Sub- Total

totals

A Based on the information provided under "Background" only, discuss (14)

whether Richard Uaai is a resident as defined for the 2025 year of

assessment. Provide reference to legislation and case law (if

applicable) to support your answer.

{15)

Decision-making

(1)

B For this part of the question, assume that Richard Uaaiand his wife

will be South African residents for Income tax purposes for the 2025

(15) (15)

year of assessment Calculate Richard Padro's Income tax payable for

the 2025 year of assessment.

5

TAX601 Y, Assessment 6

© NUST2025

|

|

6 Page 6 |

▲back to top |

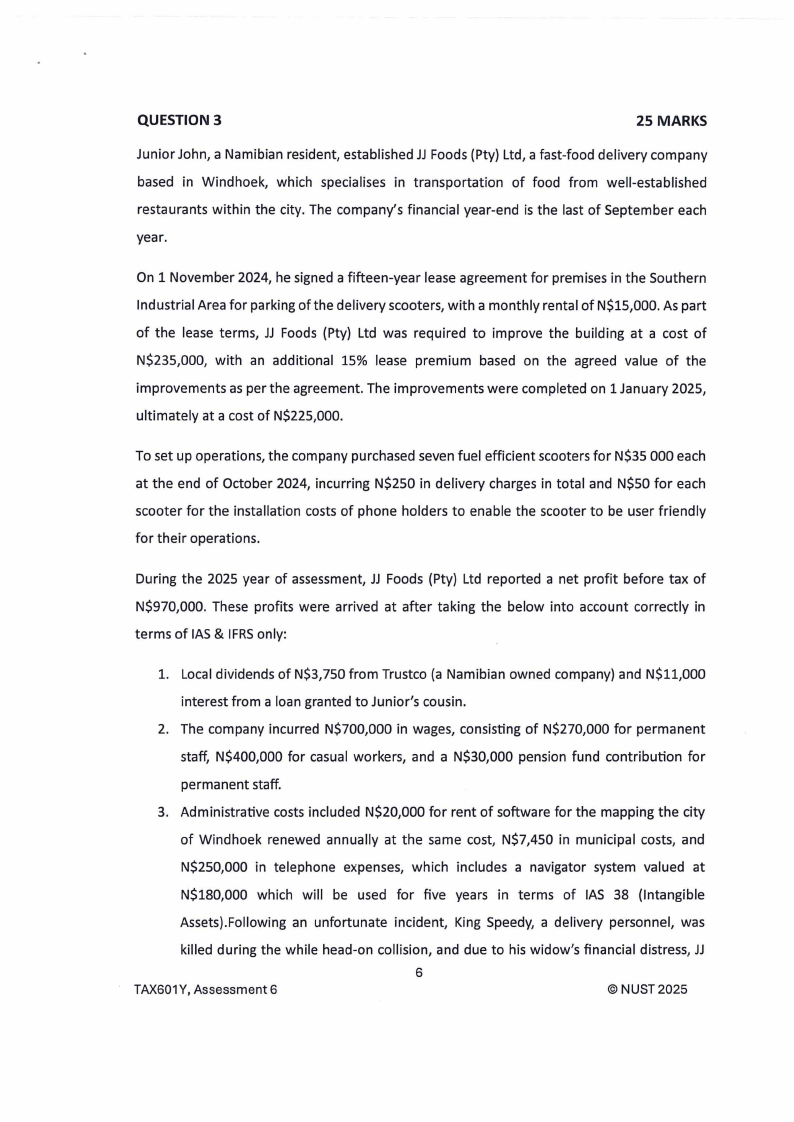

QUESTION 3

25 MARKS

Junior John, a Namibian resident, established JJ Foods (Pty) Ltd, a fast-food delivery company

based in Windhoek, which specialises in transportation of food from well-established

restaurants within the city. The company's financial year-end is the last of September each

year.

On 1 November 2024, he signed a fifteen-year lease agreement for premises in the Southern

Industrial Area for parking of the delivery scooters, with a monthly rental of N$15,000. As part

of the lease terms, JJ Foods (Pty) Ltd was required to improve the building at a cost of

N$235,000, with an additional 15% lease premium based on the agreed value of the

improvements as per the agreement. The improvements were completed on 1 January 2025,

ultimately at a cost of N$225,000.

To set up operations, the company purchased seven fuel efficient scooters for N$35 000 each

at the end of October 2024, incurring N$250 in delivery charges in total and N$50 for each

scooter for the installation costs of phone holders to enable the scooter to be user friendly

for their operations.

During the 2025 year of assessment, JJ Foods (Pty) Ltd reported a net profit before tax of

N$970,000. These profits were arrived at after taking the below into account correctly in

terms of IAS & IFRS only:

1. Local dividends of N$3,750 from Trustco (a Namibian owned company) and N$11,000

interest from a loan granted to Junior's cousin.

2. The company incurred N$700,000 in wages, consisting of N$270,000 for permanent

staff, N$400,000 for casual workers, and a N$30,000 pension fund contribution for

permanent staff.

3. Administrative costs included N$20,000 for rent of software for the mapping the city

of Windhoek renewed annually at the same cost, N$7,450 in municipal costs, and

N$250,000 in telephone expenses, which includes a navigator system valued at

N$180,000 which will be used for five years in terms of IAS 38 (Intangible

Assets).Following an unfortunate incident, King Speedy, a delivery personnel, was

killed during the while head-on collision, and due to his widow's financial distress, JJ

6

TAX601Y, Assessment 6

© NUST 2025

|

|

7 Page 7 |

▲back to top |

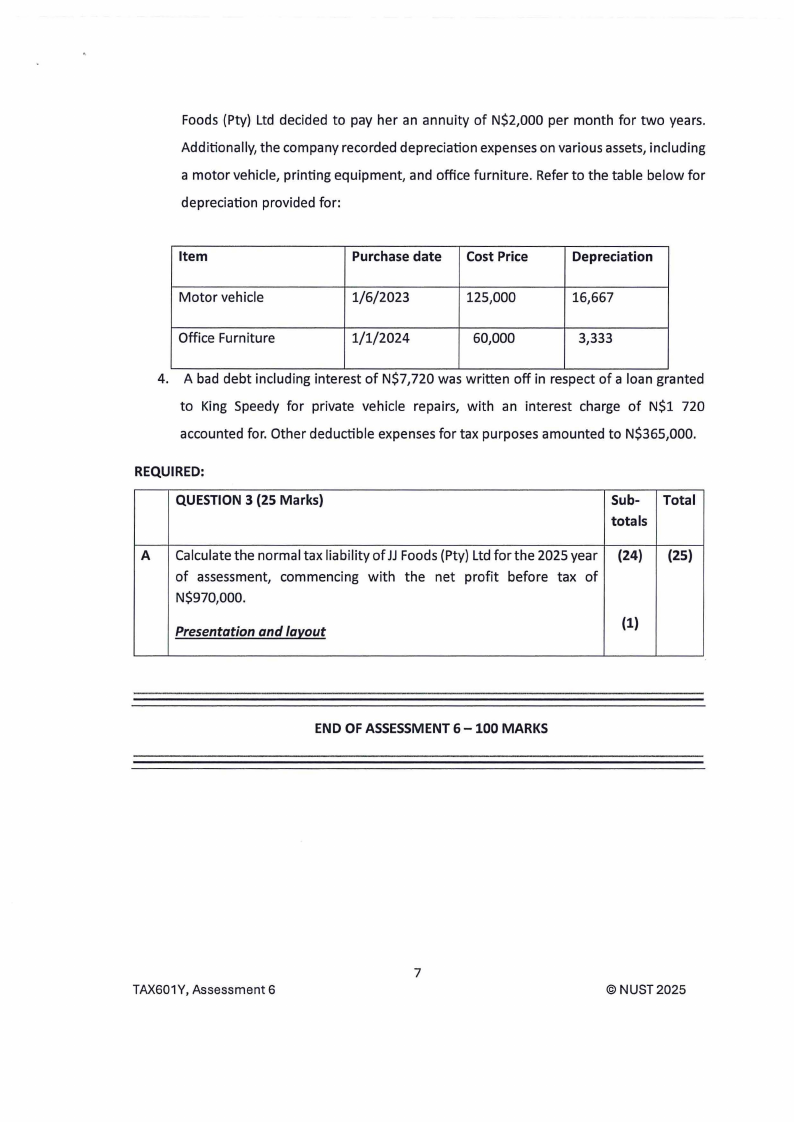

Foods (Pty) Ltd decided to pay her an annuity of N$2,000 per month for two years.

Additionally, the company recorded depreciation expenses on various assets, including

a motor vehicle, printing equipment, and office furniture. Refer to the table below for

depreciation provided for:

Item

Purchase date Cost Price

Depreciation

Motor vehicle

1/6/2023

125,000

16,667

Office Furniture

1/1/2024

60,000

3,333

4. A bad debt including interest of N$7,720 was written off in respect of a loan granted

to King Speedy for private vehicle repairs, with an interest charge of N$1 720

accounted for. Other deductible expenses for tax purposes amounted to N$365,000.

REQUIRED:

QUESTION 3 (25 Marks)

Sub- Total

totals

A Calculate the normal tax liability of JJ Foods (Pty) Ltd for the 2025 year (24) (25)

of assessment, commencing with the net profit before tax of

N$970,000.

(1)

Presentation and la'l,out

END OF ASSESSMENT 6 - 100 MARKS

7

TAX601Y, Assessment 6

© NUST 2025

|

|

8 Page 8 |

▲back to top |

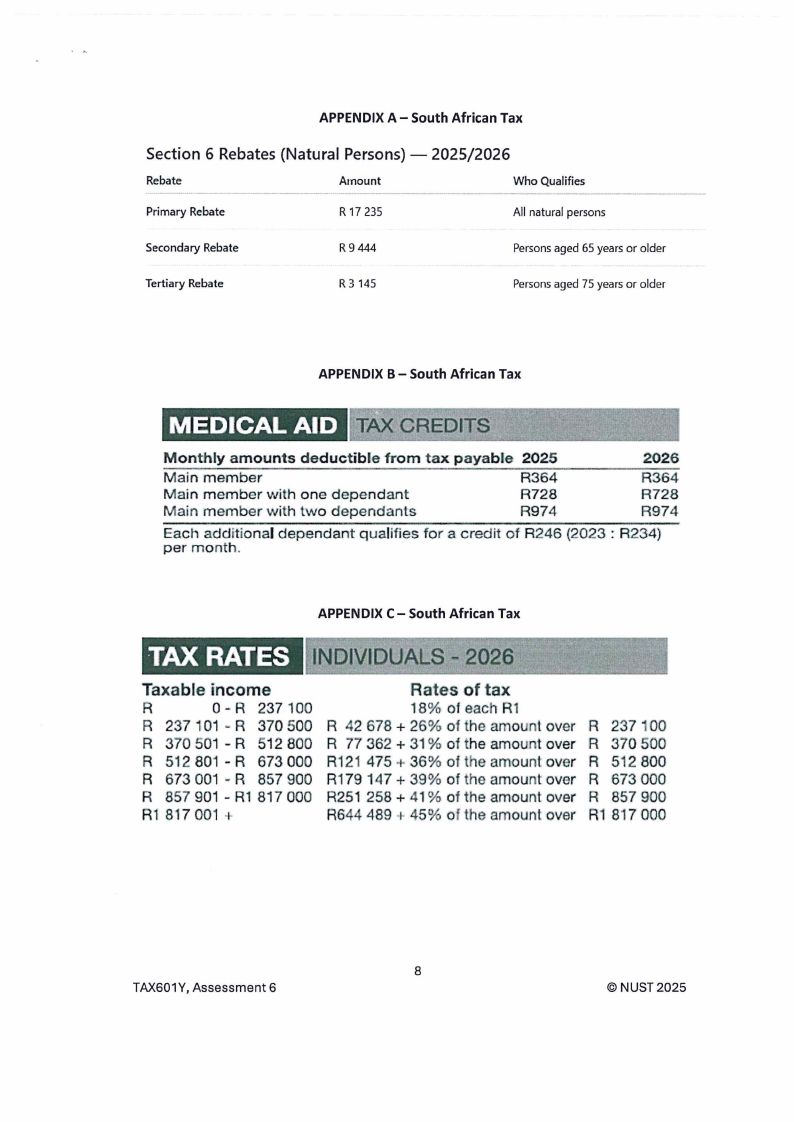

APPENDIX A - South African Tax

Section 6 Rebates (Natural Persons) - 2025/2026

Rebate

--·---·-•· --- --------

Primary Rebate

Amount

R 17 235

Who Qualifies

All natural persons

Secondary Rebate

R9444

Persons aged 65 years or older

Tertiary Rebate

R 3 145

Persons aged 75 years or older

APPENDIX B - South African Tax

MEDICAL AID TAX CREDITS

Monthly amounts deductible from tax payable 2025

2026

Main member

Main member with one dependant

Main m ember w ith two dependants

R364

R728

R974

R364

R728

R974

Each additional dependant q ualifies fo r a cred it ot R246 {2023 : R234)

per month.

APPENDIX C - South African Tax

,TAX RATES INDIVIDUALS - 2026

Taxable income

R

O- R 237 100

R 237 101 - R 370 500

R 370 501 - R 512 800

R 512 801 - R 673 000

R 673 001 - R 857 900

R 857 901 - R1 81 7 000

Rl 817 001 ·I

Rates of tax

18% of each R1

R 42 678 + 26% of the amount over

R 77 362 + 31 % of the amount over

R12 1 475 + 36 % of t e amount' over

R179 147 + 39 % of the amount over

R251 258 + 41% of the amount over

R644 489 + 45% of the amoun t over

R 237 100

R 370 00

R 512 800

R 673 000

R 857 900

R1 817 000

8

TAX601Y, Assessment 6

© NUST 2025