|

FMH810S- FINANCIAL MANAGEMENT FOR HOSPITALITY AND TOURISM- 1ST OPP-JUNE 2025 |

|

|

1 Page 1 |

▲back to top |

nAmlBIA UnlVERSITY

OF SCIEnCE Ano TECHnDLOGY

FACULTYOFCOMMERCEH, UMANSCIENCEAS ND EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING & FINANCE

QUALIFICATION: BACHELOR OF HOSPITALITY AND

TOURISM MANAGEMENT HONOURS

QUALIFICATION CODE: 08BHTH

LEVEL: 8

COURSE CODE: FMH810S

COURSE NAME: FINANCIAL MANAGEMENT FOR

HOSPITALITY AND TOURISM

SESSION: JUNE 2025

DURATION: 3 HOURS

PAPER: THEORY AND APPLICATION

MARKS: 100

FIRST OPPORTUNITY EXAMINATION QUESTION PAPER

EXAMINERS:

Kuhepa Tjondu

MODERATOR: Mr. A Okafor

INSTRUCTIONS

• This question paper is made up of FOUR(4) questions.

• Start each question on a new page.

• Answer All the questions and in blue or black ink.

• You are advised to pay due attention to expression and presentation. Failure to do so will

cost you marks.

• Start each question on a new page in your answer booklet and show all your workings.

• Questions relating to this paper may be raised in the initial 30 minutes after the start of

the paper. Thereafter, candidates must use their initiative to deal with any perceived error

or ambiguities and any assumption made by the candidate should be clearly stated.

PERMISSIBLE MATERIALS

Non-programmable calculator/financial calculator

THIS QUESTION PAPER CONSISTS OF 7 PAGES (Including this front page)

1

|

|

2 Page 2 |

▲back to top |

Question 1

(25 marks)

The independent board of governors of the state-funded Oukongo school for 11- to

16-year-old children met to consider its most recent set of public examination results.

(The board of governors is an independent oversight body, comprised of local

residents, parents and other concerned citizens).

One of the key responsibilities placed upon the school's governors is the delivery, to

its local government authority, of a report on exam performance in a full and timely

manner. A report on both the exam results and the reasons for any improvement or

deterioration over previous years are required from the governors each year.

Accordingly, the annual meeting on exam performance was always considered to be

very important. Although the school taught the national curriculum (a standard syllabus

taught in all schools in the country) as required of it, the exam results at Oukongo had

deteriorated in recent years and on this particular occasion, they were very poor

indeed.

In order to address the weaknesses in the school, Oukongo's budget had increased

in recent years and a number of new teachers had been employed to help improve

results. Despite this, exam performance continued to fal I. A recent overspend against

budget was funded through the closure of part of the school library and the sale of a

sports field.

One member of the board of governors was Sally Murorua. She believed that the local

government authority might attempt to close Oukongo school if these exam results

were reported with no convincing explanation. One solution to avoid this threat, she

said, was to either send the report in late or to select only the best results and submit

a partial report so the school's performance looked better than it actually was. There

is no central computerised exam results service in the country in which Oukongo is

located by which the local authority could establish the exam performance at Oukongo

school.

A general feeling at the governors' meeting was that the school needed some new

leadership, and it might be time to remove the existing headteacher. Mr Mbeze had

been in the role for many years and his management style was thought to be

ineffective. He was widely liked by staff in the school because he believed that each

teacher knew best how to manage their teaching, and so he tried not to intervene

wherever possible. Mr Mbeze had sometimes disagreed with the governors when they

suggested changes which could be made to improve exam performance, preferring to

rely on what he believed were tried and tested ways of managing his teaching staff.

He was thought to be very loyal to long-standing colleagues and had a dislike of

confrontation.

REQUIRED:

(a) Explain, using evidence from the case, the characteristics which identify

Oukongo school as a public sector organisation and assess how its (10)

objectives as a public sector orQanisation have not been met.

(b)

Explain the roles of a board of governors in the governance of Oukongo

school, and discuss, in the context of Sally Murorua's suaaestion, the

(9)

2

|

|

3 Page 3 |

▲back to top |

importance of transparency in the board of governors' dealings with the local

Qovernment authority.

(c)

Discuss the potential advantages to Oukongo school of replacing the

headteacher as part of the process of addressinQ its problems.

(6)

TOTAL

(25)

Question 2

(25 marks)

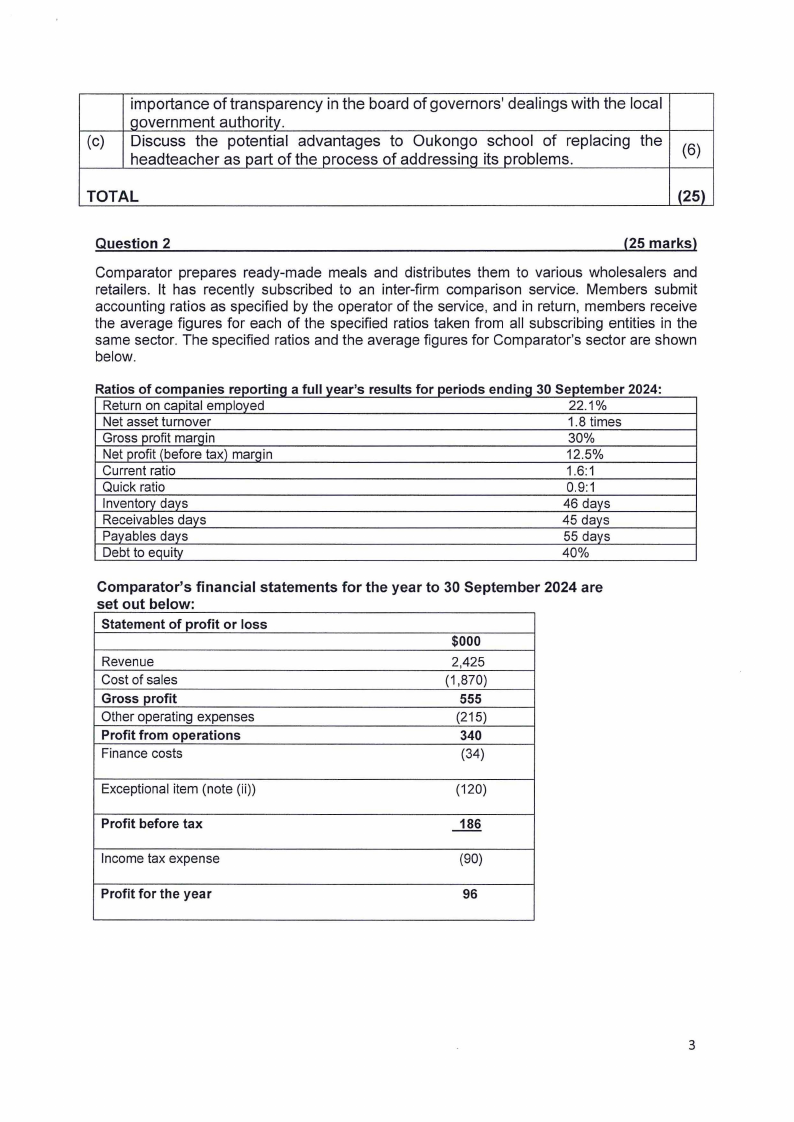

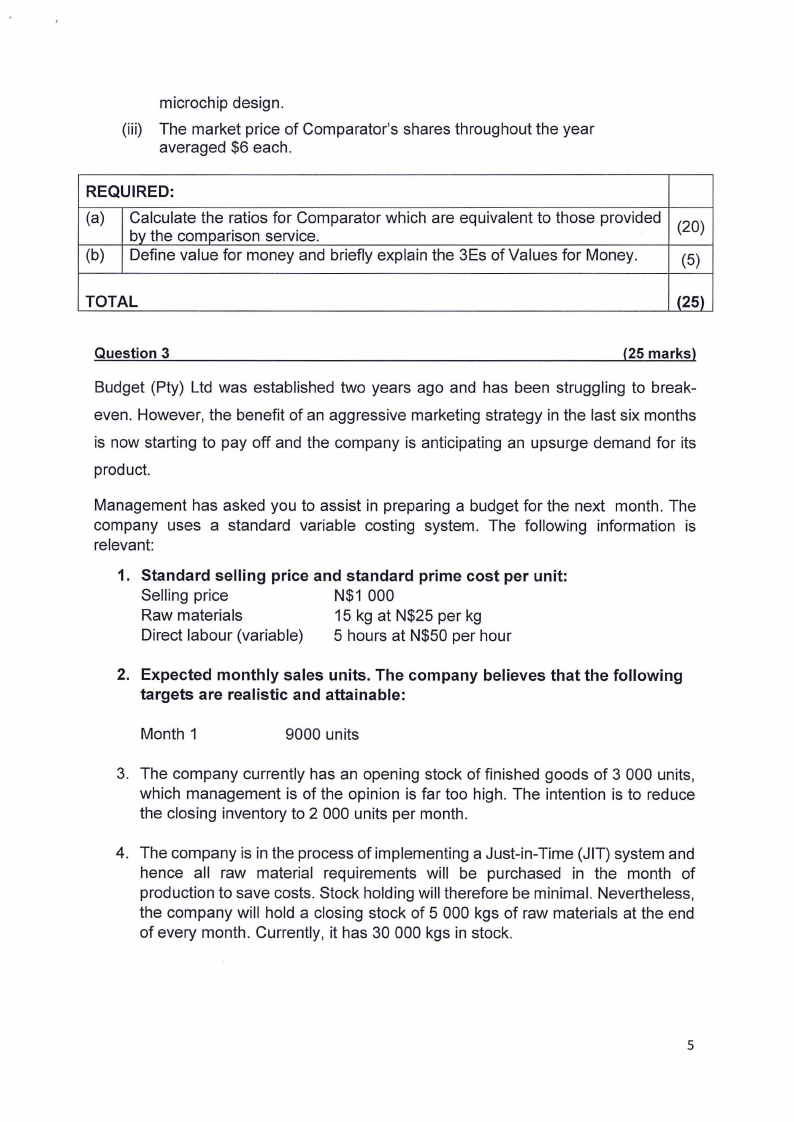

Comparator prepares ready-made meals and distributes them to various wholesalers and

retailers. It has recently subscribed to an inter-firm comparison service. Members submit

accounting ratios as specified by the operator of the service, and in return, members receive

the average figures for each of the specified ratios taken from all subscribing entities in the

same sector. The specified ratios and the average figures for Comparator's sector are shown

below.

Rat1. os of companies reporting a fuII year s resu Its for peri.o ds end.mg 30 Septem ber 2024

Return on capital employed

22.1%

Net asset turnover

1.8 times

Gross profit marqin

30%

Net profit (before tax) marqin

12.5%

Current ratio

1.6:1

Quick ratio

0.9:1

Inventory days

46 days

Receivables days

45 days

Payables days

55 days

Debt to equity

40%

Comparator's financial statements for the year to 30 September 2024 are

set out below:

Statement of profit or loss

$000

Revenue

2,425

Cost of sales

(1,870)

Gross profit

555

Other operating expenses

(215)

Profit from operations

340

Finance costs

(34)

Exceptional item (note (ii))

(120)

Profit before tax

186

Income tax expense

(90)

Profit for the year

96

3

|

|

4 Page 4 |

▲back to top |

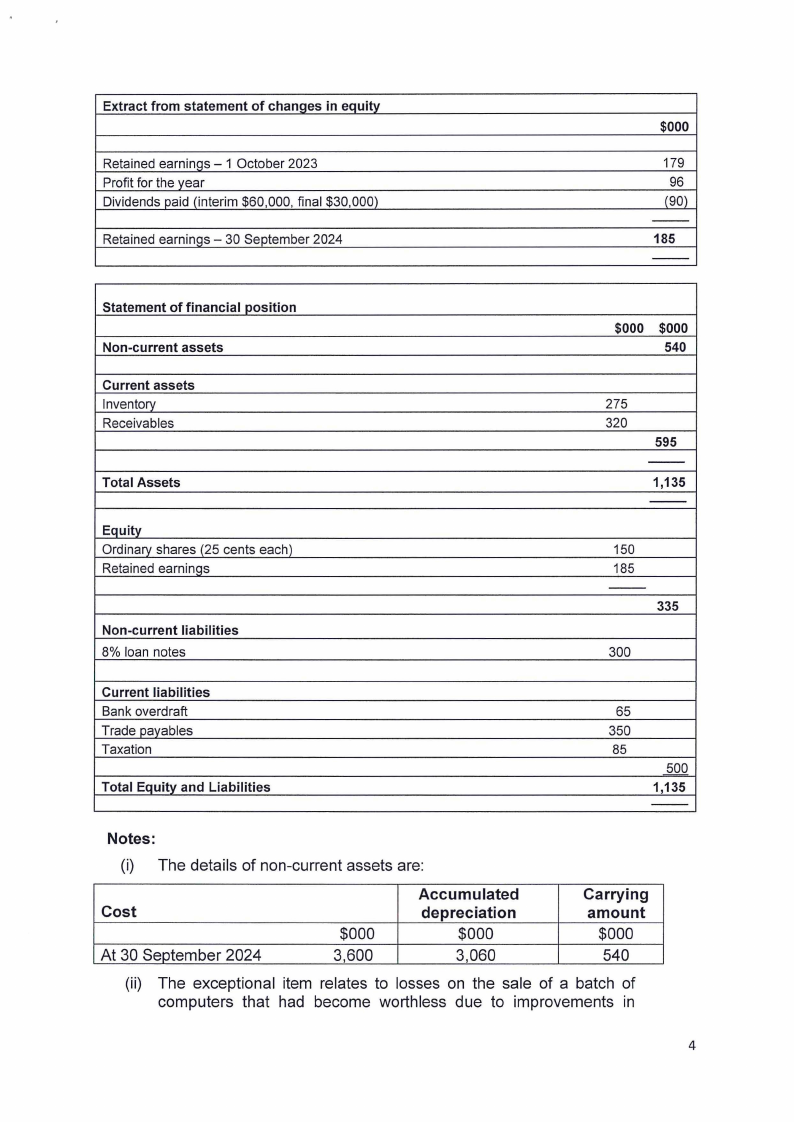

Extract from statement of changes in equity

Retained earnings - 1 October 2023

Profit for the year

Dividends paid (interim $60,000, final $30,000)

Retained earnings - 30 September 2024

$000

179

96

(90)

--

185

--

Statement of financial position

Non-current assets

$000 $000

540

Current assets

Inventory

Receivables

Total Assets

EQuitv

Ordinary shares (25 cents each)

Retained earnings

Non-current liabilities

8% loan notes

275

320

595

--

1,135

--

150

185

--

335

300

Current liabilities

Bank overdraft

Trade payables

Taxation

Total Equity and Liabilities

65

350

85

500

1,135

--

Notes:

(i) The details of non-current assets are:

Cost

At 30 September 2024

$000

3,600

Accumulated

depreciation

$000

3,060

Carrying

amount

$000

540

(ii) The exceptional item relates to losses on the sale of a batch of

computers that had become worthless due to improvements in

4

|

|

5 Page 5 |

▲back to top |

microchip design.

(iii) The market price of Comparator's shares throughout the year

averaged $6 each.

REQUIRED:

(a)

Calculate the ratios for Comparator which are equivalent to those provided

by the comparison service.

(20)

(b) Define value for money and briefly explain the 3Es of Values for Money.

(5)

TOTAL

(25)

Question 3

(25 marks)

Budget (Pty) Ltd was established two years ago and has been struggling to break-

even. However, the benefit of an aggressive marketing strategy in the last six months

is now starting to pay off and the company is anticipating an upsurge demand for its

product.

Management has asked you to assist in preparing a budget for the next month. The

company uses a standard variable costing system. The following information is

relevant:

1. Standard selling price and standard prime cost per unit:

Selling price

N$1 000

Raw materials

15 kg at N$25 per kg

Direct labour (variable) 5 hours at N$50 per hour

2. Expected monthly sales units. The company believes that the following

targets are realistic and attainable:

Month 1

9000 units

3. The company currently has an opening stock of finished goods of 3 000 units,

which management is of the opinion is far too high. The intention is to reduce

the closing inventory to 2 000 units per month.

4. The company is in the process of implementing a Just-in-Time (JIT) system and

hence all raw material requirements will be purchased in the month of

production to save costs. Stock holding will therefore be minimal. Nevertheless,

the company will hold a closing stock of 5 000 kgs of raw materials at the end

of every month. Currently, it has 30 000 kgs in stock.

5

|

|

6 Page 6 |

▲back to top |

REQUIRED:

(a) Prepare the following functional budgets for Months 1:

(i) Sales Budget (units and value)

(3)

(ii) Production Budget

(4)

(iii) Material usage and purchases Budget (units and value)

(8)

(iv) Direct labour Budget (hours and value)

(5)

(b) Name and briefly explain FIVE (5) uses or purposes of budgeting

(5)

TOTAL

(25)

Question 4

(25 marks)

Ms. Elaine is a businesswoman who is running a successful hospitality and tourism

company in Namibia. Ms. Elaine believes that the organization must embrace

emerging technology if it is to compete in the highly competitive Tourism Sector of

Namibia. She attended a workshop last week where she learned that "Big data is a

term for a collection of data which is so large that it becomes difficult to store and

process using traditional databases and data processing applications". Big data often

also includes more than simply financial information and can involve other

organizational data (both internal and external) which is often unstructured.

Her business partner Ms. Abbi agreed that the organization must embrace technology

but it is important to understand the advantages and possible disadvantages of any

emerging technology by it can be adopted by the organization.

REQUIRED:

(a)

Name and explain the characteristics of big data which are also known as

the 5Vs.

(10)

(b) Explain the possible disadvantages and/or risks of Big Data?

(8)

(c) List Seven (7) benefits of using Big Data?

(7)

TOTAL

(25)

6

|

|

7 Page 7 |

▲back to top |

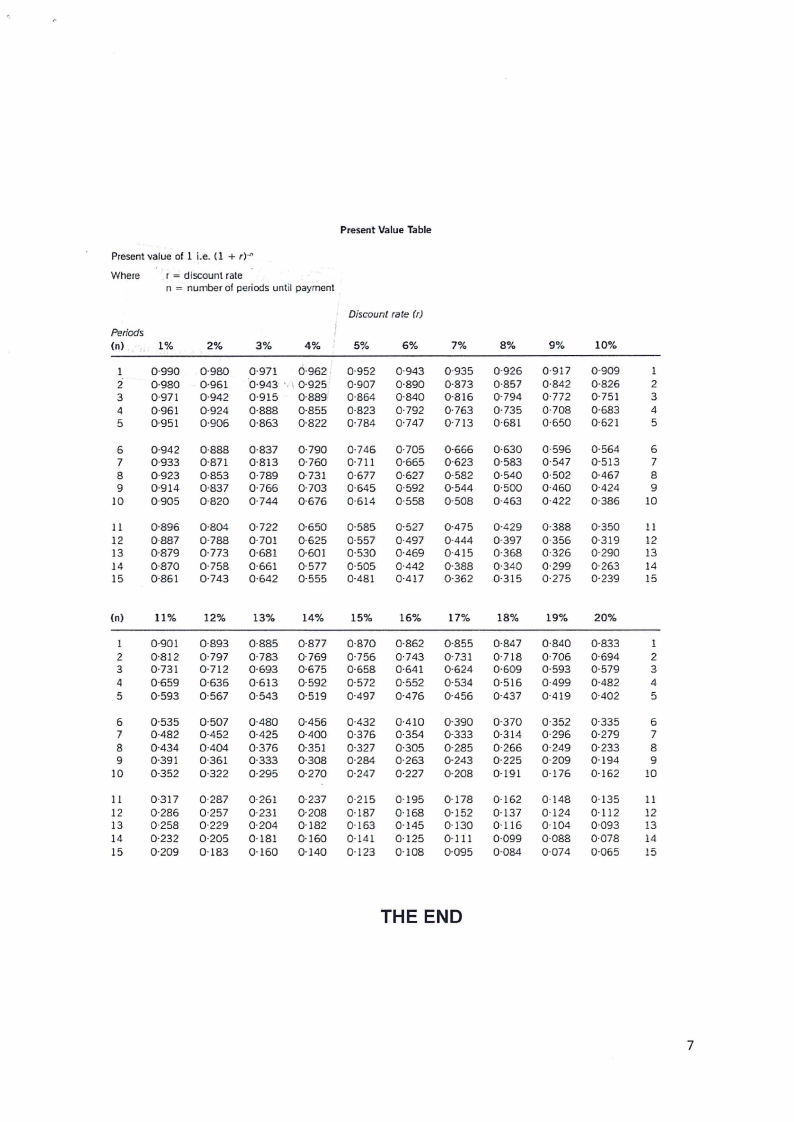

Present Value Table

Present value of 1 i.e. (1 + r)-"

Where

r = discount rate

n = number of periods until payment

Discount rate (rJ

Periods

(n) ..

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

1

0·990 0·980 0·971 0·962 0·952 0·943 0·935 0·926 0·917 0·909

1

2

0·980 0·961 ·o-943· ·. \\ 0-925 0·907 0·890 0·873 0·857 0·842 0·826

2

3

0·971 0·942 0·915 0·889 0·864 0·840 0·816 0·794 0·772 0·751

3

4

0·961 0·924 0·888 0·855 0·823 0·792 0·763 0·735 0·708 0·683

4

5

0·951 0·906 0·863 0·822 0·784 0·747 0·713 0·681 0·650 0·621

5

6

0·942 0·888 0·837 0·790 0·746 0·705 0·666 0·630 0·596 0·564

6

7

0·933 0·871 0·813 0·760 0·711 0·665 0·623 0·583 0·547 0·513

7

8

0·923 0·853 0·789 0·731 0·677 0·627 0·582 0·540 0·502 0·467

8

9

0·914 0·837 0·766 0·703 0·645 0·592 0·544 0·500 0·460 0·424

9

10

0·905 0·820 0·744 0·676 0·614 0·558 0·508 0·463 0·422 0·386

10

Il

0·896 0·804 0·722 0·650 0·585 0·527 0·475 0·429 0·388 0·350

11

12

0·887 0·788 0·70! 0·625 0·557 0·497 0·444 0·397 0·356 0·319

12

13

0·879 0·773 0·681 0·601 0·530 0-469 0·415 0·368 0·326 0·290

13

14

0·870 0·758 0·661 0·577 0·505 0·442 0·388 0·340 0·299 0·263

14

15

0·861 0·743 0·642 0·555 0·481 0-417 0·362 0·315 0·275 0·239

15

(n)

11%

12%

13%

14%

15%

16%

17%

18%

19%

20%

1 0·901 0·893 0·885 0·877 0·870 0·862 0·855 0·847 0·840 0·833

I

2

0·812 0·797 0·783 0·769 0·756 0·743 0·731 0·718 0·706 0·694

2

3

0·731 0·712 0·693 0·675 0·658 0·641 0·624 0·609 0·593 0·579

3

4

0·659 0·636 0·613 0·592 0·572 0·552 0·534 0·516 0-499 0·482

4

5

0·593 0·567 0·543 0·519 0·497 0·476 0·456 0·437 0·419 0·402

5

6

0·535 0·507 0·480 0·456 0·432 0-410 0·390 0·370 0352

0·335

6

7

0-482 0·452 0·425 0·400 0·376 0·354 0·333 0·314 0·296 0·279

7

8

0·434 0·404 0·376 0·351 0·327 0·305 0·285 0·266 0·249 0·233

8

9

0·391 0·361 0·333 0·308 0·284 0·263 0·243 0·225 0·209 0·194

9

10

0·352 0·322 0·295 0·270 0·247 0·227 0·208 0·191 0·176 0·162

!O

II

0·317 0·287 0·261 0·237 0·215 0·195 0·178 0·162 0·!48 0·135

l!

12

0·286 0·257 0·231 0·208 0·187 0·168 0·152 0·137 0·124 0·112

12

13

0·258 0·229 0·204 0·182 0·163 0·145 0·130 0· 116 0·104 0·093

13

14

0·232 0·205 0· 18! 0·160 0· 141 0·125 0·111 0·099 0·088 0·078

14

15

0·209 0·183 0·!60 0·140 0·123 0·108 0·095 0·084 0·074 0·065

15

THE END

7