|

CMA611S-COST AND MANAGEMENT ACCOUNTING 201-1ST OPP- JUNE 2025 |

|

|

1 Page 1 |

▲back to top |

nAmlBIA UnlVERSITY

0 F SCIEn CE Ano TECHn OLOGY

FACULTY OF COMMERCE, HUMAN SCIENCES AND EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING AND FINANCE

QUALIFICATION: BACHELOR OF ACCOUNTING

QUALIFICATION CODE: 07BGAC

LEVEL: 6

COURSE CODE: CMA611S

COURSE NAME: COST & MANAGEMENT ACCOUNTING 201

SESSION: JUNE 2025

DURATION: 3 HOURS

PAPER: THEORY AND CALCULATIONS

MARKS: 100

EXAMINERS

FIRST OPPORTUNITY EXAMINATION QUESTION PAPER

Mrs Modestus, M., Ms Mkhulisi, M., Ms Shikoyeni, F .,and Sheehama, K.G.H.

MODERATOR Kangala, H.

INSTRUCTIONS

• Answer ALL the questions in blue or black ink only. NO PENCIL.

• Start each question on a new page, number the answers correctly and clearly.

• Write clearly, and neatly showing all your workings/assumptions.

• Work with at least four (4) decimal places in all your calculations and only round off only

final answers to two (2) decimal places.

• Questions relating to this examination may be raised in the initial 30 minutes after the start

of the examination. Thereafter, candidates must use their initiative to deal with any

perceived errors or ambiguities and any assumptions made by the candidate should be

clearly stated.

PERMISSIBLE MATERIALS

• Silent, non-programmable calculators

THIS QUESTION PAPER CONSISTS OF _6_ PAGES (excluding this front page)

0

|

|

2 Page 2 |

▲back to top |

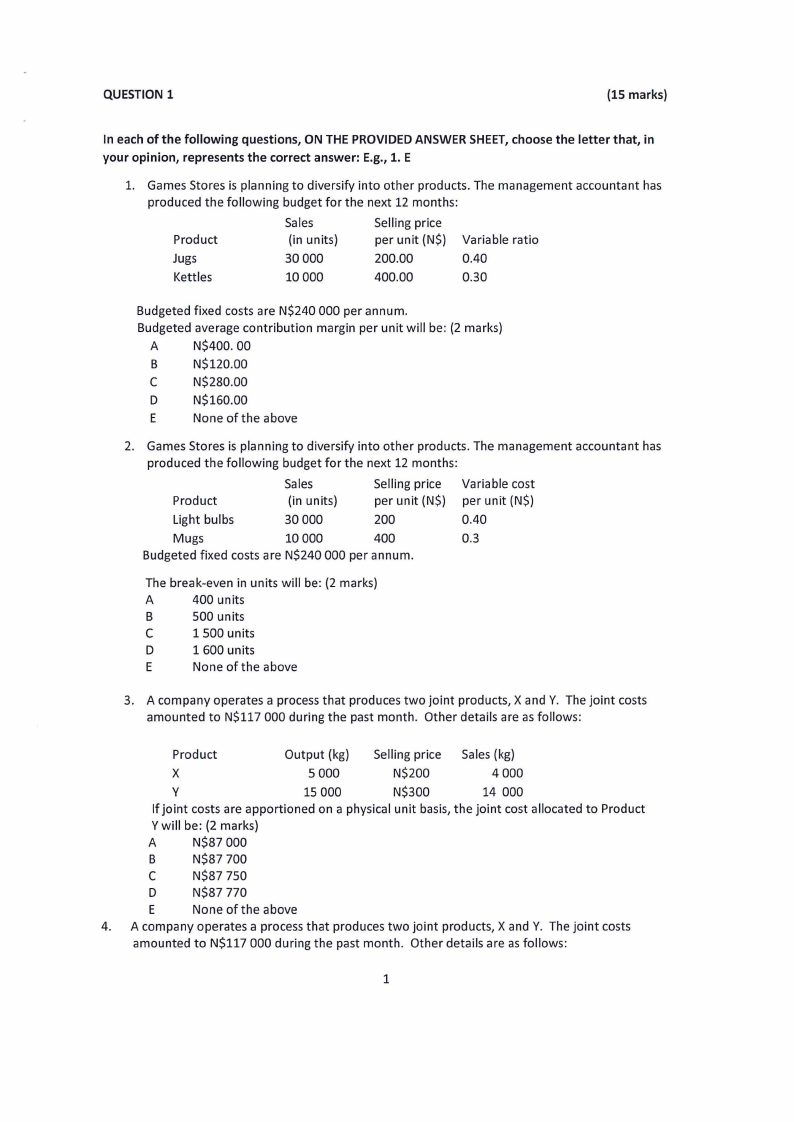

QUESTION 1

(15 marks)

In each of the following questions, ON THE PROVIDED ANSWER SHEET, choose the letter that, in

your opinion, represents the correct answer: E.g., 1. E

1. Games Stores is planning to diversify into other products. The management accountant has

produced the following budget for the next 12 months:

Product

Sales

(in units)

Selling price

per unit (N$) Variable ratio

Jugs

30000

200.00

0.40

Kettles

10000

400.00

0.30

Budgeted fixed costs are N$240 000 per annum.

Budgeted average contribution margin per unit will be: (2 marks)

A

N$400.00

B

N$120.00

C

N$280.00

D

N$160.00

E

None of the above

2. Games Stores is planning to diversify into other products. The management accountant has

produced the following budget for the next 12 months:

Product

Sales

(in units)

Selling price Variable cost

per unit (N$) per unit (N$)

Light bulbs

30 000

200

0.40

Mugs

10 000

400

0.3

Budgeted fixed costs are N$240 000 per annum.

The break-even in units will be: (2 marks)

A

400 units

B

500 units

C

1 500 units

D

1 600 units

E

Noneoftheabove

3. A company operates a process that produces two joint products, X and Y. The joint costs

amounted to N$117 000 during the past month. Other details are as follows:

Product

Output (kg) Selling price Sales (kg)

X

5 000

N$200

4 000

y

15 000

N$300

14 000

If joint costs are apportioned on a physical unit basis, the joint cost allocated to Product

Y will be: (2 marks)

A

N$87 000

B

N$87 700

C

N$87 750

D

N$87 770

E

None of the above

4. A company operates a process that produces two joint products, X and Y. The joint costs

amounted to N$117 000 during the past month. Other details are as follows:

1

|

|

3 Page 3 |

▲back to top |

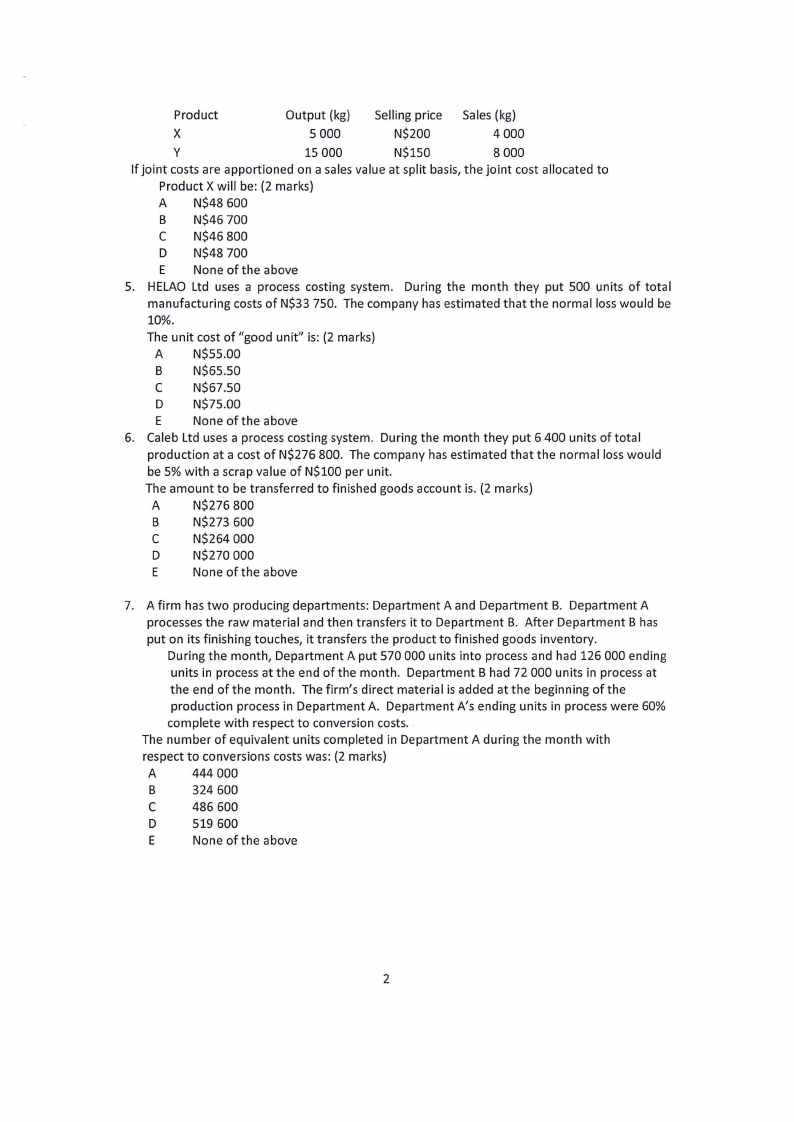

Product

Output (kg) Selling price Sales (kg)

X

5 000

N$200

4000

y

15 000

N$150

8 000

If joint costs are apportioned on a sales value at split basis, the joint cost allocated to

Product X will be: (2 marks)

A N$48 600

B N$46 700

C N$46 800

D N$48 700

E None of the above

5. HELAO Ltd uses a process costing system. During the month they put 500 units of total

manufacturing costs of N$33 750. The company has estimated that the normal loss would be

10%.

The unit cost of "good unit" is: (2 marks)

A N$55.00

B N$65.50

C N$67.50

D N$75.00

E None of the above

6. Caleb Ltd uses a process costing system. During the month they put 6 400 units of total

production at a cost of N$276 800. The company has estimated that the normal loss would

be 5% with a scrap value of N$100 per unit.

The amount to be transferred to finished goods account is. (2 marks)

A

N$276 800

B

N$273 600

C

N$264 000

D

N$270 000

E

None of the above

7. A firm has two producing departments: Department A and Department B. Department A

processes the raw material and then transfers it to Department B. After Department B has

put on its finishing touches, it transfers the product to finished goods inventory.

During the month, Department A put 570 000 units into process and had 126 000 ending

units in process at the end of the month. Department B had 72 000 units in process at

the end of the month. The firm's direct material is added at the beginning of the

production process in Department A. Department A's ending units in process were 60%

complete with respect to conversion costs.

The number of equivalent units completed in Department A during the month with

respect to conversions costs was: (2 marks)

A

444 000

B

324 600

C

486 600

D

519 600

E

None of the above

2

|

|

4 Page 4 |

▲back to top |

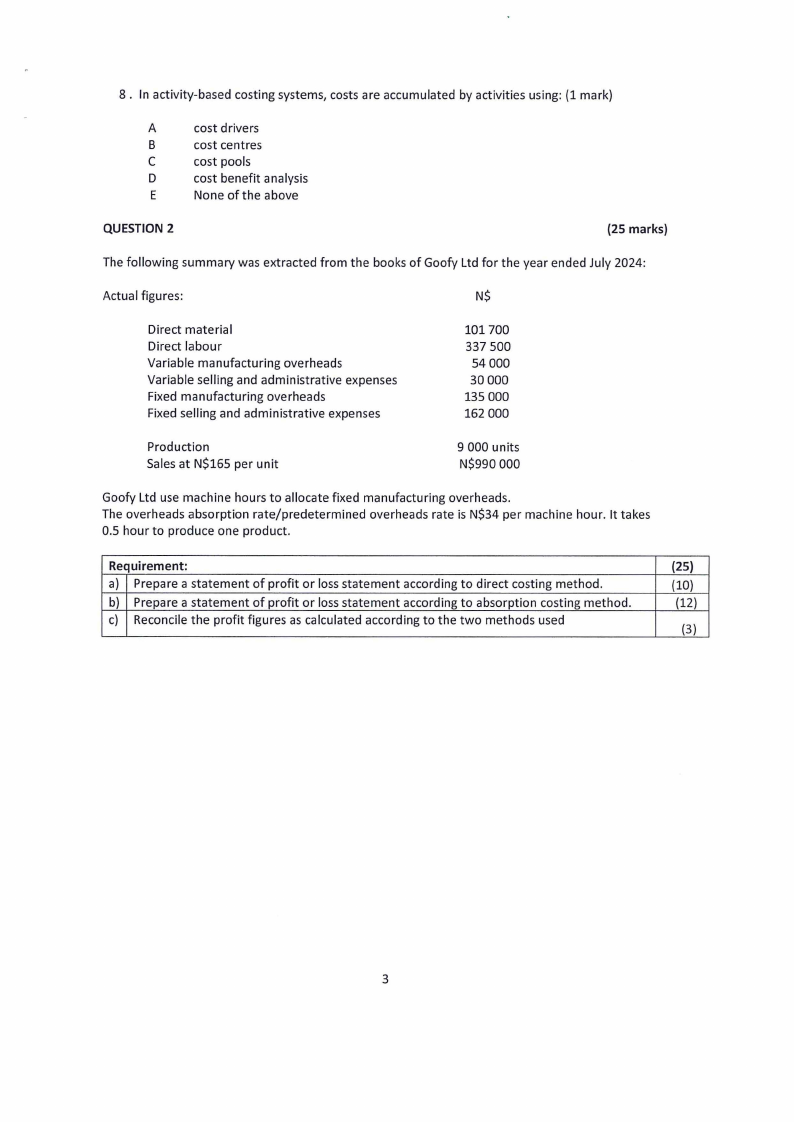

8. In activity-based costing systems, costs are accumulated by activities using: (1 mark)

A

cost drivers

B

cost centres

C

cost pools

D

cost benefit analysis

E

None of the above

QUESTION 2

{25 marks)

The following summary was extracted from the books of Goofy Ltd for the year ended July 2024:

Actual figures:

N$

Direct material

Direct labour

Variable manufacturing overheads

Variable selling and administrative expenses

Fixed manufacturing overheads

Fixed selling and administrative expenses

101 700

337 500

54 000

30 000

135000

162 000

Production

Sales at N$165 per unit

9 000 units

N$990 000

Goofy Ltd use machine hours to allocate fixed manufacturing overheads.

The overheads absorption rate/predetermined overheads rate is N$34 per machine hour. It takes

0.5 hour to produce one product.

Requirement:

a) Prepare a statement of profit or loss statement according to direct costing method.

b) Prepare a statement of profit or loss statement according to absorption costing method.

c) Reconcile the profit figures as calculated according to the two methods used

(25)

(10)

(12)

(3)

3

|

|

5 Page 5 |

▲back to top |

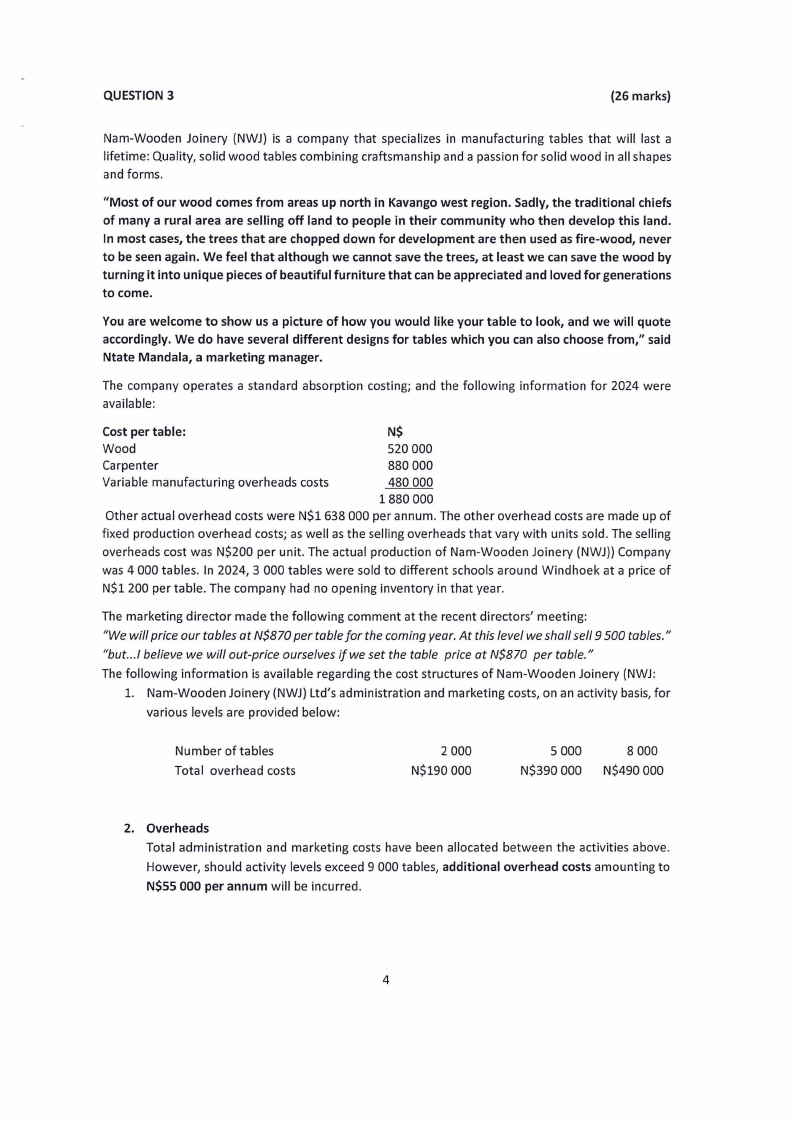

QUESTION 3

(26 marks)

Nam-Wooden Joinery (NWJ) is a company that specializes in manufacturing tables that will last a

lifetime: Quality, solid wood tables combining craftsmanship and a passion for solid wood in all shapes

and forms.

"Most of our wood comes from areas up north in Kavango west region. Sadly, the traditional chiefs

of many a rural area are selling off land to people in their community who then develop this land.

In most cases, the trees that are chopped down for development are then used as fire-wood, never

to be seen again. We feel that although we cannot save the trees, at least we can save the wood by

turning it into unique pieces of beautiful furniture that can be appreciated and loved for generations

to come.

You are welcome to show us a picture of how you would like your table to look, and we will quote

accordingly. We do have several different designs for tables which you can also choose from," said

Ntate Mandala, a marketing manager.

The company operates a standard absorption costing; and the following information for 2024 were

available:

Cost per table:

N$

Wood

520 000

Carpenter

880 000

Variable manufacturing overheads costs

480 000

1880 000

Other actual overhead costs were N$1 638 000 per annum. The other overhead costs are made up of

fixed production overhead costs; as well as the selling overheads that vary with units sold. The selling

overheads cost was N$200 per unit. The actual production of Nam-Wooden Joinery (NWJ)) Company

was 4 000 tables. In 2024, 3 000 tables were sold to different schools around Windhoek at a price of

N$1 200 per table. The company had no opening inventory in that year.

The marketing director made the following comment at the recent directors' meeting:

"We will price our tables at N$870 per table for the coming year. At this level we shall sell 9 500 tables."

"but.../ believe we will out-price ourselves if we set the table price at N$870 per table."

The following information is available regarding the cost structures of Nam-Wooden Joinery (NWJ:

1. Nam-Wooden Joinery (NWJ) Ltd's administration and marketing costs, on an activity basis, for

various levels are provided below:

Number of tables

Total overhead costs

2 000

N$190 000

5 000

N$390000

8 000

N$490000

2. Overheads

Total administration and marketing costs have been allocated between the activities above.

However, should activity levels exceed 9 000 tables, additional overhead costs amounting to

N$55 000 per annum will be incurred.

4

|

|

6 Page 6 |

▲back to top |

Requirement:

(26)

a) Determine the break-even point of Nam-Wooden Joinery (NWJ n units and value, for the

year 2024.

(8)

b) Comment on whether you agree or disagree with the marketing director's statement that

decreasing the selling price to N$870 will be detrimental, assuming the variable cost per unit

remains constant. (show all workings clearly).

(8)

c) Determine the new contribution margin per packet if Nam-Wooden Joinery (NWJ) would like

to sell 3 000 packets without making a loss or profit, assuming the variable cost per unit

remains constant.

(2)

d) What is the percentage increase or decrease in the selling price if Nam-Wooden Joinery

(NWJ ould like to sell 3 000 packets without making a loss or profit, assuming the variable

cost per unit remains constant?

(2)

e) What assumptions are usually made when using cost volume (CVP) analysis concerning the

costs?

(6)

5

|

|

7 Page 7 |

▲back to top |

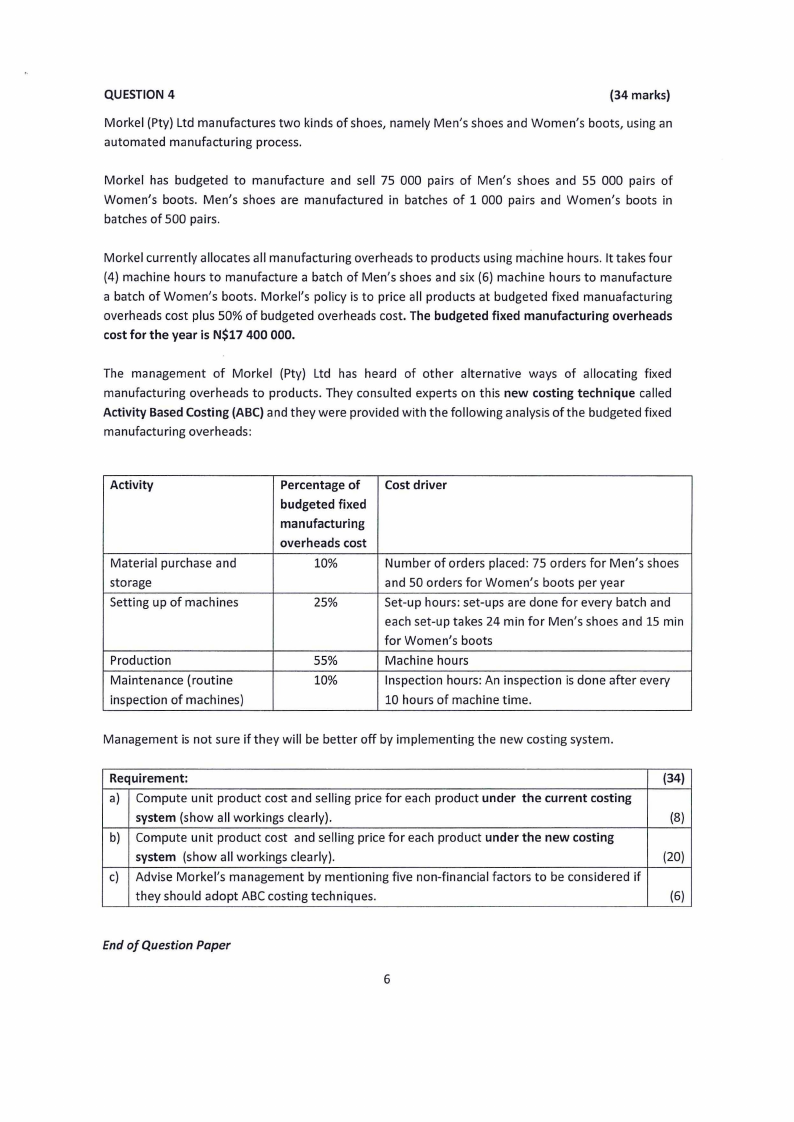

QUESTION 4

(34 marks)

Markel (Pty) Ltd manufactures two kinds of shoes, namely Men's shoes and Women's boots, using an

automated manufacturing process.

Markel has budgeted to manufacture and sell 75 000 pairs of Men's shoes and 55 000 pairs of

Women's boots. Men's shoes are manufactured in batches of 1 000 pairs and Women's boots in

batches of 500 pairs.

Markel currently allocates all manufacturing overheads to products using machine hours. It takes four

(4) machine hours to manufacture a batch of Men's shoes and six (6) machine hours to manufacture

a batch of Women's boots. Morkel's policy is to price all products at budgeted fixed manuafacturing

overheads cost plus 50% of budgeted overheads cost. The budgeted fixed manufacturing overheads

cost for the year is N$17 400 000.

The management of Markel (Pty) Ltd has heard of other alternative ways of allocating fixed

manufacturing overheads to products. They consulted experts on this new costing technique called

Activity Based Costing (ABC) and they were provided with the following analysis of the budgeted fixed

manufacturing overheads:

Activity

Material purchase and

storage

Setting up of machines

Production

Maintenance (routine

inspection of machines)

Percentage of

budgeted fixed

manufacturing

overheads cost

10%

25%

55%

10%

Cost driver

Number of orders placed: 75 orders for Men's shoes

and 50 orders for Women's boots per year

Set-up hours: set-ups are done for every batch and

each set-up takes 24 min for Men's shoes and 15 min

for Women's boots

Machine hours

Inspection hours: An inspection is done after every

10 hours of machine time.

Management is not sure if they will be better off by implementing the new costing system.

Requirement:

(34)

a) Compute unit product cost and selling price for each product under the current costing

system (show all workings clearly).

(8)

b) Compute unit product cost and selling price for each product under the new costing

system (show all workings clearly).

(20)

c) Advise Morkel's management by mentioning five non-financial factors to be considered if

they should adopt ABC costing techniques.

(6)

End of Question Paper

6