|

ITA412S-INTRODUCATION TO ACCOUNTING -1ST OPP-NOV 2025 |

|

|

1 Page 1 |

▲back to top |

nAm I BIA u n IVE RSITY

OF SCIEnCE Ano TECHnOLOGY

FACULTY OF COMMERCE, HUMAN SCIENCES AND EDUCATION

DEPARTMENT OF ECONOMIC, ACCOUNTING AND FINANCE

QUALIFICATION: BRIDGING PROGRAMME

QUALIFICATION CODE: 04NBR

LEVEL: 4

COURSE CODE: ITA 412S

COURSE NAME: INTRODUCTION TO

ACCOUNTING

SESSION: NOVEMBER 2025

DURATION: 3 HOURS

PAPER: THEORY AND CALCULATIONS

MARKS: 100

FIRST OPPORTUNITY EXAMINATION QUESTION PAPER

EXAMINER(S) Dr. D.R. MUZIRA; Ms YANSY CARIDAD ODIO LOPEZ; Mrs LINDSAY JAHS

MODERATOR: Mr. KUHEPA TJONDU

INSTRUCTIONS

1. Answer all questions.

2. Read all the questions carefully before answering.

3. Make sure your name and surname, question number and the

date appears on the answer script.

4. Please ensure that your writing is legible, neat and presentable.

THIS QUESTION PAPER CONSISTS OF 3 PAGES (Including this front page)

|

|

2 Page 2 |

▲back to top |

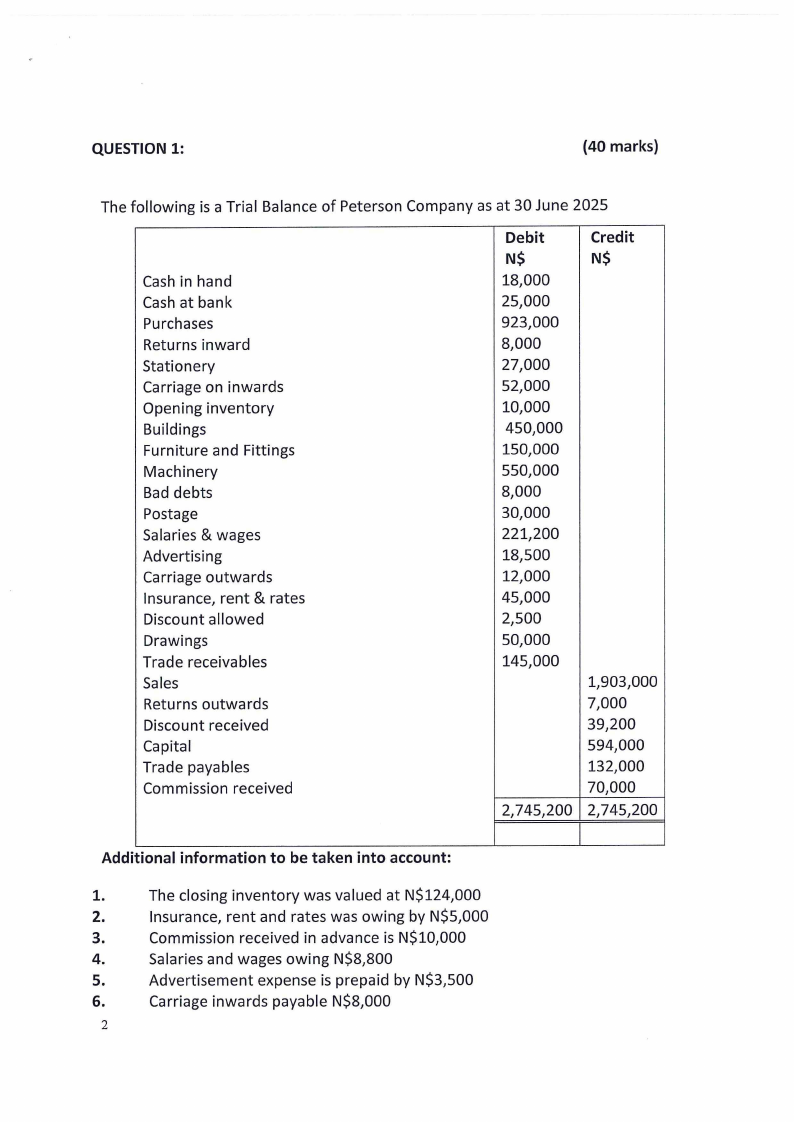

QUESTION 1:

(40 marks)

The following is a Trial Balance of Peterson Company as at 30 June 2025

Cash in hand

Cash at bank

Purchases

Returns inward

Stationery

Carriage on inwards

Opening inventory

Buildings

Furniture and Fittings

Machinery

Bad debts

Postage

Salaries & wages

Advertising

Carriage outwards

Insurance, rent & rates

Discount allowed

Drawings

Trade receivables

Sales

Returns outwards

Discount received

Capital

Trade payables

Commission received

Debit

N$

18,000

25,000

923,000

8,000

27,000

52,000

10,000

450,000

150,000

550,000

8,000

30,000

221,200

18,500

12,000

45,000

2,500

50,000

145,000

2,745,200

Credit

N$

1,903,000

7,000

39,200

594,000

132,000

70,000

2,745,200

Additional information to be taken into account:

1.

The closing inventory was valued at N$124,000

2.

Insurance, rent and rates was owing by N$5,000

3.

Commission received in advance is N$10,000

4.

Salaries and wages owing N$8,800

5.

Advertisement expense is prepaid by N$3,500

6.

Carriage inwards payable N$8,000

2

|

|

3 Page 3 |

▲back to top |

Required: Prepare the following Financial Statements at 30 June 2025:

a) The Statement of Profit or Loss.

{20)

b) The Statement of financial position.

{20)

QUESTION 2

{25 marks)

Dee is a registered Value Added Tax (VAT) vendor. The business recorded the following

transactions during the VAT period ended 30 June 2025. The applicable VAT rate is

15%. Dee uses the periodic inventory system . All amounts include VAT, unless stated

otherwise.

1 June: Bought goods for resale N$130 000 (excl VAT) on credit from AD Supplies.

7 June: Bought Vehicle for delivery purposes N$285 000 paid via Electronic Fund

Transfer {EFT).

10 June: Some of the goods, valued at N$57 000 (excl VAT) which were bought on 1

June were returned to AD Supplies, having been found to be defective.

12 June: Sold Goods for N$70 000 to ABC Traders on Credit.

14 June: Bought snacks and cool drinks for the office. A total amount of N$3 500 cash

was paid to Pick 'n Pay.

15 June: ABC Traders returned some of the goods sold on 12 June, valued at

N$ 15 000.

Required:

a) Prepare the general journals for the above transactions. Journal narrations are

required.

{20)

b) Differentiate zero-rated goods from exempt goods and give an example of each

(5)

QUESTION 3

35 marks

a) Name and explain the 4 enhancing qualitative characteristics of useful financial

information.

(8)

b) Name and define the elements of the financial statements. {10)

c) Using a table, compare and contrast the differences between financial

accounting and management accounting

(12)

d) State FIVE reasons why a trial balance might not balance (5)

THE END

3