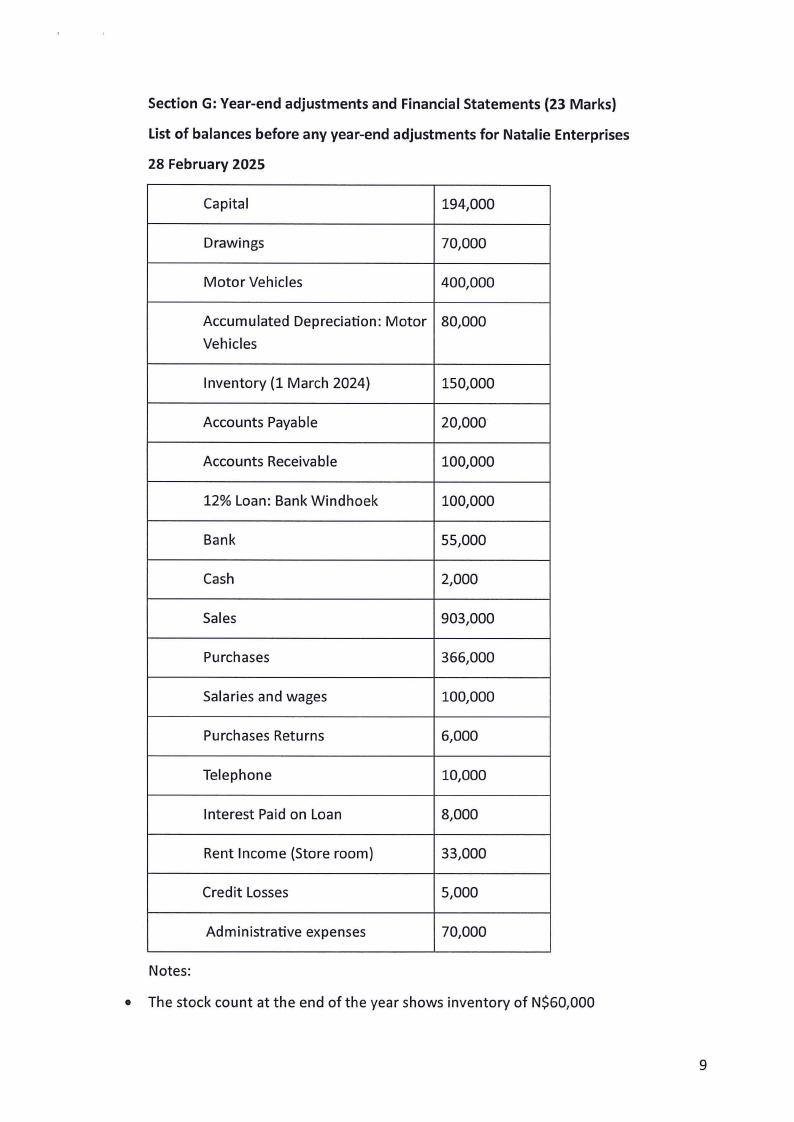

• The loan at bank Windhoek was entered into 3 years ago.

• The rent for the store room was only received for 11 months.

• The salaries and wages have been prepaid by N$15,000. This transaction relates to the

office administrator who went on leave and received a portion of the March 2025

salary.

• Motor vehicle depreciation is charged over 5 years, and a residual value of N$50,000

is provided for. The motor vehicle was bought in 2023.

Questions 42-51 relate to the above information.

42. Depreciation on motor vehicles will have the following effect: (2 marks):

a. Depreciation of N$80,000, and a net book value of N$320,000

b. Depreciation of N$140,000, and a net book value of N$200,000

c. Depreciation of N$70,000, and a net book value of N$250,000

d. Depreciation of N$80,000 and a net book value of N$320,000

e. None of the above

43. The depreciable amount is presented as:

a. Cost price less residual value

b. Cost price less accumulated depreciation

c. Cost price less net Book Value

d. Market value

e. None of the above

44. Net Book Value is calculated as:

a. Cost price less depreciation

b. Cost price less accumulated depreciation

c. Depreciable amount less residual value

d. Cost price less residual value

e. None of the above

45. The prepaid salaries and wages will have the following effect on the financial

statement (2 marks)

a. A total expense of N$115,000 and an asset of N$5,000

b. A total expense of N$85,000 and an asset of N$15,000

c. A total expense of N$100,000 and a liability of N$5,000

d. A total income of N$85,000 and an asset of N$15,000

e. None of the above

46. The cost of sales can be calculated as: (4 marks)

a. N$450,000

b. N$456,000

c. N$366,000

10