Questions 1-3

Introduction of Cost Accounting (Theory) (3 Questions x 1 mark)

1. Which one of the following statements is incorrect (1 mark)

a. Financial Accounting uses historical information.

b. No specific body or organisation govern Financial Accounting.

c. Financial Accounting produces statements for external users.

d. A cash flow statement is part of a set of financial statements.

e. None of the above.

2. Sunk costs refer to (1 mark)

a. Costs directly influenced by the decisions of the unit manager

b. Costs that should be incurred in a specific production process

c. Past costs that are now irrevocable

a. Costs that may be eliminated if production levels decrease

b. None of the above

3. Which of the following best describes a fixed cost (1 mark)

a. It may change in total where such a change is unrelated to units of production

b. It may change in total where such a change is related to units of production

c. It remains constant per unit produced

d. It may change in total, depending on production within a relevant range.

e. None of the above

Questions 4-11

Materials and inventory control (Theory, application and calculations) (16 marks)

4. Which entry is recorded when materials are transferred to production? (2 marks)

a. Debit Raw Materials and Credit Work in Process

b. Debit Manufacturing Overhead and Credit Raw Materials

c. Debit Materials Expense and Credit Raw Materials

d. Debit Work in Process and Credit Raw Materials

5. Which entry is recorded when materials with a cost of N$20,000 are sold to a

customer? The customer paid cash for the goods (4 marks)

a. Debit cost of sales, credit finished goods, debit bank, credit Sales

b. Debit finished goods, credit cost of sales, debit bank, credit Sales

c. Debit finished goods, credit cost of sales, debit bank, credit cash sales

d. Debit finished goods, credit cost of sales, debit bank, credit cash sales

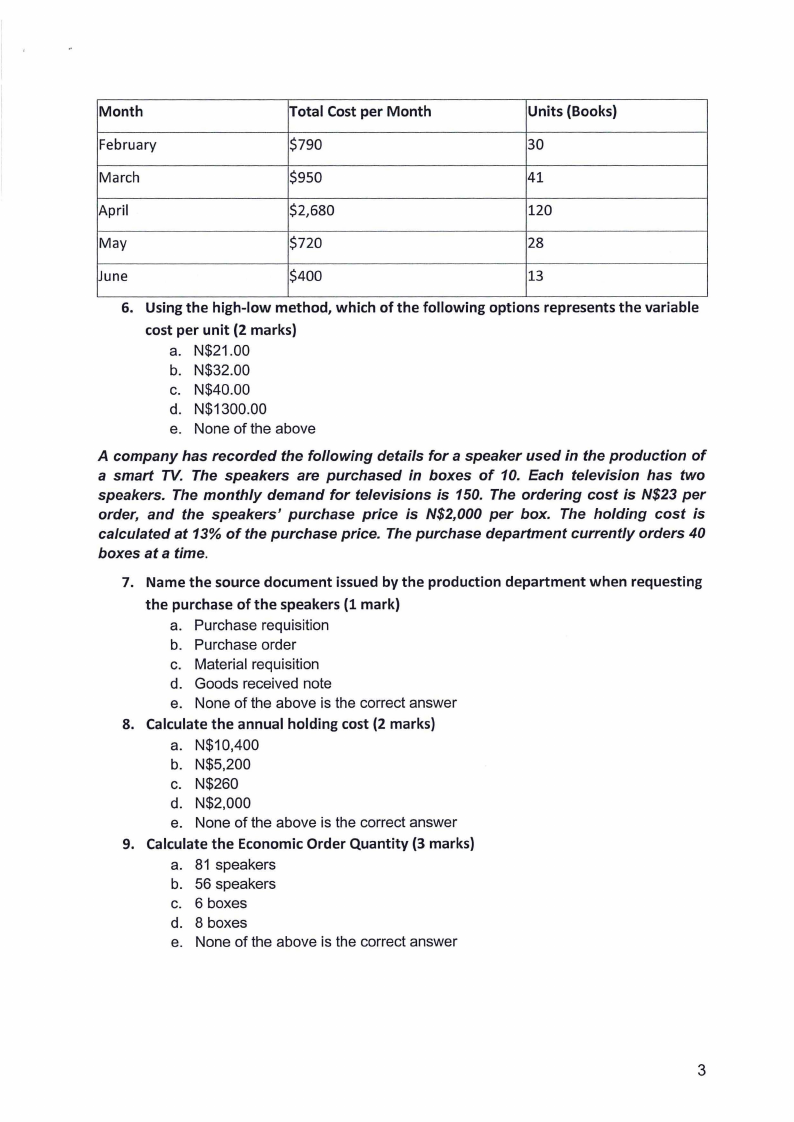

This information relates to Question 6. Below are the company's costs per month, along

with the units produced, specifically baby bottles, for a six-month period. When performing

these calculations, round the amount to the nearest N$ throughout. (Example: N$10.50 will

become N$11.00, but N$10.49 will remain N$10.00)

Month

January

Total Cost per Month

$1,650

Units (Books)

70

2