|

GMA711S- MANAGEMENT ACCOUNTING 310- 1ST OPP- JUNE 2023 |

|

|

1 Page 1 |

▲back to top |

n Am I BI A u n IVER s ITY

OF SCIEnCE Ano TECHnOLOGY

FACULTY OF COMMERCE, HUMAN SCIENCES AND EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING AND FINANCE

QUALIFICATION: BACHELOR OF ACCOUNTING

QUALIFICATION CODE: 07BOAC LEVEL:?

COURSE CODE: GMA711 S

COURSE NAME: MANAGEMENT ACCOUNTING 310

SESSION: JUNE 2023

PAPER: THEORY AND CALCULATIONS

DURATION: 3 HOURS

MARKS: 100

EXAMINERS

MODERATOR

FIRST OPPORTUNITY EXAMINATION QUESTION PAPER

Sydney Lishokomosi and Lameck Odada

Alfred Makosa

INSTRUCTIONS

1. Answer ALL the FOUR (4) questions in blue or black ink only. NO PENCIL.

2. Start each question on a new page, and number the answers correctly and clearly.

3. Write clearly, and neatly and show all your workings/assumptions.

4. Work with four (4) decimal places in all your calculations and only round off final answers

to two (2) decimal places unless otherwise stated.

5. Questions relating to this examination may be raised in the initial 30 minutes after the start

of the examination. Thereafter, candidates must use their initiative to deal with any

perceived error or ambiguities, and any assumptions the candidate makes should be

clearly stated.

PERMISSIBLE MATERIALS

1. Silent, non-programmable calculators

THIS QUESTION PAPER CONSISTS OF_ 4_ PAGES (excluding this front page and tables)

0

|

|

2 Page 2 |

▲back to top |

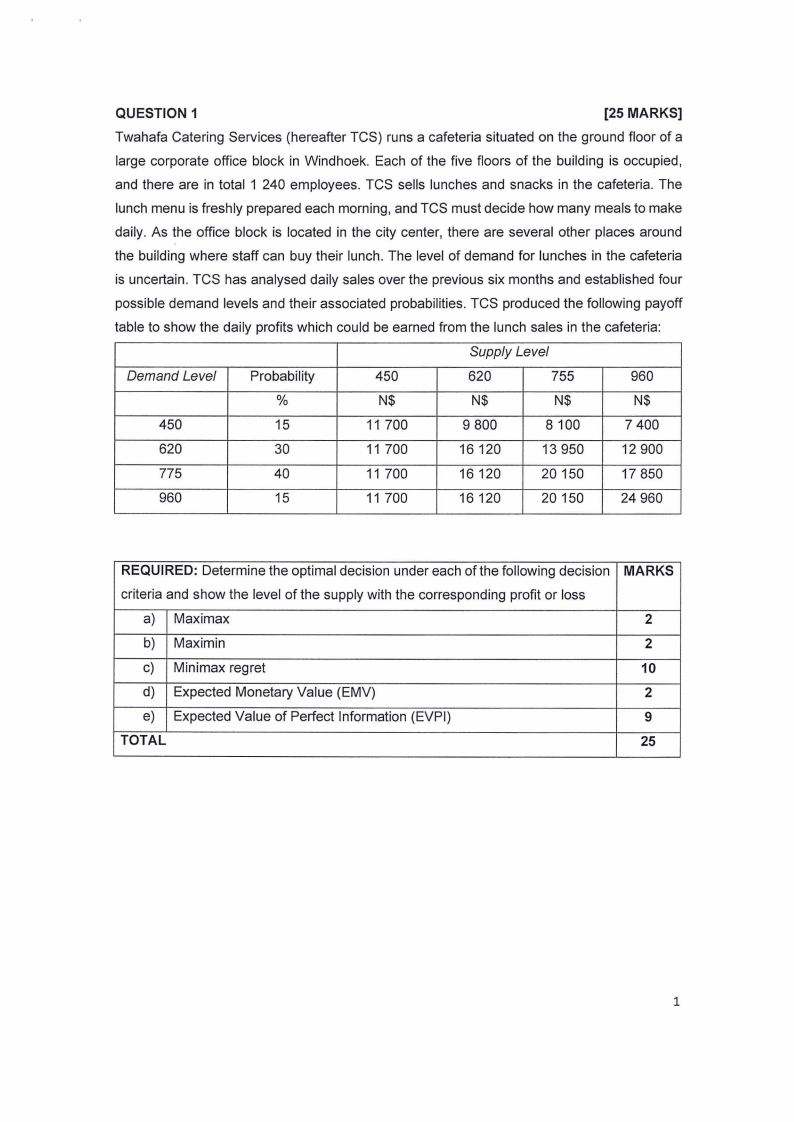

QUESTION 1

(25 MARKS]

Twahafa Catering Services (hereafter TCS) runs a cafeteria situated on the ground floor of a

large corporate office block in Windhoek. Each of the five floors of the building is occupied,

and there are in total 1 240 employees. TCS sells lunches and snacks in the cafeteria. The

lunch menu is freshly prepared each morning, and TCS must decide how many meals to make

daily. As the office block is located in the city center, there are several other places around

the building where staff can buy their lunch. The level of demand for lunches in the cafeteria

is uncertain. TCS has analysed daily sales over the previous six months and established four

possible demand levels and their associated probabilities. TCS produced the following payoff

table to show the daily profits which could be earned from the lunch sales in the cafeteria:

Supply Level

Demand Level

Probability

450

620

755

960

%

N$

N$

N$

N$

450

15

11 700

9 800

8100

7 400

620

30

11 700

16 120

13 950

12 900

775

40

11 700

16 120

20 150

17 850

960

15

11 700

16 120

20 150

24 960

REQUIRED: Determine the optimal decision under each of the following decision

criteria and show the level of the supply with the corresponding profit or loss

a) Maximax

b) Maximin

c) Minimax regret

d) Expected Monetary Value (EMV)

e) Expected Value of Perfect Information (EVPI)

TOTAL

MARKS

2

2

10

2

9

25

1

|

|

3 Page 3 |

▲back to top |

QUESTION 2

[26 MARKS]

Super Save needs to increase production capacity to meet the increasing demand for an

existing product, 'super' used in food processing. A new machine, with a useful life of four

years and a maximum output of 600 000 kilograms of super per year, could be bought for

N$800 000, payable immediately. The scrap value of the machine after four years would be

N$30 000. Forecast demand and production of super over the next four years are as follows:

Year

Demand (kg)

1

1.4 million

2

1.5 million

3

1.6 million

4

1.7 million

The existing production capacity for super is limited to one million kilograms per year, and the

new machine would only be used for additional demand. The current selling price of super is

N$8 per kilogram, and the variable cost of materials is N$5 per kilogram. Other variable costs

of production are N$1.90 per kilogram. Fixed costs of production associated with the new

machine would be N$240 000 in the first year of production, increasing by N$20 000 per year

in each subsequent year of operation.

Super Save pays tax one year in arrears at an annual rate of 30% and can claim capital

allowances (tax-allowable depreciation) on a 25% reducing balance basis. A balancing

allowance is claimed in the final year of operation. Super Save uses its after-tax weighted

average cost of capital (WACC) of 10% when appraising investment projects.

REQUIRED:

MARKS

Calculate the Net Present Value (NPV) of buying the new machine and 20

a)

advise on the acceptability of the proposed purchase

At a 20% discount factor, calculate the Internal Rate of Return (IRR) of

6

b)

buying the new machine to the nearest whole number.

TOTAL

26

2

|

|

4 Page 4 |

▲back to top |

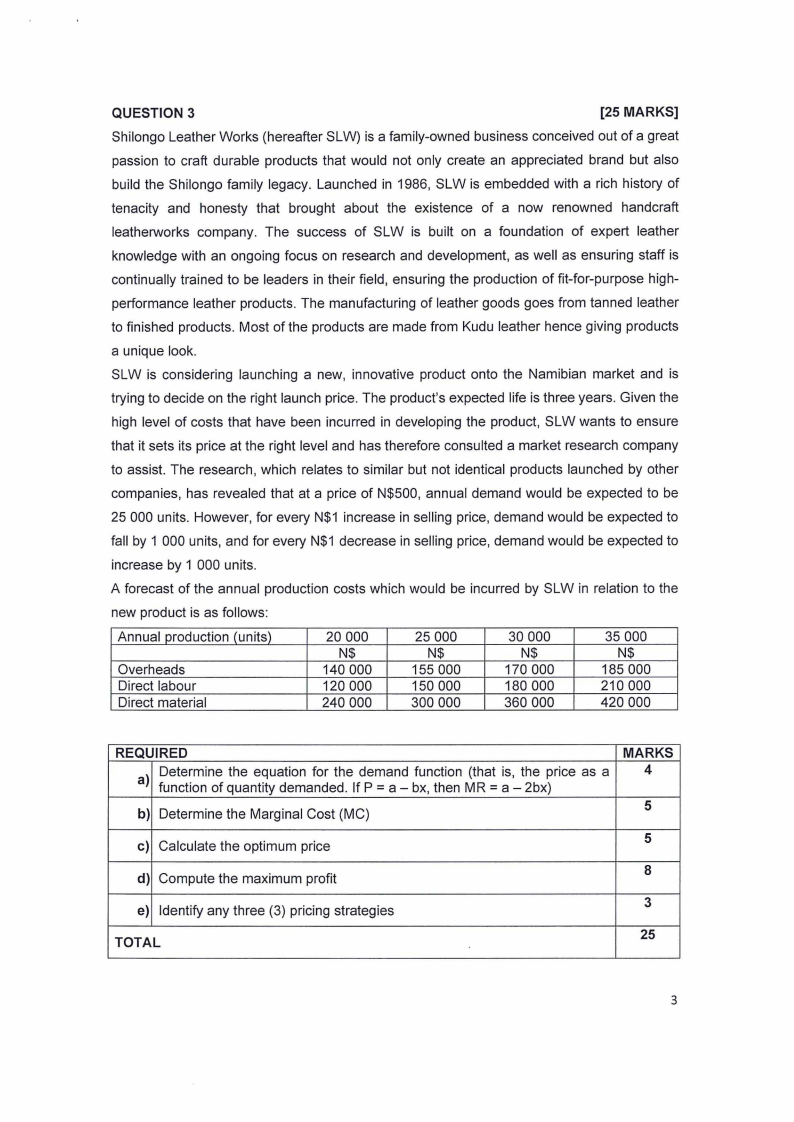

QUESTION 3

[25 MARKS]

Shilongo Leather Works (hereafter SLW) is a family-owned business conceived out of a great

passion to craft durable products that would not only create an appreciated brand but also

build the Shilongo family legacy. Launched in 1986, SLW is embedded with a rich history of

tenacity and honesty that brought about the existence of a now renowned handcraft

leatherworks company. The success of SLW is built on a foundation of expert leather

knowledge with an ongoing focus on research and development, as well as ensuring staff is

continually trained to be leaders in their field, ensuring the production of fit-for-purpose high-

performance leather products. The manufacturing of leather goods goes from tanned leather

to finished products. Most of the products are made from Kudu leather hence giving products

a unique look.

SLW is considering launching a new, innovative product onto the Namibian market and is

trying to decide on the right launch price. The product's expected life is three years. Given the

high level of costs that have been incurred in developing the product, SLW wants to ensure

that it sets its price at the right level and has therefore consulted a market research company

to assist. The research, which relates to similar but not identical products launched by other

companies, has revealed that at a price of N$500, annual demand would be expected to be

25 000 units. However, for every N$1 increase in selling price, demand would be expected to

fall by 1 000 units, and for every N$1 decrease in selling price, demand would be expected to

increase by 1 000 units.

A forecast of the annual production costs which would be incurred by SLW in relation to the

new product is as follows:

Annual production (units)

Overheads

Direct labour

Direct material

20 000

N$

140 000

120 000

240 000

25 000

N$

155 000

150 000

300 000

30 000

N$

170 000

180 000

360 000

35 000

N$

185 000

210 000

420 000

REQUIRED

a)

Determine the equation for the demand function (that is, the price

function of quantity demanded. If P = a - bx, then MR= a - 2bx)

as

a

b) Determine the Marginal Cost (MC)

MARKS

4

5

c) Calculate the optimum price

5

d) Compute the maximum profit

8

e) Identify any three (3) pricing strategies

3

TOTAL

25

3

|

|

5 Page 5 |

▲back to top |

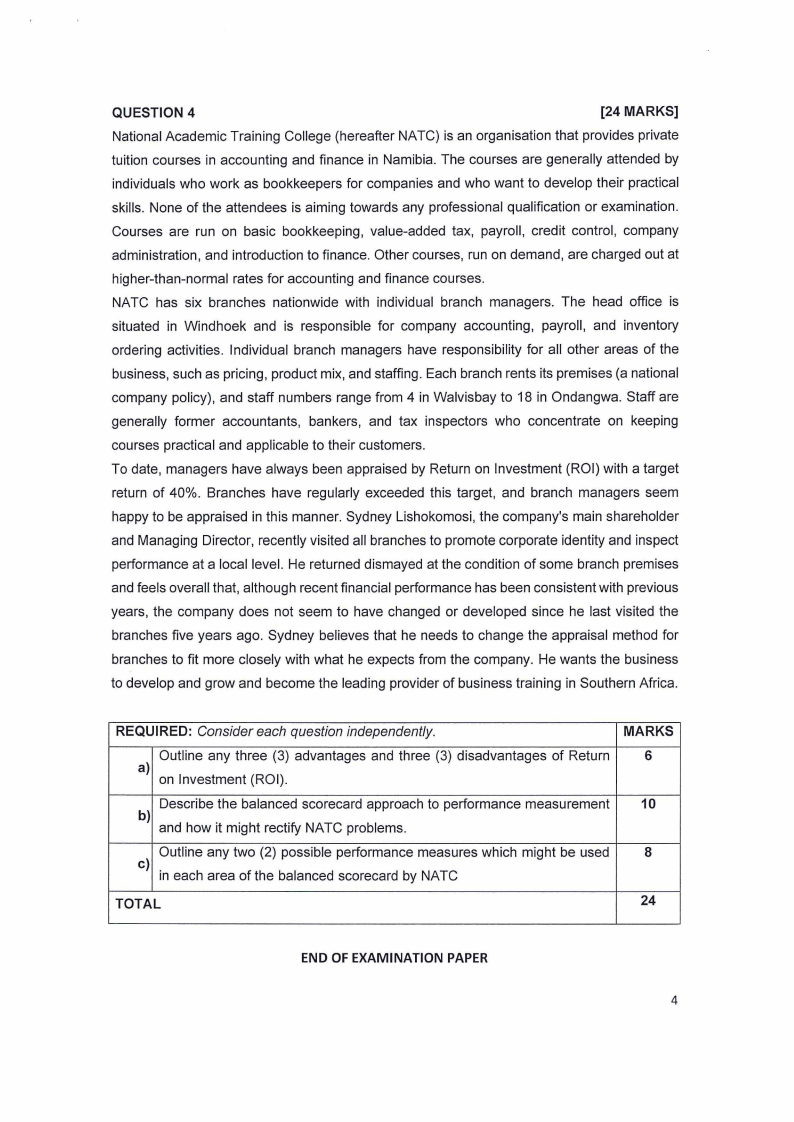

QUESTION 4

[24 MARKS]

National Academic Training College (hereafter NATC) is an organisation that provides private

tuition courses in accounting and finance in Namibia. The courses are generally attended by

individuals who work as bookkeepers for companies and who want to develop their practical

skills. None of the attendees is aiming towards any professional qualification or examination.

Courses are run on basic bookkeeping, value-added tax, payroll, credit control, company

administration, and introduction to finance. Other courses, run on demand, are charged out at

higher-than-normal rates for accounting and finance courses.

NATC has six branches nationwide with individual branch managers. The head office is

situated in Windhoek and is responsible for company accounting, payroll, and inventory

ordering activities. Individual branch managers have responsibility for all other areas of the

business, such as pricing, product mix, and staffing. Each branch rents its premises (a national

company policy), and staff numbers range from 4 in Walvisbay to 18 in Ondangwa. Staff are

generally former accountants, bankers, and tax inspectors who concentrate on keeping

courses practical and applicable to their customers.

To date, managers have always been appraised by Return on Investment (ROI) with a target

return of 40%. Branches have regularly exceeded this target, and branch managers seem

happy to be appraised in this manner. Sydney Lishokomosi, the company's main shareholder

and Managing Director, recently visited all branches to promote corporate identity and inspect

performance at a local level. He returned dismayed at the condition of some branch premises

and feels overall that, although recent financial performance has been consistent with previous

years, the company does not seem to have changed or developed since he last visited the

branches five years ago. Sydney believes that he needs to change the appraisal method for

branches to fit more closely with what he expects from the company. He wants the business

to develop and grow and become the leading provider of business training in Southern Africa.

REQUIRED: Consider each question independently.

MARKS

Outline any three (3) advantages and three (3) disadvantages of Return

6

a)

on Investment (ROI).

Describe the balanced scorecard approach to performance measurement

10

b)

and how it might rectify NATC problems.

Outline any two (2) possible performance measures which might be used

8

c)

in each area of the balanced scorecard by NATC

TOTAL

24

END OF EXAMINATION PAPER

4

|

|

6 Page 6 |

▲back to top |

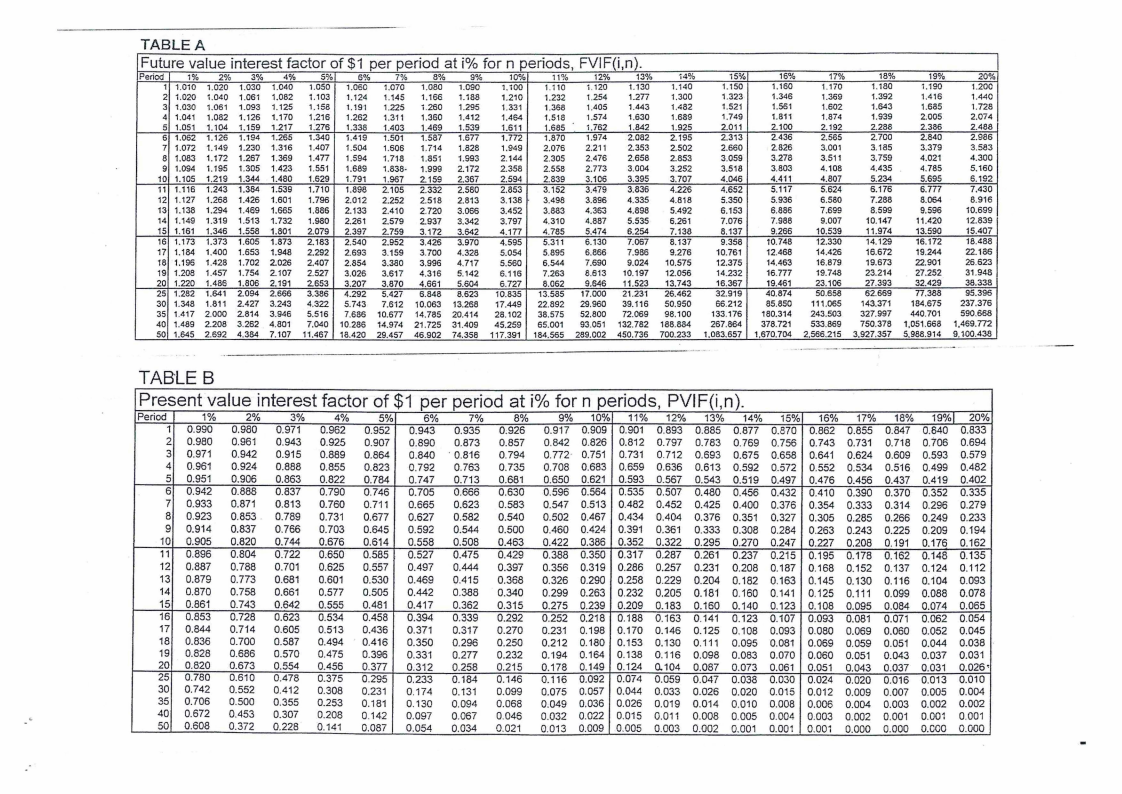

TABLE A

Future value interest factor of $1 per period at io/ofor n periods, FVIF(i,n).

Period

1%

1 1.010

2 1.020

3 1.030

4 1,041

5 1.051

6 1.062

7 1.072

8 1.083

9 1.094

10 1.105

11 1.116

2%

1.020

1.040

1.061

1.082

1.104

1.126

1,149

1.172

1.195

1,219

1.243

3%

1.030

1.061

1.093

1.126

1.159

1.194

1.230

1.267

1,305

1.344

1.384

4%

1.040

1.082

1.125

1.170

1.217

1.265

1.316

1.369

1.423

1.480

1.539

5%

1.050

1.103

1.158

1.216

1.276

1.340

1.407

1.477

1.551

1.629

1.710

6~1o

1.060

1.124

1,19"1

1.262

1.338

1.419

1.504

1,594

1.689

1.791

1.898

7%

1.070

1.145

1.225

1.311

1.403

1.501

1.606

1.718

1.838-

1.967

2.105

8%

1.080

1.166

1.260

1.360

1.469

1.587

1.714

1,851

1.999

2.169

2.332

9%

1.090

1.188

1.295

1.412

1.539

1.677

1.828

1.993

2.172

2.367

2.580

10%

1.100

1.210

1.331

1.464

1.611

1.772

1,949

2.144

2.358

2.594

2.853

11%

1.110

1.232

1.368

1,518

1.685

1.870

2.076

2.305

2.558

2.839

3.152

12%

1.120

1.254

1,405

1,574

1,762

1,974

2.211

2.476

2.773

3.106

3.479

13%

1.130

1.277

1.443

1.630

1.842

2.082

2.353

2.658

3,004

3.395

3.836

i4%

1.140

1.300

1.482

1.689

1.925

2.195

2.502

2.853

3.252

3.707

4.226

12 1.127 1.268 1.426 1.601 1.796 2.012 2.252 2.518 2.813

13 1.138 1.294 1.469 1.665 1.886 2.133 2.410 2.720 3,066

3.138

3.452

3.498

3.883

3.896

4.363

4.335

4.898

4.818

5.492

14 1.149

15 1.161

16 1.173

17 1.184

18 1.196

1.319

1.346

1.373

1.400

1.428

1.513

1.558

1.605

1.653

1.702

1.732

1.801

1.873

1.948

2.026

1.980

2.079

2.183

2.292

2.407

2.261

2.397

2.540

2.693

2.854

2.579

2.759

2.952

3.159

3.380

2.937

3.172

3.426

3.700

3.996

3.342

3.642

3.970

4.328

4.717

3.797

4.177

4.595

5.054

5.560

4.310

4.785

5.311

5.895

6,544

4.887

5.474

6.130

6.866

7.690

5.535

6.254

7.067

7.986

9.024

6.261

7.138

8.137

9.276

10,575

19 1.208

20 1.220

25 1.282

30 1.348

1.457

1.486

1.641

1.811

1.754

1.806

2.094

2.427

2.107

2.191

2.666

3.243

2.527

2.653

3,386

4,322

3.026

3.207

4.292

5.743

3.617

3,870

5.427

7.612

4.316

4,661

6.848

10.063

5.142

5.604

8.623

13.268

6.116

6.727

10.835

17.449

7,263

8.062

13.586

22.892

8.613

9.646

17.000

29.960

10.197

11.523

21.231

39.116

12.056

13.743

26.462

50.950

35 1.417 2.000 2.814 3.946

40 1.489 2.208 3.262 4.801

50 1.645 2.692 4.384 7.107

5.516 7.686 10.677 14.785 20.414

7.040 10.286 14.974 21.725 31.409

11.467 18.420 29.457 46.902 74.358

28.102

45.259

117.391

38.575 52.800 72.069 98.100

65.001 93.051 132.782 188.884

184.565 289.002 450.736 700.233

15%

1.150

1.323

1.521

1.749

2.011

2.313

2.660

3,059

3.518

4.046

4.652

5.350

6.153

7.076

8.137

9.358

10.761

12.375

14.232

16.367

32.919

66.212

133.176

267.864

1.083.657

16~10

17%

18%

1.160

1.1i0

1.180

1.346

1.369

1.392

1.561

1.602

1.643

1.811

1,874

1,939

2.100

2,192

2.288

2.436

2.565

2.700

2.826

3.001

3.185

3.278

3.511

3.759

3.803

4.108

4.435

4.411

4.807

5.234

5,117

5.624

6.176

5.936

6.580

7.288

6.886

7.699

8,599

7.988

9.007

10.147

9.266

10.539

11.974

10.748

12.330

14.129

12.468

14.426

16.672

14.463

16.879

19.673

16.777

19.748

23.214

19.461

23.106

27.393

40.874

50.658

62.669

85.850 111.065 143.371

180.314 243.503 327.997

378.721 533,869 750.378

1,670,704 2,566,215 3.927,357

··-· ------'------

19%

1.190

1.416

1.685

2.005

2.386

2.840

3.379

4.021

4.785

5.695

6.777

8.064

9,596

11.420

13.590

16.172

19.244

22.901

27.252

32.429

77,388

184.675

440.701

1,051.668

5.988.914

20%

1.200

1.440

1,728

2.074

2.488

2.986

3.583

4.300

5.160

6.192

7,430

8.916

10.699

12.839

15.407

18.488

22.186

26.623

31,948

38.338

95.396

237.376

590.668

1,469.772

9,100.438

TABLE B

Present value interest factor of $1 per period at i% for n periods, PVIF(i,n).

Period

1

2

3

4

5

6

7

8

9

10

11

12

13

14

15

16

17

18

19

20

25

30

35

40

50

1%

0.990

0.980

0.971

0.961

0.951

0.942

0.933

0.923

0.914

0.905

0.896

0.887

0.879

0.870

0.861

0.853

0.844

0.836

0.828

0.820

0.780

0.742

0.706

0.672

0.608

2%

0.980

0.961

0.942

0.924

0.906

0.888

0.871

0.853.

0.837

0.820

0.804

0.788

0.773

0.758

0.743

0.728

0.714

0.700

0.686

0.673

0.610

0.552

0.500

0.453

0.372

3%

0.971

0.943

0.915

0.888

0.863

0.837

0.813

0.789

0.766

0.744

0.722

0.701

0.681

0.661

0.642

0.623

0.605

0.587

0.570

0.554

0.478

0.412

0.355

0.307

0.228

4%

0.962

0.925

0.889

0.855

0.822

0.790

0.760

0.731

0.703

0.676

0.650

0.625

0.601

0.577

0.555

0.534

0.513

0.494

0.475

0.456

0.375

0.308

0.253

0.208

0.141

5%

0.952

0.907

0.864

0.823

0.784

0.746

0.711

0.677

0.645

0.614

0.585

0.557

0.530

0.505

0.481

0.458

0.436

0.416

0.396

0.377

0.295

0.231

0.181

0.142

0.087

6%

0.943

0,890

0.840

0.792

0.747

0.705

0.665

0.627

0.592

0.558

0.527

0.497

0.469

0.442

0.417

0.394

0.371

0.350

0.331

0.312

0.233

0.174

0.130

0.097

0.054

7%

0.935

0.873

. 0.816

0.763

0.713

0.666

0.623

0.582

0.544

0.508

0.475

0.444

0.415

0.388

0.362

0.339

0.317

0.296

0.277

0.258

0.184

0.131

0.094

0.067

0.034

8%

0.926

0.857

0.794

0.735

0.681

0.630

0.583

0.540

0.500

0.463

0.429

0.397

0.368

0.340

0.315

0.292

0.270

0.250

0.232

0.215

0.146

0.099

0.068

0.046

0.021

9% 10% 11% 12% 13% 14% 15% 16% 17% 18% 19%1 20%

0.917 0.909 0.901 0.893 0.885 0.877 0.870 0.862 0.855 0.847 0.840 0.833

0.842 0.826 0.812 0.797 0.783 0.769 0.756 0.743 0.731 0.718 0.706 0.694

0.772· 0.751 0.731 0.712 0.693 0.675 0.658 0.641 0.624 0.609 0.593 0.579

0.708 0.683 0.659 0.636 0.613 0.592 0.572 0.552 0.534 0.516 0.499 0.482

0.650 0.621 0.593 0.567 0.543 0.519 0.497 0.476 0.456 0.437 0.419 0.402

0.596 0.564 0.535 0.507 0.480 0.456 0.432 0.410 0.390 0.370 0.352 0.335

0.547 0.513 0.482 0.452 0.425 0.400 0.376 0.354 0.333 0.314 0.296 0.279

0.502 0.467 0.434 0.404 0.376 0.351 0.327 0.305 0.285 0.266 0.249 0.233

0.460 0.424 0.391 0.361 0.333 0.308 0.284 0.263 0.243 0.225 0.209 0.194

0.422 0.386 0.352 0.322 0.295 0.270 0.247 0.227 0.208 0.191 0.176 0.162

0.388 0.350 0.317 0.287 0.261 0.237 0.215 0.195 0.178 0.162 0.148 0.135

0.356 0.319 0.286 0.257 0.231 0.208 0.187 0.168 0.152 0.137 0.124 0.112

0.326 0.290 0.258 0.229 0.204 0.182 0.163 0.145 0.130 0.116 0.104 0.093

0.299 0.263 0.232 0.205 0.181 0.160 0.141 0.125 0.111 0.099 0.088 0.078

0.275 0.239 0.209 0.183 0.160 0.140 0.123 0.108 0.095 0.084 0.074 0.065

0.252 0.218 0.188 0.163 0.141 0.123 0.107 0.093 0.081 0.071 0.062 0.054

0.231 0.198 0.170 0.146 0.125 0.108 0.093 0.080 0.069 0.060 0.052 0.045

0.212 0.180 0.153 0.130 0.111 0.095 0.081 0.069 0.059 0.051 0.044 0.038

0.194 0.164 0.138 0.116 0.098 0.083 0.070 0.060 0.051 0.043 0.037 0.031

0.178 0.149 0.124 0.104 0.087 0.073 0.061 0.051 0.043 0.037 0.031 0.026•

0.116 0.092 0.074 0.059 0.047 0.038 0.030 0.024 0.020 0.016 0.013 0.010

0.075 0.057 0.044 0.033 0.026 0.020 0.015 0.012 0.009 0.007 0.005 0.004

0.049 0.036 0.026 0.019 0.014 0.010 0.008 0.006 0.004 0.003 0.002 0.002

0.032 0.022 0.015 0.011 0.008 0.005 0.004 0.003 0.002 0.001 0.00~ 0.001

0.013 0.009 0.005 0.003 0.002 0.001 0.00~ 0.001 0.000 0.000 0.000 0.000

|

|

7 Page 7 |

▲back to top |

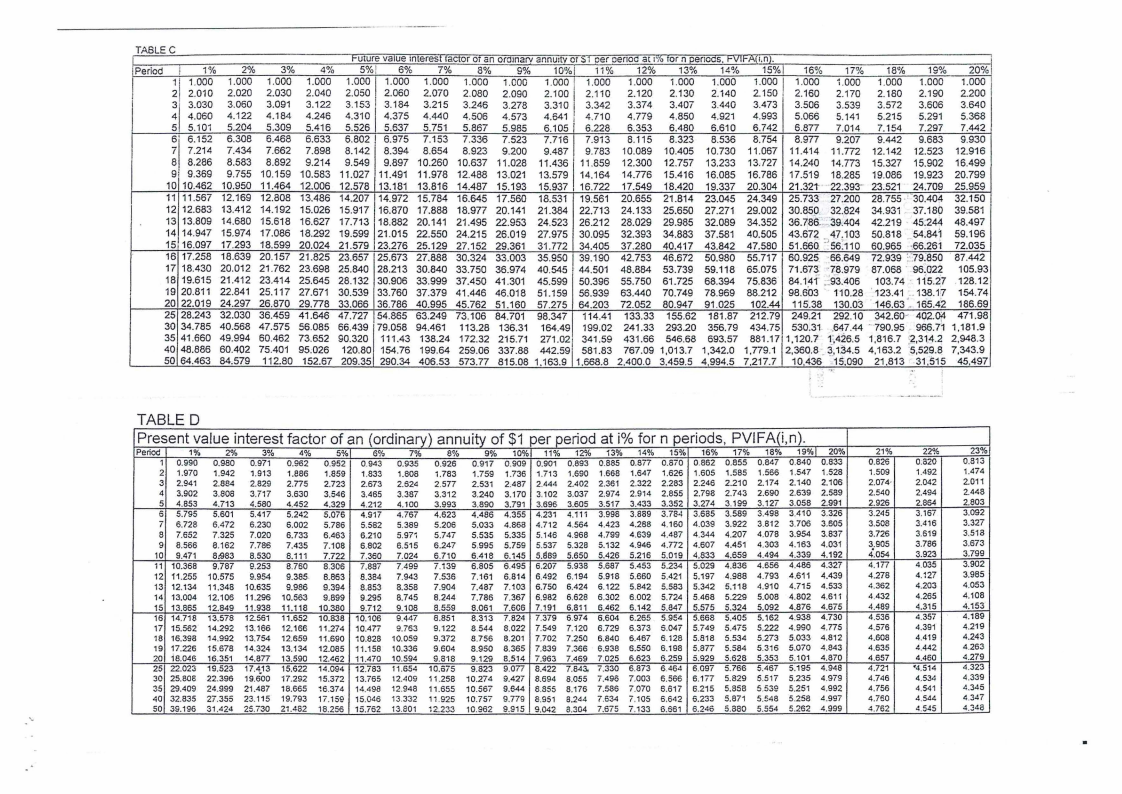

TASLI= C

Future value 1nteres! rac!or Oi an oramarv annu:!v or ::,1 oer oenoa at 1°10ror n oenocs. rv,,Ao.nJ.

Period ! 1%

2%

3%

4~"1 5%1 6%

7%

8%

9% 10% 11% 12% 13% 14% 15%1 16% 17% 18% 19°/4 20%

1 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000 1.000

2 2.010 2.020 2.030 2.040 2.050 2.060 2.070 2.080 2.090 2.100 2.110 2.120 2.130 2.140 2.150 2.160 2.170 2.180 2.190 2.200

3 3.030 3.060 3.091 3.122 3.153 3.184 3.215 3.246 3.278 3.310 3.342 3.374 3.407 3.440 3.473 3.506 3.539 3.572 3.606 3.640

4 4.060 4.122 4.184 4.246 4.310 4.375 4.440 4.506 4.573 4.641 4.710 4.779 4.850 4.921 4.993 5.066 5.141 5.215 5.291 5.368

5 5.101 5.204 5.309 5.416 5.526 5.637 5.751 5.867 5.985 6.105 6.228 6.353 6.480 6.610 6.742 6.877 7.014 7.154 7.297 7.442

6 6.152 6.308 6.468 6.633 6.802 6.975 7.153 7.336 7.523 7.716 7.913 8.115 8.323 8.536 8.754 8.977 9.207 9.442 9.683 9.930

7 7.214 7.434 7.662 7.898 8.142 8.394 8.654 8.923 9.200 9.487 9.783 10.089 10.405 10.730 11.067 11.414 11.772 12.142 12.523 12.916

8 8.286 8.583 8.892 9.214 9.549 9.897 10.260 10.637 11.028 11.436 11.859 12.300 12.757 13.233 13.727 14.240 14.773 15.327 15.902 16.499

9 9.369 9.755 10.159 10.583 11.027 11.491 11.978 12.488 13.021 13.579 14.164 14.776 15.416 16.085 16.786 17.519 18.285 19.086 19.923 20.799

10 10.462 10.950 11.464 12.006 12.578 13.181 13.816 14.487 15.193 15.937 16.722 17.549 18.420 19.337 20.304 21.321' 22.393' 23.521 24.709 25.959

11 11.567 12.169 12.808 13.486 14.207 14.972 15.784 16.645 17.560 18.531 19.561 20.655 21.814 23.045 24.349 25.733 27.200 28.755 ···30.404 32.150

12 12.683 13.412 14.192 15.026 15.917 16.870 17.888 18.977 20.141 21.384 22.713 24.133 25.650 27.271 29.002 30.850 32.824 34.931 37.180 39.581

13 13.809 14.680 15.618 16.627 17.713 18.882 20.141 21.495 22.953 24.523 26.212 28.029 29.985 32.089 34.352 36.786. 39.404 42.219 45.244 48.497

14 14.947 15.974 17.086 18.292 19.599 21.015 22.550 24.215 26.019 27.975 30.095 32.393 34.883 37.581 40.505 43.67?. :,47;103 50.818 54.841 59.196

15 16.097 17.293 18.599 20.024 21.579 23.276 25.129 27.152 29.361 31.772 34.405 37.280 40.417 43.842 47.580 51.66Q .56.110 60.965 ~66.261 72.035

16 17.258 18.639 20.157 21.825 23.657 25.673 27.888 30.324 33.003 35.950 39.190 42.753 46.672 50.980 55.717 60.925 66.649 72.939 :79:850 87.442

17 18.430 20.012 21.762 23.698 25.840 28.213 30.840 33.750 36.974 40.545 44.501 48.884 53.739 59.118 65.075 71.673 ·78.979 87.068 . 96.022 105.93

18 19.615 21.412 23.414 25.645 28.132 30.906 33.999 37.450 41.301 45.599 50.396 55.750 61.725 68.394 75.836 84.14-r -~93.406 103.74 115.27 128.12

19 20.811 22.841 25.117 27.671 30.539 33.760 37.379 41.446 46.018 51.159 56.939 63.440 70.749 78.969 88.212 98.603 110.28 . 123.41 .. 138. 1•7 154.74

20 22.019 24.297 26.870 29.778 33.066 36.786 40.995 45.762 51.160 57.275 64.203 72.052 80.947 91.025 102.44 115.38 130.03 146.63 ._ 165.42 186.69

25 28.243 32.030 36.459 41.646 47.727 54.865 63.249 73.106 84.701 98.347 114.41 133.33 155.62 181.87 212.79 249.21 292.10 342.60- 402.0fl 471.98

30 34.785 40.568 47.575 56.085 66.439 79.058 94.461 113.28 136.31 164.49 199.02 241.33 293.20 356.79 434.75 530.31 .64_7.44. 790.95 966.71 1,181.9

35 41.660 49.994 60.462 73.652 90.320 111.43 138.24 172.32 215.71 271.02 341.59 431.66 546.68 693.57 881.17 1,120.7 f,426.5 1,816.7 ,2,314.2 2,948.3

40 48.886 60.402 75.401 95.026 120.80 154.76 199.64 259.06 337.88 442.59 581.83 767.09 1,013.7 1,342.0 1,779.1 2,360.8 . 3,1.34.5 4,163.2 5,529.8 7,343.9

50 64,463 84.579 112.80 152.67 209.35 290.34 406.53 573.77 815.08 1,163.9 1,668.8 2,400.0 3.459.5 4,994.5 7,217.7 10 436 ..15.090 21,813 31,515 45,497

TABLED

Present value interest factor of an (ordinary) annuity of $1 per period at i% for n periods, PVIFA(i,n).

Period

1%

1 0.990

2 1,970

3 2.941

4 3.902

5 4.853

6 5.795

7 6.728

8 7.652

9 8.566

10 9.471

11 10.368

12 11.255

13 12.134

14 13.004

15 13.865

16 14.718

17 15.562

18 16.398

19 17.226

20 18.046

25 22.023

30 25.808

35 29.409

40 32.835

so 39.196

2%

0.980

1.942

2,884

3,808

4.713

5.601

6.472

7.325

8.162

8:983

9,787

10.575

11.348

12.106

12.849

13.578

14.292

14.992

15.678

16.351

19,523

22.396

24.999

27.355

31.424

3%

0.971

1.913

2.829

3,717

4,580

5.417

6.230

7.020

7.786

8.530

9.253

9.954

10.635

11.296

11.938

12.561

13.166

13,754

14,324

14.87i

17.4,13

19.600

21.487

23.115

25.730

4%

0.962

1.886

2.n5

3.630

4.452

5.242

6.002

6.733

7.435

8.111

8.760

9.385-

9.986

10.563

11.118

11.652

12.166

12.659

13.134

13.590

15.622

17.292

18.665

19.793

21.482

5%

0.952

1.859

2.723

3.546

4.329

5.076

5.786

6.463

7.108

7.722

8.306

8.863

9.394

9.899

10.380

10.838

11.274

11.690

12.085

12.462

14.094

15.372

16.374

17.159

18.256

6%

0.943

1.833

2.673

3.465

4.212

4.917

5.582

6.210

6.802

7,360

7.887

8.384

8.853

9.295

9.i12

10,106

10.47i

10,828

11.158

11.470

12.783

13.765

14.498

15.046

15.762

7%

0.935

1.808

2.624

3.387

4.100

4.76i

5.389

5.97~

6.515

7.024

7.499

7.943

8.358

8.745

9.108

9.447

9.763

10.059

10.336

10.594

11.654

12.409

12.948

13.332

13.801

8%

0.926

1,783

2,577

3.312

3.993

4.623

5.206

5.747

6.247

6.710

7.139

7.536

7.904

8.244

8.559

8.851

9,122

9.372

9.604

9.818

10.675

11.258

11.655

11.925

12.233

9%

0.917

1.759

2.531

3.240

3.890

4.486

5.033

5.535

5.995

6.418

6.805

7.161

7.487

7.786

8.061

8.313

8.544

8.756

8.950

9.129

9.823

10.274

10.56i

10.75i

10.962

10% 11% 12%

0.909 0,901 0.893

1.736 1.i13 1.690

2.487 2.444 2.402

3.170 3.102 3.037

3.791 3.696 3.605

4.355 4.231 4.111

4.868 4.712 4.564

5.335 5.146 4.968

5.759 5.53i 5.328

6.145 5.S89 5.650

6.495 6.207 5.938

6.814 6.492 6,194

7.103 6.750 6.424

7.367 6.982 6.628

7.606 7.191 6.811

7.824 7.379 6.974

8.022 7.549 7.120

8.201 7.702 7.250

8.365 7.839 7,366

8,514 7.963 7.469

9.01 I 8.422 7.843,

9.42i 8.694 8.055

9.644 8.855 8.176

9.779 8.951 8.244

9.915 9,042 8.304

13% 14% 15%

0.885 0.8i7 O.SiO

1.668 1.647 1.626

2.361 2.322 2.283

2.974 2.914 2.855

3,517 3.433 3.352

3,996 3.889 3.784

4.423 4.288 4.160

4.799 4.639 4,487

5.132 4.946 4,772

5.426 5.216 5.019

5.687 5.453 5.234

5.918 5.660 5.421

6.122 5.842 5.583

6.302 6.002 5.724

6.462 6.142 5,847

6.604 6.265 5.954

6.729 6.373 6.047

6.840 6.467 6.128

6,938 6.550 6.198

7.025 6.623 6.259

7.330 6.873 6.464

7.496 7.003 6.566

7.586 7.070 6,617

7.534 7.105 6,642

7.675 i.133 6.661

16%

0.862

1.605

2.246

2,798

3.274

3,685

4.039

4.344

4.607

4,833

5.029

5,197

5.342

5.468

5.575

5.668

5.749

5.818

5.87i

5.929

6.097

6.177

6.215

5,233

6.246

17%

0.855

1.585

2.210

2.743

3.199

3,589

3.922

4.207

4.451

4.659

4.836

4.988

5,118

5.229

5.324

5.405

5.475

5.534

5.584

5.628

5.766

5.829

5.858

5.871

5.880

18%

0.847

1.566

2.174

2.690

3.12i

3.498

3.812

4.078

4.303

4.494

4.656

4.793

4.910

5.008

5.092

5.162

5,222

5.273

5.316

5.353

5.467

5.517

5.539

5.548

5.554

19%1 20%

0.840 0.833

1.547 1.528

2.140 2.106

2.639 2.589

3.058 2.991

3.410 3.326

3.706 3.605

3.954 3,837

4.163 4.031

4,339 4.192

4.486 4.327

4,611 4.439

4.715 4.533

4.802 4.611

4.876 4.675

4.938 4.730

4.990 4.775

5,033 4.812

5,070 4,843

5.101 4.870

5.195 4.948

5.235 4.979

5.251 4.992

5.258 4.997

5.262 4.999

21%

0.826

1.509

2.074·

2.540

2.926

3.245

3.508

3.726

3.905

4',054

4.177

4.278

4.362

4.432

4.489

4.536

4.576

4.608

4.635

4.657

4.721

4.746

4,756

4.760

4.762

22%

0:820

1.492

2.042

2.494

2.864

3.167

3.416

3,619

3.786

3.923

4.035

4.127

4.203

4.265

4.315

4.35i

4.391

4.419

4.442

4.460

'4.514

4.534

4,541

4.544

4.545

23%

0,813

1.474

2.011

2.448

2.803

3.092

3.327

3.518

3.673

3.799

3.902

3.985

4.053

4,108

4.153

4.189

4.219

4.243

4.263

4.279

4.323

4.339

4.345

4.347

4.348