|

AEM810S-APPLIED ECONOMETRICS-1ST OPP- JUNE 2025 |

|

|

1 Page 1 |

▲back to top |

nAmlBIA UnlVERSITY

OF SCIEnCE TECHn OLDGY

FACULTYOF COMMERCE,HUMAN SCIENCESAND EDUCATION

DEPARTMENTOF ECONOMICS,ACCOUNTINGAND FINANCE

QUALIFICATION: BACHELOROF ECONOMICSHONOURS

QUALIFICATIONCODE: 08BECH

LEVEL:8

COURSECODE:AEM810S

COURSENAME: APPLIED ECONOMETRICS

SESSION:MAY/ JUNE 2025

DURATION: 3 HOURS

PAPER: 1

MARKS: 100

FIRSTOPPORTUNITYEXAMINATION QUESTION PAPER

EXAMINER Dr. Valdemar J. Undji (NUST)

MODERATOR: Ms. Ndesheetelwa N. Shitenga (NUST)

INSTRUCTIONS

1. Read the questions carefully and answer ALL questions

2. Unless specified, all final answers must be round to 2 decimal places

3. Use 5% Significance level

4. Appendixes are attached

5. The use of a calculator is allowed

THIS QUESTION PAPERCONSISTSOF _6_ PAGES(Including this front page)

|

|

2 Page 2 |

▲back to top |

QUESTION 1

= a) Consider the following non-linear model: y

2

e(ax+bx + u).

[25 marks]

Transform the above model into a linear model which can be estimated by means of an ordinary

least square (OLS).

(4)

b) Interpret the coefficients of the transformed model you specified in (a).

(4)

c) Explain the following components of a time series and provide a relevant example for each:

i) Trend

(3)

ii) Cyclical

(3)

iii) Seasonal

(3)

iv) Irregular

(3)

= d) Consider the following autoregressive process of order one, AR(l): Yt PYt-i + Ut, where

Ut is a white-noise process. State the condition under which:

i) Yt is a stationary time series.

(2)

ii) Yt is a non-stationary time series.

(3)

2

|

|

3 Page 3 |

▲back to top |

OUESTION2

[251

2.1 Consider the following production model: GDPt = /30 + /31 EMPt + /32 GCFt+ ut, where

= E(u 2) a 2 GCF/. The dependent variable GDP is the level of economic growth. The independent

variables EMP and GCF denote employment and gross capital formation, respectively.

a) What obvious violation of the CLRM is depicted by the expected value of the squared residual?

Justify your answer.

(3)

b) State the appropriate approach for rectifying the issue identified in (a) and show how you would

go about rectify the problem.

(7)

c) Outline the consequences for the OLS estimates if the issue identified in (a) is ignored. (3)

(t) = 2.2 Consider the following regression model: Yt a0 + /3 + t:i

* 'r/ y,x 0

a) What sort of functional form is the model?

(2)

b) It is possible to estimate the model by means of an ordinary least square (OLS) estimation?

Justify your answer.

(4)

c) What is the behaviour of y as x tends to approach infinity?

(3)

d) Provide an example where such a model may be applicable.

(3)

3

|

|

4 Page 4 |

▲back to top |

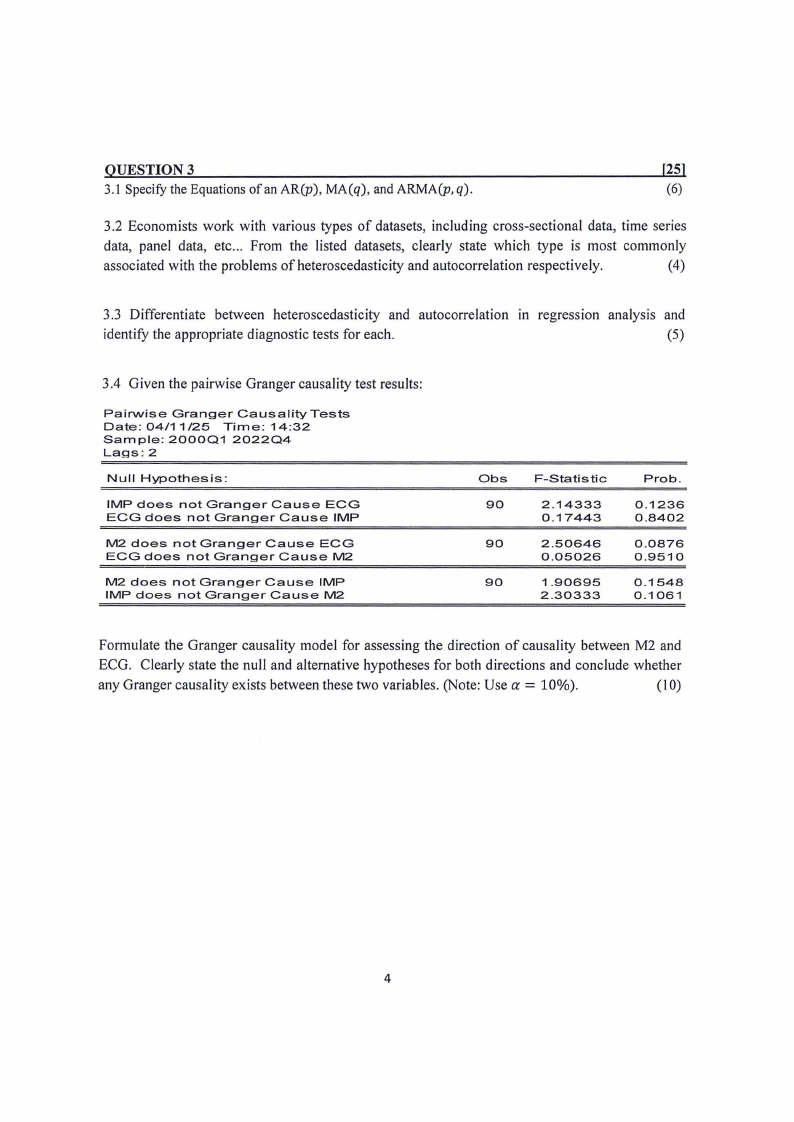

OUESTION3

[25)

3.1 Specify the Equations of an AR(p), MA(q), and ARMA(p, q).

(6)

3.2 Economists work with various types of datasets, including cross-sectional data, time series

data, panel data, etc ... From the listed datasets, clearly state which type is most commonly

associated with the problems of heteroscedasticity and autocorrelation respectively.

(4)

3 .3 Differentiate between heteroscedasticity and autocorrelation m regression analysis and

identify the appropriate diagnostic tests for each.

(5)

3.4 Given the pairwise Granger causality test results:

Pairwise

Granger

Date: 04/11 /25

Sam pie: 200001

Lags:2

Causality

Time: 14:32

202204

Tests

Null Hypothesis:

IMP does not Granger

Cause ECG

ECG does not Granger

Cause IMP

M2 does not Granger

Cause ECG

ECG does not Granger

Cause M2

M2 does not Granger

IMP does not Granger

Cause IMP

Cause M2

Obs

F-Statistic

90

2.14333

0.17443

90

2.50646

0.05026

90

1.90695

2.30333

Prob.

0.1236

0.8402

0.0876

0.9510

0.1548

0.1061

Formulate the Granger causality model for assessing the direction of causality between M2 and

ECG. Clearly state the null and alternative hypotheses for both directions and conclude whether

any Granger causality exists between these two variables. (Note: Use a= 10%).

(10)

4

|

|

5 Page 5 |

▲back to top |

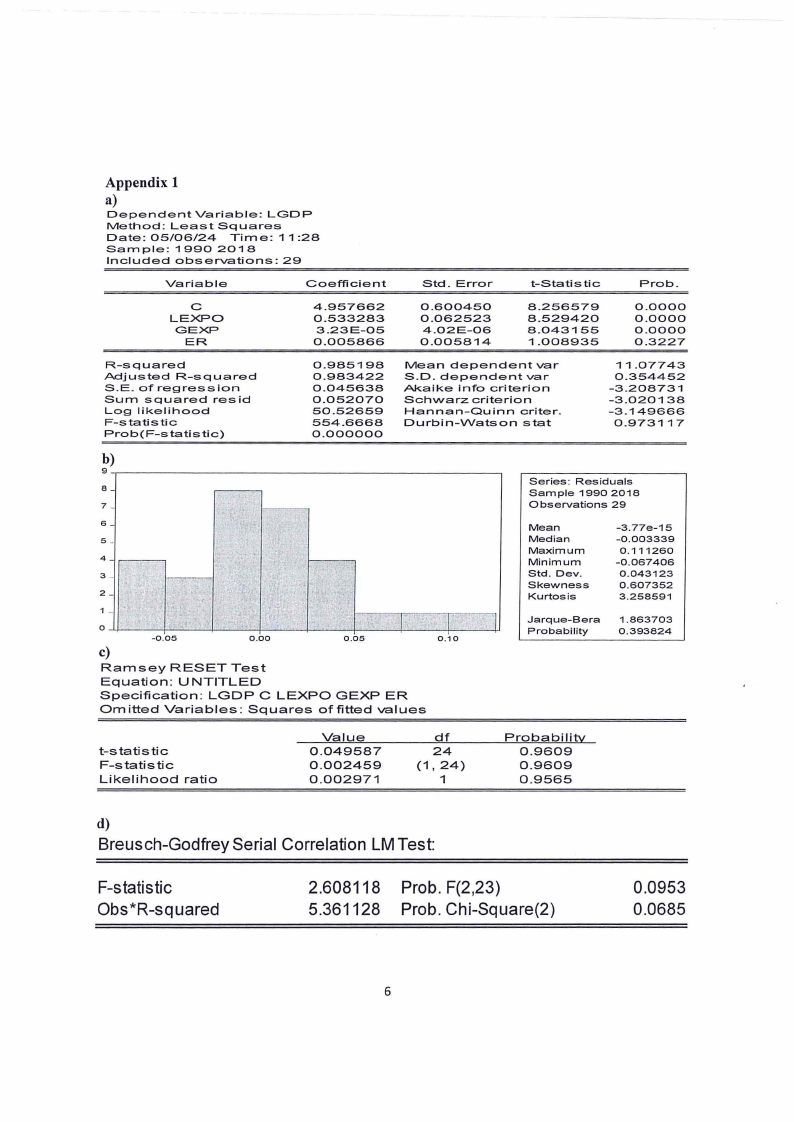

OUESTION4

[25]

Refer to Appendix l, which displays the output of the model examining the relationship between

exports of goods and services and economic growth, specified as follows:

Where, LGDP = Log of Gross Domestic Product; LEXPO = Log of Export, GEXP= Government

expenditure, ER =Exchange rate in US$.

Use Appendix l to answer the questions that follow.

a) Interpret the coefficients /31 and /32 .

(5)

b) Explain what the Variance Inflation Factor (VIF) is and its use.

(5)

c) Is the model's functional form correctly specified? Justify.

(5)

d) Are the residuals of the estimated regression normally distributed? Justify.

(5)

e) Does the model suffer from first order serial correlation? Justify.

(5)

5

|

|

6 Page 6 |

▲back to top |

Appendix 1

a)

Dependent

Variable:

Method:

Least

Squares

Date: 05/06/24

Time:

Sample:

1990 2018

Included

observations:

LGDP

11 :28

29

Variable

Coefficient

Std. Error

t-Statistic

Prob.

C

LEXPO

GEXP

ER

4.957662

0.533283

3.23E-05

0.005866

0.600450

0.062523

4.02E-06

0.005814

8.256579

8.529420

8.043155

1.008935

0.0000

0.0000

0.0000

0.3227

R-squared

Adjusted

R-squared

S.E. of regression

Sum squared

resid

Log likelihood

F-statistic

Prob(F-statistic)

0.985198

0.983422

0.045638

0.052070

50.52659

554.6668

0.000000

Mean dependent

var

S.D. dependent

var

Akaike

info criterion

Schwarz

criterion

Hannan-Quinn

criter.

Durbin-VVatson

stat

11.07743

0.354452

-3.208731

-3.020138

-3.149666

0.973117

b)

9---,---------------------------~

8

7-

6

5_

4

3_

2

1-

0 -4-----,----+-----+---+-----+--~-+---+-----+'

-0.05

0.00

0.05

0.10

c)

Ramsey

RESET Test

Equation:

UNTITLED

Specification:

LGDP C LEXPO GEXP ER

Omitted Variables:

Squares

of fitted values

Series: Residuals

Sample 1990 2018

Observations

29

Mean

Median

Maximum

Minimum

Std. Dev.

Skewness

Kurtosis

-3.77e-15

-0.003339

0.111260

-0.067406

0.043123

0.607352

3.258591

Jarque-Bera

Probability

1.863703

0.393824

t-statistic

F-s tati s tic

Likelihood

ratio

Value

0.049587

0.002459

0.002971

df

24

(1, 24)

1

Prob ab i I ity

0.9609

0.9609

0.9565

d)

Breusch-Godfrey Serial Correlation LM Test:

F-statistic

Obs*R-squared

2.608118 Prob. F(2,23)

5.361128 Prob. Chi-Square(2)

0.0953

0.0685

6