|

PAR812S-PUBLIC SECTOR FINANCIAL ACCOUNTING AND REPORTING-2ND OPP-DEC 2025 |

|

|

1 Page 1 |

▲back to top |

n Am I BI A u n IVER s I TY

OF SCI En CE Ano TECH n OLOGY

FACULTY OF COMMERCE, HUMAN SCIENCES AND EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING & FINANCE

QUALIFICATION: BACHELOR OF ACCOUNTING (HONOURS}

QUALIFICATION CODE: 08BOAH

COURSE CODE: PAR812S

LEVEL: 8

COURSE NAME: PUBLIC SECTOR FINANCIAL

ACCOUNTING & REPORTING

SESSION: DECEMBER 2025

DURATION: 3 HOURS

PAPER: THEORY AND APPLICATION

MARKS: 100

SECOND OPPORTUNITY EXAMINATION QUESTION PAPER

EXAMINERS: Mr. Kuhepa Tjondu

MODERATOR: Mr. Emmanuel Milijala

INSTRUCTIONS

• Th is question paper is made up of THREE (3) questions.

• Answer All the questions and in blue or black ink.

• Show all your working in the answer sheet.

• Start each question on a new page in your answer booklet and show all your workings.

• Questions relating to this paper may be raised in the initial 30 minutes after the start of

the paper. Thereafter, candidates must use their initiative to deal with any perceived error

or ambiguities and any assumption made by the candidate should be clearly stated.

PERMISSIBLE MATERIALS

Non-programmable calculator/financial calculator

THIS QUESTION PAPER CONSISTS OF 8 PAGES (Including this front page}

1

|

|

2 Page 2 |

▲back to top |

QUESTION 1

[25 MARKS]

a) The Ministry of Indigenous Enterprises has been charged to collect legacy fixed

assets data and value them in accordance with International Public Sector Accounting

Standards (IPSAS). The Fixed Assets Coordinating Unit (FACU) of the Ministry has

collected for valuation the following data for your action:

The Ministry owns a four (4) storey Office Administration block. The average cost per

floor is N$4, 741 ,256.25. The building was constructed on a land size of 20 plots of

land owned by the Ministry. Currently a plot of land in that area costs N$2,500 ,000 .

The FACU has measured the sizes of the building as follows: Length at 87.5 meters,

Width 42.65 meters. FACU intends to apply a reference price per square metre of

N$4,432 to the area of the measurement in order to determine the value of the asset.

However, a professional body, the Institute of Architects and Engineers has given the

reference price for cost of such office Building at an estimated price of N$87,965,025.

The building has not seen any further face lift ever since. However, a fence wall with

a gate to enforce security and secure the land has just been completed in the current

year at a cost of N$8,970,000 with a lifespan of 50 years.

The year of construction of the office building could not be determined, yet an old

watchman who had been there for ages remembers that the building was constructed

some 42 years ago, a time when his seventh child was born . It is the decision of

Government of Namibia on adoption of IPSAS not to take advantage of the three-year

exemption period, but account for legacy fixed assets by taking 60% of the reference

cost of the legacy assets as the Deemed cost, with reduced life span to 30 years.

Required:

i) Calculate the cost of the land and buildings with structures to be brought into the

books on adoption of IPSAS and determine the depreciation chargeable in the first

year in respect of these asset.

(9 marks)

ii) Show the extract of Statement of Financial Position of the Ministry of Indigenous

Enterprises as at that date.

(3 marks)

b) You are the Director of Finance at the Namibia Water Development Authority, an

entity under the Ministry of Forestry and Water. The Authority has a five-member

Board chaired by the daughter of the Sector Minister. The Chief Executive Officer of

the Authority has just been appointed by Government for an initial term of four years.

The Chairperson of the board runs boutique services. The Authority buys a lot of

presents from this boutique whenever they are confronted with the need to give out

presents to any high-profile person . The Chairperson has made a request to the

Authority to finance her boutique services with an amount of N$546,000 to enable her

business pay some urgent bills. No terms or conditions were provided in the request.

Such an assistance from a financial institution would attract current prevailing bank

interest on loan at a rate of 35% p.a . Recently another member of the Board contracted

loan from the Bank for her child 's university entrance fees at that rate.

2

|

|

3 Page 3 |

▲back to top |

Management of the Authority indicated that the amount was not significant to the

Authority and has been approved by the Head of the entity and the Chief Director. The

approved document has been handed over to you for payment. Considering the PFM

Laws and IPSAS, you engaged the Chief Director about the request, but you were

directed to go ahead and pay and use the appropriate accounting treatment in such

circumstances. You accordingly raised the necessary documentations and effected

the payment.

Required:

In relation to IPSAS 20: Related Party Disclosures:

i) Explain the implications of this transaction on the Authority and state how you would

account for this transaction in the financial statements of the entity.

(4 marks)

ii) State FOUR situations where related party transactions may lead to disclosures by

a reporting entity.

(4 marks)

iii) Explain FIVE reasons for disclosing related party transactions/relations. (5 marks)

QUESTION 2

[25 MARKS]

Namibia Wind Farms LTD, a State-Owned Enterprise (SOE), has appointed a new

Board of Directors in January 2023. The new Board after settling for a year, are

interested in assessing their performance for the year 2023 as against the

performance of the previous Board in the year 2022 through ratio analysis. Below is

the Financial Statement of Namibia Wind Farms LTD for the two years.

Namibia Wind Farms LTD

Statement of Profit or Loss for the Year Ended 31

December 2023

2023

2022

N$

N$

Revenue

9,860 ,000

6,218,000

Direct Cost

(5,905,000)

(5,822,000)

Gross Profit

3,955,000

396,000

Distribution costs

(297,000)

(264,000)

Administrative expenses

(505,000)

(455,000)

Other Income

236,000

13,000

Other gains

1,482,000

Operating Profit

3,389,000

1,172,000

Finance cost

(1 ,000,000)

(334 ,000)

3

|

|

4 Page 4 |

▲back to top |

Profit before tax

expense

Tax expense

Profit after tax

2,389,000

(500,000)

1,889,000

838,000

(144,000)

694,000

Namibia Wind Farms LTD

Statement of Financial Position as at 31

December

2023

N$

N$

ASSETS

2023

2022

Non-Current Assets

Property, plant

equipment

& 17,000,000

15,000,000

Investment

5,000

2,000

Advances & loans

30,000

Total

Assets

Non-Current 17,005,000

15,032,000

Current Assets

Inventories

687,000

546,000

Trade and

receivables

other 2,829,000

1,978,000

Prepayments

87,000

42 ,000

Cash and

equivalents

cash 383,000

434,000

Total Current Assets 3,986,000

3,000,000

TOTAL ASSETS

20,991,000

18,032,000

Equity attributable to the owners

Government equity

8,000

Other

Equity

Government 613,000

4

8,000

306,000

|

|

5 Page 5 |

▲back to top |

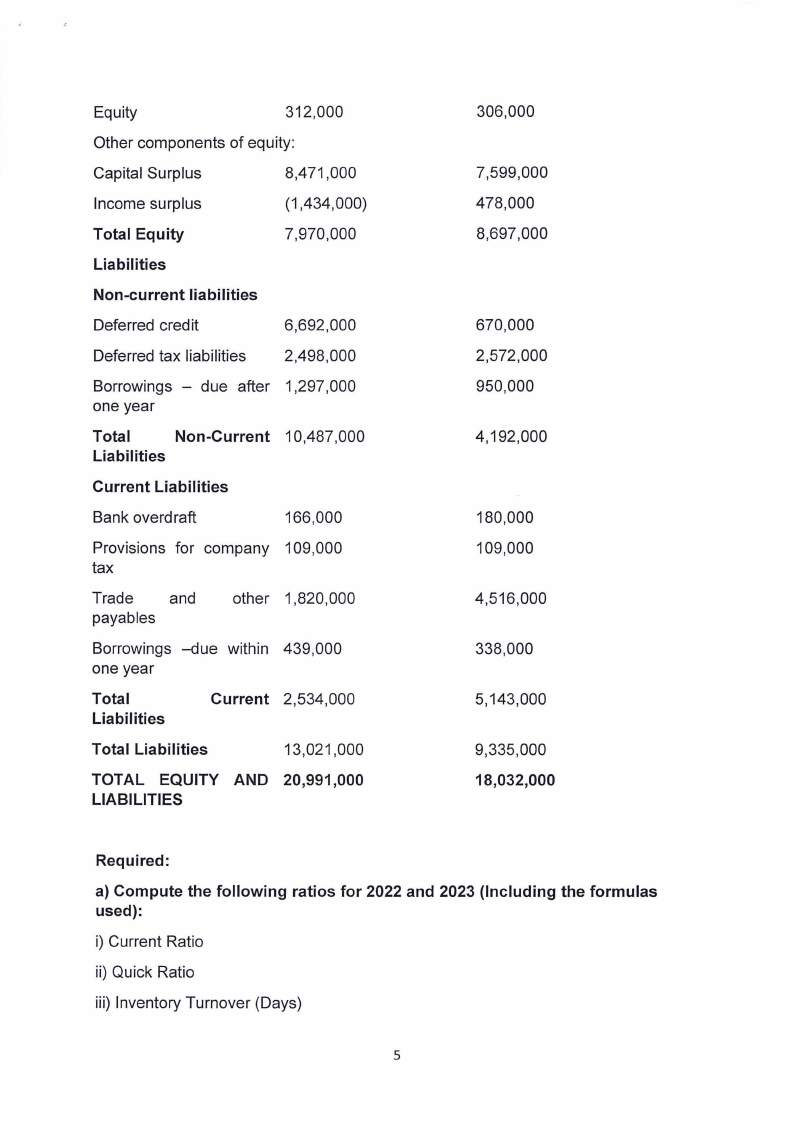

Equity

312,000

Other components of equity:

Capital Surplus

8,471,000

Income surplus

(1,434,000)

Total Equity

7,970 ,000

Liabilities

Non-current liabilities

Deferred credit

6,692,000

Deferred tax liabilities 2,498,000

Borrowings - due after 1,297,000

one year

Total

Non-Current 10,487,000

Liabilities

Current Liabilities

Bank overdraft

166,000

Provisions for company 109,000

tax

Trade and

payables

other 1,820,000

Borrowings -due within 439,000

one year

Total

Liabilities

Current 2,534,000

Total Liabilities

13,021 ,000

TOTAL EQUITY AND 20,991,000

LIABILITIES

306,000

7,599,000

478,000

8,697,000

670,000

2,572,000

950,000

4,192,000

180,000

109,000

4,516 ,000

338,000

5,143,000

9,335,000

18,032,000

Required:

a) Compute the following ratios for 2022 and 2023 (Including the formulas

used):

i) Current Ratio

ii) Quick Ratio

iii) Inventory Turnover (Days)

5

|

|

6 Page 6 |

▲back to top |

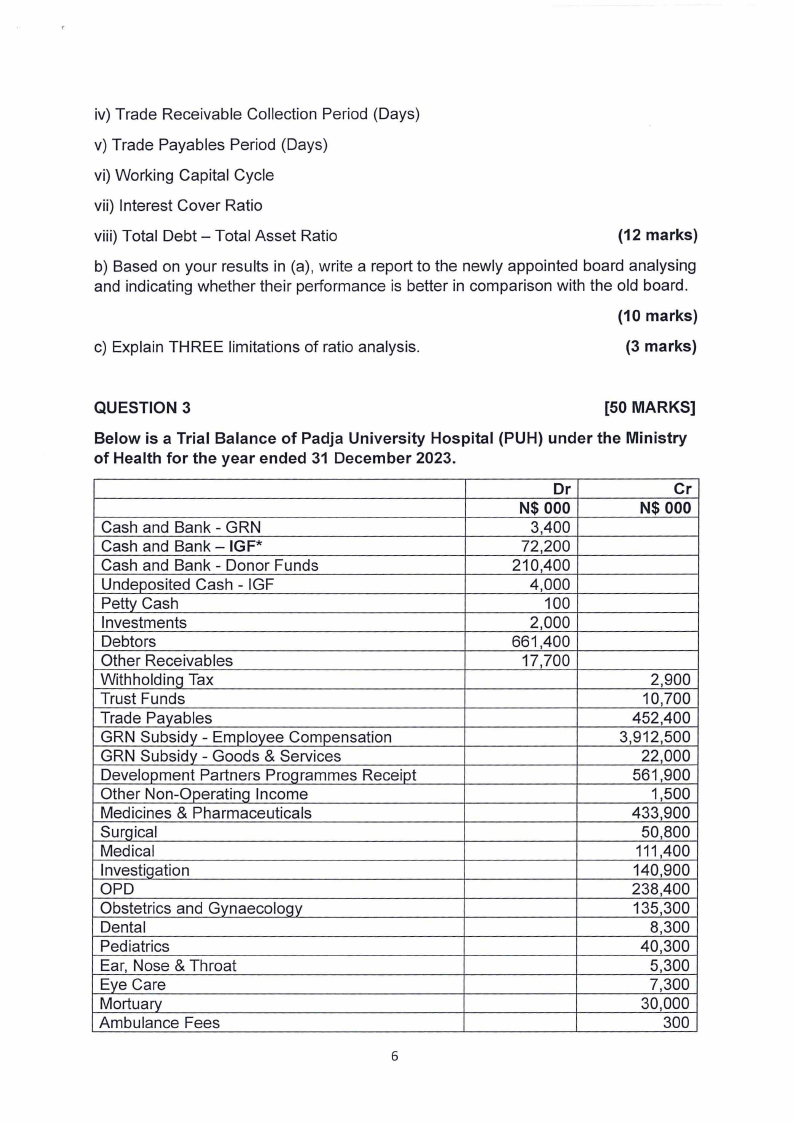

iv) Trade Receivable Collection Period (Days)

v) Trade Payables Period (Days)

vi) Working Capital Cycle

vii) Interest Cover Ratio

viii) Total Debt - Total Asset Ratio

(12 marks}

b) Based on your results in (a), write a report to the newly appointed board analysing

and indicating whether their performance is better in comparison with the old board.

(10 marks}

c) Explain THREE limitations of ratio analysis.

(3 marks}

QUESTION 3

[50 MARKS]

Below is a Trial Balance of Padja University Hospital (PUH} under the Ministry

of Health for the year ended 31 December 2023.

Cash and Bank - GRN

Cash and Bank - IGF*

Cash and Bank - Donor Funds

Undeposited Cash - IGF

Petty Cash

Investments

Debtors

Other Receivables

Withholding Tax

Trust Funds

Trade Payables

GRN Subsidy - Employee Compensation

GRN Subsidy - Goods & Services

Development Partners Proqrammes Receipt

Other Non-Operatinq Income

Medicines & Pharmaceuticals

Surgical

Medical

Investigation

OPD

Obstetrics and Gynaecoloqy

Dental

Pediatrics

Ear, Nose & Throat

Eye Care

Mortuary

Ambulance Fees

Dr

N$ 000

3,400

72,200

210,400

4,000

100

2,000

661,400

17,700

Cr

N$ 000

2,900

10,700

452,400

3,912,500

22,000

561,900

1,500

433,900

50,800

111,400

140,900

238,400

135,300

8,300

40,300

5,300

7,300

30,000

300

6

|

|

7 Page 7 |

▲back to top |

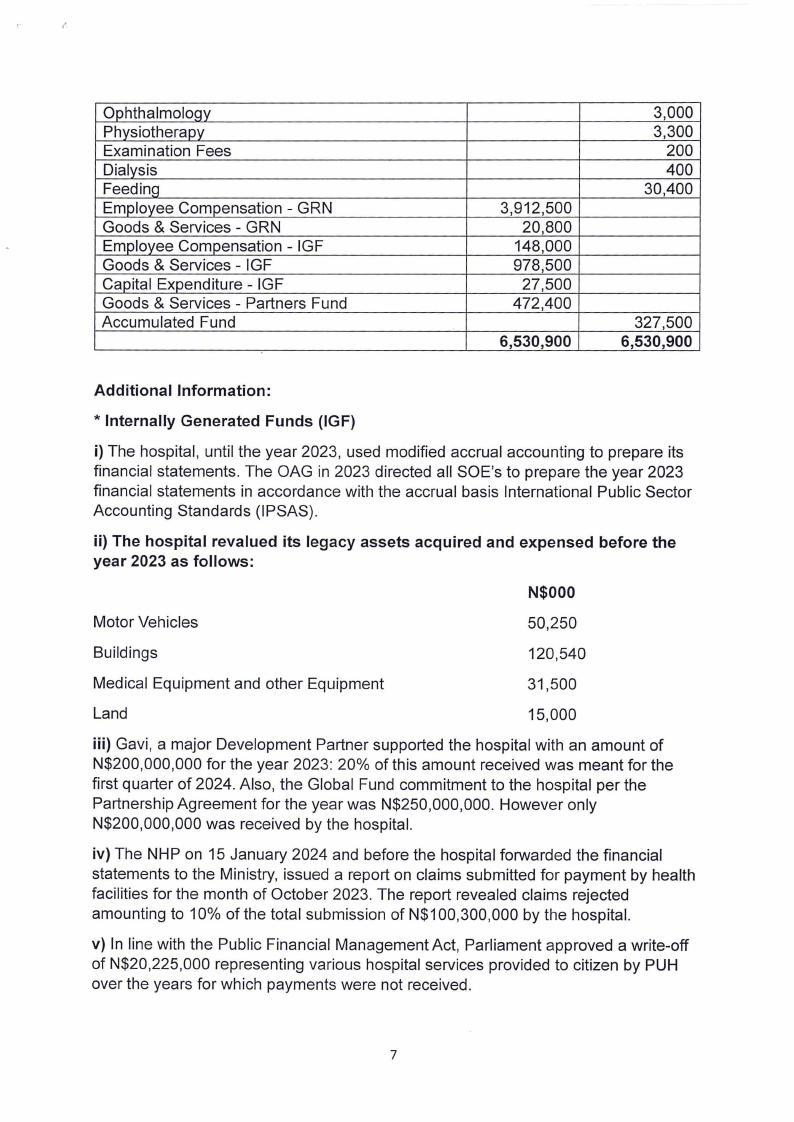

(

Oohthalmoloqy

Physiotherapy

Examination Fees

Dialysis

FeedinQ

Employee Compensation - GRN

Goods & Services - GRN

Employee Compensation - IGF

Goods & Services - IGF

Capital Expenditure - IGF

Goods & Services - Partners Fund

Accumulated Fund

3,912,500

20,800

148,000

978,500

27,500

472,400

6,530,900

3,000

3,300

200

400

30,400

327,500

6,530,900

Additional Information:

* Internally Generated Funds (IGF)

i) The hospital, until the year 2023, used modified accrual accounting to prepare its

financial statements. The OAG in 2023 directed all SOE's to prepare the year 2023

financial statements in accordance with the accrual basis International Public Sector

Accounting Standards (IPSAS) .

ii) The hospital revalued its legacy assets acquired and expensed before the

year 2023 as follows:

N$000

Motor Vehicles

50,250

Buildings

120,540

Medical Equipment and other Equipment

31,500

Land

15,000

iii) Gavi, a major Development Partner supported the hospital with an amount of

N$200,000,000 for the year 2023: 20% of this amount received was meant for the

first quarter of 2024. Also, the Global Fund commitment to the hospital per the

Partnership Agreement for the year was N$250,000,000. However only

N$200,000,000 was received by the hospital.

iv) The NHP on 15 January 2024 and before the hospital forwarded the financial

statements to the Ministry, issued a report on claims submitted for payment by health

facilities for the month of October 2023 . The report revealed claims rejected

amounting to 10% of the total submission of N$100,300,000 by the hospital.

v) In line with the Public Financial Management Act, Parliament approved a write-off

of N$20,225,000 representing various hospital services provided to citizen by PUH

over the years for which payments were not received.

7

|

|

8 Page 8 |

▲back to top |

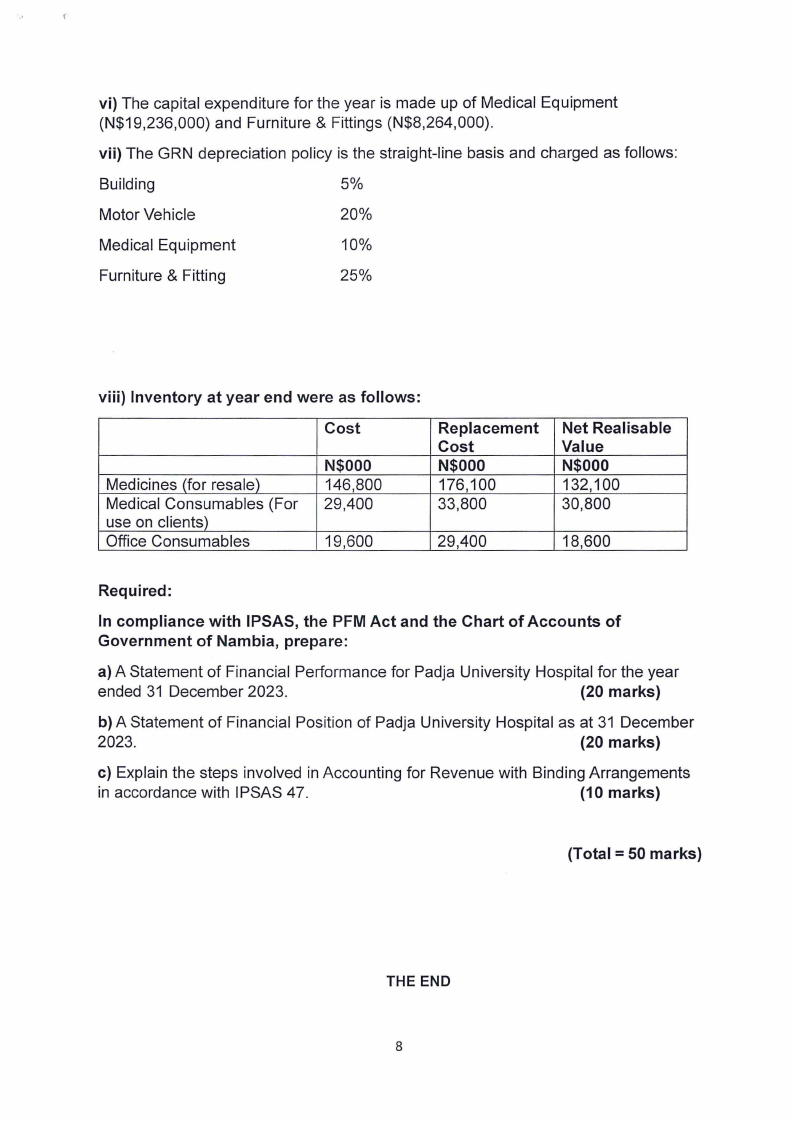

vi) The capital expenditure for the year is made up of Medical Equipment

(N$19,236 ,000) and Furniture & Fittings (N$8,264,000).

vii) The GRN depreciation policy is the straight-line basis and charged as follows :

Building

5%

Motor Vehicle

20%

Medical Equipment

10%

Furniture & Fitting

25%

viii) Inventory at year end were as follows:

Cost

Medicines (for resale)

Medical Consumables (For

use on clients)

Office Consumables

N$000

146,800

29,400

19,600

Replacement

Cost

N$000

176,100

33,800

29,400

Net Realisable

Value

N$000

132,100

30,800

18,600

Required:

In compliance with IPSAS, the PFM Act and the Chart of Accounts of

Government of Nambia, prepare:

a) A Statement of Financial Performance for Padja University Hospital for the year

ended 31 December 2023.

(20 marks)

b) A Statement of Financial Position of Padja University Hospital as at 31 December

2023 .

(20 marks)

c) Explain the steps involved in Accounting for Revenue with Binding Arrangements

in accordance with IPSAS 47.

(10 marks)

(Total= 50 marks)

THE END

8