|

CAC710S-COMPUTERISED ACCOUNTING 301-1ST OPP-JUNE 2025 |

|

|

1 Page 1 |

▲back to top |

n Am I BI A u n IVER s ITY

OF SCIEn CE AnD TECHn OLOGY

FACULTY OF COMMERCE, HUMAN SCIENCE AND EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING & FINANCE

QUALIFICATION: BACHELOR OF ACCOUNTING/BACHELOR OF ACCOUNTING (CA)

QUALIFICATION CODE: 07BGAC/07BACC

COURSE CODE: CAC710S

LEVEL: 7

COURSE NAME: COMPUTERISED

ACCOUNTING 301

SESSION: JUNE 2025

PAPER: PRACTICAL

DURATION: 3 HOURS (Including printing and set

up)

MARKS: 100

FIRST OPPORTUNITY EXAMINATION QUESTION PAPER

EXAMINERS:

H Namwandi, Y Elago, C Mahindi and A Peter

MODERATOR: E Milijala

INSTRUCTIONS

• This question paper comprises one (1) question, split into three parts.

• Ensure your student number appears on all reports (Generated through the system,

not handwritten).

• It's your responsibility to ensure that all reports are printed and submitted.

• Ensure that all work done during the assessment is your own.

• The use of the internet on any electronic device is prohibited during the assessment.

• Questions relating to this paper may be raised in the initial 30 minutes after the start

of the paper. Thereafter, candidates must use their initiative to deal with any

perceived error or ambiguities and any assumption made by the candidate should be

clearly stated.

PERMISSIBLE MATERIALS

Non-programmable calculator

THIS QUESTION PAPER CONSISTS OF 7 PAGES (Including this front page)

|

|

2 Page 2 |

▲back to top |

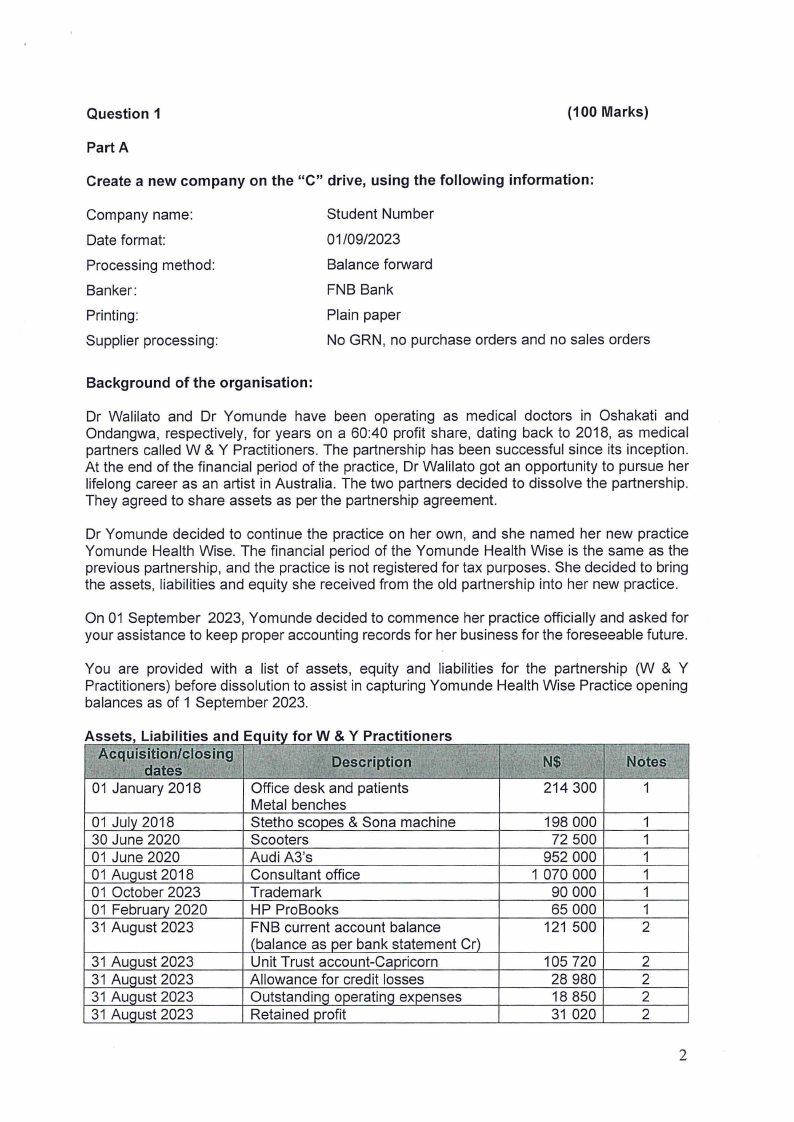

Question 1

(100 Marks)

Part A

Create a new company on the "C" drive, using the following information:

Company name:

Date format:

Processing method:

Banker:

Printing:

Supplier processing:

Student Number

01/09/2023

Balance forward

FNB Bank

Plain paper

No GRN, no purchase orders and no sales orders

Background of the organisation:

Dr Walilato and Dr Yomunde have been operating as medical doctors in Oshakati and

Ondangwa, respectively, for years on a 60:40 profit share, dating back to 2018, as medical

partners called W & Y Practitioners. The partnership has been successful since its inception.

At the end of the financial period of the practice, Dr Walilato got an opportunity to pursue her

lifelong career as an artist in Australia. The two partners decided to dissolve the partnership.

They agreed to share assets as per the partnership agreement.

Dr Yomunde decided to continue the practice on her own, and she named her new practice

Yomunde Health Wise. The financial period of the Yomunde Health Wise is the same as the

previous partnership, and the practice is not registered for tax purposes. She decided to bring

the assets, liabilities and equity she received from the old partnership into her new practice.

On 01 September 2023, Yomunde decided to commence her practice officially and asked for

your assistance to keep proper accounting records for her business for the foreseeable future.

You are provided with a list of assets, equity and liabilities for the partnership (W & Y

Practitioners) before dissolution to assist in capturing Yomunde Health Wise Practice opening

balances as of 1 September 2023.

Asse ts, L"Ia bT1f1 Ies an d E:QUl·ttV for W & Y PractITIoners

Ac(luisitic1m/closing

. dates

:

Description

.. /

\\:'

01 January 2018

Office desk and patients

Metal benches

01 July 2018

Stetho scooes & Sona machine

30 June 2020

Scooters

01 June 2020

Audi A3's

01 August 2018

Consultant office

01 October 2023

Trademark

01 February 2020

HP ProBooks

31 August 2023

FNB current account balance

(balance as per bank statement Cr)

31 August 2023

Unit Trust account-Caoricorn

31 Auqust 2023

Allowance for credit losses

31 August 2023

Outstandinq operatinq expenses

31 August 2023

Retained profit

,_

N$

·\\ ,~Notes

214 300

1

198 000

1

72 500

1

952 000

1

1 070 000

1

90 000

1

65 000

1

121 500

2

105 720

2

28 980

2

18 850

2

31 020

2

2

|

|

3 Page 3 |

▲back to top |

31 August 2023

31 August 2023

31 August 2023

31 August 2023

PSMES (PSM555) - receivable

Kuku Gwashambo (KKG666) -

receivable

Victoria Pharmacy (VP6886) -

payable

Lady Pohamba Hospital (LP777) -

payable

80 000

2

34 150

2

58 800

2

76 300

2

Notes 1: Property, plant and equipment's depreciation policy:

Property, plant and equipment owned by the practice are depreciated using the following

policy:

• All property, plant and equipment owned by the organisation are depreciated using the

straight-line method at a rate of 10% per annum.

• Depreciation is calculated on assets in existence at the end of each year, giving a full

year's depreciation even though the asset was bought part of the way through the year.

• No depreciation is to be charged on assets in the year of disposal.

• Trademarks and Land &buildings are not depreciated.

• The date of the transaction is the date when the assets were bought.

Note 2:

According to the dissolution agreement, cash and cash equivalents, receivables, liabilities,

and equity accounts will be shared equally because Dr Yomunde was the partner who worked

in the practice on a full-time basis. Dr Walilato will be responsible for paying off all her liabilities

in her personal capacity. All payables were informed through a hired lawyer to assist with the

dissolution agreement.

Required:

You must capture the opening balance accounts, including capital contribution and

accumulated depreciation for all non-current assets as of 1 September 2023 for Yomunde

Health Wise Practice (Period one).

UPDATE YOUR TRANSACTIONS BEFORE PROCEEDING TO THE NEXT QUESTION.

YOU ARE NOT REQUIRED TO PRINT ANY REPORT AT THIS STAGE.

Part B: Period One Transactions

In this section, you are required to process the payments and receipt transactions. All

transactions must be processed only in the general ledger {GL). No creation/modification of

accounts in the GL.

You were informed that the transactions in period one (1) for the FNB bank account were not

all recorded. The Dr asked you to assist in updating this account's transactions and prepare a

bank reconciliation after receiving the bank statement (see Annexure A on page 6).

3

|

|

4 Page 4 |

▲back to top |

The following EFT payments and receipts were made in the practice books.

EFT2602

EFT2603

EFT2604

FFT2606

EFT2608

EFT26011

FFT2610

DEP1101

DEP1103

DEP1104

DEP1105

Casual medical doctors fees

FedEx Namibia service fees

Santam Namibia service fees

Lady Pohamba Hospital - Account payment

Sisa Namdje & Co - (attorney fees)

Medisun Pharmacy - Medical supplies

Secretary's remuneration

Capricorn - Unit Trust Interest

PSMES - Account payment

Monthly consulting fees - cash patients

Kuku Gashambo - Account payment

N$8 580

N$4 370

N$2 810

N$21 750

N$8 470

N$34 550

N$6 050

N$2 490

N$31 760

N$47 370

N$5 960

Part C

Yomunde Health Wise Practice year-end adjustments:

Dr Yomunde provided you with the following year-end adjustments, which have not yet been

recorded in the practice's books. All year-end adjustments should be processed in period 12.

• At the end of the financial period, the Oshakati High Court declared Kuku Gwashambo

insolvent. This was done because she faced many financial difficulties meeting her

monthly debts.

• Dr Yomunde brought in an Erf (305 square meters) valued at N$310 700. She acquired

the Erf in her private capacity in Tsumeb and intends to open another branch in that

town in the next two years.

• The scooter owned by the practice, which cost N$29 000, was involved in an accident

on 31 July 2024. The scooter was not insured at the time of the accident.

• At the end of the financial period, Dr Yomunde adjusted the allowance for credit losses

at a rate of 10% on all outstanding receivables.

• Provide for depreciation on all non-current assets owned by the entity during the

current financial period.

4

|

|

5 Page 5 |

▲back to top |

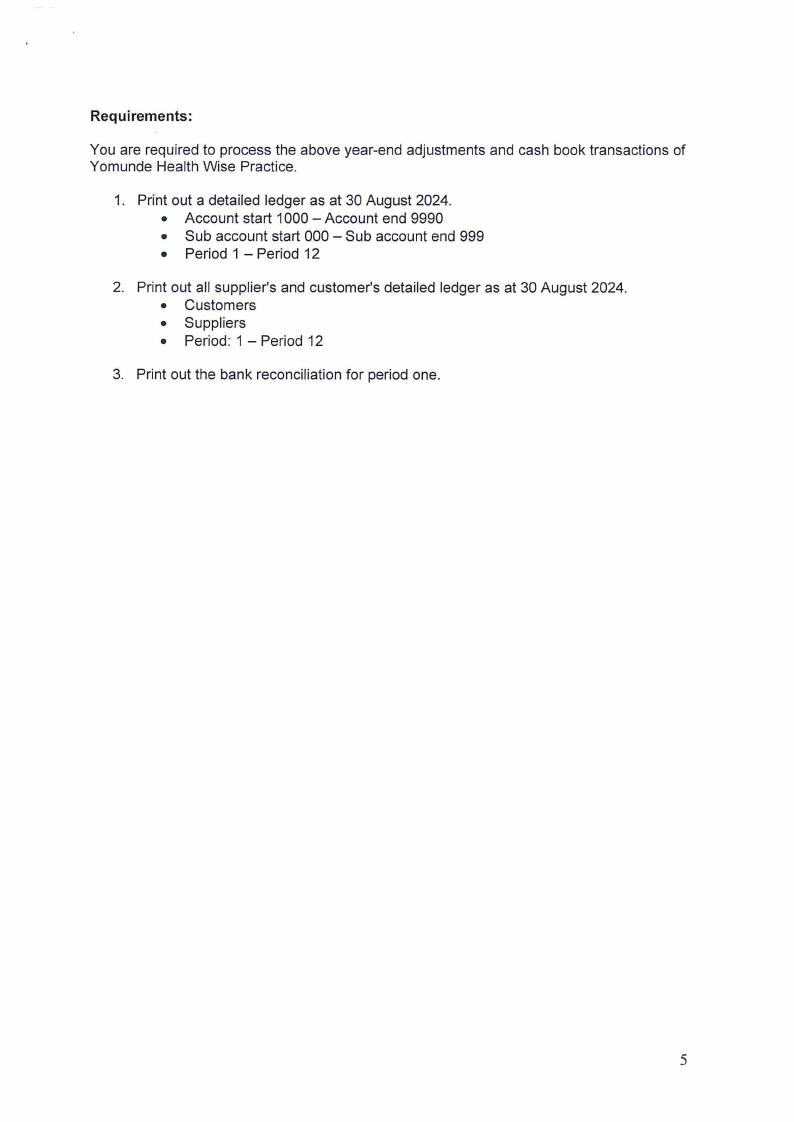

Requirements:

You are required to process the above year-end adjustments and cash book transactions of

Yomunde Health Wise Practice.

1. Print out a detailed ledger as at 30 August 2024.

• Account start 1000 - Account end 9990

• Sub account start 000 - Sub account end 999

• Period 1 - Period 12

2. Print out all supplier's and customer's detailed ledger as at 30 August 2024.

• Customers

• Suppliers

• Period: 1 - Period 12

3. Print out the bank reconciliation for period one.

5

|

|

6 Page 6 |

▲back to top |

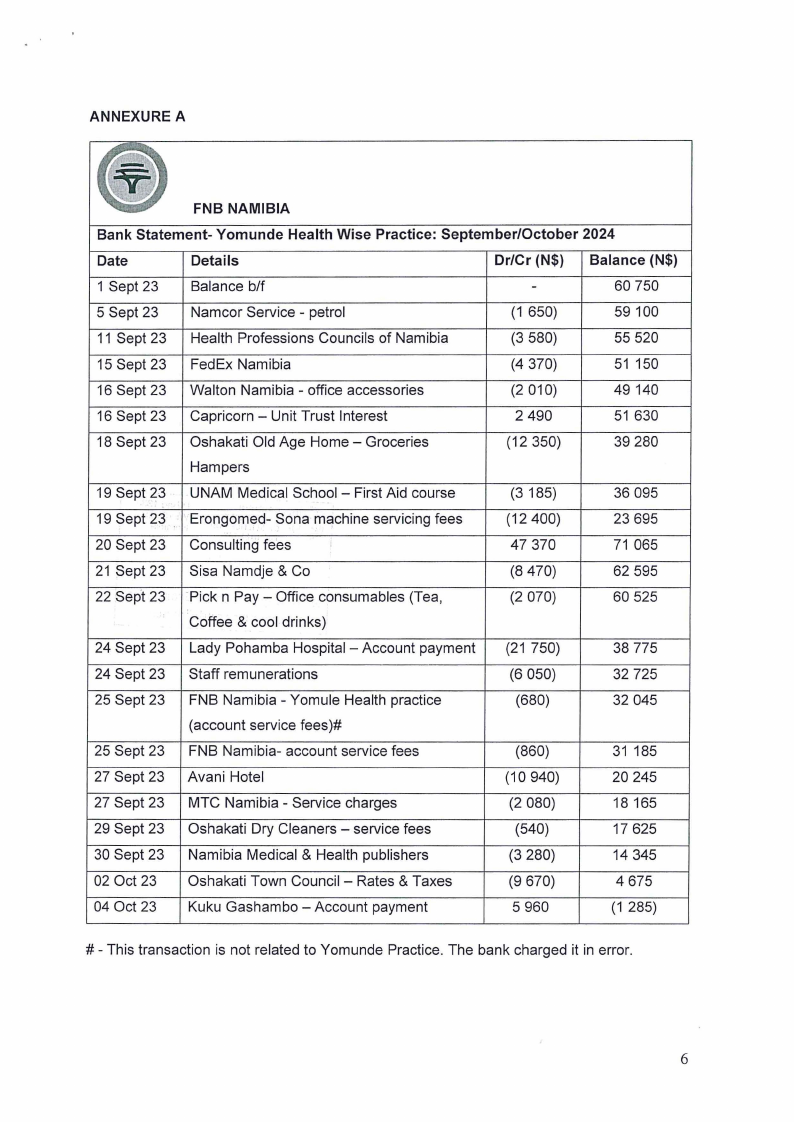

ANNEXURE A

---·,"' -~ .......

-

FNB NAMIBIA

Bank Statement- Yomunde Health Wise Practice: September/October 2024

Date

Details

Dr/Cr (N$) Balance (N$)

1 Sept 23 Balance b/f

-

60 750

5 Sept 23 Namcor Service - petrol

(1 650)

59 100

11 Sept 23 Health Professions Councils of Namibia

(3 580)

55 520

15 Sept 23 FedEx Namibia

(4 370)

51 150

16 Sept 23 Walton Namibia - office accessories

(2 010)

49 140

16 Sept 23 Capricorn - Unit Trust Interest

2 490

51 630

18 Sept 23 Oshakati Old Age Home - Groceries

(12 350)

39 280

Hampers

19 Sept 23 UNAM Medical School - First Aid course

(3 185)

36 095

19 Sept 23 . Erongon:,ed- Sona machine servicing fees

(12 400)

23 695

20 Sept 23 Consulting fees

47 370

71 065

21 Sept 23 Sisa Namdje & Co

(8 470)

62 595

22 Sep·t23 ·Pick n Pay - Office consumables (Tea,

(2 070)

60 525

Coffee & cool drinks)

24 Sept 23 Lady Pohamba Hospital - Account payment (21 750)

38 775

24 Sept 23 Staff remunerations

(6 050)

32 725

25 Sept 23 FNB Namibia - Yomule Health practice

(680)

32 045

(account service fees)#

25 Sept 23 FNB Namibia- account service fees

(860)

31 185

27 Sept 23 Avani Hotel

(10 940)

20 245

27 Sept 23 MTC Namibia - Service charges

(2 080)

18 165

29 Sept 23 Oshakati Dry Cleaners - service fees

(540)

17 625

30 Sept 23 Namibia Medical & Health publishers

(3 280)

14 345

02 Oct 23 Oshakati Town Council - Rates & Taxes

(9 670)

4 675

04 Oct 23 Kuku Gashambo - Account payment

5 960

(1 285)

# - This transaction is not related to Yomunde Practice. The bank charged it in error.

6