|

FMH810S-FINANCIAL MANAGEMENT FOR HOSPITALITY AND TOURISM-2ND OPP- JULY 2025 |

|

|

1 Page 1 |

▲back to top |

nAm I BI A u n IVE RS ITV

OF SCIEnCE Ano

FACULTY OF COMMERCE, HUMAN SCIENCESAND EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING & FINANCE

QUALIFICATION: BACHELOR OF HOSPITALITY AND

TOURISM MANAGEMENT HONOURS

QUALIFICATION CODE: 08BHTH

LEVEL: 8

COURSE CODE: FMH810S

COURSE NAME: FINANCIAL MANAGEMENT FOR

HOSPITALITY AND TOURISM

SESSION: JULY 2025

DURATION: 3 HOURS

PAPER: THEORY AND APPLICATION

MARKS: 100

SECOND OPPORTUNITY EXAMINATION QUESTION PAPER

EXAMINERS:

Kuhepa Tjondu

MODERATOR: Mr. A Okafor

INSTRUCTIONS

• This question paper is made up of FIVE (5) questions.

• Start each question on a new page.

• Answer All the questions and in blue or black ink.

• You are advised to pay due attention to expression and presentation. Failure to do so will

cost you marks.

• Start each question on a new page in your answer booklet and show all your workings.

• Questions relating to this paper may be raised in the initial 30 minutes after the start of

the paper. Thereafter, candidates must use their initiative to deal with any perceived error

or ambiguities and any assumption made by the candidate should be clearly stated.

PERMISSIBLE MATERIALS

Non-programmable calculator/financial calculator

THIS QUESTION PAPER CONSISTS OF 6 PAGES {Including this front page}

1

|

|

2 Page 2 |

▲back to top |

Question 1

(20 marks)

Namibia Railway Company (NRC) was considering two options for a new railway line

connecting two towns. Route A involved cutting a channel through an area designated

as being of special scientific importance because it was one of a very few suitable

feeding grounds for a colony of endangered birds. The birds were considered to be an

important part of the local environment with some potential influences on local

ecosystems.

The alternative was Route B which would involve the compulsory purchase and

destruction of Frekkie Stein's farm. Mr Stein was a vocal opponent of the Route B plan.

He said that he had a right to stay on the land which had been owned by his family for

four generations and which he had developed into a profitable farm. The farm

employed a number of local people whose jobs would be lost if Route B went through

the house and land. Mr Stein threatened legal action against NRC if Route B was

chosen.

An independent legal authority has determined that the compulsory purchase price of

Mr Stein's farm would be N$1 million if Route B was chosen. NRC considered this a

material cost, over and above other land costs, because the projected net present

value (NPV) of cash flows over a ten-year period would be N$5 million without buying

the farm. This would reduce the NPV by N$1 million if Route B was chosen.

The local government authority had given both routes provisional planning permission

and offered no opinion of which it preferred. It supported infrastructure projects such

as the new railway line, believing that either route would attract new income and

prosperity to the region. It took the view that as an experienced railway builder, NRC

would know best which to choose and how to evaluate the two options. Because it

was very keen to attract the investment, it left the decision entirely to NRC. NRC

selected Route A as the route to build the new line.

A local environmental pressure group, 'Save the Birds', was outraged at the decision

to choose Route A. It criticised NRC and also the local authority for ignoring the

sustainability implications of the decision. It accused the company of profiting at the

expense of the environment and threatened to use 'direct action' to disrupt the building

of the line through the birds' feeding ground if Route A went ahead.

REQUIRED:

(a)

Assess the decision to choose Route A by focusing on financial, legal,

ethical, environmental, sustainability and other factors.

(10)

(b) Discuss the importance and/or possible consequemces to NRC of

recognising all of the stakeholders in a decision such as deciding between (5)

Route A and Route B.

(c) Explain what a stakeholder 'claim' is, and critically assess the stakeholder

claims of Frekkie Stein, the local government authority and the colony of (5)

endangered birds.

TOTAL

(20)

2

|

|

3 Page 3 |

▲back to top |

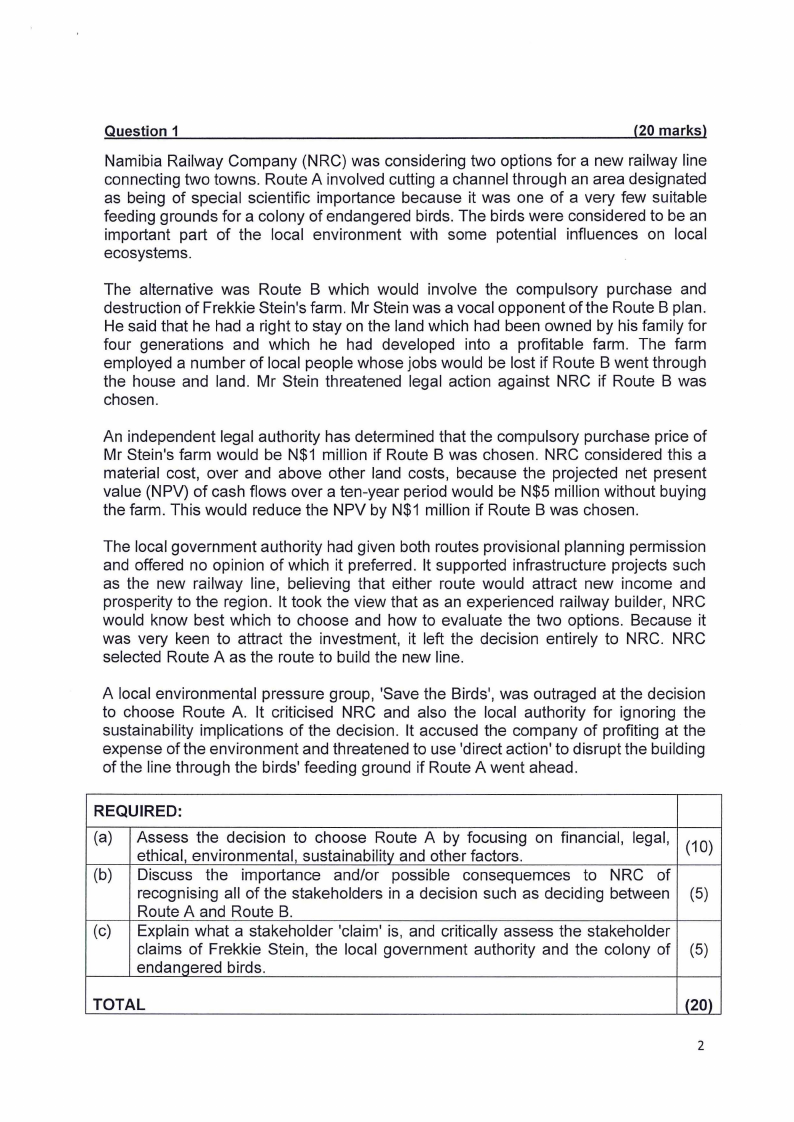

QUESTION 2

[21 MARKS]

You are working with the Chief Financial Officer (CFO) to determine the financial

viability of a number of projects and possible investments. As part of the preliminary

work your are given the following task:

Kudu Co needs to increase production capacity to meet increasing demand for an

existing product, 'Quago', which is used in food processing. A new machine, with a

useful life of four years and a maximum output of 600,000 kg of Quago per year, could

be bought for N$800,000, payable immediately. The machine has no scrap value. The

Cost of Capital for this project is estimated to be 10% and the forecast after tax

Cashflows over the next five years is as follows:

Time

Cashflow (N$)

1

200 000

2

290 000

3

338 000

4

310 000

5

-16 000 {Loss)

REQUIRED:

(a)

Calculate the net present value of buying the new machine (work to the

nearest N$1, 000) and advise on the acceptability of the proposed purchase.

(10)

(b) Calculate NPV of buying the new machine at a cost of capital of 15% and

the internal rate of return (IRR) (work to the nearest N$1,000) and Advise (11)

on the acceptability of the proposed purchase.

TOTAL

(21)

3

|

|

4 Page 4 |

▲back to top |

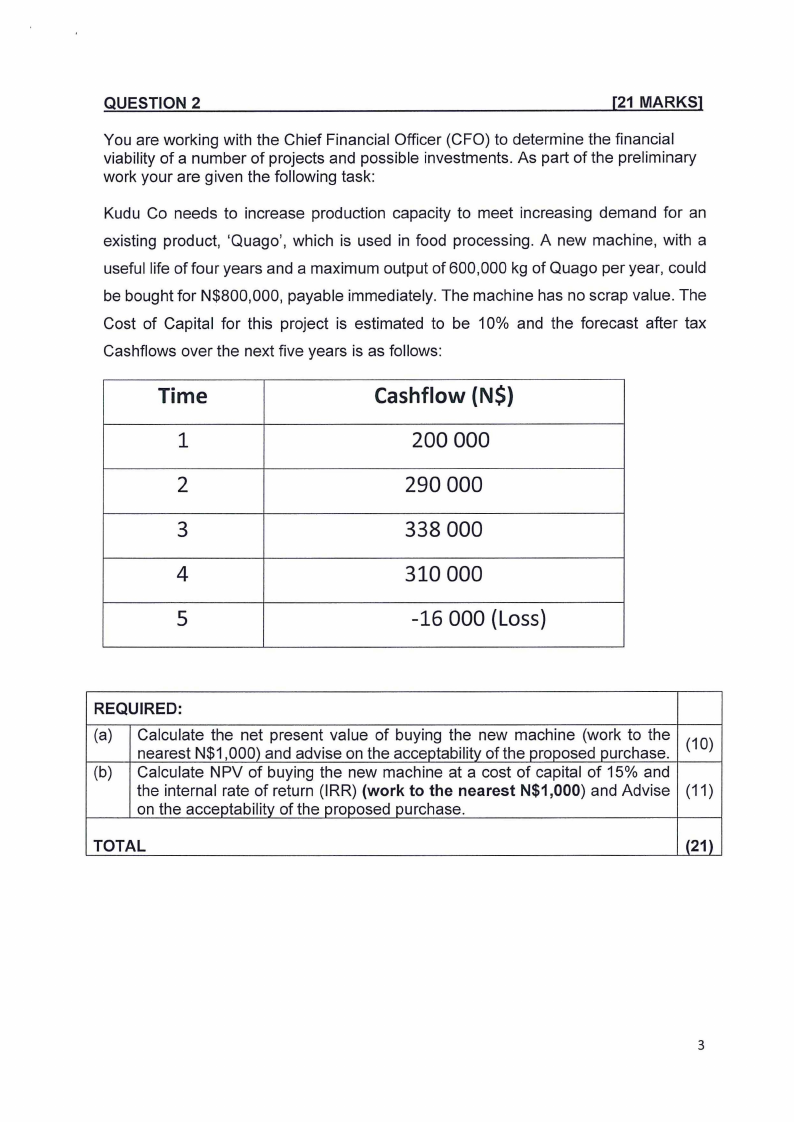

QUESTION 3

[9 MARKS]

Aibes hospitality and tourism runs a lucrative hotel situated in Windhoek.

Statements of profit or loss for the year ended 30 June 2024

Revenue

Cost of Sales

2024

$000

1,391,820

(1,050,825)

2023

$000

1t 159,850

(753,450)

Gross profit

Operating expenses

340,995

(161,450)

406,400

(170,950)

Profit from operations

Finance costs

179,545

(10,000)

235,450

(14,000)

Profits before tax

Tax

169,545

(50,800)

221,450

(66,300)

Profit for the year

118,745

155,150

Statements of financial position as at 30 June

Non-current assets

Current assets

Inventory

Receivables

Bank

2024

$000

509,590

109,400

419,455

2023

$000

341,400

88,760

206,550

95,400

1,038,445 732,110

Share capital

Share premium

Revaluation reserve

Retained earnings

100,000

20,000

50,000

376,165

100,000

20,000

287,420

546,165

407,420

Non-current liabilities

Current liabilities

Payables

Overdraft

Tax

61,600

295,480

80,200

55,000

83,100

179,590

62,000

1,038,445 732,110

4

|

|

5 Page 5 |

▲back to top |

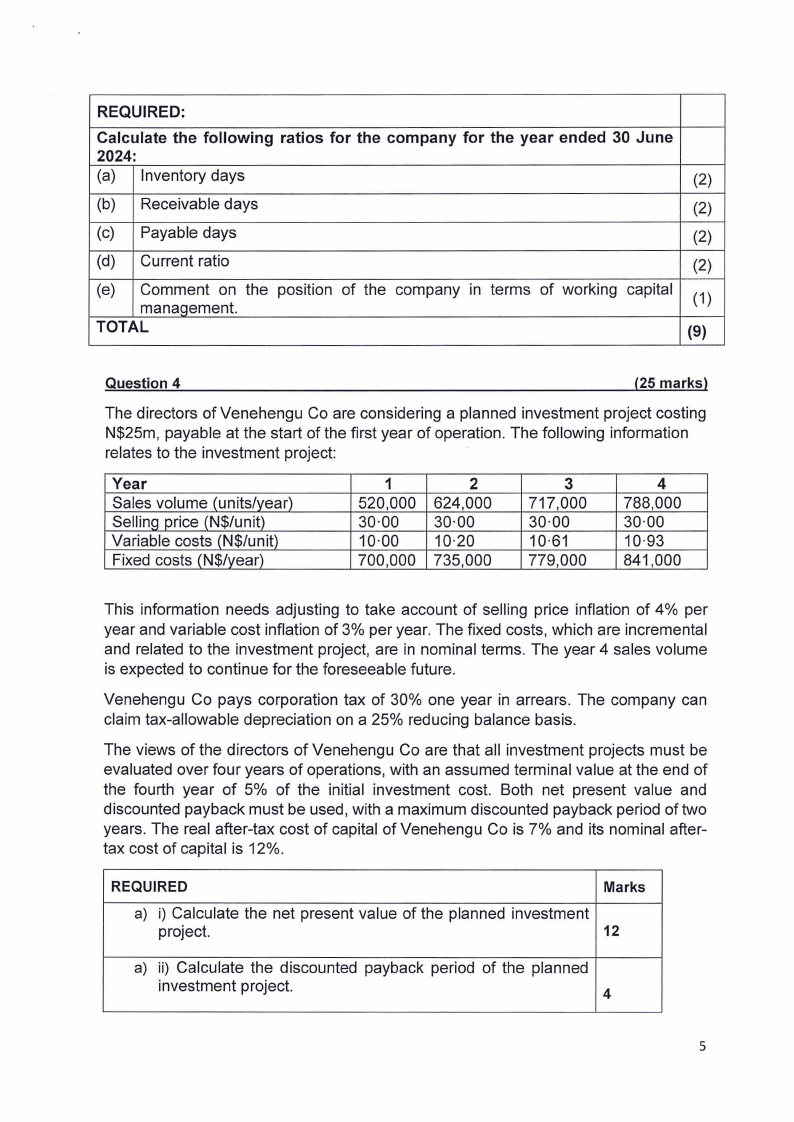

REQUIRED:

Calculate the following ratios for the company for the year ended 30 June

2024:

(a) Inventory days

(2)

(b) Receivable days

(2)

(c) Payable days

(2)

(d) Current ratio

(2)

(e)

Comment on the position of the company in terms of working capital

management.

(1)

TOTAL

(9)

Question 4

(25 marks)

The directors of Venehengu Co are considering a planned investment project costing

N$25m, payable at the start of the first year of operation. The following information

relates to the investment project:

Year

Sales volume (units/year)

Selling price (N$/unit)

Variable costs (N$/unit)

Fixed costs (N$/year)

1

520,000

30·00

10·00

700,000

2

624,000

30·00

10·20

735,000

3

717,000

30·00

10·61

779,000

4

788,000

30·00

10·93

841,000

This information needs adjusting to take account of selling price inflation of 4% per

year and variable cost inflation of 3% per year. The fixed costs, which are incremental

and related to the investment project, are in nominal terms. The year 4 sales volume

is expected to continue for the foreseeable future.

Venehengu Co pays corporation tax of 30% one year in arrears. The company can

claim tax-allowable depreciation on a 25% reducing balance basis.

The views of the directors of Venehengu Co are that all investment projects must be

evaluated over four years of operations, with an assumed terminal value at the end of

the fourth year of 5% of the initial investment cost. Both net present value and

discounted payback must be used, with a maximum discounted payback period of two

years. The real after-tax cost of capital of Venehengu Co is 7% and its nominal after-

tax cost of capital is 12%.

REQUIRED

a) i) Calculate the net present value of the planned investment

project.

Marks

12

a) ii) Calculate the discounted payback period of the planned

investment project.

4

5

|

|

6 Page 6 |

▲back to top |

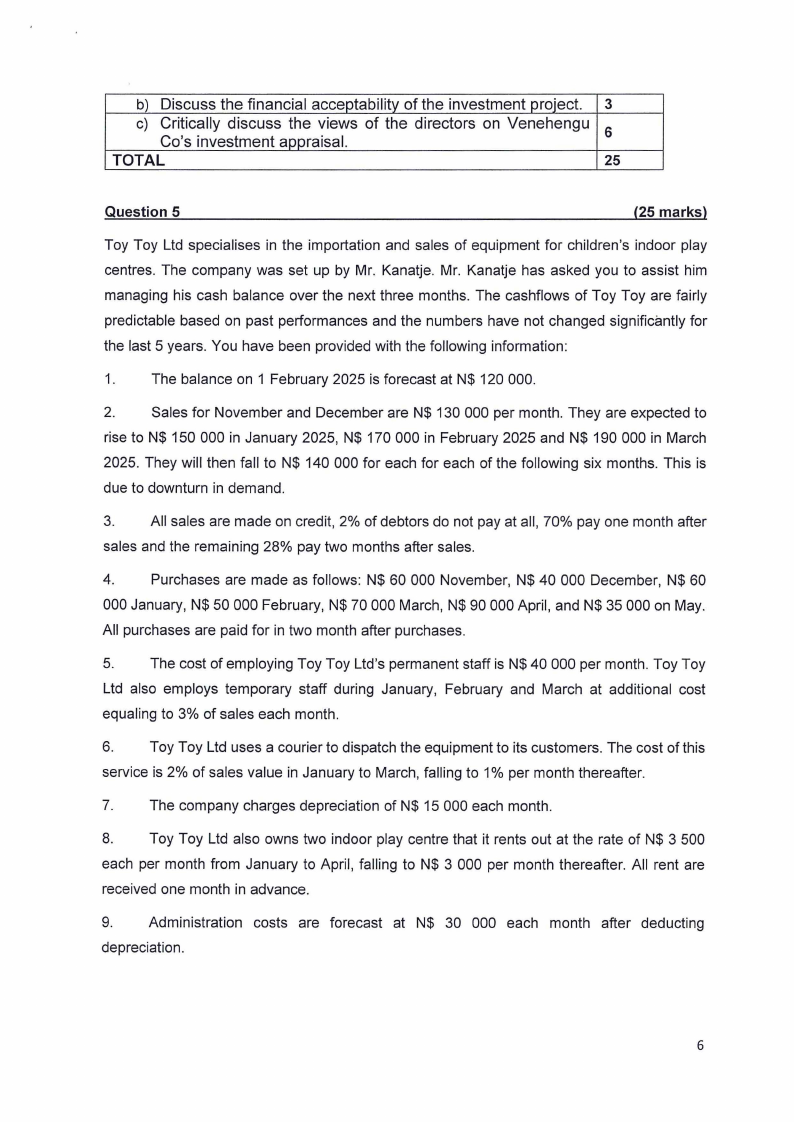

b) Discuss the financial acceptability of the investment project. 3

c) Critically discuss the views of the directors on Venehengu

Co's investment appraisal.

6

TOTAL

25

Question 5

(25 marks)

Toy Toy Ltd specialises in the importation and sales of equipment for children's indoor play

centres. The company was set up by Mr. Kanatje. Mr. Kanatje has asked you to assist him

managing his cash balance over the next three months. The cashflows of Toy Toy are fairly

predictable based on past performances and the numbers have not changed significantly for

the last 5 years. You have been provided with the following information:

1. The balance on 1 February 2025 is forecast at N$ 120 000.

2. Sales for November and December are N$ 130 000 per month. They are expected to

rise to N$ 150 000 in January 2025, N$ 170 000 in February 2025 and N$ 190 000 in March

2025. They will then fall to N$ 140 000 for each for each of the following six months. This is

due to downturn in demand.

3. All sales are made on credit, 2% of debtors do not pay at all, 70% pay one month after

sales and the remaining 28% pay two months after sales.

4.

Purchases are made as follows: N$ 60 000 November, N$ 40 000 December, N$ 60

000 January, N$ 50 000 February, N$ 70 000 March, N$ 90 000 April, and N$ 35 000 on May.

All purchases are paid for in two month after purchases.

5. The cost of employing Toy Toy Ltd's permanent staff is N$ 40 000 per month. Toy Toy

Ltd also employs temporary staff during January, February and March at additional cost

equaling to 3% of sales each month.

6. Toy Toy Ltd uses a courier to dispatch the equipment to its customers. The cost of this

service is 2% of sales value in January to March, falling to 1% per month thereafter.

7. The company charges depreciation of N$ 15 000 each month.

8. Toy Toy Ltd also owns two indoor play centre that it rents out at the rate of N$ 3 500

each per month from January to April, falling to N$ 3 000 per month thereafter. All rent are

received one month in advance.

9. Administration costs are forecast at N$ 30 000 each month after deducting

depreciation.

6

|

|

7 Page 7 |

▲back to top |

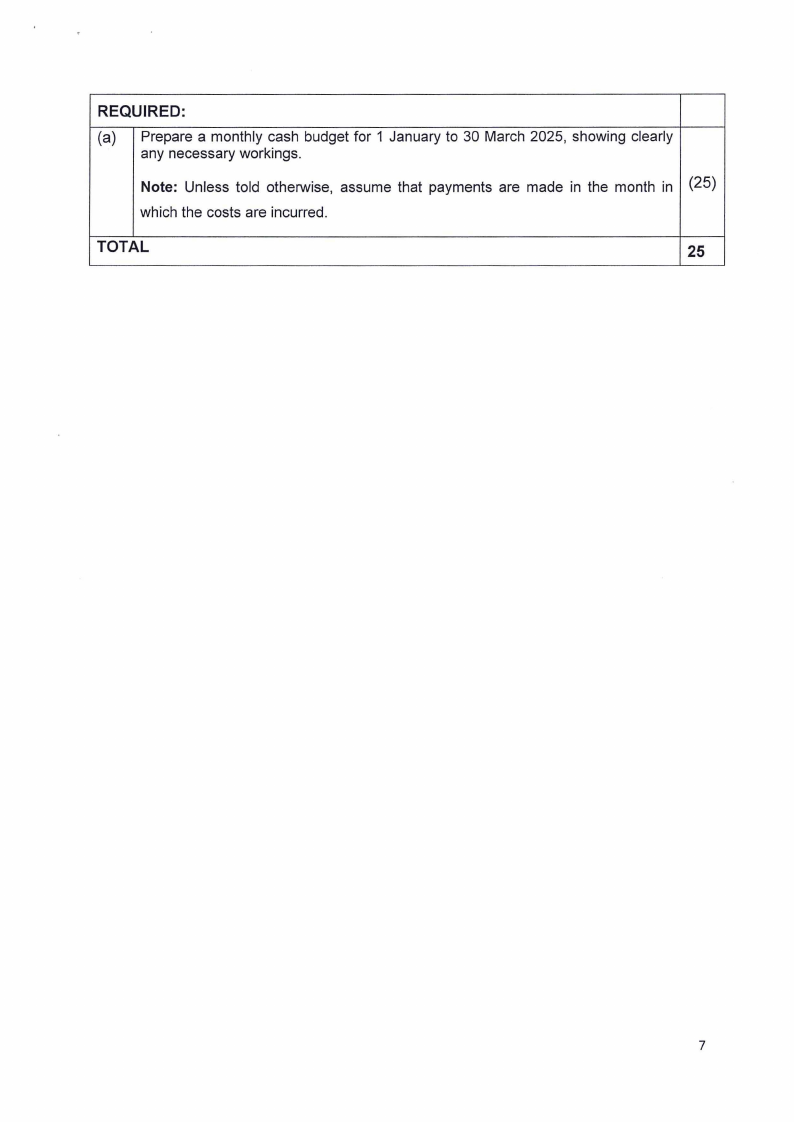

REQUIRED:

(a) Prepare a monthly cash budget for 1 January to 30 March 2025, showing clearly

any necessary workings.

Note: Unless told otherwise, assume that payments are made in the month in (25)

which the costs are incurred.

TOTAL

25

7

|

|

8 Page 8 |

▲back to top |

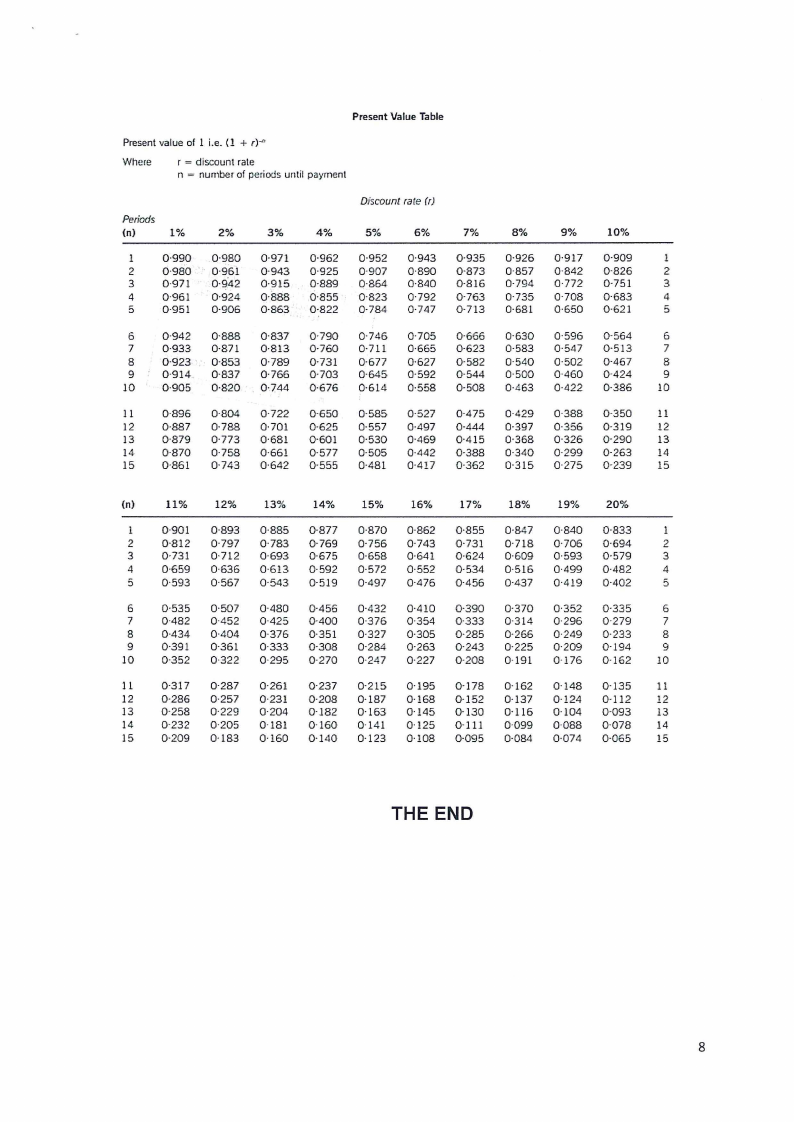

Present Value Table

Present value of l i.e. (l + r)·"

Where

r = discount rate

n = number of periCYJsuntil pa~menl

Discount rate (r)

Periods

(n)

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

1

0·990 0·980 0·971 0·962 0·952 0·943 0·935 0·926 0·917 0·909

l

2

0·980 0·961 0·943 0-925 0-907 0·890 0·873 0·857 0·842 0·826

2

3

0·971 0·942 0·915 0-889 0·864 0·840 0·816 0·794 0·772 0-751

3

4

0-961 0·924 0·888 0·855 0-823 0·792 0·763 0·735 0 708 0·683

4

5

0·951 0-906 0·863 0-822 0-784 0·747 0·713 0·681 0·650 0-621

5

6

0·942 0-888 0·837 0·790 0·746 0·705 0·666 0-630 0·596 0·564

6

7

0·933 0·871 0·8!3 0-760 0·711 0·665 0-623 0·583 0·547 0-513

7

8

0-923 0-853 0·789 0-731 0-677 0·627 0·582 0-540 0·502 0·467

8

9

0-914 0-837 0·766 0-703 0·645 0·592 0-544 0-500 0-460 0-424

9

10

0·905 0·820 0·744 0·676 0·614 0·558 0·508 0·463 0·422 0·386

10

11

0·896 0·804 0·722 0-650 0-585 0·527 0-475 0·429 0·388 0·350

11

12 0-887 0·788 0·701 0·625 0·557 0·497 0·444 0-397 0·356 0-319

12

13 0·879 0·773 0·681 0·601 0·530 0-469 0·415 0·368 0·326 0·290

13

14

0·870 0·758 0·661 0·577 0-505 0·442 0·388 0·340 0·299 0·263

14

15

0-861 0·743 0·642 0-555 0·4-81 0·417 0-362 0·315 0·275 0·239

15

(n)

11%

12%

13%

14%

15%

16%

17%

18%

19%

20%

1 0·901 0·893 0·885 0-877 0·870 0·862 0·855 0-847 0·840 0-833

1

2

0·812 0·797 0·783 0·769 0·756 0·743 0·731 0·718 0·706 0·694

2

3

0-731 0-712 0·693 0·675 0·658 0·641 0-624 0·609 0·593 0·579

3

4

0-659 0·636 0·613 0·592 0-572 0·552 0-534 0·516 0-499 0·482

4

5

0·593 0·567 0·543 0-519 0·497 0-476 0·456 0·437 0-419 0-402

5

6

0·535 0·507 0·480 0·456 0·432 0·410 0·390 0·370 0·352 0·335

6

7

0·482 0·452 0·425 0-400 0·376 0·354 0·333 0-314 0·296 0-279

7

8

0-434 0·404 0·376 0·351 0·327 0·305 0·285 0·266 0·249 0·233

8

9

0-391 0-361 0·333 0·308 0·284 0·263 0·243 0·225 0·209 0·194

9

10

0-352 0·322 0·295 0·270 0·247 0·227 0·208 0·191 0·176 0·162

10

11

0-317 0·287 0·261 0·237 0·215 0·195 0·178 0·162 0·148 0-135

11

12

0-286 0·257 0·231 0·208 0·187 0·!68 0·152 0·137 0·124 0-112

12

13

0·258 0·229 0·204 0·182 0·163 0·145 0·130 0·116 0·104 0·093

13

14

0·232 0·205 0·181 0-160 0-141 0·!25 0·111 0·099 0·088 0·078

14

15

0·209 0·183 0·160 0·140 0·123 0·108 0-095 0-084 0·074 0·065

!5

THE END

8