|

BMT620S - BUDGET AND ASSETS MANAGEMENT - 2ND OPP - DECEMBER 2025 |

|

|

1 Page 1 |

▲back to top |

n Am I BI A u n IVER s I TY

OF SCIEnCE Ano TECHnOLOGY

FACULTY OF COMMERCE, HUMAN SCIENCES AND EDUCATION

DEPARTMENT OF TECHNICAL AND VOCATIONAL EDUCATION AND TRAINING

QUALIFICATION : DIPLOMA IN TECHNICAL AND VOCATIONAL EDUCATION AND TRAINING :

MANAGEMENT

QUALIFICATION CODE: 06DTVM

LEVEL: 6

COURSE CODE: BMT620S

COURSE NAME: BUDGET AND ASSET MANAGEMENT

SESSION: DECEMBER 2025

PAPER: PAPER 2

DURATION: 3 HOURS

MARKS: 100

SECOND OPPORTUNITY EXAMINATION PAPER

EXAMINER{S): Mr. Benhardt U Kauteza

MODERATOR: Dr. Godfrey M Tubaundule

INSTRUCTIONS

1. Answer all questions.

2. Read all the questions carefully before answering.

3. This paper consists of Sections A and B with a total of six questions.

4. Make sure your name and surname, question number and the date appear on

the answer script.

5. Number the answers clearly.

6. Please ensure that your writing is legible, neat and presentable

THIS MEMORANDUM CONSISTS OF _6_ PAGES (Including this front page)

|

|

2 Page 2 |

▲back to top |

SECTION A: MULTIPLE CHOICE QUESTIONS

Question 1 - Short Questions

[10]

Question 1 consists of 10 multiple-choice questions. For each question, there are four possible

answers: A, B, C, and D. Choose only the one letter you consider correct. E.g., 1. D.

1.1 In incremental budgeting, the new budget is usually based on:

A. Expected cash inflows

B. Performance indicators only

C. Previous year's budget plus adjustments

D. Zero-balance principles

1.2 Which of the following is an example of a recurrent expenditure?

A. Construction of a new classroom block

B. Salaries and wages of staff members

C. Purchase of laboratory equipment

D. Acquisition of land for expansion

1.3 A deficit budget occurs when:

A. Revenue equals expenditure

B. Expenditure is greater than revenue

C. Expenditure is less than revenue

D. Expenditure is delayed until next year

1.4 Which budget approach links resources directly to institutional goals and objectives?

A. Traditional line-item budgeting

B. Performance-based budgeting

C. Incremental budgeting

D. Cash flow budgeting

2

|

|

3 Page 3 |

▲back to top |

1.5 In budget control, a supplementary budget is prepared when:

A. There is a significant surplus

B. Unexpected needs arise during implementation

C. The institution wants to close accounts

D. The financial year has ended

1.6 Which of the following best describes a rolling budget?

A. A budget prepared once and never updated

B. A budget continuously revised and extended overtime

C. A capital budget that rolls into an operating budget

D. A budget created only for emergencies

1.7 In budget monitoring, variance analysis is important because it:

A. Measures compliance with taxation rules

B. Identifies differences between planned and actual figures

C. Eliminates the need for financial reporting

D. Ensures that only revenues are analysed

1.8 Which financial document summarises the expected income and expenditure of an institution?

A. Ledger account

B. Budget statement

C. Asset register

D. Trial balance

1.9 One key characteristic of a good budget is that it must be:

A. Complicated and lengthy

B. Flexible and realistic

C. Based only on historical data

D. Focused on one department only

3

|

|

4 Page 4 |

▲back to top |

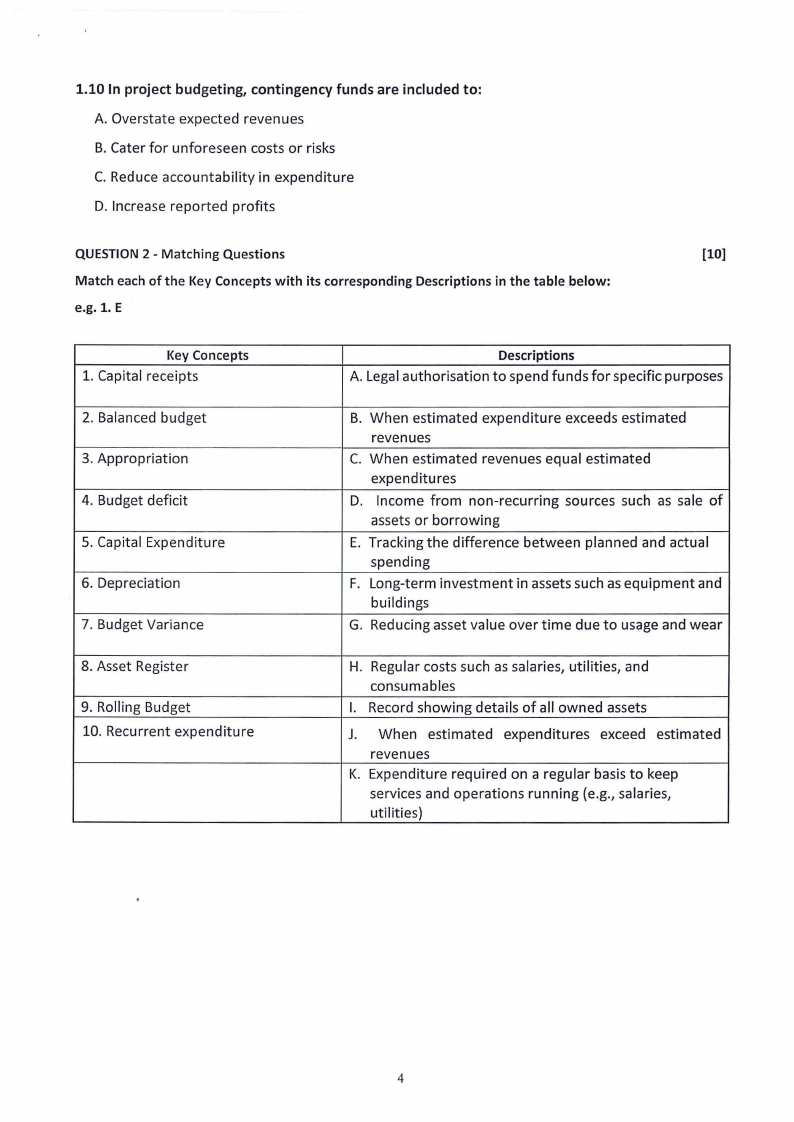

1.10 In project budgeting, contingency funds are included to:

A. Overstate expected revenues

B. Cater fo r unforeseen costs or risks

C. Reduce accountability in expenditure

D. Increase reported profits

QUESTION 2 - Matching Questions

[10]

Match each of the Key Concepts with its corresponding Descriptions in the table below:

e.g. 1. E

Key Concepts

1. Capital receipts

2. Balanced budget

3. Appropriation

4. Budget deficit

5. Capital Expenditure

6. Depreciation

7. Budget Variance

8. Asset Register

9. Rolling Budget

10. Recurrent expenditure

Descriptions

A. Legal authorisation to spend funds for specific purposes

B. When estimated expenditure exceeds estimated

revenues

C. When estimated revenues equal estimated

expenditures

D. Income from non-recurring sources such as sale of

assets or borrowing

E. Tracking the difference between planned and actual

spending

F. Long-term investment in assets such as equipment and

buildings

G. Reducing asset value over time due to usage and wear

H. Regular costs such as salaries, utilities, and

consumables

I. Record showing details of all owned assets

J. When estimated expend itures exceed estimated

revenues

K. Expenditure required on a regular basis to keep

services and operations running (e.g., salaries,

utilities)

4

|

|

5 Page 5 |

▲back to top |

SECTION B: STRUCTURED QUESTIONS

QUESTION 1 - Key Concepts of Budgets and Assets and Types of Budgets

[20]

1.1 Define the term budget and explain its significance in financial management.

(5)

1.2 Briefly explain the term assets and give two examples relevant in a TVET institution.

(4)

1.3 Describe three major types of budgets and provide one example for each.

(9)

1.4 Explain the difference between a budget deficit and a budget surplus of an organisation.

(2)

QUESTION 2 - Budget Evaluation and Budget Preparation [20]

You are a budget officer at a Technical and Vocational Education and Training (TVET} college. The

college plans to expand its training programs in ICT, automotive mechanics, and hospitality. To

support this expansion, you are tasked to:

2.1 Identify and explain any five considerations you would apply when evaluating key data sources

to prepare for a new annual budget.

(10)

2.2 Outline any five steps you would follow to prepare a realistic and comprehensive budget for the

TVET college.

(10)

QUESTION 3 - Negotiating, Managing and Controlling a Budget

[20]

The Namibian Institute of Technical Education (NITE} is preparing its annual budget for the next

academic year. The Finance Officer is tasked to:

1. Negotiate the budget with various department heads who demand more funds for equipment,

staff training, and student support services.

2. Manage and control the approved budget to ensure that expenditures align with TVET goals,

avoid wastage, and maintain accountability.

3.1 Explain the key steps and strategies the Finance Officer should apply when negotiating the

budget with heads of department.

(10)

3.2 Discuss in detail how the Finance Officer can effectively manage and control the approved

budget to ensure financial sustainability within NITE.

(10)

5

|

|

6 Page 6 |

▲back to top |

QUESTION 4 - Budgeting/Asset Management and Financial Performance

[20]

4. CASE STUDY

Read the Case Study below and answer the questions which follow.

Background

The Omuze TVET Centre offers training in Electrical Engineering, Plumbing, and Hospitality. The Centre

has a yearly budget of N$2,000,000, allocated as follows:

• Staff salaries: N$1,200,000

• Training materials: N$300,000

• Equipment and physical assets (tools, machines, furniture): N$250,000

• Maintenance and utilities: N$150,000

• Administrative and miscellaneous expenses: N$100,000

After a mid-year financial review, management realized that equipment in the Electrical Department

was breaking down frequently, causing training delays and reducing enrolments. At the same time,

expenditure on utilities was above projections due to inefficient energy use. To remain sustainable, the

TVET Centre must prepare a more effective budget, manage its physical assets, and implement

measures to improve financial performance.

Answer the following questions:

4.1 Identify two challenges faced by the TVET Centre in terms of physical asset management and

suggest suitable solutions.

(6)

4.2 Prepare a revised budget that reallocates N$50,000 from administrative/miscellaneous expenses

and N$30,000 from training materials to support equipment maintenance and energy efficiency

upgrades. Present the new allocation for each category.

(8)

4.3 Explain two practical measures the TVET Centre can implement to improve financial performance

apart from budget reallocation.

(6)

TOTAL [100 MARKS]

[End of Paper]

6