|

BAC521C-BUSINESS ACCOUNTING 1B-2ND OPP-JULY 2025 |

|

|

1 Page 1 |

▲back to top |

nAmlBIA

UnlVERSITY

OF SCIEnCE

TECHnOLOGY

HAROLDPUPKEWITZ

GraduateSchoolof Business

FACULTY OF COMMERCE, HUMAN SCIENCESAND EDUCATION

HAROLD PUPKEWITZ GRADUATE SCHOOL OF BUSINESS

QUALIFICATION: DIPLOMA IN BUSINESSPROCESSMANAGEMENT

QUALIFICATION CODE: 06DBPM LEVEL: 6

COURSE CODE: BAC521C

COURSE NAME: BUSINESSACCOUNTING lB

SESSION: JUNE 2025

PAPER: PAPER2

DURATION: 3 HOURS

MARKS: 100

SECOND OPPORTUNITY EXAMINATION QUESTION PAPER

EXAMINER

Lameck Odada

MODERATOR Hendrina Kangala

INSTRUCTIONS

1. This question paper comprises FOUR (4) questions.

2. Answer ALL the questions in blue or black ink. NO pencil

3. Start each question on a new page in your answer booklet and show all your workings.

4. Unless otherwise stated, round off only final answers to two (2) decimal places where

necessary.

5. Questions relating to this examination may be raised in the initial 30 minutes after the

start of the paper. Thereafter, candidates must use their initiative to deal with any

perceived error or ambiguity & any assumption made by the candidate should be clearly

stated.

PERMISSIBLE MATERIALS

1. Silent, non-programmable calculators

THIS QUESTION PAPER CONSISTS OF 7 PAGES (including this front page)

|

|

2 Page 2 |

▲back to top |

QUESTION 1

[24 MARKS]

For questions 1-12, just write the answer only (the correct letter chosen) in your answer book and not

on the question paper. Do not copy the question again

1. The following item is NOT a manufacturing overhead cost:

a) Depreciation of plant and equipment

b) Rent of office

c) Indirect labour

d) Indirect material

2. Conversion cost can be defined as:

a) The cost of the first stage of the manufacture of a product

b) The total direct labour and manufacturing overhead costs

c) The total direct costs of manufacturing a product

d) The total costs of manufacturing a product

3. The following statement is NOT true:

a) Total ordering cost= Cost per order x Number of orders

b) Safety inventory= Minimum inventory

c) Economic order quantity= Reorder level

d) Average inventory= Minimum inventory level+½ (Economic order quantity)

4. The following item is NOT an example of direct material cost:

a) Cotton

b) Wood

c) Steel

d) Gel

The following details refer to questions 1.5 - 1.6:

Turtle Ltd supplied the following information for the past year:

Direct material used

Indirect labour costs

Direct labour costs

Indirect material used

Depreciation: plant and equipment

Sundry factory overheads

100 000

50000

200 000

20 000

15 000

10 000

1

|

|

3 Page 3 |

▲back to top |

Depreciation: office building

5 000

5. The prime costs incurred during the year was:

a) N$150 000

b) N$200 000

c) N$250 000

d) N$300 000

6. The total manufacturing/production costs of the past year were:

a) N$295 000

b) N$300 000

c) N$395 000

d) N$400 000

The following details refer to questions 1.8 and 1.9:

A business has bought and sold identical items of inventory during 2024 as follows:

1/6/24

Bought

1000 units

@ N$100 each

1/9/24

Bought

1000 units

@ N$160 each

5/9/24

Sold

1200 units

@ N$200 each

7. What is the value of closing inventory Using the first-in, first-out (FIFO)method?

a) N$128 000

b) N$120 000

c) N$104 000

d) N$100 000

8. Using the weighted average method, what is the value of closing inventory?

a) N$128 000

b) N$120 000

c) N$104 000

d) N$100 000

9. The first-in-first-out(FIFO) method of stock valuation would be most appropriate for:

a) A bicycle components retailer

b) A motor components retailer

c) A construction retailer

d) A food retailer

2

|

|

4 Page 4 |

▲back to top |

10. A firm produced 5 000 units during the past month and incurred the following costs:

Fixed cost N$8 250; Variable cost N$12 500. The total cost budgeted for the following month for

3 500 units will be:

a) N$18 000

b) N$17 000

c) N$14 000

d) N$19 000

11. Under-absorbed overheads occur when:

a) The amount of actual overheads incurred is less than the overheads that have been

charged to production

b) Actual overheads have fallen in relation to what they were expected to be

c) budgeted overheads are less than the actual overheads incurred.

d) The overheads charged to production are lower than the actual overheads incurred.

12. An employee is paid N$30 per hour and normally works eight hours daily from Monday

to Friday. During a certain week, he also worked four (4) hours on Saturday, for which he was

remunerated at time-and-a-half. On Sunday, he worked for five (5) hours at a double rate. His/her

gross wage for the week amounted to?

a) N$1800

b) N$1180

c) N$1680

d) N$1690

1 X 2 marks each = 24 marks

3

|

|

5 Page 5 |

▲back to top |

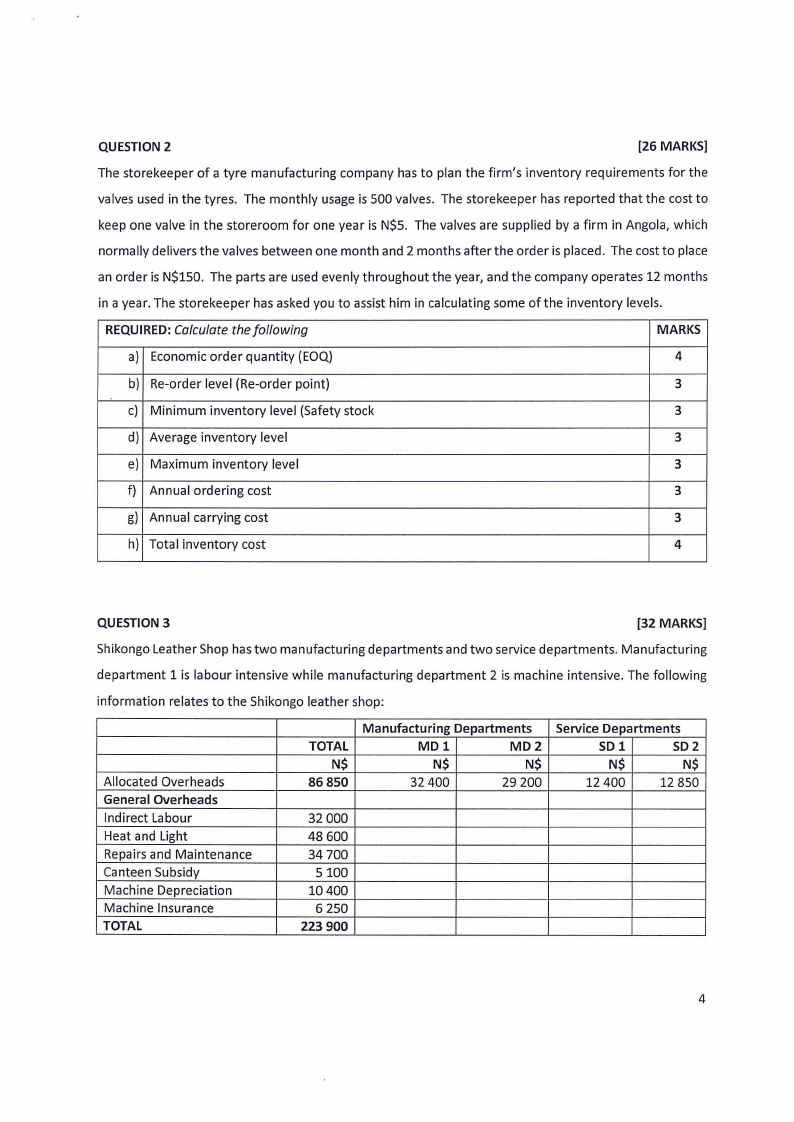

QUESTION 2

[26 MARKS]

The storekeeper of a tyre manufacturing company has to plan the firm's inventory requirements for the

valves used in the tyres. The monthly usage is 500 valves. The storekeeper has reported that the cost to

keep one valve in the storeroom for one year is N$5. The valves are supplied by a firm in Angola, which

normally delivers the valves between one month and 2 months after the order is placed. The cost to place

an order is N$150. The parts are used evenly throughout the year, and the company operates 12 months

in a year. The storekeeper has asked you to assist him in calculating some ofthe inventory levels.

REQUIRED: Calculate the following

MARKS

a) Economic order quantity (EOQ)

4

b) Re-order level (Re-order point)

3

c) Minimum inventory level (Safety stock

3

d) Average inventory level

3

e) Maximum inventory level

3

f) Annual ordering cost

3

g) Annual carrying cost

3

h) Total inventory cost

4

QUESTION 3

[32 MARKS]

Shikongo Leather Shop has two manufacturing departments and two service departments. Manufacturing

department 1 is labour intensive while manufacturing department 2 is machine intensive. The following

information relates to the Shikongo leather shop:

Allocated Overheads

General Overheads

Indirect Labour

Heat and Light

Repairs and Maintenance

Canteen Subsidy

Machine Depreciation

Machine Insurance

TOTAL

TOTAL

N$

86 850

Manufacturing Departments

MDl

MD2

N$

N$

32 400

29 200

Service Departments

SD 1

SD 2

N$

N$

12 400

12 850

32 000

48 600

34 700

5100

10400

6 250

223 900

4

|

|

6 Page 6 |

▲back to top |

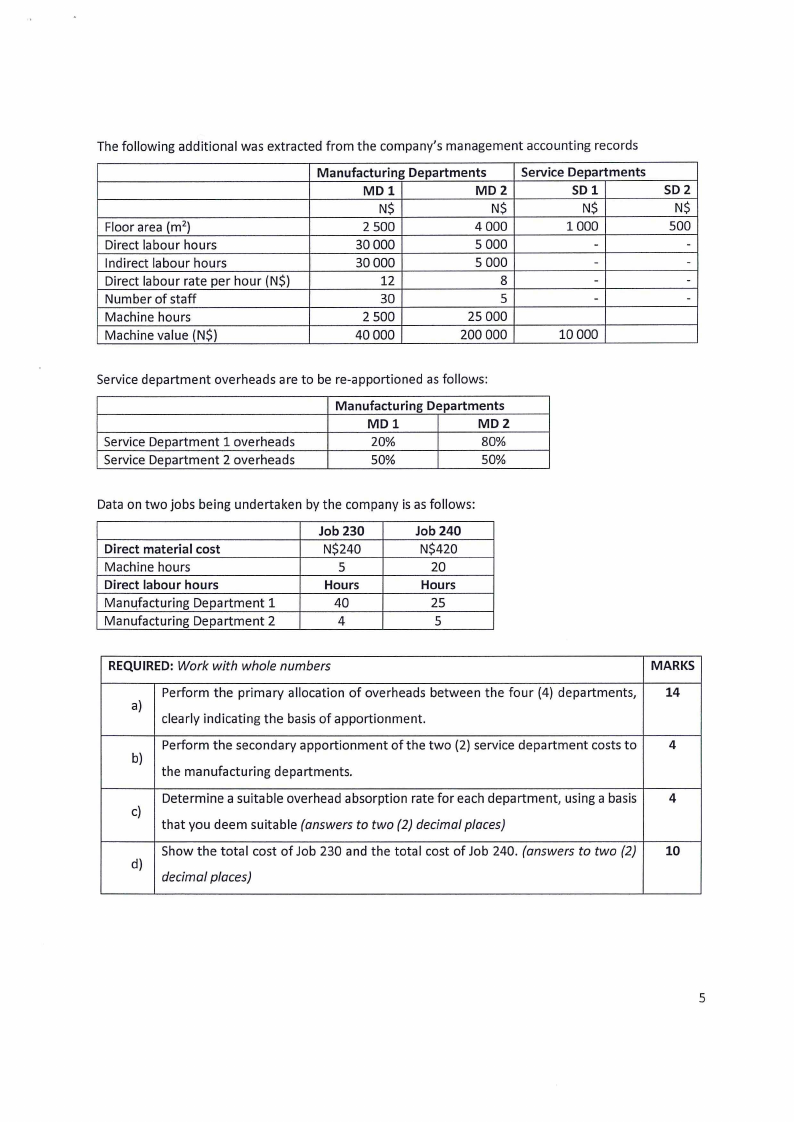

The following additional was extracted from the company's management accounting records

Floor area (m2)

Direct labour hours

Indirect labour hours

Direct labour rate per hour (N$)

Number of staff

Machine hours

Machine value (N$)

Manufacturing Departments

MDl

MD2

N$

N$

2 500

4000

30000

5 000

30000

5 000

12

8

30

5

2 500

25 000

40000

200 000

Service Departments

SD 1

N$

1000

-

-

-

-

10000

SD 2

N$

500

-

-

-

-

Service department overheads are to be re-apportioned as follows:

Service Department 1 overheads

Service Department 2 overheads

Manufacturing Departments

MDl

MD2

20%

80%

50%

50%

Data on two jobs being undertaken by the company is as follows:

Direct material cost

Machine hours

Direct labour hours

Manu_facturing Department 1

Manufacturing Department 2

Job 230

N$240

5

Hours

40

4

Job 240

N$420

20

Hours

25

5

REQUIRED:Work with whole numbers

MARKS

Perform the primary allocation of overheads between the four (4) departments,

14

a)

clearly indicating the basis of apportionment.

Perform the secondary apportionment of the two (2) service department costs to

4

b)

the manufacturing departments.

Determine a suitable overhead absorption rate for each department, using a basis 4

c)

that you deem suitable (answers to two (2) decimal places)

Show the total cost of Job 230 and the total cost of Job 240. (answers to two (2) 10

d)

decimal places)

5

|

|

7 Page 7 |

▲back to top |

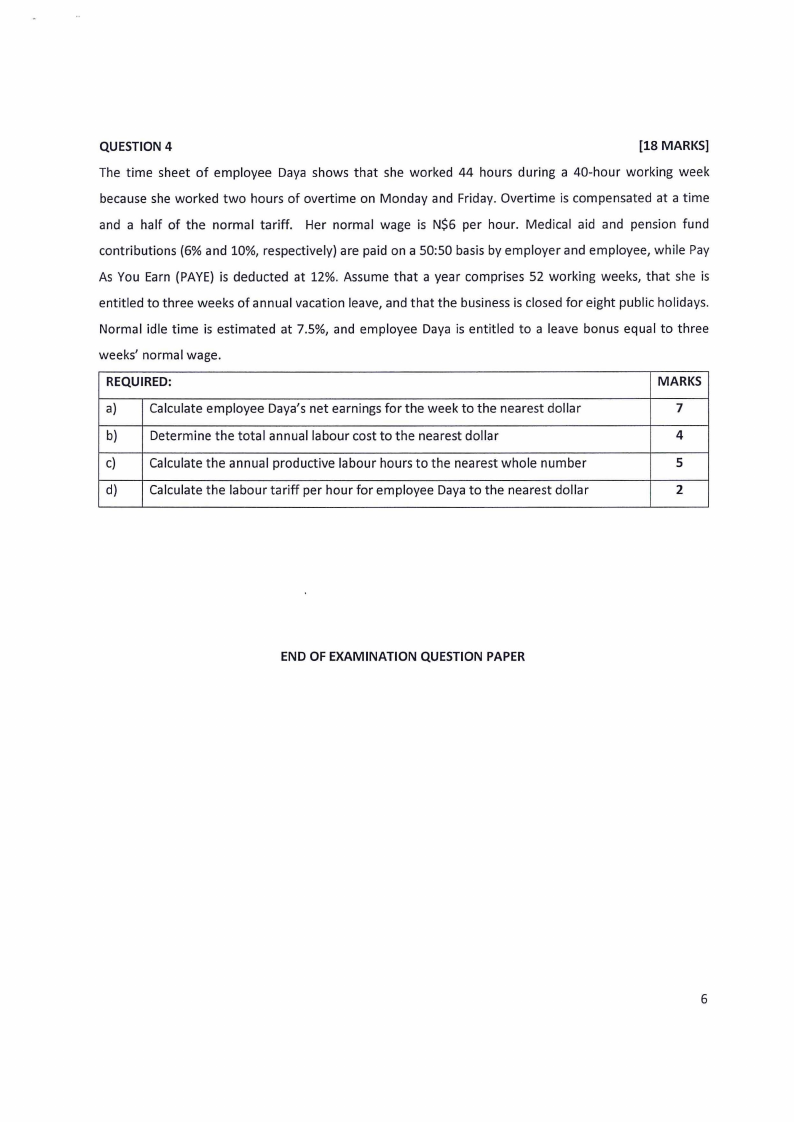

QUESTION 4

[18 MARKS]

The time sheet of employee Daya shows that she worked 44 hours during a 40-hour working week

because she worked two hours of overtime on Monday and Friday. Overtime is compensated at a time

and a half of the normal tariff. Her normal wage is N$6 per hour. Medical aid and pension fund

contributions (6% and 10%, respectively) are paid on a 50:50 basis by employer and employee, while Pay

As You Earn (PAYE) is deducted at 12%. Assume that a year comprises 52 working weeks, that she is

entitled to three weeks of annual vacation leave, and that the business is closed for eight public holidays.

Normal idle time is estimated at 7.5%, and employee Daya is entitled to a leave bonus equal to three

weeks' normal wage.

REQUIRED:

MARKS

a)

Calculate employee Daya's net earnings for the week to the nearest dollar

7

b)

Determine the total annual labour cost to the nearest dollar

4

c)

Calculate the annual productive labour hours to the nearest whole number

5

d)

Calculate the labour tariff per hour for employee Daya to the nearest dollar

2

END OF EXAMINATION QUESTION PAPER

6