|

CAC710S-COMPUTERISED ACCOUNTING 301-2ND OPP-JULY 2025 |

|

|

1 Page 1 |

▲back to top |

n Am I BI A u n IVER s I TY

OF SCIEn CE Ano TECHn OLOGY

FACULTY OF COMMERCE, HUMAN SCIENCEAND EDUCATION

DEPARTMENT OF ECONOMICS, ACCOUNTING & FINANCE

QUALIFICATION: BACHELOR OF ACCOUNTING/BACHELOR OF ACCOUNTING (CA)

QUALIFICATION CODE: 07BGAC/07BACC

COURSE CODE: CAC710S

LEVEL: 7

COURSE NAME: COMPUTERISED

ACCOUNTING 301

SESSION: JULY 2025

PAPER: PRACTICAL

DURATION: 3 HOURS (Including printing and set

up)

MARKS: 100

SECOND OPPORTUNITY EXAMINATION QUESTION PAPER

EXAMINERS:

H Namwandi, Y Elago, C Mahindi and A Peter

MODERATOR: E Milijala

INSTRUCTIONS

• This question paper comprises one (1) question, split into three parts.

• Ensure your student number appears on all reports (Generated through the system,

not handwritten).

• It's your responsibility to ensure that all reports are printed and submitted.

• Ensure that all work done during the assessment is your own.

• The use of the internet on any electronic device is prohibited during the assessment.

• Questions relating to this paper may be raised in the initial 30 minutes after the start

of the paper. Thereafter, candidates must use their initiative to deal with any

perceived error or ambiguities and any assumption made by the candidate should be

clearly stated.

PERMISSIBLE MATERIALS

Non-programmable calculator

THIS QUESTION PAPER CONSISTS OF 7 PAGES (Including this front page)

1

|

|

2 Page 2 |

▲back to top |

QUESTION 1

100 Marks

Part A

You are required to create a company on the "C" drive, using the following information.

Company Name:

Financial Year:

Date Format:

Processing Method:

Bankers:

Printing:

Supplier Processing:

Student Number

1st January 2024

01/01/2024

Balance Forward

Bank Windhoek

Plain Paper

No GRN and Purchase Orders

Background of the organisation.

You are provided information by the manager of Nakavolelwa Construction Pty Ltd.

Nakavolelwa Construction Pty Ltd was established by John and Joseph a few years back. The

organisation is constructing and selling modern townhouses in Ohangwena, Oshana and

Kavango East regions. The company's bookkeeper didn't have enough experience recording

transactions in Pastel V50, which was recently bought. Hence, she asked you to assist in

recording the transaction. Nakavolelwa Construction Pty Ltd is registered for tax purposes

(VAT Number: 6547363-01-6). You are supplied with a list of company account balances to

help the manager prepare reports.

You are provided with the following list of account balances for Nakavolelwa Pty Ltd, as at 1

January 2024.

Property, Plant and Equipment

Accounts receivable

Accounts payable

Inventory

Share capital

Cash and cash equivalents

Operating expenses already paid

Allowance for credit losses

VAT receivables

Company tax payables

Shareholders for dividends

Prior year's profits

Note

1

2

3

4

5

6

N$

3811900

926 800

942 200

648 145

2 812 250

91 999

9460

29 500

11 430

20 230

37 670

32 400

Supporting information relating to notes on opening balances:

Note 1: Property, Plant and Equipment's

N$

Non-current assets (See fixed assets register on page 3)

Office and warehouse building

1 311 400

2 500 500

3 811 900

2

|

|

3 Page 3 |

▲back to top |

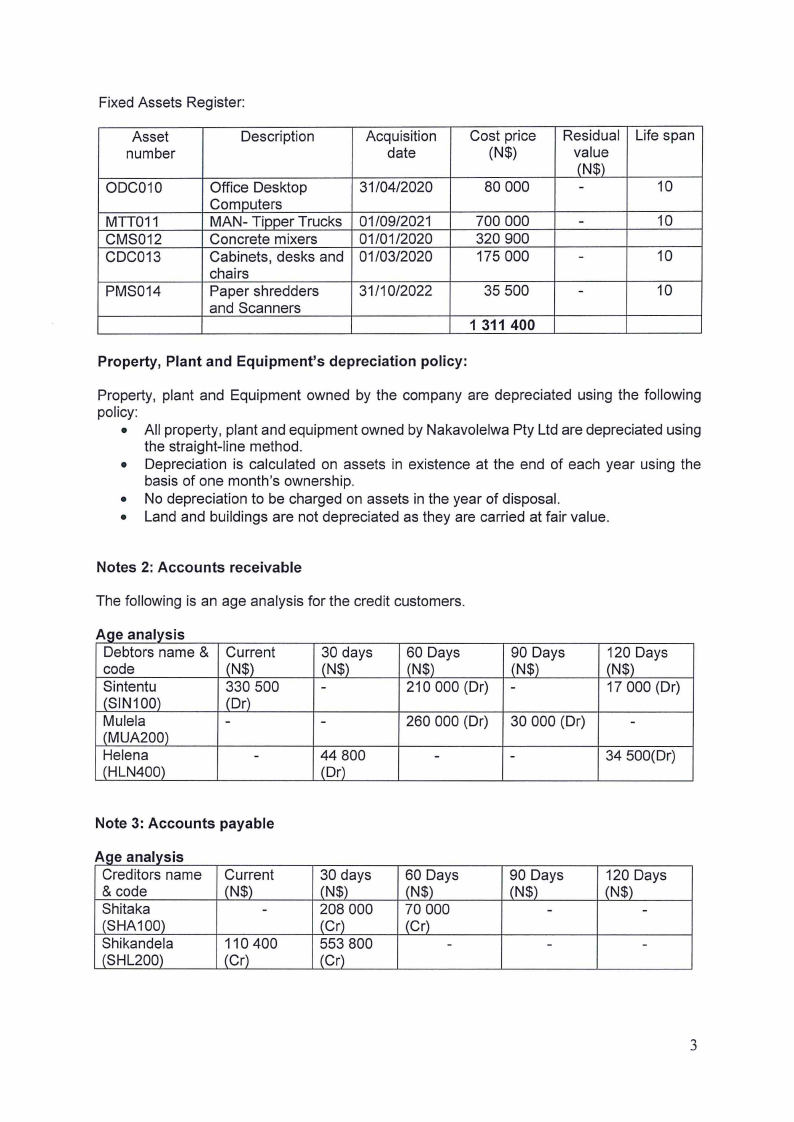

Fixed Assets Register:

Asset

number

ODC010

MTT011

CMS012

CDC013

PMS014

Description

Acquisition

date

Office Desktop

Computers

MAN- Tipper Trucks

Concrete mixers

Cabinets, desks and

chairs

Paper shredders

and Scanners

31/04/2020

01/09/2021

01/01/2020

01/03/2020

31/10/2022

Cost price

(N$)

80 000

700 000

320 900

175 000

35 500

1 311 400

Residual

value

(N$)

-

Life span

10

-

10

-

10

-

10

Property, Plant and Equipment's depreciation policy:

Property, plant and Equipment owned by the company are depreciated using the following

policy:

• All property, plant and equipment owned by Nakavolelwa Pty Ltd are depreciated using

the straight-line method.

• Depreciation is calculated on assets in existence at the end of each year using the

basis of one month's ownership.

• No depreciation to be charged on assets in the year of disposal.

• Land and buildings are not depreciated as they are carried at fair value.

Notes 2: Accounts receivable

The following is an age analysis for the credit customers.

A,ge anaIIys1.s

Debtors name &

code

Sintentu

(SIN100)

Mulela

(MUA200)

Helena

(HLN400)

Current

(N$)

330 500

(Dr)

-

-

30 days

(N$)

-

-

44 800

(Dr)

60 Days

(N$)

210 000 (Dr)

90 Days

(N$)

-

120 Days

(N$)

17 000 (Dr)

260 000 (Dr) 30 000 (Dr)

-

-

-

34 500(Dr)

Note 3: Accounts payable

Creditors name

& code

Shitaka

SHA100

Shikandela

SHL200

Current

N$

110 400

Cr

30 days

N$

60 Days

N$

Cr

90 Days

N$

120 Days

N$

3

|

|

4 Page 4 |

▲back to top |

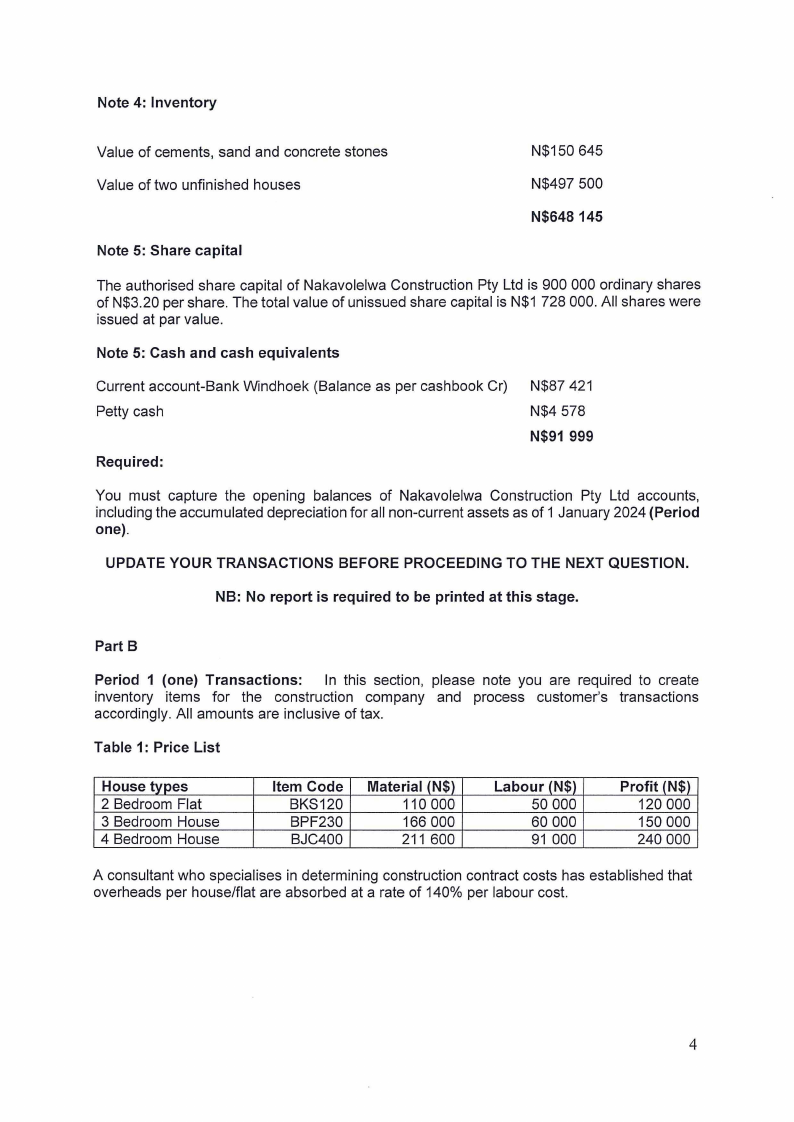

Note 4: Inventory

Value of cements, sand and concrete stones

N$150 645

Value of two unfinished houses

N$497 500

N$648 145

Note 5: Share capital

The authorised share capital of Nakavolelwa Construction Pty Ltd is 900 000 ordinary shares

of N$3.20 per share. The total value of unissued share capital is N$1 728 000. All shares were

issued at par value.

Note 5: Cash and cash equivalents

Current account-Bank Windhoek (Balance as per cashbook Cr)

Petty cash

Required:

N$87 421

N$4 578

N$91 999

You must capture the opening balances of Nakavolelwa Construction Pty Ltd accounts,

including the accumulated depreciation for all non-current assets as of 1 January 2024 (Period

one).

UPDATE YOUR TRANSACTIONS BEFORE PROCEEDING TO THE NEXT QUESTION.

NB: No report is required to be printed at this stage.

Part B

Period 1 (one) Transactions: In this section, please note you are required to create

inventory items for the construction company and process customer's transactions

accordingly. All amounts are inclusive of tax.

Table 1: Price List

House types

2 Bedroom Flat

3 Bedroom House

4 Bedroom House

Item Code

BKS120

BPF230

BJC400

Material (N$)

110 000

166 000

211 600

Labour (N$)

50 000

60 000

91 000

Profit (N$)

120 000

150 000

240 000

A consultant who specialises in determining construction contract costs has established that

overheads per house/flat are absorbed at a rate of 140% per labour cost.

4

|

|

5 Page 5 |

▲back to top |

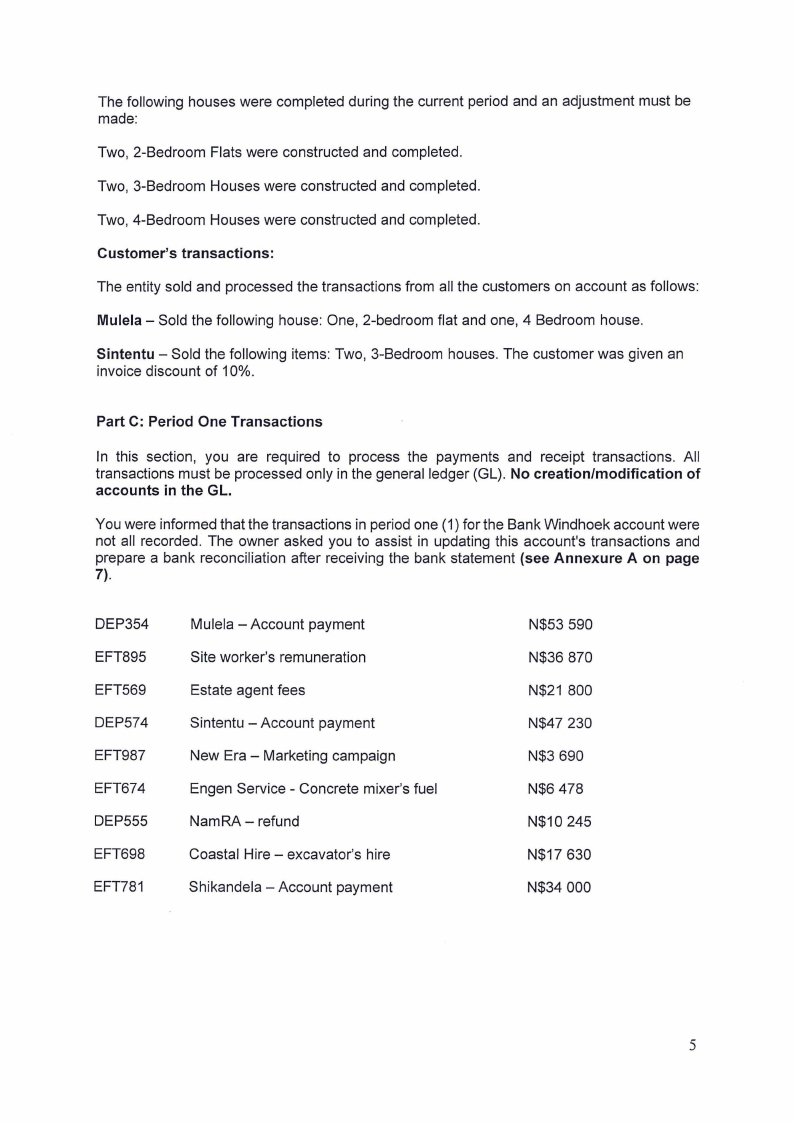

The following houses were completed during the current period and an adjustment must be

made:

Two, 2-Bedroom Flats were constructed and completed.

Two, 3-Bedroom Houses were constructed and completed.

Two, 4-Bedroom Houses were constructed and completed.

Customer's transactions:

The entity sold and processed the transactions from all the customers on account as follows:

Mulela - Sold the following house: One, 2-bedroom flat and one, 4 Bedroom house.

Sintentu - Sold the following items: Two, 3-Bedroom houses. The customer was given an

invoice discount of 10%.

Part C: Period One Transactions

In this section, you are required to process the payments and receipt transactions. All

transactions must be processed only in the general ledger (GL). No creation/modification of

accounts in the GL.

You were informed that the transactions in period one (1) for the Bank Windhoek account were

not all recorded. The owner asked you to assist in updating this account's transactions and

prepare a bank reconciliation after receiving the bank statement (see Annexure A on page

7).

DEP354

EFT895

EFT569

DEP574

EFT987

EFT674

DEP555

EFT698

EFT781

Mulela -Account payment

Site worker's remuneration

Estate agent fees

Sintentu - Account payment

New Era - Marketing campaign

Engen Service - Concrete mixer's fuel

Nam RA - refund

Coastal Hire - excavator's hire

Shikandela - Account payment

N$53 590

N$36 870

N$21 800

N$47 230

N$3 690

N$6 478

N$10 245

N$17 630

N$34 000

5

|

|

6 Page 6 |

▲back to top |

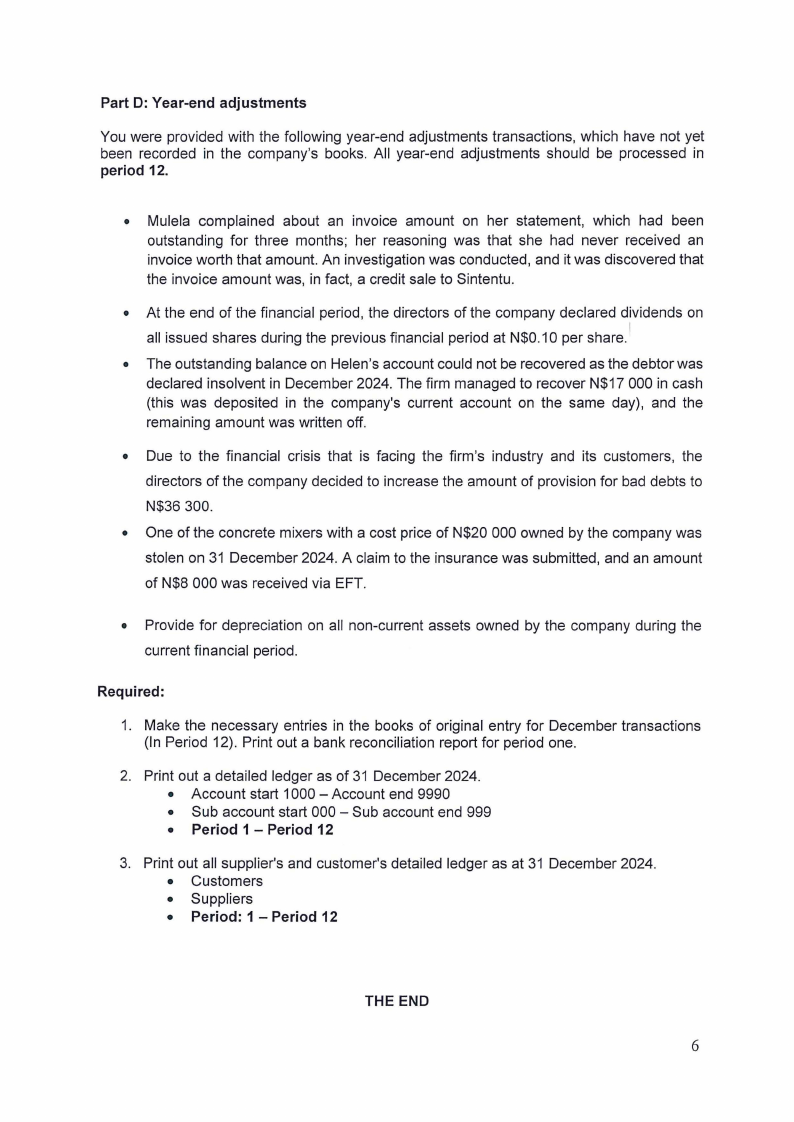

Part D: Year-end adjustments

You were provided with the following year-end adjustments transactions, which have not yet

been recorded in the company's books. All year-end adjustments should be processed in

period 12.

• Mulela complained about an invoice amount on her statement, which had been

outstanding for three months; her reasoning was that she had never received an

invoice worth that amount. An investigation was conducted, and it was discovered that

the invoice amount was, in fact, a credit sale to Sintentu.

• At the end of the financial period, the directors of the company declared dividends on

all issued shares during the previous financial period at N$0.10 per share. I

• The outstanding balance on Helen's account could not be recovered as the debtor was

declared insolvent in December 2024. The firm managed to recover N$17 000 in cash

(this was deposited in the company's current account on the same day), and the

remaining amount was written off.

• Due to the financial crisis that is facing the firm's industry and its customers, the

directors of the company decided to increase the amount of provision for bad debts to

N$36 300.

• One of the concrete mixers with a cost price of N$20 000 owned by the company was

stolen on 31 December 2024. A claim to the insurance was submitted, and an amount

of N$8 000 was received via EFT.

• Provide for depreciation on all non-current assets owned by the company during the

current financial period.

Required:

1. Make the necessary entries in the books of original entry for December transactions

(In Period 12). Print out a bank reconciliation report for period one.

2. Print out a detailed ledger as of 31 December 2024.

• Account start 1000 - Account end 9990

• Sub account start 000 - Sub account end 999

• Period 1 - Period 12

3. Print out all supplier's and customer's detailed ledger as at 31 December 2024.

• Customers

• Suppliers

• Period: 1 - Period 12

THE END

6

|

|

7 Page 7 |

▲back to top |

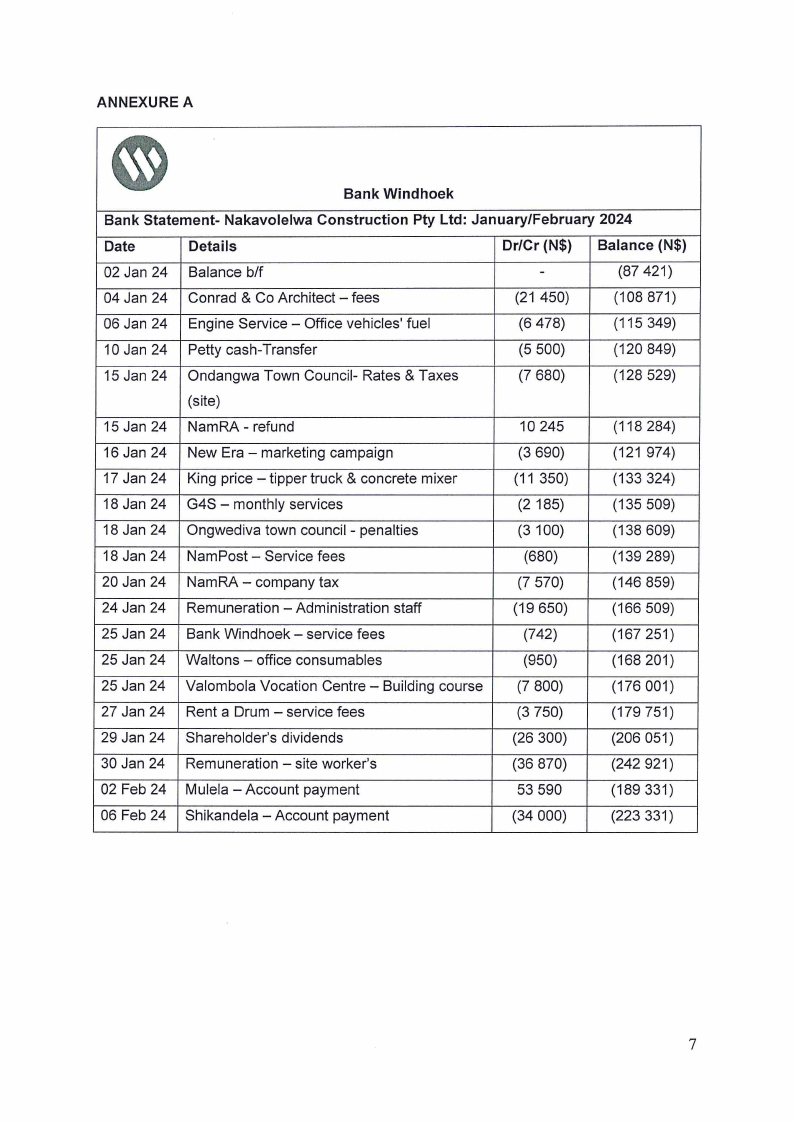

ANNEXURE A

\\\\-)t

Bank Windhoek

Bank Statement- Nakavolelwa Construction Pty Ltd: January/February 2024

Date

Details

Dr/Cr (N$) Balance (N$)

02 Jan 24 Balance b/f

-

(87 421)

04 Jan 24 Conrad & Co Architect - fees

(21 450)

(108871)

06 Jan 24 Engine Service - Office vehicles' fuel

(6 478)

(115 349)

10 Jan 24 Petty cash-Transfer

(5 500)

(120 849)

15 Jan 24 Ondangwa Town Council- Rates & Taxes

(7 680)

(128 529)

(site)

15 Jan 24 NamRA - refund

10 245

(118 284)

16 Jan 24 New Era - marketing campaign

(3 690)

(121 974)

17 Jan 24 King price - tipper truck & concrete mixer

(11 350)

(133 324)

18 Jan 24 G4S - monthly services

(2 185)

(135 509)

18 Jan 24 Ongwediva town council - penalties

(3 100)

(138 609)

18 Jan 24 Nam Post - Service fees

(680)

(139 289)

20 Jan 24 NamRA - company tax

(7 570)

(146 859)

24 Jan 24 Remuneration - Administration staff

(19 650)

(166 509)

25 Jan 24 Bank Windhoek - service fees

(742)

(167 251)

25 Jan 24 Waltons - office consumables

(950)

(168 201)

25 Jan 24 Valombola Vocation Centre - Building course

(7 800)

(176 001)

27 Jan 24 Rent a Drum - service fees

(3 750)

(179751)

29 Jan 24 Shareholder's dividends

(26 300)

(206 051)

30 Jan 24 Remuneration - site worker's

(36 870)

(242 921)

02 Feb 24 Mulela -Account payment

53 590

(189 331)

06 Feb 24 Shikandela - Account payment

(34 000)

(223 331)

7