|

GFA711S- FINANCIAL ACCOUNTING 310- 1ST OPP- JUNE 2025 |

|

|

1 Page 1 |

▲back to top |

nAmlBIA unlVERSITY

OF SCIEnCE Ano TECHnOLOGY

FACULTY OF COMMERCE, HUMAN SCIENCES AND EDUCATION

DEPARTMENT OF ACCOUNTING, ECONOMICS AND FINANCE

QUALIFICATION: BACHELOR OF ACCOUNTING

QUALIFICATION CODE: 07 BOAC LEVEL: 7

COURSE CODE: GFA711S

COURSE NAME: FINANCIAL ACCOUNTING 310

DATE: June 2025

DURATION: 3 HOURS

PAPER:THEORYAND CALCULATIONS

MARKS: 100

FIRST OPPORTUNITY EXAM

EXAMINER{S) Dr. S. Dzomira; Dr. M. Nyakuwanika; Ms. A. Peter

MODERATOR: Mr Marko Tondotsa

INSTRUCTIONS

1. Capture your full name, student number and assessment number on the first page

2. Answer ALL the questions and manage your time properly.

3. Number each page correctly

4. Write clearly and neatly.

5. Do not write in pencil and do not use tip-ex, as this will not be marked.

6. The names of people and businesses used throughout this assessment do not reflect

the reality and may be purely coincidental.

7. SHOWALLWORKINGS!

THIS QUESTION PAPER CONSISTS OF 4 PAGES (excluding this front page)

Page 1 of 5

|

|

2 Page 2 |

▲back to top |

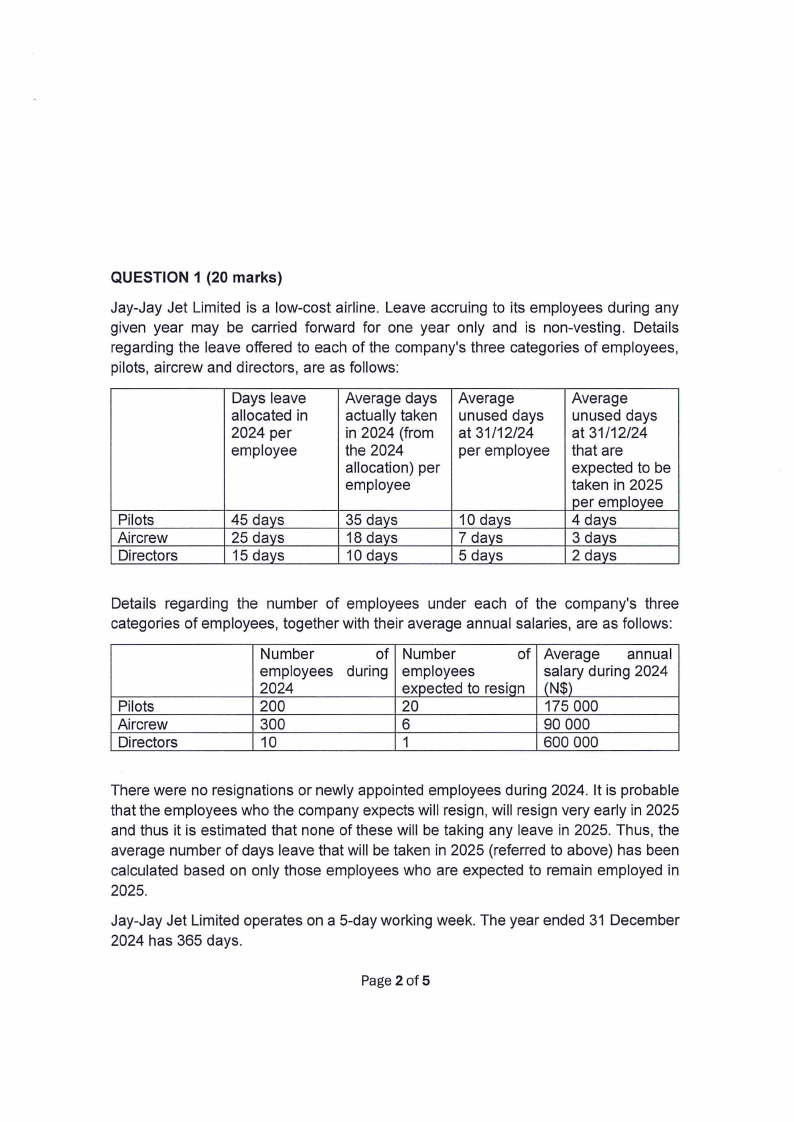

QUESTION 1 (20 marks)

Jay-Jay Jet Limited is a low-cost airline. Leave accruing to its employees during any

given year may be carried forward for one year only and is non-vesting. Details

regarding the leave offered to each of the company's three categories of employees,

pilots, aircrew and directors, are as follows:

Pilots

Aircrew

Directors

Days leave

allocated in

2024 per

employee

45 days

25 days

15 days

Average days

actually taken

in 2024 (from

the 2024

allocation) per

employee

Average

unused days

at 31/12/24

per employee

35 days

18 days

10 days

10 days

7 days

5 days

Average

unused days

at 31/12/24

that are

expected to be

taken in 2025

per employee

4 days

3 days

2 days

Details regarding the number of employees under each of the company's three

categories of employees, together with their average annual salaries, are as follows:

Pilots

Aircrew

Directors

Number

employees

2024

200

300

10

of

during

Number

of

employees

expected to resiqn

20

6

1

Average annual

salary during 2024

(N$)

175 000

90 000

600 000

There were no resignations or newly appointed employees during 2024. It is probable

that the employees who the company expects will resign, will resign very early in 2025

and thus it is estimated that none of these will be taking any leave in 2025. Thus, the

average number of days leave that will be taken in 2025 (referred to above) has been

calculated based on only those employees who are expected to remain employed in

2025.

Jay-Jay Jet Limited operates on a 5-day working week. The year ended 31 December

2024 has 365 days.

Page 2 of 5

|

|

3 Page 3 |

▲back to top |

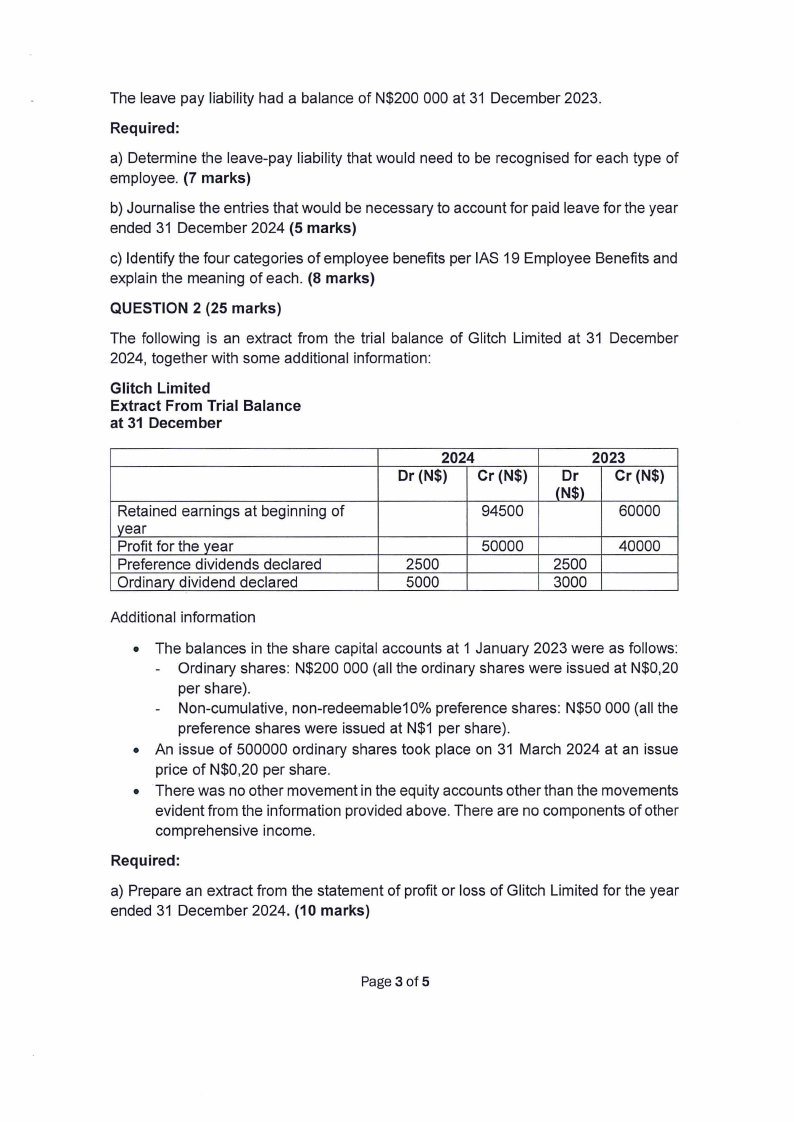

The leave pay liability had a balance of N$200 000 at 31 December 2023.

Required:

a) Determine the leave-pay liability that would need to be recognised for each type of

employee. (7 marks)

b) Journalise the entries that would be necessary to account for paid leave for the year

ended 31 December 2024 (5 marks)

c) Identify the four categories of employee benefits per IAS 19 Employee Benefits and

explain the meaning of each. (8 marks)

QUESTION 2 (25 marks)

The following is an extract from the trial balance of Glitch Limited at 31 December

2024, together with some additional information:

Glitch Limited

Extract From Trial Balance

at 31 December

Retained earnings at beginning of

year

Profit for the year

Preference dividends declared

Ordinary dividend declared

2024

Dr (N$) Cr (N$)

94500

2500

5000

50000

2023

Dr

Cr (N$)

(N$)

60000

2500

3000

40000

Additional information

• The balances in the share capital accounts at 1 January 2023 were as follows:

- Ordinary shares: N$200 000 (all the ordinary shares were issued at N$0,20

per share).

- Non-cumulative, non-redeemable10% preference shares: N$50 000 (all the

preference shares were issued at N$1 per share).

• An issue of 500000 ordinary shares took place on 31 March 2024 at an issue

price of N$0,20 per share.

• There was no other movement in the equity accounts other than the movements

evident from the information provided above. There are no components of other

comprehensive income.

Required:

a) Prepare an extract from the statement of profit or loss of Glitch Limited for the year

ended 31 December 2024. (10 marks)

Page 3 of 5

|

|

4 Page 4 |

▲back to top |

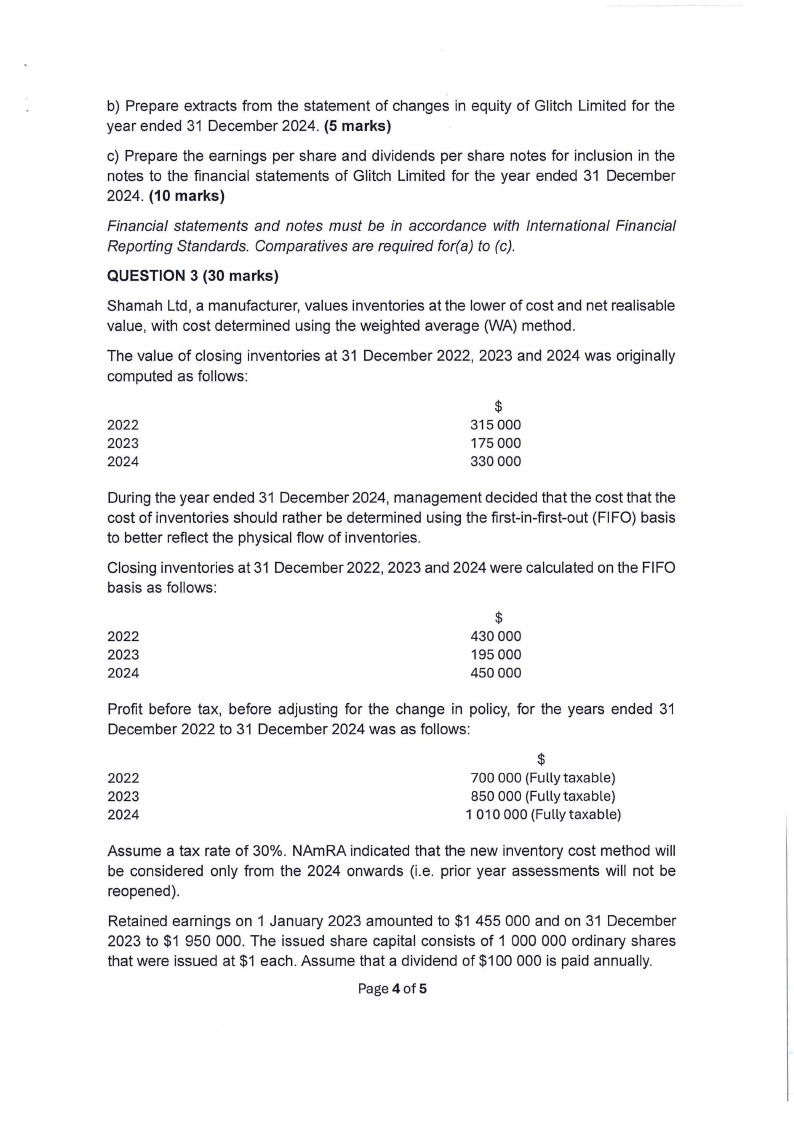

b) Prepare extracts from the statement of changes in equity of Glitch Limited for the

year ended 31 December 2024. (5 marks)

c) Prepare the earnings per share and dividends per share notes for inclusion in the

notes to the financial statements of Glitch Limited for the year ended 31 December

2024. (10 marks)

Financial statements and notes must be in accordance with International Financial

Reporting Standards. Comparatives are required for(a) to (c).

QUESTION 3 (30 marks)

Shamah Ltd, a manufacturer, values inventories at the lower of cost and net realisable

value, with cost determined using the weighted average (WA) method.

The value of closing inventories at 31 December 2022, 2023 and 2024 was originally

computed as follows:

2022

2023

2024

$

315 000

175 000

330 000

During the year ended 31 December 2024, management decided that the cost that the

cost of inventories should rather be determined using the first-in-first-out (FIFO) basis

to better reflect the physical flow of inventories.

Closing inventories at 31 December 2022, 2023 and 2024 were calculated on the FIFO

basis as follows:

2022

2023

2024

$

430 000

195 000

450 000

Profit before tax, before adjusting for the change in policy, for the years ended 31

December 2022 to 31 December 2024 was as follows:

2022

2023

2024

$

700 000 (Fully taxable)

850 000 (Fully taxable)

1 01 0 000 (Fully taxable)

Assume a tax rate of 30%. NAmRA indicated that the new inventory cost method will

be considered only from the 2024 onwards (i.e. prior year assessments will not be

reopened).

Retained earnings on 1 January 2023 amounted to $1 455 000 and on 31 December

2023 to $1 950 000. The issued share capital consists of 1 000 000 ordinary shares

that were issued at $1 each. Assume that a dividend of $100 000 is paid annually.

Page 4of 5

|

|

5 Page 5 |

▲back to top |

Required:

Disclose the above information in the statement of profit or loss and other

comprehensive income and statement of changes in equity of Shamah Ltd for the year

ended 31 December 2024. (30 marks)

QUESTION 4 (25 marks)

Smart Limited enters a contract with Property Limited for the lease of three floors of

an office building. The exact floors are specified in the contract and Property Limited

is not permitted to relocate tenants to other floors of the building.

The commencement date of the lease is July 2024 and the duration of the lease is for

five years with the option to extend for a further five years. Smart Limited is reasonably

certain to exercise the option to extend the lease.

The lease payments are N$50 000 per annum during the initial term and N$55 000

per annum during the optional term, all payable in advance.

Smart Limited incurred initial direct costs of N$20 000, comprising N$15 000 as

compensation to the tenant formerly occupying the three floors and N$5 000 as agents

commission. These are paid on 1 July 2024. Property Limited agrees to reimburse the

N$5 000 agents commission.

The interest rate implicit in the lease is not readably determinable. Smart Limited's

incremental borrowing rate is 5% per annum. The following present value table is

provided:

Present value annuity in advance of N$1 for years 1 to 5, discounted at 5%

Present value annuity in advance of N$1 for years 6 to 10, discounted at 5%

PV factor

4,5459

3,5619

Required:

a) Calculate the amount to record as the initial lease liability and the right of use

asset, explaining your answer. (15 marks)

b) Prepare the journal entries in the accounting records of Smart Limited for the

year ended 30 June 2025 and 30 June 2026. (10 marks)

Ignore tax.

Page 5 of 5